Automotive Multi-Link Suspension Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Component (Control Arms, Bushings, Ball Joints & Spherical Joints, Knuckles/Wheel Carriers, and Fasteners & Mounting Hardware), By Axle Fitment (Rear Multi-Link and Front Multi-Link), By Material of Links (Iron, Steel, Aluminum, and Composite), By Propulsion (ICE and Electric), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

Automotive Multi-Link Suspension Market Size and Future Outlook

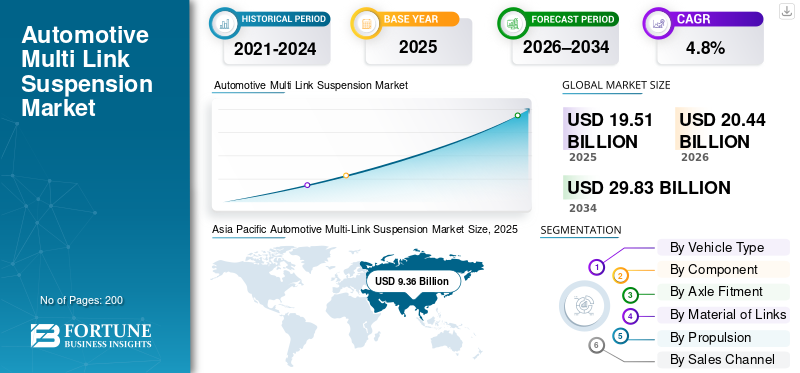

The global automotive multi-link suspension market size was valued at USD 19.51 billion in 2025. The market is projected to grow from USD 20.44 billion in 2026 to USD 29.83 billion by 2034, exhibiting a CAGR of 4.8% during the forecast period. Asia Pacific dominated the Automotive multi link suspension market with a market share of 6.97% in 2025.

The global automotive multi-link suspension market represents the segment of the global automotive suspension market focused on advanced independent suspension architectures that use multiple links to control wheel movement. These systems are primarily adopted in passenger cars, SUVs, and premium passenger vehicle platforms where ride comfort, handling stability, and vehicle dynamics are critical. Multi-link systems are designed to better manage vehicle weight, improve cornering behavior, and reduce noise and vibration compared to simpler suspension layouts.

Market growth is supported by rising demand for improved ride quality, increasing vehicle sales, and changing consumer preferences toward comfort-oriented and performance-focused vehicles. As automakers introduce heavier platforms due to electrification and safety requirements, the need for precise wheel control has increased, making multi-link systems more relevant during the forecast period. While shock absorbers and springs remain separate suspension components, multi-link architectures provide the structural foundation that enables compatibility with electronically controlled, semi active, and active suspension technologies.

Applications of multi-link suspension systems span mid-size sedans, premium SUVs, and selected light commercial vehicles where ride stability is prioritized. Growth is also supported by modular vehicle platforms, which allow automakers to deploy similar suspension designs across multiple models while maintaining cost effectiveness.

The market size is expected to expand steadily as OEMs balance performance requirements with manufacturing efficiency. The adoption of active suspension systems is expected to further increase the relevance of multi-link designs as a base architecture.

Leading suppliers such as Continental AG, ZF, and other global Tier-1 manufacturers are investing in lightweight materials, integrated control arm designs, and scalable chassis solutions to strengthen their competitive position.

Download Free sample to learn more about this report.

AUTOMOTIVE MULTI-LINK SUSPENSION MARKET TRENDS

Lightweight Material Adoption in Multi-Link Systems is a Key Market Trend

Manufacturers are increasingly adopting aluminum and high-strength steel links to reduce vehicle weight while maintaining strength. This trend supports fuel efficiency and EV range while preserving ride quality, making multi-link systems more attractive across the global automotive suspension industry.

For instance, ZF has highlighted lightweight chassis components as a key development focus in recent annual reports.

MARKET DYNAMICS

MARKET DRIVERS

Rising Passenger Vehicle Comfort Expectations Accelerate Adoption

Growing emphasis on comfort and handling in passenger cars is driving the adoption of multi-link suspension systems. As consumer preferences shift toward smoother ride quality and better road isolation, automakers increasingly favor multi-link designs over simpler layouts. The system’s ability to manage higher vehicle weight and integrate with advanced chassis electronics further supports automotive multi-link suspension market growth during the forecast period.

