Automotive Pillar Market Size, Share & Industry Analysis, By Pillar Type (A-Pillar, B-Pillar, C-Pillar, D-Pillar & Others), By Material (Steel, Aluminum, Composites/Carbon Fiber, Plastic/Polymers), By Vehicle Type (Hatchback, Sedan, SUVs, LCVs, HCVs, Buses & Coaches), and Regional Forecast, 2026-2034

Automotive Pillar Market Size

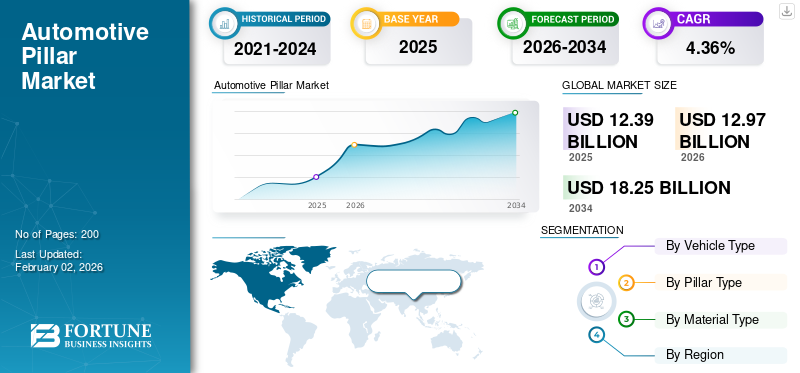

The global automotive pillar market size was valued at USD 12.39 billion in 2025. The market is projected to grow from USD 12.97 billion in 2026 to USD 18.25 billion by 2034, exhibiting a CAGR of 4.36% during the forecast period. Asia Pacific dominated the automotive pillar market with a share of 48.22% in 2025.

Automotive pillars are vertical structural supports in a vehicle that connect the roof to body, enhancing strength, crash resistance, and passenger safety. Classified as A, B, C, and sometimes D-pillars, these components influence visibility, aerodynamics, and vehicle design. They play a critical role in meeting safety regulations while also shaping the aesthetics of passenger cars, SUVs, buses, and commercial vehicles across global automotive industry. The market is driven by growing safety regulations, rising adoption of lightweight materials, and increasing demand for fuel-efficient and electric vehicles. Advancements in structural composites, crashworthiness standards, and vehicle design innovations also push the market growth.

Key players in the market include Magna International, Gestamp Automoción, Toyoda Iron Works, Kirchhoff Automotive, and Benteler International. These companies focus on advanced material usage, such as aluminum and carbon fiber, to reduce weight while ensuring durability. Strategic investments in research, design, and regional manufacturing facilities strengthen their competitive edge. Partnerships with automakers, innovations in crash-resistant designs, and sustainability initiatives further define their role in shaping the market landscape.

Download Free sample to learn more about this report.

Automotive Pillar Market Key Takeaways

- 2025 Market Size: USD 12.39 billion

- 2026 Market Size: USD 12.97 billion

- 2034 Forecast Market Size: USD 18.25 billion

- CAGR: 4.36% from 2026–2034

- Asia Pacific dominated the automotive pillar market with a 48.22% share in 2025.

- The SUV segment is projected to account for 41.24% of the market in 2026.

- The B-pillar segment is projected to hold a 38.73% market share in 2026.

Asia Pacific

Asia Pacific accounted for 48.22% of the market, valued at USD 5.97 billion in 2025.

North America

North America held a 24.17% market share, reaching USD 2.99 billion in 2025.

Europe

Europe captured 18.48% of the market, valued at USD 2.29 billion in 2025.

U.S

The market is projected to reach USD 2.48 billion in 2026.

Japan

The market is projected to reach USD 1.00 billion in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Stringent Safety Regulations and Crashworthiness Standards Drive Market Growth

Stringent safety regulations and crashworthiness standards are the primary forces driving the automotive pillar market growth. Governments and safety bodies such as NHTSA, Euro NCAP, and ASEAN NCAP enforce strict rules for rollover protection, side-impact resistance, and roof strength, making pillars an essential structural element. Automakers are required to design A- and B-pillars using advanced high strength steel, aluminum, or composites to comply with crash-test ratings. Failure to meet these standards impact sales, brand reputation, and regulatory approval. This mandatory compliance ensures continuous innovation and investment in stronger, lightweight, and crash-resistant pillars, positioning safety regulations as the key driver of market growth globally. In September 2025, China released draft safety rules for Level-2 driving assistance systems that will require detecting driver disengagement, sending alerts, and disabling the system if no response. These regulations, effective from 2027, underscore the growing regulatory scrutiny around ADAS (advanced driver assistance systems), which interact with pillar design when cameras or sensors are mounted on or near A-/B-pillars.

