Automotive OEM Coatings Market Size, Share & Industry Analysis, By Coating Layer (Pretreatment, Electrocoat (E-coat), Primer, Basecoat, and Clearcoat), By Vehicle Type (Passenger Cars, LCVs, and HCVs), By Technology Type (Water-Borne Coatings, Solvent-Borne Coatings, Powder Coatings, and UV-Curable & Low-Bake Coatings), By Resin Type (Polyurethane, Acrylic, Epoxy, Polyester, and Others), and Regional Forecast, 2026-2034

Automotive OEM Coatings Market Size and Future Outlook

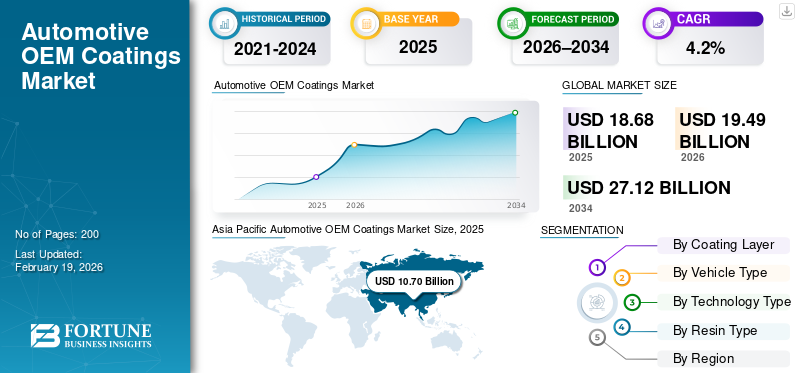

The global automotive OEM coatings market size was valued at USD 18.68 billion in 2025. The market is projected to grow from USD 19.49 billion in 2026 to USD 27.12 billion by 2034, exhibiting a CAGR of 4.2% during the forecast period. Asia Pacific dominated the automotive OEM coatings market with a market share of 57.28% in 2025.

Automotive OEM coatings are factory-applied protective and decorative coating systems used during vehicle manufacturing to enhance corrosion resistance, durability, surface finish, and visual appeal across passenger and commercial vehicles. Key drivers of the market include rising vehicle production, growing demand for corrosion-resistant and durable finishes, tightening VOC and environmental regulations, increased adoption of electric vehicles, and OEM focus on lightweight materials, premium aesthetics, energy-efficient paint shops, and advanced coating technologies.

Major players or companies in the market such as PPG Industries, BASF, AkzoNobel, Axalta, Nippon Paint, and Kansai Paint are focusing on waterborne, powder, and low-bake coatings, digital paint-shop solutions, sustainability-led formulations, and EV-specific coating innovations to strengthen OEM partnerships globally.

Download Free sample to learn more about this report.

Automotive OEM Coatings MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 18.68 billion

- 2026 Market Size: USD 19.49 billion

- 2034 Forecast Market Size: USD 27.12 billion

- CAGR: 4.2% from 2026–2034

- Asia Pacific dominated the automotive OEM coatings market with a 57.28% share in 2025.

- Passenger cars held the largest 74.5% market share in 2025.

- Water-borne coatings held the largest market share by technology type.

North American

North America recorded steady growth, supported by stable vehicle production and increasing adoption of low-VOC coating technologies.

Europe

Europe witnessed strong demand, driven by stringent environmental regulations and high adoption of water-borne coating technologies.

Asia Pacific

Asia Pacific is the largest and fastest-expanding region in the global market.

U.S.

The market was valued at USD 2.59 billion in 2025, supported by strong passenger vehicle and light truck production.

