Automotive Digital Aftermarket Service Market Size, Share & Industry Analysis, By Service Type (Digital Diagnostics & Remote Monitoring Services, Software & OTA-Enabled Aftermarket Services, Digital Repair & Maintenance Management Services, Digital Parts & E-Commerce Services, and Fleet & Commercial Digital Aftermarket Services), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Provider Type (OEM-Owned Digital Aftermarket Services, Authorized Dealer-Led Digital Services, Independent Aftermarket Digital Platforms, Fleet & Telematics Service Providers), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

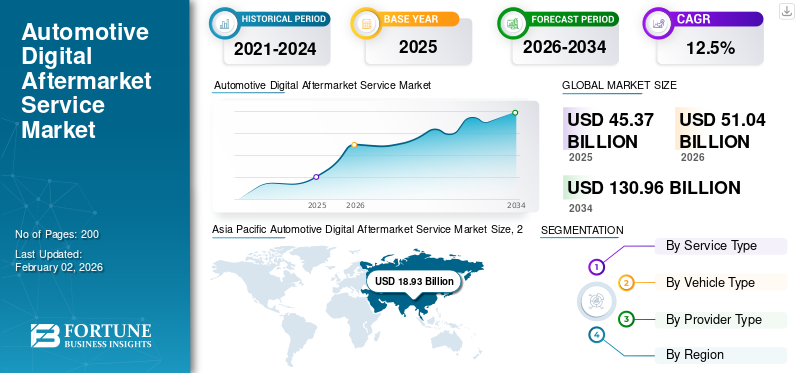

The global automotive digital aftermarket service market size was valued at USD 45.37 billion in 2025. The market is projected to grow from USD 51.04 billion in 2026 to USD 130.96 billion by 2034, exhibiting a CAGR of 12.5% during the forecast period. Asia Pacific dominated the global market with a market share of 41.72% in 2025.

The service demand is expanding steadily as automakers, fleets, and independent service networks increasingly monetize the vehicle lifecycle. This is made possible through connected diagnostics, remote monitoring, OTA software updates, subscription-based features, digital service booking/workshop platforms, and parts e-commerce enablement. The market’s growth is driven by the rising installed base of connected vehicles, increasing Software-Defined Vehicle (SDV) strategies, and stronger demand for predictive maintenance and uptime, especially in commercial fleets. Rapid EV adoption further accelerates OTA and software-service monetization.

Major providers such as Bosch, Continental, ZF, DENSO, Aptiv, HARMAN, Geotab, Verizon Connect, Trimble, and other OEM and independent digital platforms are strengthening competitiveness. Some factors contributing to this are connected diagnostics ecosystems, OTA capability expansion, cloud/AI analytics, and integrated service/parts digitalization, improving service efficiency, customer retention, and recurring revenue capture across the global aftermarket.

Download Free sample to learn more about this report.

Automotive Digital Aftermarket Service Market Trends

Software-Defined Vehicles Accelerate Digital Aftermarket Transformation

The transition toward Software-Defined Vehicles (SDVs) is reshaping the automotive aftermarket industry by shifting value creation from hardware-centric repairs to software-enabled services delivered throughout the vehicle lifecycle. Vehicles increasingly rely on centralized computing, embedded connectivity, and cloud integration, enabling continuous diagnostics, feature upgrades, and service personalization after sale. This trend supports recurring revenue through OTA updates, digital subscriptions, remote diagnostics, and app-based service ecosystems. As vehicle software content grows, digital aftermarket services become integral to maintaining performance, compliance, and user experience, particularly for EVs and premium vehicles, where functionality is closely tied to software reliability and updates.

- In October 2024, Ford highlighted software-enabled and subscription-based services as a core pillar of its Ford Pro platform, supporting connected diagnostics, OTA updates, and fleet intelligence monetization.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Connected Vehicle Parc Drives Post-Sale Digital Monetization

The growing global installed base of connected vehicles is a primary driver supporting the expansion of automotive digital aftermarket services. Connectivity enables continuous data flow between vehicles, OEMs, service providers, and cloud platforms, allowing predictive maintenance, remote diagnostics, digital service scheduling, and OTA feature activation. As more vehicles are sold with embedded telematics and connectivity hardware, the addressable market for digital services expands beyond new vehicle sales into long-term aftermarket engagement. This driver is particularly strong in regions with high connectivity penetration and EV adoption, where software updates and remote services are essential for vehicle operation, safety, and customer satisfaction.