MARKET RESTRAINTS:

High Material and Manufacturing Costs Limit Market Expansion

High material and manufacturing costs act as a key restraint in the market. Advanced lightweight materials such as aluminum, composites, and carbon fiber significantly enhance safety and fuel efficiency but remain expensive to source and process. Specialized manufacturing methods, including hot stamping and hydroforming, further adds to production expenses, making these solutions viable primarily for luxury and premium vehicles. In price-sensitive segments, automakers prefer traditional steel pillars due to affordability. This cost barrier limits the large-scale adoption of innovative pillar technologies, slowing market penetration and restraining growth across emerging and mass-market vehicle categories.

MARKET OPPORTUNITIES:

Lightweight Material Adoption Creates Lucrative Growth Opportunities

The most significant opportunity for the market lies in the adoption of lightweight materials to support electric vehicle (EV) growth and fuel-efficiency goals. As EVs gain prominence, reducing overall vehicle weight becomes crucial to extending battery range and enhancing performance. Automotive pillars made from aluminum, carbon fiber, advanced composites, and hybrid alloys provide the strength-to-weight balance required by modern designs. Additionally, stricter global emission regulations encourage automakers to replace traditional steel with sustainable and lighter alternatives. Companies developing cost-effective, lightweight pillar solutions are well-positioned to capture demand from both EV manufacturers and fuel-efficient internal combustion vehicles. In November 2024, Group-TTM developed advanced casting transfer dies tailored for manufacturing A-pillars using lightweight metals such as aluminum. These tools enable better control over deformation in light material forming and improve production efficiency and part consistency.

MARKET CHALLENGES:

Balancing Safety Standards with Driver Visibility Remains a Key Challenge

The greatest challenge in the market lies in balancing safety standards with driver visibility. Pillars, particularly A-pillars, are essential for meeting stringent crashworthiness and rollover protection requirements. However, reinforcing them for greater strength often increases thickness, restricting the driver’s field of vision and creating blind spots. This trade-off complicates design, as regulators demand stronger structures while consumers expect better visibility and driving comfort. Although solutions such as transparent materials, slimmer yet stronger alloys, and camera-based systems are being explored, high costs and integration complexities limit large-scale adoption, making this balance the industry’s toughest challenge. In June 2025, Mercedes-Benz issued a recall for about 90,000 vehicles as the C pillar and roof lining failed FMVSS (Federal Motor Vehicle Safety Standard), impacting absorption tests. The issue relates to improper stiffness, which reduced energy absorption.

AUTOMOTIVE PILLAR MARKET TRENDS:

Integration of Sensors and ADAS into Pillar Structures is an Emerging Market Trend

One of the most significant automotive pillar market trend is the integration of sensors and advanced driver-assistance systems (ADAS) into pillar structures. Traditionally served as passive safety supports, pillars are now being designed to accommodate cameras, radar, LiDAR, and driver-monitoring sensors that enhance visibility and enable collision avoidance. A- and B-pillars, in particular, are key locations for embedding these technologies without compromising vehicle aesthetics. This shift reflects the industry’s transition toward connected and autonomous vehicles, where pillars serve a dual purpose—maintaining crashworthiness while enabling smart mobility features. Such multifunctional pillars represent the future of automotive design and safety. In August 2025, Tesla updated its Sentry Mode to include footage from the Cybertruck’s B-pillar cameras, enhancing vehicle security by covering blind spots previously missed by front and rear cameras. This upgrade strengthens side surveillance and highlights the growing role of pillar-integrated technologies in improving vehicle safety.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

Growing Consumer Preference for Safety Features Drives the SUVs Segment Expansion

On the basis of vehicle type, the market is classified into hatchback, sedan, SUVs, LCVs, HCVs, buses & coaches.