Japan

The market was valued at USD 1.56 billion in 2025, driven by advanced coating technologies and high-quality vehicle production

Read More

AUTOMOTIVE OEM COATINGS MARKET TRENDS

Accelerating Electrification to Drive Coating Innovation and Demand

The transition to electric vehicles (EVs) is reshaping the demand for automotive OEM coatings, requiring tailored solutions that balance protective performance with compatibility with advanced materials, including aluminum, composites, and battery housings. EVs often operate in environments that are both thermal and electrically sensitive, prompting coating suppliers to develop formulations that enhance corrosion protection, thermal management, and surface aesthetics. Growth in electrical components also increases the demand for specialized primers and clearcoats that contribute to sensor performance and crash safety. As EV production grows globally, coatings suppliers are expanding R&D initiatives and product lines, improving adhesion and durability for new-generation vehicles. Continued investment in EV-tailored coatings helps OEMs reduce production defects and meet rising consumer expectations for sustainable and premium finishes.

- In March 2025, PPG Industries reported that its automotive OEM coatings business delivered an 8% increase in net sales with growth above market in all regions, reflecting strong demand and innovation momentum in OEM coatings aligned with broader automotive production growth.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Environmental Regulations to Catalyze Sustainable Coating Adoption

Environmental and emissions regulations are driving the industry toward lower-emission, eco-friendly coating technologies, such as waterborne, powder, and low-VOC formulations. Historically, OEM coatings in the automotive sector relied on solvent-borne technologies. Still, increasingly tighter regulations on volatile organic compounds (VOCs) and hazardous substances compel suppliers to innovate products that meet evolving standards while maintaining performance. These regulatory pressures also influence manufacturing processes, requiring paint shops to install equipment that minimizes emissions and improves energy efficiency. This, in turn, accelerates R&D activities in sustainable coatings that reduce environmental impact without compromising corrosion resistance, finish quality, or durability, boosting automotive OEM coatings market growth. Standards in key markets such as Europe, North America, and Asia Pacific collectively shape global coating specifications, encouraging OEMs and suppliers to collaborate on compliant solutions. EPA rules limiting VOC emissions in surface coating operations highlight ongoing regulatory focus on emissions reductions across automotive painting operations.

MARKET RESTRAINTS

Raw Material Cost Volatility May Restrain Market Expansion

The market faces restraints due to significant volatility in raw material prices, particularly for key resin systems and pigment components. Resin systems such as epoxy resins and polyurethane represent a large share of production costs, and disruptions in supply, energy pricing, or chemical feedstock availability directly impact coatings manufacturers’ margins. Price volatility also affects procurement strategies, often forcing OEMs and coating suppliers to adapt sourcing plans, hedge risks, or absorb cost increases. Periods of resource scarcity can slow coatings innovation cycles and constrain expansion in certain regions, especially where logistics and supply chain bottlenecks add complexity. This restraint is magnified during economic downturns or when global chemical markets face imbalances, limiting predictable growth trajectories for coatings suppliers. Titanium dioxide and epoxy resin price spikes between 2021 and 2022 exemplify raw material cost pressures impacting coatings supply chains.

MARKET OPPORTUNITIES

Lightweight and Advanced Materials to Present New Market Opportunities

The shift toward lightweight vehicle structures and advanced materials opens fresh opportunities for OEM coatings suppliers. As automakers incorporate aluminum, high-strength steels, composites, and engineered plastics to improve fuel efficiency or EV range, coatings must adapt to ensure compatibility across diverse substrates. This creates the demand for multi-functional and adhesion-optimized coating systems that protect against corrosion, enhance mechanical performance, and maintain aesthetic qualities. Light weighting also encourages the development of coatings that improve thermal, chemical, and environmental resistance in service conditions. Suppliers investing in formulation science and substrate-specific solutions can capture incremental market share by aligning with OEM requirements for next-generation vehicle platforms. Advanced coatings tailored for multi-material bodies represent a growing niche within the broader OEM coatings value chain. Advanced ceramic coating R&D for EV battery enclosures demonstrates the potential for coatings to add functional value beyond traditional protection.