- In April 2024, the International Energy Agency confirmed that China, Europe, and the U.S. accounted for around 95% of global electric car sales, underscoring the rapid expansion of software and connectivity intensive vehicle fleets.

MARKET RESTRAINTS

Data Privacy and Cybersecurity Concerns Limit Digital Service Adoption

Rising concerns about vehicle data ownership, cybersecurity risks, and regulatory compliance are key restraints. Digital services rely on continuous data collection, cloud storage, and remote access, which increases their exposure to cyber threats and unauthorized data usage. Stricter data protection regulations and varying regional compliance requirements add complexity and increase costs for service providers, particularly independent platforms that operate across borders. These concerns can slow consumer behaviors, consumer acceptance, limit data-sharing partnerships, and increase investment requirements for secure digital infrastructure, especially for services involving remote vehicle control or OTA software deployment.

- In January 2024, the European Union reinforced vehicle cybersecurity and software update requirements under UNECE regulations, increasing compliance obligations for connected and OTA-enabled automotive services.

MARKET OPPORTUNITIES

Fleet Digitalization Creates High-Value Aftermarket Revenue Opportunities

The rapid digitalization of commercial vehicle fleets presents a significant growth opportunity for automotive digital aftermarket service. Fleet operators increasingly adopt telematics, predictive maintenance, uptime management platforms, and digital service contracts to reduce operating costs and improve vehicle availability. These services typically generate higher recurring revenue per vehicle than consumer-focused offerings and are often sold through long-term contracts. Growth in e-commerce, urban logistics, shared mobility, and cross-border transportation further amplifies demand for fleet-focused digital aftermarket solutions, particularly in emerging markets where fleet optimization delivers immediate economic benefits.

- In October 2024, Ford reported approximately 630,000 paid Ford Pro Intelligence subscriptions, reflecting strong uptake of fleet-focused digital diagnostics and software services.

MARKET CHALLENGES

Fragmented Aftermarket Ecosystem Challenges Scalable Digital Integration

The global market remains highly fragmented, with OEMs, authorized dealers, independent workshops, independent repair shops, fleet operators, and digital platforms operating across diverse systems and standards. This fragmentation complicates data integration, interoperability, and consistent service delivery across vehicle brands and regions. Independent service providers often lack access to OEM-level data, while OEMs seek to retain control over digital interfaces and customer relationships. These structural challenges slow ecosystem-wide digital adoption, limit the scalability of multi-brand platforms, and increase integration costs, particularly in regions with diverse regulatory and technological maturity levels.

- In March 2024, the European Automobile Manufacturers’ Association reiterated the importance of balanced access to in-vehicle data to ensure fair competition between OEMs and independent service providers.

Segmentation Analysis

By Service Type

Rising Adoption of Predictive Maintenance Increases Demand for Digital Diagnostics & Remote Monitoring Services

Based on service type, the market is sub-segmented into digital diagnostics & remote monitoring services, software & OTA-enabled aftermarket services, digital repair & maintenance management services, digital parts & e-commerce services, and fleet & commercial digital aftermarket services.

Digital diagnostics & remote monitoring services dominate due to their critical role in real-time vehicle health monitoring, fault detection, and predictive maintenance across passenger and commercial vehicle ages. OEMs, fleets, and workshops widely adopt these services to reduce downtime, improve service accuracy, and optimize lifecycle costs. Their applicability across ICE and electric vehicles supports consistent revenue generation.

Software & OTA-enabled aftermarket services are projected to grow at a CAGR of 14.7% over the forecast period, driven by the increasing adoption of software-defined vehicle architectures.

- In October 2024, Ford highlighted large-scale adoption of connected diagnostics and monitoring through its Ford Pro Intelligence platform for commercial fleets.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

SUV Proliferation and Connectivity Expansion Drive Vehicle-Type Leadership

Based on vehicle type, the market is sub-divided into hatchback/sedan, SUV, LCV, and HCV.

SUVs represent both the dominant and fastest-growing vehicle type segment, supported by higher electronic content, advanced infotainment systems, ADAS features, and a greater consumer willingness to pay for digital services. SUVs increasingly integrate connected diagnostics, OTA updates, and digital service platforms as standard offerings, resulting in higher per-vehicle digital aftermarket spend. Their growing penetration across developed and emerging markets further reinforces segment dominance. The SUV segment is projected to grow at a CAGR of 13.4% over the forecast period, outperforming other vehicle types.

Hatchbacks and sedans remain the second-largest segment globally, supported by their large installed base and longer vehicle lifecycles. Demand for digital diagnostics, service booking platforms, and OTA updates sustains steady growth, particularly in cost-sensitive and high-volume markets.

