Automotive MRO Market Size, Share & Industry Analysis, By Service Type (Maintenance Services, Repair Services, Overhaul Services, Body & Cosmetic Services, & Diagnostics & Software), By Vehicle Type (Hatchback/Sedan, SUV, Light Duty Vehicle, & Heavy Duty Vehicle), By Service Provider (OEM Authorized Service Centers, Independent Workshops, Multi-brand Service Chains ), By Replacement Part Type (Engine Components, Transmission Components, Brake Components, Electrical & Electronic Components), By Vehicle Age (0–3 Years, 4–7 Years, 8–12 Years, & Above 12 Years), & Regional Forecast, 2026-2034

AUTOMOTIVE MRO MARKET SIZE AND FUTURE OUTLOOK

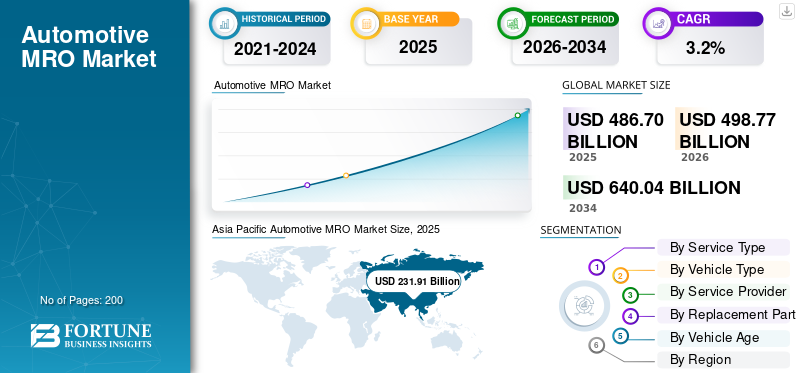

The global automotive MRO market size was valued at USD 486.70 billion in 2025. The market is projected to grow from USD 498.77 billion in 2026 to USD 640.04 billion by 2034, exhibiting a CAGR of 3.2% during the forecast period. Asia Pacific dominated the automotive MRO market with a market share of 47.65% in 2025.

The automotive MRO (Maintenance, Repair, and Overhaul) sector is involved in the inspection, servicing, repair, and replacement of vehicle components to ensure optimal performance, safety, and regulatory compliance. It includes spare parts, consumables, tools, equipment, and related services for passenger cars, light commercial vehicles, and heavy trucks. The market covers preventive maintenance, corrective repairs, diagnostics, bodywork, and overhaul activities across OEM-authorized and independent service networks.

Key drivers of the market include rising global vehicle parc, increasing average vehicle age, higher vehicle utilization, and growing demand for preventive maintenance. Technological complexity in modern vehicles, stricter emission and safety regulations, expanding aftermarket networks, and increasing road traffic accidents further contribute to the steady demand for repair and maintenance services.

Key players in the market include Bosch, 3M, Continental AG, Denso Corporation, ZF Friedrichshafen AG, Bridgestone Corporation, and LKQ Corporation. They compete through extensive aftermarket distribution networks, advanced diagnostic capabilities, high-quality spare parts, digital service platforms, predictive maintenance solutions, and strategic partnerships with OEMs and independent workshops to strengthen global presence and customer loyalty.

Download Free sample to learn more about this report.

AUTOMOTIVE MRO MARKET TRENDS

Shift toward Organized Aftermarket and Multi-Brand Service Networks to Drive the Market Growth

A prominent trend in the market is the growing shift from unorganized local garages to organized, multi-brand service networks. Consumers are increasingly prioritizing standardized service quality, genuine spare parts, warranty assurance, and transparent billing practices. Organized players leverage centralized procurement, digital inventory management, and trained technicians to deliver consistent service experiences across locations. Franchised workshops are expanding rapidly, particularly in emerging economies where vehicle ownership is rising. OEMs are also strengthening their authorized service networks beyond warranty periods to retain customers. This structural transformation enhances service reliability, improves brand trust, and increases formalization within the aftermarket ecosystem. Over time, the organized segment is expected to capture a larger revenue share, reshaping competitive dynamics in the MRO landscape.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expanding Vehicle Parc and Aging Fleet to Drive Aftermarket Service Demand