- For instance, European OEMs have increased rear multi-link adoption to meet ride quality expectations, particularly in premium passenger vehicles.

MARKET RESTRAINTS

Higher Cost Compared to Conventional Suspension Systems to Restrain Market Growth

Multi-link suspension systems involve more suspension components, higher material usage, and complex assembly, increasing costs compared to torsion beam or strut systems. This limits adoption in entry-level vehicles and price-sensitive markets. OEMs focused on affordability may continue to use simpler architectures, restricting penetration in lower-cost passenger vehicle segments.

- For instance, OEM cost-optimization strategies continue to favor torsion beam suspensions in entry-level vehicles to maintain pricing competitiveness.

MARKET OPPORTUNITIES

Integration with Semi-Active and Active Suspension Technologies to Offer Growth Opportunities

The growing adoption of semi active and active suspension technologies creates opportunities for multi-link architectures. These systems require precise wheel control; which multi-link designs inherently provide. As electronically controlled suspensions expand in premium and electric vehicles, demand for compatible multi-link systems is expected to rise significantly.

- For instance, Continental AG continues to develop suspension solutions compatible with electronically controlled chassis systems.

MARKET CHALLENGES

Balancing Performance Gains with Cost Effectiveness Emerges a Market Challenge

Achieving performance improvements without significantly increasing system costs remains a challenge. Multi-link suspension requires careful engineering to ensure durability and manufacturability. Suppliers must balance advanced design with cost effectiveness to maintain competitiveness across diverse vehicle segments.

- For instance, Automotive suppliers continue optimizing suspension architectures to meet OEM cost and performance targets.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

To know how our report can help streamline your business, Speak to Analyst

On the basis of vehicle type, the market is divided into Hatchback/Sedan, SUV, LCV and HCV.

Hatchbacks/sedan segment dominate the market due to their large global base of passenger cars and consistent use of rear multi-link suspension for comfort and stability. Automakers increasingly deploy multi-link systems in mid-size sedans to meet ride-quality expectations while managing vehicle weight and handling performance. High production volumes ensure steady OEM and aftermarket demand.

- For instance, ACEA highlights widespread use of independent rear suspension in European passenger cars.

SUVs segment is expected to grow at a CAGR of 5.9% over the forecast period.

By Component

Multiple Arms Per Axle, Continuous Stress, and Durability-Weight Optimization Drives Control Arms Segment Growth

On the basis of component, the market is segmented into control arms, bushings, ball joints & spherical joints, knuckles/wheel carriers, and fasteners & mounting hardware.

The control arms segment dominates as multi-link systems rely on multiple arms per axle, increasing material usage and replacement demand. Control arms experience continuous mechanical stress, driving higher aftermarket consumption. Ongoing efforts to balance strength, durability, and weight further support value growth within this component category across vehicle platforms.

- For instance, Lemförder supplies multi-link control arms across multiple global OEM platforms.

Bushings segment is expected to grow at a CAGR of 5.5% over the forecast period.

By Axle Fitment

Widespread Rear Axle Adoption for Ride Comfort and Handling Stability Boosts Rear Multi-Link Segment Growth

On the basis of axle fitment, the market is segmented into rear multi-link and front multi-link.

Rear multi-link segment dominates due to higher penetration across both mass-market and premium vehicles. The rear axle benefits most from multi-link geometry, improving ride comfort, handling stability, and noise isolation. This configuration is widely adopted in passenger vehicles, making it the largest contributor to overall market value.

- For instance, OICA production data reflects high rear independent suspension adoption in passenger vehicles.

Front multi-link segment is expected to grow at a CAGR of 5.2% over the forecast period.

By Material of Links

Strength, Durability, Cost Efficiency, and Long Service Life Preference Drives Steel Segment Growth

On the basis of material of links, the market is segmented into iron, steel, aluminum and composite.

Steel dominates due to its balance of strength, durability, and cost effectiveness, particularly in high-volume applications. While aluminum adoption is increasing, steel remains preferred for load-bearing links in vehicles requiring long service life. Its established supply chain supports consistent usage across regions and vehicle segments.

- For instance, in October 2025, World Bank materials outlook highlighted steel’s continued relevance in automotive manufacturing.

Composite segment is expected to grow at a CAGR of 6.9% over the forecast period.