- In May 2024, the International Energy Agency reported that SUVs accounted for more than half of global passenger car sales, reinforcing their growing software and connectivity footprint.

By Provider Type

OEM-Controlled Digital Ecosystems Consolidate Aftermarket Leadership Owing to Direct Control

Based on provider type, the market is classified into OEM-owned digital aftermarket services, authorized dealer-led digital services, independent aftermarket digital platforms, and fleet & telematics service providers.

OEM-owned digital aftermarket services dominate due to direct control over vehicle software architectures, embedded connectivity, OTA pipelines, and customer interfaces. OEMs are increasingly monetizing post-sale services through subscriptions, feature activation, and remote diagnostics, thereby strengthening long-term customer retention and generating recurring revenue. Tight integration with vehicle systems limits the ability to substitute third-party components.

Fleet & telematics service providers are projected to grow at a CAGR of 13.7% over the forecast period, supported by the expansion of commercial fleet digitalization and data-driven maintenance strategies.

- In February 2024, General Motors reaffirmed that software-enabled services and subscriptions, including OnStar, will continue to be a core component of its long-term revenue strategy.

Automotive Digital Aftermarket Service Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

Asia Pacific Automotive Digital Aftermarket Service Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America exhibits strong growth, driven by high connected-vehicle penetration, early adoption of software-defined vehicle architectures, and a mature digital service ecosystem. OEM-led subscriptions, OTA updates, and advanced diagnostics are widely adopted, while commercial fleets increasingly rely on telematics, predictive maintenance, and uptime platforms. High internet penetration, strong regulatory clarity, and large fleet operators accelerate the process of monetization. Growth is further supported by increasing EV adoption, which raises demand for software updates, remote monitoring, and digital service management across both passenger and commercial vehicles.

U.S.

The U.S. leads regional growth due to high connected-vehicle penetration, strong OEM subscription strategies, and widespread adoption of digital fleet management. EV adoption and large commercial fleets significantly boost demand for OTA services, diagnostics, and telematics-driven aftermarket platforms.

Europe

A large vehicle parc, strong regulatory focus on vehicle safety and software compliance, and rapid EV adoption support Europe’s automotive digital aftermarket growth. OEM-owned digital platforms and OTA-enabled services are expanding steadily, while fleet operators increasingly adopt predictive maintenance and digital service contracts. Although vehicle sales growth is moderate, high per-vehicle digital spend sustains market expansion. Data protection regulations shape service design, but also encourage the development of standardized, secure digital aftermarket ecosystems across major European automotive markets.

U.K.

The U.K. market benefits from high connectivity levels, strong adoption of digital service booking and diagnostics platforms, and a growing EV parc, supporting demand for OTA updates, remote monitoring, and subscription-based aftermarket services.

Germany

Germany drives Europe’s digital aftermarket through premium vehicles, software-intensive platforms, and OEM-led OTA strategies. Strong EV penetration and advanced manufacturing ecosystems support high-value digital diagnostics, feature activation, and lifecycle service monetization.

Asia Pacific

Asia Pacific dominates global growth due to its massive vehicle base, leadership in EV production and adoption, and rapid expansion of connected and software-defined vehicles. China, Japan, and India collectively drive demand for OTA services, digital diagnostics, and app-based maintenance platforms. Rising smartphone usage, improving internet infrastructure, and government support for smart mobility further accelerate adoption. While per-vehicle digital spend varies widely, the region’s scale ensures the highest absolute revenue growth globally.

China

China leads global growth with the world’s largest EV and connected-vehicle fleet. Strong OEM software monetization, OTA updates, and app-based service ecosystems drive high adoption of digital aftermarket services across passenger and commercial vehicles.

Japan

Advanced vehicle electronics, robust OEM platforms, and the adoption of high-quality diagnostics are driving Japan’s growth. Digital aftermarket services focus on reliability, predictive maintenance, and gradual OTA expansion across hybrid and connected vehicle fleets.

India

India exhibits rapid growth from a low base, supported by a rising vehicle parc, expanding internet access, and an increasing use of digital service booking, diagnostics, and fleet platforms, particularly in SUVs and last-mile commercial vehicles.

Rest of the World

The rest of the world segment will experience the fastest growth rate as connectivity improves and digital aftermarket adoption accelerates from a low base. Latin America/South America and the Middle East & Africa are increasingly adopting fleet telematics, diagnostics, and digital parts platforms to control operating costs. While passenger vehicle digital penetration remains uneven, heavy commercial vehicles and logistics fleets drive early monetization, as infrastructure investments and smartphone adoption support the long-term expansion of digital aftermarket services.

