Automotive Piston Pin Market Size, Share & Industry Analysis, By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), and 2 Wheelers & 3 Wheelers), By Engine Type (Gasoline Engines and Diesel Engines), By Engine Configuration (Inline Engines, V-Type Engines, and Flat / Boxer Engines), By Piston Pin Type (Fixed Piston Pin, Semi-Floating Piston Pin, and Fully Floating Piston Pin), and Regional Forecast, 2026–2034

Automotive Piston Pin Market Size and Future Outlook

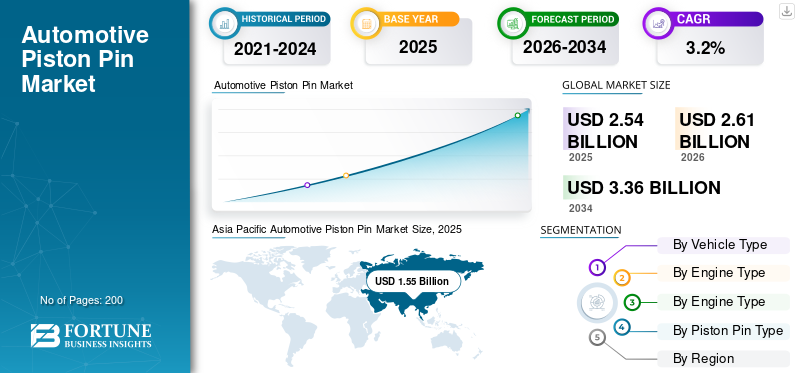

The global automotive piston pin market size was valued at USD 2.54 billion in 2025. The market is projected to grow from USD 2.61 billion in 2026 to USD 3.36 billion by 2034, exhibiting a CAGR of 3.2% during the forecast period. Asia Pacific dominated the automotive piston pin market with a market share of 61.02% in 2025.

An automotive piston pin is a cylindrical metal component connecting the piston to a rod in an internal combustion engine, enabling pivoting motion and transferring combustion forces for efficient engine operation. Increasing vehicle production, rising market demand for fuel-efficient engines, advancements in lightweight materials, expanding automotive aftermarket, and growing engine performance requirements are key factors driving market growth.

Major players in the market include Tenneco Inc., Shriram Pistons & Rings Ltd., Amsted Automotive, and Burgess-Norton Manufacturing Company. These players are competing through advanced metallurgy, precision manufacturing, lightweight materials, and strong OEM partnerships.

Download Free sample to learn more about this report.

Automotive Piston Pin Market Takeaways

- 2025 Market Size: USD 2.54 billion

- 2026 Market Size: USD 2.61 billion

- 2034 Forecast Market Size: USD 3.36 billion

- CAGR: 3.2% from 2026–2034

- Asia Pacific dominated the automotive piston pin market with a 61.02% share in 2025.

- Passenger cars remained the leading vehicle segment, supported by high global production volumes and aftermarket demand.

- Fully floating piston pins dominated the market due to superior durability and reduced friction in modern engines.

North America

North America remained the second-largest market, supported by a large vehicle parc and strong aftermarket demand.

Europe

Europe held the third-largest share, backed by premium vehicle production and advanced engine engineering capabilities.

Asia Pacific

Asia Pacific led the market, driven by strong automotive manufacturing bases across China, India, Japan, and South Korea.

U.S.

The market is estimated to reach USD 0.29 billion in 2026, supported by strong pickup, SUV, and aftermarket demand.

Japan

The market is estimated to reach USD 0.21 billion in 2026, driven by advanced engine technologies and a strong OEM presence.

Read More

AUTOMOTIVE PISTON PIN MARKET TRENDS

Increasing Adoption of Lightweight Engine Components to Improve Efficiency

Automotive manufacturers are increasingly focusing on lightweight engine components to enhance fuel efficiency and reduce emissions. This trend is encouraging the use of advanced materials such as high-strength steel alloys and coated piston pins that offer improved durability with reduced weight. As automakers continue to optimize internal combustion engines for better performance and regulatory compliance, catering to the increasing demand for fuel efficient vehicles, piston pin designs are evolving to support lower friction and enhanced load-bearing capabilities. These developments are shaping broader market trends, encouraging suppliers to invest in advanced manufacturing processes and material innovations.