The SUV segment by vehicle type is projected to account for a market size of USD 5.35 billion, representing a 41.24% share. SUVs dominate and are the fastest-growing vehicle type in the market due to their global popularity, larger structural frames, and rising consumer demand for safety and comfort in the passenger cars segment. Pillars in SUVs must be stronger to support bigger body sizes, higher center of gravity, and larger roofs, including panoramic sunroofs. Additionally, consumer preference for premium SUVs with advanced safety features drives the need for innovative pillar materials and designs. Emerging economies with growing middle-class populations are also fueling SUV sales, further boosting the demand for strong, lightweight, and stylish pillars that balance safety, visibility, and design aesthetics. In September 2025, Jetour, a Chinese SUV brand, announced expansion into Europe, starting with Poland, aiming to grow global sales from 560,000 units in 2024 to 800,000 units in 2025, leveraging demand for SUVs in market.

By Pillar Type

Critical Role in Crashworthiness and Passenger Protection Drives the B-Pillar Segment Expansion

In terms of pillar type, the market is categorized into A-pillar, B-pillar, C-pillar, D-pillar & others.

The B-pillar segment by pillar type is expected to reach USD 5.02 billion, capturing 38.73% of the market share. The B-pillar is the dominating segment in the market as it plays a central role in vehicle crashworthiness and structural rigidity. Positioned between the front and rear doors, it anchors critical safety components such as seatbelts, side-impact protection systems, and curtain airbags. B-pillars are essential for preventing cabin intrusion during collisions and ensuring passenger safety, making them indispensable in all vehicle types. As safety regulations become stricter globally, automakers invest heavily in strengthening B-pillars using advanced high-strength steel and lightweight alloys, safeguarding compliance while maintaining cost efficiency. Their irreplaceable structural and safety functions ensure segment dominance. In November 2021, Novelis released Advanz 7UHS-s701, a new aluminum alloy targeted for safety-critical applications such as A and B-pillar reinforcements. It offers lightweighting (up to 40% over hot-formed steel) while meeting crash, loading, and design requirements. It is also designed to work with hot stamping, aiding compatibility with existing production processes.

The D- and other supporting pillars are the fastest-growing segment due to rising production of SUVs, crossovers, minivans, and luxury vehicles that require additional roof and structural support. D-pillars are crucial for larger vehicles with extended cabin space, panoramic roofs, and rear-side openings, enhancing rigidity and crash resistance. Growing consumer demand for SUVs and premium designs is pushing automakers to integrate stylish yet strong D-pillars. The adoption of lightweight materials and aesthetic customization also accelerates the segment growth. As SUVs dominate global markets, D-pillars and other supportive pillars increasingly contribute to vehicle safety, stability, and modern design architecture. In 2025 U.S. Large SUV Sales Figures, Chevrolet Tahoe sold 60,094 units in the year-to-date period, up from 48,443 during the same period last year, a growth of nearly 24%.

To know how our report can help streamline your business, Speak to Analyst

By Material Type

Cost-Effectiveness and Structural Reliability Ensure the Steel Segment Dominance

Based on material type, the market is segmented into steel, aluminum, composites/carbon fiber, and plastic/polymers.

The steel segment by material is anticipated to dominate the market with a value of USD 9.09 billion, accounting for 70.05% of the total share. Steel dominates the market as it remains the most widely used material for structural safety, cost efficiency, and mass-market scalability. High-strength and ultra-high-strength steel variants offer superior crash resistance while being relatively affordable compared to aluminum or composites. Its well-established supply chains, proven manufacturing processes, and repairability make steel the preferred choice for automakers globally. Steel pillars are integral in meeting stringent crashworthiness regulations while keeping vehicle costs competitive, particularly in mass-market models. Despite lightweighting trends, steel upholds dominance due to its versatility, durability, and ability to provide structural integrity across all vehicle categories. In April 2025, Kirchhoff Automotive announced new product developments using a silicon-boron steel grade. Hot-formed B-pillar tests showed higher crash safety through improved energy absorption with less material usage. An innovative steel module cross member (open-shell design) was also introduced to provide functional integration and cost reduction.

Composites and carbon fiber represent the fastest-growing material segment due to rising demand for lightweight structures that improve fuel efficiency and EV range. These materials deliver superior strength-to-weight ratios compared to traditional metals, enabling safer yet lighter designs. Premium and electric vehicle manufacturers are increasingly adopting composites to enhance performance, aesthetics, and sustainability. Although cost remains a limitation, ongoing innovations in material processing and mass-production techniques are improving feasibility. As automakers focus on lightweight strategies to meet emission norms and extend EV battery efficiency, composites and carbon fiber pillars are experiencing rapid adoption and growth in the automotive pillar market. In July 2025, Kraiburg TPE introduced its Thermolast R RC/UV/AP series for automotive pillars, offering lighter-weight thermoplastic elastomer materials that maintain strength, durability, and compliance with crash deformation and safety standards. The innovation enables slimmer pillar profiles without compromising structural integrity.