MARKET CHALLENGES

Complex Material Compatibility and Substrate Diversity to Create Challenges for Market Expansion

The rapid shift in vehicle design toward lightweight materials, including aluminum, high-strength steels, composites, and engineered plastics, presents a technical challenge for automotive OEM coatings. Coating systems must deliver consistent adhesion, corrosion protection, and finish quality across diverse substrates with differing surface energies. This increases formulation complexity and testing requirements, driving up R&D costs and prolonging validation cycles. Variability in substrate chemistry also raises the risk of paint defects, requiring more advanced surface pretreatments and precise process controls in paint shops. As vehicle electrification and material innovation accelerate, balancing multi-material compatibility with environmental compliance and durability expectations remains a significant challenge for coating manufacturers and OEMs.

- In January 2025, Toyota confirmed expanded evaluations of paint adhesion for aluminum and composite panels on upcoming electric SUV models, reflecting real-world challenges in coating multi-material vehicles.

Download Free sample to learn more about this report.

Segmentation Analysis

By Coating Layer

Surging Consumer Preference for Customized Finishes to Propel Basecoat Segment Leadership

Based on coating layer, the market is segmented into pretreatment, electrocoat (E-coat), primer, base coat, and clearcoat.

The basecoat segment dominates the market due to its critical role in delivering color, visual differentiation, and brand identity. Increasing consumer preference for metallic, pearlescent, and customized finishes directly elevates basecoat value per vehicle. High repaint sensitivity, complex pigments, and multilayer effects further strengthen its revenue contribution despite thinner film thickness.

The Electrocoat (E-coat) segment is the fastest-growing segment and is projected to grow at a CAGR of 4.7% over the forecast period, driven by stricter corrosion protection requirements and increasing use of lightweight metals.

By Vehicle Type

Sustained Passenger Vehicle Production to Foster Passenger Cars Segmental Expansion

Based on vehicle type, the market is segmented into passenger cars, LCVs, and HCVs.

The passenger cars segment dominates the market due to their high global production volumes and greater emphasis on exterior aesthetics, gloss retention, and premium finishes. Multiple coating layers, frequent model refresh cycles, and rising EV penetration amplify the value per unit of coatings in this segment. The strong presence of SUVs and crossovers further boosts coating consumption.

The LCVs segment is the fastest-growing segment and is projected to grow at a CAGR of 4.5% over the forecast period. This is supported by e-commerce growth, urban logistics demand, and increased fleet renewal across regions.

To know how our report can help streamline your business, Speak to Analyst

By Technology Type

Environmental Compliance to Strengthen the Dominance of Water-Borne Coatings Segment

Based on technology type, the market is segmented into water-borne coatings, solvent-borne coatings, powder coatings, and UV-curable & low-bake coatings.

The water-borne coatings segment holds the dominant automotive OEM coatings market share owing to their widespread adoption in basecoat applications and compliance with stringent VOC regulations across major automotive manufacturing regions. OEM investments in advanced paint shops and sustainable production further reinforce this dominance.

The UV-curable & low-bake coatings segment is the fastest-growing segment and is projected to grow at a CAGR of 6.5% over the forecast period. This is driven by EV production, increased use of plastic components, and the need for energy-efficient curing processes.

By Resin Type

Acrylic Resins Segment Leads the Market with Wide Usage in Basecoats and Clearcoats

Based on resin type, the market is segmented into polyurethane, acrylic, epoxy, polyester, and others.

The acrylic resins segment dominates the market due to their extensive use in basecoats and clearcoats, offering excellent color clarity, color matching, UV resistance, and cost efficiency. Their compatibility with water-borne technologies further strengthens adoption across high-volume vehicle platforms.

The polyurethane resins segment is the fastest-growing segment and is projected to grow at a CAGR of 4.9% over the forecast period. This is supported by the rising demand for scratch resistance, gloss durability, and premium clearcoat performance, especially in EVs and luxury vehicles.

AUTOMOTIVE OEM COATINGS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive OEM Coatings Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the largest and fastest-expanding region in the global market. Growth is driven by massive vehicle production volumes, expanding middle-class demand, and increasing localization of OEM manufacturing. While cost efficiency remains critical, regulatory tightening and EV growth are accelerating the adoption of water-borne, powder, and advanced coating technologies across key countries.