The steady expansion of the global vehicle parc, coupled with the rising average age of vehicles, is a primary factor driving automotive MRO market growth. As vehicles remain in operation for longer periods due to improved build quality and higher replacement costs, the frequency of maintenance, component replacement, and repair activities increases. Older vehicles typically require more frequent servicing, including brake systems, suspension parts, filters, batteries, and engine components. In developing economies, growing vehicle ownership further accelerates the demand for periodic maintenance and aftermarket parts. Additionally, higher vehicle utilization in ride-hailing, logistics, and fleet operations amplifies wear and tear, creating consistent service requirements. This expanding and aging fleet base ensures recurring revenue streams for MRO service providers, spare parts manufacturers, and independent workshops worldwide.

MARKET RESTRAINTS

High Cost of Advanced Components and Skilled Labor to Limit Profit Margins

One of the key restraints for the market is the rising cost of advanced vehicle components and skilled labor. Modern vehicles are increasingly equipped with ADAS, electronic control units, sensors, and hybrid or electric powertrain systems, making repairs more complex and expensive. Specialized diagnostic tools and certified technicians are required to service such systems, increasing operational costs for workshops. Smaller independent garages often struggle to invest in updated equipment and workforce training, limiting their ability to service technologically advanced vehicles. Moreover, fluctuations in raw material prices and supply chain disruptions can elevate spare part costs, impacting affordability for consumers. These factors may lead to deferred maintenance or a shift toward low-cost alternatives, thereby restraining overall market growth potential in price-sensitive regions.

MARKET OPPORTUNITIES

Digital Service Platforms and Predictive Maintenance to Unlock New Revenue Streams

The integration of digital platforms and predictive maintenance technologies presents significant growth opportunities in the automotive MRO market. Telematics, connected vehicle data, and AI-driven diagnostics enable real time monitoring of vehicle health, allowing service providers to anticipate failures before they occur. This proactive approach reduces the downtime for fleet operators and enhances customer satisfaction for individual vehicle owners. Mobile applications for service booking, digital inspection reports, and transparent pricing models further improve customer engagement and retention. Additionally, e-commerce platforms for aftermarket parts expand market reach beyond traditional distribution channels. As vehicles become increasingly connected, MRO providers can leverage data analytics to offer subscription-based maintenance packages and value-added services. Such digital transformation enhances operational efficiency while creating scalable and recurring revenue models.

- For instance, in July 2025, Bosch announced FleetME, a unified maintenance management solution that connects vehicle data/diagnostics with maintenance scheduling, supporting predictive, data-driven MRO models for fleets.

MARKET CHALLENGES

Counterfeit Parts Proliferation and Quality Assurance Concerns to Challenge Market Expansion

The widespread availability of counterfeit and substandard spare parts creates a major challenge for market players. Low-cost imitation components often attract price-sensitive customers but compromise vehicle safety, performance, and durability. The use of counterfeit parts can damage brand reputation for genuine manufacturers and create liability risks for service providers. In many developing markets, fragmented supply chains and limited regulatory enforcement make it difficult to monitor product authenticity. Additionally, customers may lack awareness regarding the long term risks associated with inferior components. Addressing this issue requires stronger quality control mechanisms, traceability systems, and collaboration between OEMs, distributors, and regulatory authorities. Ensuring part authenticity and maintaining service standards remain critical to sustaining consumer trust and long-term market stability.

Segmentation Analysis

By Service Type

Recurring Service Requirements to Strengthen the Dominance of the Maintenance Services Segment

Based on service type, the market is classified into maintenance services, repair services, overhaul services, body & cosmetic services, and diagnostics & software.

The maintenance services segment dominates the global automotive MRO market share due to mandatory periodic servicing requirements, including oil changes, filter replacements, brake inspections, tire rotation, and fluid checks. Rising vehicle parc and aging fleets increase routine service frequency, ensuring recurring workshop visits and steady revenue generation. Preventive maintenance awareness, warranty-linked servicing schedules, and fleet uptime optimization further reinforce the consistent demand across both OEM-authorized and independent service networks globally.