Automotive Pillar Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific dominates and is the fastest-growing market for automotive pillars, driven by the massive automotive industries in China, Japan, India, and South Korea. Rising middle-class income, rapid urbanization, and increasing safety awareness are fueling vehicle demand, especially SUVs and electric vehicles. Governments are enforcing stricter safety and emission standards, compelling automakers to adopt stronger, lightweight pillars. Additionally, Asia Pacific leads in EV adoption, further boosting demand for composite and aluminum pillars. Cost-competitive manufacturing, large-scale vehicle exports, and the presence of global as well as regional automakers make Asia Pacific the hub for both volume and innovation. In September 2025, Global NCAP rolled out stricter safety protocols, introducing tougher side-impact tests that place greater emphasis on strength of car pillars, particularly B- and C-pillars, to protect passengers during collisions. The Maruti Suzuki Victor became the first Indian car to achieve a 5-star rating under these rules, highlighting the role of reinforced pillars in crash safety. The Japan market is projected to reach USD 1 billion by 2026, the China market is projected to reach USD 3.71 billion by 2026, and the India market is projected to reach USD 0.57 billion by 2026. Asia Pacific maintained a strong presence in the global market, reaching USD 5.97 billion in 2025, accounting for 48.22% share, and is expected to reach USD 6.32 billion in 2026.

North America

North America holds the second-largest automotive pillar market share, driven by stringent safety regulations, strong demand for SUVs and pickup trucks, and high consumer awareness regarding crash protection. Automakers in the region prioritize compliance with NHTSA and IIHS standards, pushing innovation in pillar strength and design. Lightweighting initiatives also support growth as manufacturers shift to fuel-efficient and electric vehicles. The presence of global OEMs and Tier-1 suppliers ensures continuous advancements in material usage, especially ultra-high-strength steel and aluminum. Rising consumer demand for luxury and technologically advanced vehicles further reinforces North America’s market development. The U.S. market is projected to reach USD 2.48 billion by 2026. In 2025, the North America market stood at USD 2.99 billion, representing 24.17% of global demand, and is projected to grow to USD 3.11 billion in 2026.

U.S.

The U.S. dominates the North American region due to its robust automotive manufacturing base, particularly in SUVs and pickup trucks, which require stronger structural supports. Stringent federal crashworthiness standards and advanced consumer safety expectations drive continuous innovation in A- and B-pillar designs. U.S. automakers invest heavily in high-strength steel, aluminum, and composite pillars to balance safety with efficiency. Strong R&D investments, advanced manufacturing infrastructure, and the presence of leading OEMs position the U.S. as the dominant market within the region.

Europe

Europe’s market is driven by strict safety regulations from Euro NCAP and the EU, alongside a strong consumer preference for premium vehicles. German, French, and U.K. automakers lead in adopting lightweight and sustainable materials for pillars to meet emissions and efficiency goals. Rising EV production and increasing demand for luxury cars also boost the adoption of advanced composite and aluminum pillars. Moreover, European manufacturers emphasize integrating ADAS and sensor technologies into pillar structures to support semi-autonomous driving. Sustainability initiatives and a strong focus on crashworthiness ensure Europe remains a vital market for innovative pillar solutions. In July 2025, Valeo and Mobileye teamed up to supply Volkswagen Group brands (VW, SEAT, Škoda) with their Surround ADAS architecture, which uses multiple cameras and sensors around the vehicle perimeter. This system’s design implies mounting sensors near the A/B-pillar areas to ensure 360° coverage. The UK market is projected to reach USD 0.44 billion by 2026, while the Germany market is projected to reach USD 0.63 billion by 2026. The Europe region captured 18.48% of the global market in 2025, generating USD 2.29 billion in revenue, and is projected to reach USD 2.36 billion in 2026.