COMPETITIVE LANDSCAPE

Key Industry Players

Connected Platforms, Software Monetization, and Ecosystem Partnerships Define Digital Aftermarket Competition

The rapid expansion of connected diagnostics, OTA-enabled software services, and data-driven lifecycle management solutions shapes the global market trends. Leading aftermarket players, including Bosch, Continental, ZF, DENSO, Aptiv, HARMAN, Geotab, Verizon Connect, and Trimble, compete through scalable telematics platforms, predictive maintenance analytics, cloud-based service ecosystems, and subscription-driven business models. OEMs strengthen competitiveness by retaining control over vehicle data, expanding OTA capabilities, and integrating digital services into proprietary apps, while independent platforms focus on multi-brand compatibility and cost efficiency. Companies increasingly form strategic partnerships with cloud providers, AI analytics firms, and mobility operators to enhance service intelligence, improve uptime management, and unlock recurring aftermarket revenue streams across passenger and commercial vehicles.

LIST OF KEY AUTOMOTIVE DIGITAL AFTERMARKET SERVICE COMPANIES PROFILED

- Bosch (Germany)

- Continental (Germany)

- ZF Friedrichshafen (Germany)

- DENSO (Japan)

- Aptiv (Ireland)

- HARMAN (U.S.)

- Visteon (U.S.)

- NXP Semiconductors (Netherlands)

- Geotab (Canada)

- Verizon Connect (U.S.)

- Trimble (U.S.)

- ACTIA Group (France)

- TomTom (Netherlands)

- Carly Solutions (Germany)

- Snap-on (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Kinetic Engineering has formalized a strategic technology partnership with Jio Things Limited to integrate advanced digital features into all upcoming electric vehicle models. The collaboration will introduce voice-assisted controls, IoT-powered smart clusters, and connected vehicle technologies, positioning the company as one of India's first to offer mass-market voice-assisted connected EV scooters and strengthening the transition to intelligent electric mobility. Jio Things offers a unified ecosystem comprising edge devices, connectivity, cloud infrastructure, remote device management, installation support, and aftermarket services.

- November 2025: Autorox and Bosch announced partnership to empower over 25,000 independent repairers and parts sellers worldwide digitally, expanding Bosch Mobility Platform distribution and Autorox digital tools for scheduling, procurement, and predictive analytics, targeting 100 million yearly vehicle services to improve workshop efficiency and connected service delivery.

- October 2025: HARMAN invested around USD 30 million to expand its automotive electronics facility in Pune, boosting telematics, connectivity units, and advanced automotive electronics production. This enhancement is expected to increase India’s role in connected mobility, increase capacity for four million infotainment units and 0.8 million telematics units annually, and create new jobs.

- July 2025: L&T Technology Services and ThyssenKrupp formed a strategic partnership to establish a new automotive software development center in Pune, India, focused on connected vehicle systems, ADAS, OTA updates, cybersecurity, and software-defined mobility innovations for next-generation vehicles.

- March 2025: myTVS, a leading player in the Indian automotive aftermarket space, showcased its latest innovation, TVS Astra, an integrated solution designed to revolutionize fleet management and automotive services.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Market Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type, Vehicle Type, Provider Type, and Region |

|

By Service Type |

· Digital Diagnostics & Remote Monitoring Services · Software & OTA-Enabled Aftermarket Services · Digital Repair & Maintenance Management Services · Digital Parts & E-Commerce Services · Fleet & Commercial Digital Aftermarket Services |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · LCV · HCV |

|

By Provider Type |

· OEM-Owned Digital Aftermarket Services · Authorized Dealer-Led Digital Services · Independent Aftermarket Digital Platforms · Fleet & Telematics Service Providers |

|

By Geography |

· North America (By Service Type, Vehicle Type, Provider Type, and Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Service Type, Vehicle Type, Provider Type, and Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Service Type, Vehicle Type, Provider Type, and Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Service Type, Vehicle Type, and Provider Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 45.37 billion in 2025 and is projected to reach USD 130.96 billion by 2034.

In 2025, Asia Pacifics market value stood at USD 18.93 billion.

The market is expected to grow at a CAGR of 12.5% during the forecast period.

The SUV segment led the market share by vehicle type.

Expanding connected vehicle parc drives post-sale digital monetization.

Top players in the market include Bosch, Continental, ZF, DENSO, Aptiv, HARMAN, and Geotab.

Asia Pacific accounted for the largest share of the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us