The diagnostics & software segment is projected to grow at a CAGR of 5% during the forecast period. Increasing vehicle electrification, ADAS integration, and connected systems require advanced diagnostic tools, ECU programming, and software updates, accelerating the demand for specialized digital servicing capabilities across modern workshops.

By Vehicle Type

Rising Ownership and Higher Component Replacement Rates to Cement SUV Segment Leadership

In terms of vehicle type, the market is categorized into hatchbacks/sedans, SUVs, light duty vehicles, and heavy duty vehicles.

The SUV segment dominates the market due to its strong global sales momentum and expanding vehicle parc across developed and emerging economies. SUVs typically incur higher maintenance and replacement costs owing to larger tires, robust suspension systems, advanced safety features, and higher engine capacities. The growing consumer preference for SUVs, particularly in North America, China, and Europe, sustains recurring servicing demand. Additionally, increased usage in urban and semi-urban regions contributes to steady wear and tear, reinforcing workshop footfall and spare parts consumption across authorized and independent service networks.

The hatchback/sedan segment is projected to grow at a CAGR of 3.1% over the forecast period. Despite market maturity in several regions, its extensive installed base and continued demand in cost-sensitive markets ensure consistent maintenance, repair, and replacement activity.

To know how our report can help streamline your business, Speak to Analyst

By Service Provider

Strong Consumer Trust and Warranty-Linked Servicing to Sustain OEM Authorized Service Center Segment Dominance

Based on service provider, the market is segmented into OEM authorized service centers, independent workshops, multi-brand service chains, and others.

The OEM authorized service centers segment dominate the market due to strong consumer trust, access to genuine spare parts, standardized service protocols, and manufacturer-backed warranties. Vehicles under warranty are typically serviced within authorized networks, ensuring consistent service inflow. These centers also possess advanced diagnostic tools, proprietary software access, and trained technicians capable of handling modern, technology-intensive vehicles. Additionally, OEMs increasingly offer extended warranty packages and service contracts, strengthening long-term customer retention. Their structured supply chains and quality assurance standards further reinforce leadership, particularly for newer vehicles and premium segments across developed and emerging markets.

The multi-brand service chains segment is projected to grow at a CAGR of 4.3% over the forecast period. Rapid network expansion, standardized pricing, digital booking platforms, and growing consumer preference for cost-effective yet reliable alternatives are accelerating their market penetration globally.

By Replacement Part Type

High Vehicle Performance Role to Bolster Engine Components Segment Leadership

Based on replacement part type, the market is segmented into engine components, transmission components, brake components, electrical & electronic components, and others.

The engine components segment dominates the market due to the engine’s central role in vehicle performance and longevity. Components such as filters, spark plugs, gaskets, belts, pistons, and fuel system parts require periodic replacement to maintain efficiency and comply with emission norms. Aging vehicle fleets and rising average mileage further increase engine-related servicing frequency. Additionally, preventive maintenance schedules strongly emphasize engine health checks, ensuring recurring demand across passenger and commercial vehicles. The high replacement rate and broad applicability across vehicle types reinforce the segment’s sustained revenue contribution within the global aftermarket ecosystem.

The electrical & electronic components segment is projected to grow at a CAGR of 4.2% over the forecast period. Increasing vehicle electrification, integration of sensors, ECUs, infotainment systems, and ADAS technologies are accelerating the demand for electronic module diagnostics, repair, and replacement across modern vehicles.

By Vehicle Age

High Vehicle Repair Frequency and Vehicle Retention for Longer Periods to Drive Above 12 Years Segment Dominance

Based on vehicle age, the market is segmented into 0–3 years, 4–7 years, 8–12 years, and above 12 years.

The above 12 years segment dominates the market as older vehicles require frequent repairs, part replacements, and major component servicing. With rising vehicle durability and higher new vehicle prices, owners are retaining vehicles for longer periods. Aging systems such as engine parts, suspension, braking systems, and electrical components experience higher wear and failure rates, increasing workshop visits. Additionally, older vehicles are typically out of warranty, shifting servicing to independent and cost-competitive networks. This high repair intensity and recurring component replacement cycle significantly elevate aftermarket revenue contribution from vehicles operating beyond twelve years of age.