Rest of the World

The Rest of the World market is driven by increasing vehicle production and rising safety regulations in Latin America, the Middle East, and Africa. Growing adoption of SUVs and commercial vehicles in these regions creates demand for structurally strong pillars. Although cost sensitivity limits widespread use of composites or advanced materials, steel pillars dominate due to affordability and durability. Gradual enforcement of crashworthiness standards, coupled with growing consumer safety awareness, is expected to strengthen the regional market growth. Investments in localized manufacturing and the entry of global OEMs into these markets will further boost demand for advanced pillar designs. The Rest of the World market generated USD 1.13 billion in 2025, representing 9.12% of the global market landscape, and is expected to reach USD 1.18 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Innovation in Lightweight Materials and ADAS Integration Drives Competitive Edge

The market is highly competitive, with global Tier-1 suppliers and regional players focusing on innovation, lightweighting, and compliance with stringent safety standards. Leading companies such as Magna International, Gestamp Automoción, Kirchhoff Automotive, Benteler International, and Toyoda Iron Works dominate through strong OEM partnerships and global manufacturing footprints. Competition centers around the development of ultra-high-strength steel, aluminum, and composite pillars that balance safety with weight reduction. Increasing focus on sustainability and ADAS integration further intensifies rivalry. Strategic collaborations, R&D investments, and localized production are key strategies adopted by players to strengthen market presence and differentiation.

LIST OF KEY AUTOMOTIVE PILLARS COMPANIES PROFILED:

- Magna International Inc. (Canada)

- Gestamp Automoción S.A. (Spain)

- Kirchhoff Automotive GmbH (Germany)

- Benteler International AG (Austria)

- Toyoda Iron Works Co., Ltd. (Japan)

- G-TEKT Corporation (Japan)

- Aisin Seiki Co., Ltd. (Japan)

- Dura Automotive Systems, LLC (U.S.)

- Hirotec Corporation (Japan)

- Martinrea International Inc. (Canada)

- CIE Automotive S.A. (Spain)

- Hyundai Mobis Co., Ltd. (South Korea)

- Thyssenkrupp AG (Germany)

- ArcelorMittal S.A. (Luxembourg)

- UACJ Corporation (Japan)

- BaoSteel Group Corporation (China)

- SeAH Steel Holdings Corporation (South Korea)

KEY INDUSTRY DEVELOPMENTS:

- In September 2025, Kirchhoff Automotive unveiled a hot-formed B-pillar made of silicon-boron steel (“SIBORA”), developed with Volkswagen and other partners. The pillar, shown at IAA Mobility 2025, was awarded the Swedish Steel Prize for its innovative steel grade. Key features include variable hardness control through temperature adjustments during production, achieving improved crash safety while supporting lightweight and sustainability goals.

- In September 2025, AISIN Corporation unveiled its Intelligent Pillar Unit at IAA Mobility 2025. The technology integrates sensing functions into the pillar, achieving over three times the recognition distance and four times the recognition angle compared to industry benchmarks for keyless entry. It also enhances aesthetic appearance.

- In September 2025, DURA began modernizing production with automated 3D inspection (MetroFactory) to improve dimensional accuracy and quality for safety-critical body components. This capability supports precise pillar manufacture and assembly tolerances required for modern high-strength and sensor-integrated pillars.

- In May 2025, Zeekr unveiled its 007 GT electric vehicle, which features an interactive intelligent B-pillar system incorporating two cameras. This innovation enhances side visibility and supports autonomous features by adding sensory input to the pillar structure.

- In January 2025, at the Bharat Mobility Global Expo, Gestamp introduced a “Door Ring” in its GES-GIGASTAMPING range: a one-piece component replacing several parts. This improves safety cell integrity in crash scenarios, reduces weight, simplifies assembly, and lowers manufacturing complexity, all relevant to strengthening pillars and adjacent body structure.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021–2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021–2024 |

| Growth Rate | |

| Unit | Value (USD Billion) |

| By Vehicle Type |

|

| By Pillar Type |

|

| By Material Type |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 12.39 billion in 2025 and is projected to reach USD 18.25 billion by 2034.

In 2025, the market value stood at USD 12.39 billion.

The market is expected to exhibit a CAGR of 4.36% during the forecast period of 2026-2034.

The steel segment led the market by material type.

Stringent safety regulations and crashworthiness standards drive market growth.

Leading companies such as Magna International, Gestamp Automoción, Kirchhoff Automotive, Benteler International, and Toyoda Iron Works dominate the market.

Asia Pacific held the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us