By Propulsion

ICE Vehicles Continue to Anchor Demand

On the basis of propulsion, the market is segmented into ICE and Electric.

ICE vehicles dominate as they account for the majority of global vehicle sales, sustaining demand for conventional multi-link suspension architectures. Despite growth in electric vehicles, ICE-powered passenger vehicles continue to represent the largest installed base, supporting consistent OEM production and aftermarket replacement volumes.

- For instance, IEA reports ICE vehicles still form the majority of global vehicle stock.

Electric segment is expected to grow at a CAGR of 9.4% over the forecast period.

By Sales Channel

Aftermarket Segment Dominates Due to Wear-related Replacements, Aging Fleets, and Recurring Multi-Link Maintenance

On the basis of sales channel, the market is segmented into OEM and aftermarket.

The aftermarket segment dominates due to wear-related replacement of suspension links, bushings, and joints over extended vehicle lifespans. Aging fleets and increasing emphasis on ride quality sustain aftermarket demand.

Link systems require periodic maintenance, supporting recurring sales beyond initial OEM installation.

- For instance, in January 2025, ACEA noted in a report Europe’s aging vehicle fleet supports aftermarket component demand.

Aftermarket segment is expected to grow at a CAGR of 6.0% over the forecast period.

Automotive Multi-Link Suspension Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific Automotive Multi-Link Suspension Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant automotive multi-link suspension market share in 2025, valued at USD 9.36 billion, and also maintained the leading share in 2024, with USD 8.94 billion. This growth is driven by high passenger vehicle production, strong vehicle sales, and growing demand for comfort-oriented suspension systems. China, Japan, and South Korea contribute significant OEM volumes, while India supports long-term growth through rising passenger car adoption. Increasing use of independent suspension systems across regional platforms further strengthens market leadership.

- For instance, in 2024, IBEF reported that the Asia Pacific leads global vehicle production, supporting large-scale adoption of digital instrument clusters across mass-market and premium vehicles.

China Automotive Multi-Link Suspension Market

China’s automotive multi-link suspension market is projected to be one of the largest worldwide, with 2025 revenues valued at USD 5.15 billion, representing roughly 26.4% of global automotive multi-link suspension market.

India Automotive Multi-Link Suspension Market

India automotive multi-link suspension market in 2025 was valued at USD 1.12 billion, accounting for roughly 5.8% of global automotive multi-link suspension revenues.

Europe

Europe recorded a valuation of USD 4.49 billion in 2025 and secured the position of the second largest region in the market. The region shows stable growth driven by premium passenger cars and early adoption of advanced suspension architectures. Higher expectations for ride quality and handling continue to support multi-link penetration across mid-size and luxury vehicles.

Germany Automotive Multi-Link Suspension Market

Germany automotive multi-link suspension market in 2025 was valued at USD 1.26 billion, accounting for roughly 6.4% of global automotive multi-link suspension revenues.

U.K. Automotive Multi-Link Suspension Market

U.K. automotive multi-link suspension market in 2025 reached a valuation of USD 0.54 billion, accounting for roughly 2.8% of global automotive multi-link suspension revenues.

North America

North America is projected to record a growth rate of 4.7% in the coming years, which is the third highest among all regions, and reach a valuation of USD 4.08 billion by 2026. The region is expected to grow steadily, supported by high SUV penetration and greater suspension content per vehicle. Automakers increasingly prioritize ride comfort and handling, sustaining demand for multi-link systems. The U.S. market benefits from strong aftermarket activity and continued preference for larger vehicles.

U.S. Automotive Multi-Link Suspension Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.24 billion, representing roughly 14.0% of global automotive multi-link suspension market.

Rest of the World

Growth in the rest of the world is driven by gradual vehicle platform upgrades and improving road infrastructure. As manufacturers introduce higher-specification passenger vehicles, adoption of multi-link suspension systems increases steadily.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovation and Technology-Driven Competition Strengthen the Market Position

The competitive landscape of the global automotive multi-link suspension market is shaped by global Tier-1 suppliers with strong engineering depth, long-standing OEM relationships, and broad manufacturing footprints. These companies compete primarily on system-level integration, durability, and the ability to support multiple vehicle platforms across regions. As multi-link suspension systems involve several interconnected suspension components, suppliers with in-house design, testing, and validation capabilities hold a clear advantage.