- According to the U.S. Department of Energy, advanced lightweight and high strength materials significantly improve vehicle fuel efficiency while maintaining safety and performance. A 10% reduction in vehicle weight can improve fuel economy by approximately 6-8%. Replacing conventional steel and cast iron components with aluminum, magnesium alloys, high-strength steel, carbon fiber, and polymer composites can reduce body and chassis weight by up to 50%, lowering fuel consumption and enabling more efficient engine performance.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Global Vehicle Production to Support Component Demand

The steady increase in global passenger and commercial vehicle production is a key factor supporting automotive piston pin market growth. As automakers expand production to meet rising mobility needs and replacement demand in emerging markets, the requirement for reliable engine components continues to grow. Piston pins play a critical role in ensuring engine durability and smooth mechanical performance. With internal combustion engines still dominating the global vehicle fleet, suppliers are experiencing consistent product demand, particularly from OEM manufacturers seeking high-quality, precision-engineered components.

- According to OICA, in the first 3 quarters of 2025, vehicle production recorded 68.7 million units, up by 3.8% year on year, compared to the first three quarters' production volume of 2024.

MARKET RESTRAINTS

Increasing Shift toward Electrification of Vehicles May Hamper Market Growth

The gradual transition toward electric vehicles presents a restraint for the industry. Electric powertrains do not require traditional engine components such as pistons and piston pins, which may reduce long-term demand for these parts in fully electric vehicles. As governments promote electrification through incentives and stricter emission regulations, automakers are accelerating their EV development strategies. This transition could moderate the pace of expansion for internal combustion engine components during the forecast period, particularly in regions where electric vehicle adoption is advancing rapidly.

MARKET OPPORTUNITIES

Expansion of the Automotive Aftermarket for Engine Replacement Parts to Support Market Growth

The expanding global vehicle parc and aging fleet are creating strong opportunities in the automotive aftermarket. Older vehicles require regular engine maintenance and component replacement, which increases the demand for pistons pins and related engine parts. Independent repair workshops and aftermarket distributors are increasingly sourcing high-quality replacement components to ensure engine reliability and longevity. This trend presents a significant opportunity for manufacturers to strengthen distribution networks and capture additional automotive piston pin market share, particularly in developing regions where vehicle lifespans are relatively longer.

- In January 2026, Allied Motor Parts highlighted advancements in aftermarket pistons, emphasizing forged aluminum alloys, precision CNC machining, and advanced surface coatings to improve heat resistance, reduce friction, and enhance engine durability and performance.

MARKET CHALLENGES

Maintaining Precision and Durability under High Engine Stress to Propel Market Growth

Automotive piston pins must operate under extreme mechanical loads, high temperatures, and continuous friction within the engine assembly. Ensuring precision manufacturing and long-term durability while maintaining cost efficiency remains a major challenge for component manufacturers. Even minor dimensional inaccuracies can affect engine performance and reliability.

Segmentation Analysis

By Vehicle Type

High Global Passenger Car Production and Large Vehicle Parc to Support Passenger Cars Segment Growth

Based on vehicle type, the market is segmented into passenger cars, light commercial vehicles (LCVs), heavy commercial vehicles (HCVs), and 2-wheelers & 3-wheelers.

The passenger cars segment dominates the market due to its significant global vehicle production and large installed vehicle parc. Passenger cars account for majority of internal combustion engine vehicles worldwide, generating substantial demand for engine components such as piston pins. High usage rates, frequent engine servicing, and strong replacement cycles further support consistent component consumption. Additionally, OEM production volumes and extensive aftermarket maintenance requirements reinforce the segment’s strong market share and sustained demand.