The 8–12 years segment holds the second-largest automotive MRO market share. Vehicles in this age bracket transition out of extended warranty coverage and begin requiring higher-value repairs, including transmission servicing, suspension replacement, and electronic module maintenance, supporting steady aftermarket demand.

Automotive MRO Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive MRO Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is projected to witness the fastest growth over the forecast period. The region benefits from the world’s largest vehicle parc, particularly in China, India, and the Southeast Asia. Rising vehicle ownership, expanding middle-class population, and increasing average vehicle age support sustained maintenance demand. Rapid urbanization and strong two-wheeler and passenger vehicle penetration further accelerate servicing volumes. Additionally, the expansion of organized aftermarket networks and digital service platforms strengthens regional growth momentum.

China Automotive MRO Market

The Chinese market is estimated to touch around USD 139.09 billion in 2026, accounting for a significant share of global market revenues. Growth is driven by the world’s largest vehicle parc, aging fleets, expanding independent workshops, and rising preventive maintenance adoption.

India Automotive MRO Market

The India market is estimated to reach around USD 20.98 billion in 2026, accounting for a notable share of global market revenues. Rapid vehicle ownership growth, expanding two-wheeler and passenger car base, and increasing organized service penetration drive the fastest-growing demand.

Europe

Europe holds the second-largest share of the market and is expected to grow at a CAGR of 3.3% over the forecast period. The region’s growth is supported by an aging vehicle fleet, stringent emission regulations, and strong preventive maintenance culture. High penetration of advanced vehicles, including hybrids and electric cars, increases the demand for diagnostics and specialized repair services. Well-established independent workshop networks and structured aftermarket distribution channels further sustain steady revenue generation across Western and Central Europe.

Germany Automotive MRO Market

The Germany market is estimated to reach around USD 21.78 billion in 2026, accounting for a steady share of global market revenues. Aging vehicles, stringent emission norms, strong preventive servicing culture, and advanced diagnostics adoption support consistent aftermarket expansion.

U.K. Automotive MRO Market

The U.K. market is estimated to reach around USD 14.62 billion in 2026, accounting for a moderate share of global market revenues. Rising vehicle age, structured aftermarket networks, and increasing hybrid and EV servicing requirements sustain stable growth.

North America

North America represents the third-largest market, driven by a high average vehicle age and strong vehicle ownership rates in the U.S. and Canada. Increasing light truck and SUV penetration contributes to higher maintenance spending per vehicle. The presence of organized service chains, advanced diagnostic adoption, and strong DIY/ DIFM (Do-It-For-Me) culture supports consistent aftermarket activity. Fleet operations and commercial transportation further strengthen the demand for routine maintenance and replacement components.

U.S. Automotive MRO Market

The U.S. market is estimated to touch around USD 75.22 billion in 2026, accounting for a substantial share of global market revenues. High vehicle ownership, increasing light truck and SUV parc, aging fleet, and strong DIFM servicing culture drive demand.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, presents emerging growth opportunities in the market. Rising urbanization, improving road infrastructure, and gradual growth in vehicle ownership are supporting service demand. While informal workshops dominate in several countries, the increasing entry of organized service networks is improving service quality and spare parts availability. The growing awareness of preventive maintenance is expected to gradually strengthen market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Emphasize Strong Brand Recognition and Wide Distribution Networks to Secure an Edge over Competitors

The automotive MRO market is highly fragmented, characterized by the presence of global component manufacturers, OEM-authorized service networks, independent workshops, and emerging multi-brand service chains. Leading players compete through extensive distribution networks, strong brand recognition, and access to genuine spare parts. OEM-backed centers leverage proprietary diagnostic software and trained technicians, while independent operators compete primarily on pricing flexibility and localized service offerings. Strategic partnerships, acquisitions, and network expansion remain key competitive strategies to strengthen regional penetration and customer retention.