China Automotive OEM Coatings Market

China led the Asia Pacific market with a share of 56.4% in 2025 due to unmatched vehicle production volumes and rapid growth in EV manufacturing. Rising quality expectations, stricter environmental regulations, and large-scale investments in automated paint shops are driving strong demand for advanced OEM coating systems.

Japan Automotive OEM Coatings Market

Technological sophistication, consistent vehicle exports, and high-quality coating standards characterize Japan’s market. OEMs focus on durability, corrosion protection, and precision finishes to support the stable demand for advanced primers, basecoats, and environmentally compliant coating technologies. The Japan market was valued at USD 1.56 billion in 2025.

India Automotive OEM Coatings Market

The India market is poised to depict high-growth with a CAGR of 6.6% over the forecast period. This is driven by the rising passenger cars and LCV production. Increasing localization, improving paint quality standards, and gradual adoption of water-borne technologies contribute to expanding coating consumption and value growth.

North America

North America represents a mature yet steadily growing market, supported by stable vehicle production, strong pickup and SUV demand, and continuous upgrades in OEM paint shop technologies. Environmental compliance has accelerated the shift toward water-borne and low-VOC coatings, while EV investments are increasing the demand for advanced primers and clearcoats. High coating value per vehicle, especially in LCVs and premium passenger cars, sustains market growth despite moderate production volume expansion.

U.S. Automotive OEM Coatings Market

The U.S. dominated the North American market with a value of USD 2.59 billion in 2025 due to the high production of passenger vehicles and light trucks. Strong demand for durable, premium finishes, increasing EV manufacturing, and OEM investments in sustainable paint shops drive higher coating value per vehicle, supporting consistent market expansion.

Europe

The Europe market is shaped by stringent environmental regulations, high penetration of water-borne technologies, and a strong premium vehicle mix. OEMs prioritize advanced coating systems to meet VOC norms while delivering superior finish quality. Electrification, lightweighting, and frequent model updates continue to support steady coatings demand, even as overall vehicle production grows at a moderate pace.

U.K. Automotive OEM Coatings Market

Passenger-car production, premium-vehicle exports, and rising EV assembly drive the U.K. market, which reached a value of USD 0.76 billion in 2025. Strong regulatory focus on emissions and sustainability supports high adoption of water-borne and low-bake coatings, while OEM emphasis on appearance quality propels the demand for advanced basecoats and clearcoats.

Germany Automotive OEM Coatings Market

Germany accounted for Europe’s largest market with a share of 27.3% in 2025, supported by high vehicle output and a strong luxury and performance car segment. Advanced paint technologies, complex color finishes, and EV production significantly increase the value of coatings per vehicle, reinforcing the country’s dominant position.

Rest of the World

The market in the rest of the world, including Latin America, the Middle East, and Africa, is driven by the gradual expansion of local vehicle assembly, improvements in industrial infrastructure, and the replacement of aging vehicle fleets. While solvent-borne coatings remain relevant, regulatory evolution and OEM investments are encouraging a gradual shift toward sustainable coating technologies, supporting long-term growth potential.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Adopt Sustainability-driven Technologies and Innovation to Consolidate their Industry Positions

Continuous formulation innovation, sustainability-driven technologies, and long-term partnerships between coating suppliers and vehicle manufacturers shape the global automotive OEM coatings market trends. Leading players such as PPG Industries, BASF Coatings, AkzoNobel, Axalta Coating Systems, Nippon Paint Holdings, Kansai Paint, and Sherwin-Williams compete through advanced waterborne, powder, and low-bake coating systems that meet stringent environmental and performance standards. Companies strengthen competitiveness by expanding regional production facilities near OEM plants, investing in high-throughput and energy-efficient paint shop solutions, and developing coatings tailored for electric vehicles and lightweight substrates. Strategic focus areas include corrosion-resistant electrocoats, premium appearance clearcoats, and digitally enabled color management systems. Partnerships with OEMs emphasize long-term supply contracts, joint R&D programs, and sustainability goals. In June 2024, BASF Coatings expanded its water-borne OEM coatings portfolio to support lower-VOC automotive paint processes, reinforcing its competitive positioning across global manufacturing platforms.