- In 2025, according to OICA, passenger car production volume rose to 50.2 million units, from 47.6 million units, representing 5.5% growth year on year.

The 2-wheelers & 3-wheelers segment is projected to grow at the fastest CAGR of 5.1% during the forecast period. Rising two-wheeler ownership in emerging economies, expanding urban mobility demand, and cost-effective transportation solutions are increasing engine component replacement needs, supporting steady growth.

To know how our report can help streamline your business, Speak to Analyst

By Engine Type

Expanding Gasoline Engine Adoption to Strengthen Gasoline Engine Segment Leadership

Based on engine type, the market is segmented into gasoline engines and diesel engines.

The gasoline engines segment holds the largest market share due to its extensive use in passenger cars and two-wheelers across the global automotive market. Gasoline engines dominate light-duty vehicle production, particularly in urban mobility segments where efficiency, lower emissions, and smoother performance are prioritized. Continuous advancements in engine efficiency and lightweight component integration are further supporting the demand for precision engine parts such as piston pins. Strong OEM production volumes and consistent aftermarket replacement cycles sustain stable market demand.

- In May 2024, Toyota, Subaru, and Mazda announced the joint development of next-generation internal combustion engines optimized for electrification, featuring compact architectures, higher thermal efficiency, and compatibility with carbon-neutral fuels such as e-fuels, biofuels, and liquid hydrogen.

The diesel engines segment is expected to grow at the fastest CAGR of 5.0% during the forecast period. The increasing usage of diesel engines in commercial vehicles, logistics fleets, and heavy-duty transportation applications is supporting the demand for durable engine components capable of handling higher mechanical loads.

By Engine Configuration

Widespread Adoption of Compact and Cost-Efficient Engine Designs to Support Inline Engines Segment Growth

Based on engine configuration, the market is segmented into inline engines, V-type engines, and flat/boxer engines.

The inline engines segment dominates the market due to its widespread adoption across passenger cars, light commercial vehicles, and two-wheelers. Inline engine configurations are preferred for their compact design, lower manufacturing cost, and simplified mechanical structure. These engines are extensively used in mass-production vehicles, particularly in emerging automotive markets where cost efficiency and ease of maintenance are key priorities. As a result, consistent OEM production volumes and steady replacement cycles support the segment’s strong market share.

- In June 2024, Toyota announced next-generation 1.5-L and 2.0-L inline-four engines with compact architecture, shorter piston stroke, hybrid vehicles compatibility, and improved thermal efficiency, supporting carbon-neutral fuels and future electrified powertrains.

The flat/boxer engines segment is projected to grow at the fastest CAGR of 5.2% during the forecast period. The increasing adoption in high-performance and premium vehicles, where balanced engine operation and improved vehicle stability are essential, is driving the demand for specialized engine components, including piston pins.

By Piston Pin Type

Superior Load Distribution and Reduced Friction to Support Fully Floating Piston Pin Segment Dominance

Based on piston pin type, the market is segmented into fixed piston pin, semi-floating piston pin, and fully floating piston pin.

The fully floating piston pin segment holds the largest market share due to its ability to rotate freely within both the piston and connecting rod. This design reduces friction, distributes mechanical loads evenly, and improves engine durability under high operating stress. Fully floating piston pins are widely used in modern automotive engines, particularly in passenger cars and high-performance vehicles. Their reliability, enhanced lubrication efficiency, and compatibility with advanced engine designs support sustained adoption across OEM production and aftermarket replacement cycles.

The fixed piston pin segment is expected to grow at the fastest CAGR of 4.0% during the forecast period. The increasing adoption in compact and cost-sensitive engine designs, particularly in small vehicles and two-wheelers, is supporting steady demand for simpler and cost-effective piston pin configurations.

- In March 2026, Ferrari revealed a patented oblong piston engine design, enabling a wider piston surface and improved combustion efficiency, potentially increasing power density, optimizing valve placement, and enhancing high-performance engine airflow dynamics.