Competition is increasingly shaped by digital integration, service standardization, and technological capability. Market participants are investing in advanced diagnostic tools, predictive maintenance platforms, and inventory management systems to enhance operational efficiency. Multi-brand chains are expanding through franchise models, offering transparent pricing and service warranties to attract cost-conscious customers. Meanwhile, component manufacturers are strengthening e-commerce channels and direct-to-workshop distribution models. As vehicles become more software-driven and electronically complex, technical expertise and access to updated repair data are becoming critical differentiators.

LIST OF KEY AUTOMOTIVE MRO COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Denso Corporation (Japan)

- ZF Friedrichshafen AG (Germany)

- Continental AG (Germany)

- 3M Company (U.S.)

- Bridgestone Corporation (Japan)

- Michelin Group (France)

- LKQ Corporation (U.S.)

- BorgWarner Inc. (U.S.)

- Valeo SA (France)

- Schaeffler AG (Germany)

- Tenneco Inc. (U.S.)

- Aisin Corporation (Japan)

- Mahle GmbH (Germany)

- Hitachi Astemo Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Bosch Mobility Aftermarket continued to publish new regional product and diagnostic updates across Europe via its aftermarket news channels. The updates included expanded parts coverage, enhanced diagnostic software capabilities, and service data improvements. These would support workshops in maintaining compatibility with evolving vehicle technologies and strengthening Bosch’s aftermarket footprint across European markets.

- January 2026: Hunter Engineering signed a partnership with RockED, a people development platform, for providing targeted microlearning designed to service advisors. This would support a more consistent vehicle service experience and help strengthen their customer communication. Set to be delivered through RockED’s mobile learning platform, the training program would be available for enrollment via Hunter University, Hunter’s global learning platform for technicians, customers, students, and instructors.

- October 2025: Hunter Engineering introduced the new Road Force WalkAway wheel balancer, which can bring up to 45% reduction in door-to-door four-tire changeover times. The key component for the dramatic timesaving is the WalkAway Inflation System, which automatically releases the inflation chuck when inflation is completed, allowing the machine to then perform the balance spin. This greatly reduces the time spent inflating assemblies on the tire changer.

- September 2025: Toyota and Lexus issued approval for Hunter’s Ultimate ADAS alignment and calibration system, expanding OEM compatibility. The approval strengthened Hunter’s credibility within authorized service networks, enabling OEM dealerships and independent workshops to perform OEM-compliant ADAS calibrations and alignments for a wider range of vehicle models.

- August 2025: Bosch announced expansion initiatives for its mobility solutions with strategic goals tied to Software-Hardware integration post-CES. The strategy focused on integrating advanced software platforms with hardware diagnostics, enabling connected workshop ecosystems, predictive maintenance capabilities, and improved operational efficiency across the automotive aftermarket value chain.

- July 2025: Hunter Engineering announced the HawkEye Elite Xpandable alignment and ADAS solution for broader shop integration. The system enables scalable alignment and calibration functionality, allowing workshops to integrate ADAS services seamlessly, improve workflow efficiency, and accommodate increasing demand for precise vehicle alignment and advanced safety system calibration.

- May 2025: Bosch introduced 82 new aftermarket part numbers, covering nearly 63 million vehicles in operation worldwide. The expansion enhanced coverage across braking, engine management, and filtration categories, reinforcing Bosch’s commitment to strengthening global aftermarket supply while supporting repair shops with broader, vehicle-specific replacement solutions.

REPORT COVERAGE

The global automotive MRO market analysis provides an in-depth study of market size and forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service Type, By Vehicle Type, By Service Provider, By Replacement Part Type, By Vehicle Age, and By Region |

| By Service Type |

|

| By Vehicle Type |

|

| By Service Provider |

|

| By Replacement Part Type |

|

| By Vehicle Age |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 486.70 billion in 2025 and is projected to reach USD 640.04 billion by 2034.

In 2025, the market value stood at USD 231.91 billion.

The market is expected to exhibit a CAGR of 3.2% during the forecast period of 2026-2034.

The SUV segment leads the market by vehicle type.

Expanding vehicle parc and aging fleet are key factors driving the market growth.

Asia Pacific dominates the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us