LIST OF KEY AUTOMOTIVE OEM COATINGS COMPANIES PROFILED

- PPG Industries (U.S.)

- Axalta Coating Systems (U.S.)

- BASF Coatings (Germany)

- AkzoNobel (Netherlands)

- Nippon Paint Automotive Coatings (Japan)

- Kansai Paint (Japan)

- Sherwin-Williams (Automotive Finishes Group) (U.S.)

- Jotun (Norway)

- KCC Corporation (South Korea)

- Beckers Group (Sweden)

- RPM International (Valspar Automotive) (U.S.)

- Clariant (Automotive Coatings Additives) (Switzerland)

- Covestro (Germany)

- DSM Coating Resins (Netherlands)

- Berger Paints (OEM & Industrial Coatings) (India)

KEY INDUSTRY DEVELOPMENTS

- January 2026: PPG and 4Plastic launched next-generation texture coatings designed to repair non-painted, textured plastic auto parts in the U.S. and Canada. The coatings replicate OEM textures, improving durability and finish accuracy, while a mobile app helps technicians identify and match correct textures, enhancing repair precision and sustainability by reducing part replacements.

- November 2025: AkzoNobel and Axalta signed a definitive all-stock merger of equals, creating a combined global coatings leader with USD 17 billion in revenue and USD 25 billion in enterprise value, targeting USD 600 million in cost synergies. The deal strengthens the scale, technology breadth, and global footprint of automotive OEM and industrial coatings.

- November 2025: BASF Coatings commissioned a new automotive OEM coatings production plant in Munster, Germany, designed for high-volume, high-runner colors. The facility emphasizes consistent quality, automation-driven efficiency, and more sustainable operations, supporting OEM customers with a faster, stable supply of popular color SKUs.

- October 2025: BASF and Carlyle (with QIA) reached a binding agreement for BASF’s coatings business, including automotive OEM coatings, refinish, and surface treatments, valuing it at around USD 8.5 billion enterprise value, with BASF retaining a 40% equity stake and closing expected in Q2 2026 (subject to approvals).

- October 2025: Toyoda Gosei and Kansai Paint jointly announced Japan’s first in-mold coating technology applicable to the mass production of large plastic exterior parts. Painting inside the mold improves appearance quality and can simplify finishing steps, enabling new design possibilities for large components while supporting manufacturing efficiency and process innovation.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.2% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Coating Layer, By Vehicle Type, By Technology Type, By Resin Type, and By Region |

|

By Coating Layer |

· Pretreatment · Electrocoat (E-coat) · Primer · Basecoat · Clearcoat |

|

By Vehicle Type |

· Passenger cars · LCVs · HCVs |

|

By Technology Type |

· Water-borne coatings · Solvent-borne coatings · Powder coatings · UV-curable & low-bake coatings |

|

By Resin Type |

· Polyurethane · Acrylic · Epoxy · Polyester · Others (alkyd, hybrid systems) |

|

By Geography |

· North America (By Coating Layer, By Vehicle Type, By Technology Type, By Resin Type, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Coating Layer, By Vehicle Type, By Technology Type, By Resin Type, and By Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Coating Layer, By Vehicle Type, By Technology Type, By Resin Type, and By Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Coating Layer, By Vehicle Type, By Technology Type, and By Resin Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 18.68 billion in 2025 and is projected to reach USD 27.12 billion by 2034.

In 2025, the market value stood at USD 10.70 billion.

The market is expected to grow at a CAGR of 4.2% during the forecast period from 2026 to 2034.

By vehicle type, the passenger cars segment leads the market share.

Stringent environmental regulations are key factors anticipated to drive market expansion.

PPG Industries, BASF se, AkzoNobel, Axalta, Nippon Paint, Sherwin Williams Company, and Kansai Paint are the top players in the market.

Asia Pacific accounts for the largest share of the market.

North America, Europe, Asia Pacific, and the rest of the world have been considered in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us