Automotive Piston Pin Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Piston Pin Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to its large automotive manufacturing base and rapidly expanding vehicle parc. Countries such as China, India, Japan, and South Korea are major automotive production hubs, supporting strong demand for engine components. Rising passenger vehicle ownership, increasing two-wheeler sales, and expanding commercial vehicle fleets further strengthen regional market growth. Additionally, the presence of leading automotive OEMs, cost-efficient manufacturing capabilities, and a well-established supplier ecosystem contribute to the region’s dominant market share during the forecast period.

- In December 2023, Abilities India secured a patent for an advanced piston–cylinder coating technology designed to reduce friction, enhance wear resistance, improve heat dissipation, and increase internal combustion engine durability and efficiency.

China Automotive Piston Pin Market

The China market is estimated to touch around USD 0.80 billion in 2026, accounting for roughly 31.7% of the global market revenues. Strong vehicle production, large passenger car volumes, and a robust automotive component supply chain sustain steady market demand and manufacturing expansion.

Japan Automotive Piston Pin Market

The Japan market is estimated to reach around USD 0.21 billion in 2026, accounting for roughly 8.3% of the global market revenues. Advanced engine engineering, strong OEM presence, and high-quality component manufacturing support stable demand and technological innovation.

India Automotive Piston Pin Market

The India market is estimated at around USD 0.22 billion in 2026, accounting for roughly 8.9% of the global market revenues. Rapid vehicle ownership growth, expanding two-wheeler production, and rising domestic automotive manufacturing support strong market growth.

Europe

Europe holds the third-largest market share due to the presence of premium automotive manufacturers and strong engineering expertise. Countries such as Germany, France, and Italy depict the presence of major vehicle manufacturers that emphasize high-performance and fuel-efficient engine technologies. These factors create consistent market demand for high-quality piston pins and related engine components. Additionally, Europe’s well-established automotive supply chain, strong export activities, and continued development of efficient internal combustion engines contribute to steady regional market growth.

- In March 2026, Renault announced a five-year strategy targeting 36 new vehicle models and annual sales of 2 million units by 2030, strengthening global production capacity and supporting sustained demand for internal combustion engine components.

Germany Automotive Piston Pin Market

The Germany market is estimated to reach around USD 0.10 billion in 2026, accounting for roughly 3.9% of the global market revenues. Strong automotive engineering capabilities, premium vehicle manufacturing, and established component suppliers sustain consistent OEM and aftermarket demand.

U.K. Automotive Piston Pin Market

The U.K. market is estimated to touch around USD 0.02 billion in 2026, accounting for roughly 0.7% of the global market revenues. The presence of specialized automotive manufacturing, performance vehicle production, and advanced engineering capabilities supports stable component demand.

North America

North America represents the second-largest market, supported by a strong automotive aftermarket and advanced engine manufacturing capabilities. The U.S. and Canada maintain a substantial vehicle parc requiring regular engine maintenance and replacement components. In addition, the region’s focus on high-performance vehicles, pickup trucks, and SUVs sustains consistent market demand for durable engine components. Investments in precision manufacturing, technological advancements in engine design, and established automotive supply chains further strengthen the regional market analysis and component consumption.

- In January 2025, Piston Automotive secured a USD 8.5 million state grant to build a 713,000-square-foot manufacturing plant in Michigan, supplying General Motors assembly operations and supporting large-scale automotive component logistics and production.

U.S. Automotive Piston Pin Market

The U.S. market is estimated to reach around USD 0.29 billion in 2026, accounting for roughly 11.1% of the global market revenues. Large vehicle parc, strong pickup and SUV production, and a mature automotive aftermarket sustain consistent demand.