Leading players focus on modular suspension architectures that allow automakers to deploy similar designs across different passenger cars, SUVs, and selected light commercial vehicles, while maintaining differentiation through tuning and material selection. This approach improves scalability and supports cost effectiveness over the vehicle lifecycle. Increasing vehicle electrification and higher vehicle weight are also pushing suppliers to redesign links and joints to handle higher loads without compromising comfort.

Strategic investments in lightweight materials, optimized control arm geometry, and compatibility with electronically controlled chassis functions are key competitive priorities. Suppliers are also aligning multi-link designs with semi active and active suspension requirements, ensuring their systems can serve as base architectures for advanced ride-control technologies.

Geographic expansion remains important, particularly in the Asia Pacific, where suppliers are strengthening local production and engineering capabilities to support high-volume passenger vehicle programs. At the same time, aftermarket presence is being enhanced through broader product catalogs and distribution networks, supporting recurring revenue beyond OEM supply.

- For instance, in September 2023, ZF strengthened its chassis portfolio by expanding integrated suspension system offerings for global passenger vehicle platforms.

LIST OF KEY AUTOMOTIVE MULTI-LINK SUSPENSION COMPANIES PROFILED

- ZF Friedrichshafen AG (Germany)

- Continental AG (Germany)

- Benteler Automotive (Germany)

- Magna International (Canada)

- KYB Corporation (Japan)

- Mando Corporation (South Korea)

- Thyssenkrupp Automotive (Germany)

- Bosch (Germany)

- Tenneco (U.S.)

- Hitachi Astemo (Japan)

KEY INDUSTRY DEVELOPMENTS

- October 2025: KYB broadened its European aftermarket portfolio, increasing steering and suspension part coverage to support higher service penetration across passenger vehicles.

- October 2025: SMS group and Jiangsu Pacific commissioned a high-capacity forging press to scale aluminum suspension component production, supporting lightweight vehicle architectures.

- September 2025: ZF presented steer-by-wire and integrated chassis software concepts supporting future electronically controlled suspension and vehicle dynamics architectures.

- April 2025: Tenneco introduced its Monroe CVSA2 electronically controlled suspension technology for Chinese OEMs, targeting improved ride comfort and vehicle stability. The launch supports growing adoption of semi active and active suspension systems in high-volume passenger vehicles, particularly in mid-range and premium segments.

- February 2025: ZF strengthened its partnership with NIO by supporting steer-by-wire integration for premium electric vehicle platforms, enhancing advanced suspension compatibility.

- February 2025: Continental reaffirmed continued R&D spending on vehicle technologies, including chassis and suspension-related innovations, despite near-term market headwinds.

- January 2025: Brembo finalized the acquisition of Öhlins Racing, a specialist in high-performance suspension systems. The deal strengthens Brembo’s presence beyond braking systems, enabling the development of integrated vehicle corner solutions that combine braking, suspension, and ride control technologies for premium passenger vehicles and motorsport applications.

REPORT COVERAGE

The global automotive multi-link suspension market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.8% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, Component, Axle Fitment, Material of Links, Propulsion, Sales Channel and Region |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · LCV · HCV |

|

By Component |

· Control Arms · Bushings · Ball Joints & Spherical Joints · Knuckles / Wheel Carriers · Fasteners & Mounting Hardware |

|

By Axle Fitment |

· Rear Multi-Link · Front Multi-Link |

|

By Material of Links |

· Iron · Steel · Aluminum · Composite |

|

By Propulsion |

· ICE · Electric |

|

By Sales Channel |

· OEM · Aftermarket |

|

By Geography |

· North America (By Vehicle Type, Component, Axle Fitment, Material of Links, Propulsion, Sales Channel and Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, Component, Axle Fitment, Material of Links, Propulsion, Sales Channel and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, Component, Axle Fitment, Material of Links, Propulsion, Sales Channel and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Vehicle Type, Component, Axle Fitment, Material of Links, Propulsion, Sales Channel and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 19.51 billion in 2025 and is projected to reach USD 29.83 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 9.36 billion.

The market is expected to exhibit a CAGR of 4.8% during the forecast period of 2026-2034.

Hatchback/sedan segment led the market by vehicle type.

Rising passenger vehicle comfort expectations is the key factor driving the market.

ZF Friedrichshafen, Continental, Benteler and Magna International are some of the top players in the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us