Rest of the World

The market in the rest of the world is projected to grow at the fastest CAGR of 4.9% during the forecast period. Increasing vehicle production in Latin America, the Middle East, and Africa is supporting the rising demand for automotive engine components. Improving economic conditions, expanding urban mobility needs, and growing investments in automotive manufacturing facilities are contributing to regional expansion. Furthermore, the gradual development of automotive aftermarket networks and increasing vehicle ownership are expected to strengthen long-term growth opportunities in emerging markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Metallurgy, Precision Engineering, and OEM Partnerships Define Competitive Intensity

The automotive piston pin market is moderately fragmented, with several global and regional manufacturers competing through advanced metallurgy, precision machining, and strong OEM relationships. Key players such as Tenneco Inc., Shriram Pistons & Rings Ltd., Amsted Automotive, and Burgess-Norton Manufacturing Company focus on developing lightweight, high-strength piston pins to enhance engine durability and efficiency. To strengthen market share, companies are investing in advanced coating technologies, expanding manufacturing capabilities, and forming strategic supply agreements with automakers. Partnerships with OEMs and aftermarket distributors help optimize production efficiency and strengthen global supply networks.

LIST OF KEY AUTOMOTIVE PISTON PIN COMPANIES PROFILED

- MAHLE GmbH (Germany)

- Burgess-Norton Manufacturing Company (U.S.)

- Amsted Automotive (U.S.)

- Power Industries (India)

- Shriram Pistons & Rings Ltd. (India)

- Tenneco Inc. (U.S.)

- Ross Racing Pistons (U.S.)

- Jiashan Biguo Piston Pin Co., Ltd. (China)

- Menon Bearings Ltd. (India)

- Wellfar Engine Parts (China)

- Art-Serina Piston Co., Ltd. (Thailand)

KEY INDUSTRY DEVELOPMENTS

- October 2025: MAHLE introduced new aftermarket engine components at AAPEX 2025, including advanced pistons, rings, and filtration systems designed to improve engine efficiency, thermal stability, and durability for modern internal combustion engines.

- August 2025: Oak Ridge National Laboratory developed Dualumina, a 3D-printable aluminum alloy for high-temperature automotive components such as pistons, offering improved thermal stability, oxidation resistance, and mechanical strength in advanced engine environments.

- December 2024: MAHLE announced the development of advanced engine components for MAN Truck & Bus, including optimized pistons and related systems designed to improve combustion efficiency, thermal management, and durability in heavy-duty diesel engines.

- October 2024: Tenneco expanded its powertrain testing capabilities by integrating hydrogen internal combustion engine (H2-ICE) testing, enabling the validation of pistons, piston pins, rings, and bearings under hydrogen combustion conditions.

- December 2023: Rheinmetall announced the sale of its small-bore pistons business to Comitans Capital, aligning with its strategy to streamline operations while maintaining focus on advanced automotive technologies and powertrain solutions.

- February 2023: Shriram Pistons & Rings acquired a 75% stake in Japan’s Takahata Precision, expanding capabilities in precision injection-molded automotive components and strengthening global supply chains for advanced engine and powertrain parts.

- July 2021: Rheinmetall introduced low-friction, lightweight piston and piston pin technologies using optimized skirt coatings and reduced mass designs to lower mechanical losses, improve engine efficiency, and support stricter emission standards.

REPORT COVERAGE

The global automotive piston pin market analysis provides an in-depth study of the market size & forecast by all the market segmentation included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, By Engine Type, By Engine Configuration, By Piston Pin Type, and By Region |

| By Vehicle Type |

|

| By Engine Type |

|

| By Engine Configuration |

|

| By Piston Pin Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.54 billion in 2025 and is projected to reach USD 3.36 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.55 billion.

The market is expected to exhibit a CAGR of 3.2% during the forecast period of 2026-2034.

The passenger cars segment leads the market in terms of vehicle type.

The rising global vehicle production is a key factor driving the market.

Key players such as Tenneco Inc., Shriram Pistons & Rings Ltd., Amsted Automotive, and Burgess-Norton Manufacturing Company lead the market among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us