Automotive Service Market Size, Share & Industry Analysis, By Service Type (Periodic Maintenance Services, Wear & Tear Parts Replacement, Mechanical & Electrical Repairs, Diagnostics & Software-Related Services, and Body & Paint & Collision Repair Services), By Service Nature (Scheduled and Unscheduled), By Vehicle Type (Passenger Cars, LCVs, and HCVs), By Service Provider Type (Authorized OEM/Dealer Workshops, Independent Aftermarket Garages, and Specialist Service Chains), By Propulsion (ICE and Electric), and Regional Forecast, 2026-2034

Automotive Service Market Size & Industry Overview

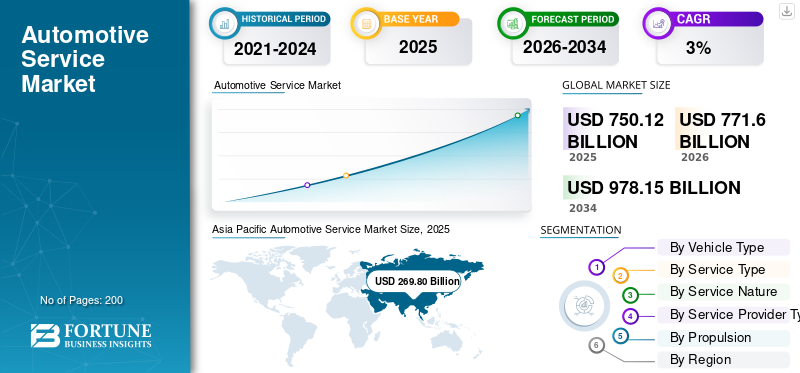

The global automotive service market size was valued at USD 750.12 billion in 2025. The market is projected to grow from USD 771.60 billion in 2026 to USD 978.15 billion by 2034, exhibiting a CAGR of 3.0% during the forecast period. Asia Pacific dominated the automotive service market with a market share of 35.97% in 2025.

Automotive service refers to the inspection, maintenance, repair, and replacement of vehicle components to ensure optimal performance. It also encompasses the services pertaining to safety, reliability, and compliance with manufacturers as per regulatory standards. Key market drivers such as rising demand, technological advancements, regulatory support, cost efficiency, and changing consumer preferences actively stimulate market growth and expansion.

Major players in the market include leading manufacturers and service providers such as Robert Bosch GmbH, Bridgestone Corporation, Michelin Group, Mobivia Groupe, and Goodyear Tire & Rubber Company, among others. These companies compete through advanced equipment technologies, digital diagnostics integration, automation, improved service efficiency, and compliance with evolving safety and emission standards.

Download Free sample to learn more about this report.

Automotive Service Market Key Takeaways

- 2025 Market Size: USD 750.12 Billion

- 2026 Market Size: USD 771.60 Billion

- 2034 Forecast Market Size: USD 978.15 Billion

- CAGR: 3.0% from 2026–2034

- Asia Pacific dominated the automotive service market with a 35.97% share in 2025.

- The light commercial vehicles segment is the fastest-growing, expanding at a CAGR of 4.0% during the forecast period.

- Diagnostics and software-related services represent the fastest-growing service segment, expanding at a CAGR of 4.9%.

Asia Pacific

Asia Pacific is the largest and fastest-growing market, driven by rising vehicle ownership and expanding service networks.

North America

North America is the second-largest market, supported by a mature automotive ecosystem and aging vehicle fleet.

Europe

Europe holds the third-largest market share, driven by strict safety regulations and preventive maintenance practices.

U.S.

The market is estimated to reach USD 170.69 billion in 2026, accounting for roughly 22.1% of global revenue.

Japan

The market is estimated to reach USD 45.37 billion in 2026, representing approximately 5.9% of global revenue.

Read More

AUTOMOTIVE SERVICE MARKET TRENDS

Digitalization and Connected Workshop Solutions to Shape Market Trends

Digitalization and connected technologies are key market trends shaping the automotive repair and maintenance services industry. Modern equipment increasingly integrates with cloud connectivity, data analytics, and software-based diagnostics to improve accuracy and efficiency. Connected workshop solutions enable predictive maintenance, remote updates, and real-time performance monitoring. Integration with workshop management platforms improve workflow transparency and resource utilization, influencing purchasing decisions across OEM-authorized service centers and independent service centers. This occurs, since workshops today pursue higher productivity, lower downtime, and improved customer experience levels consistently on a global level.

- For instance, in July 2024, East Auto showcased new advanced diagnostic systems, digital service workflows, and connected workshop tools aimed at enhancing repair accuracy, reducing turnaround times, and integrating software-driven maintenance for modern vehicles.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Vehicle Parc and Aging Fleet to Drive Service Equipment Demand

The continuous rise in the global vehicle parc, combined with an aging fleet, is a key driver for the automotive service market growth. Older vehicles require more frequent inspection, maintenance, and component replacement which leads to an increase in workshop visits. This directly boosts demand for automotive service equipment such as lifts, diagnostics, and fluid management systems. Additionally, higher vehicle ownership rates in urban and semi-urban areas are expanding the installed base of service centers, further supporting sustained market growth worldwide over the long term and across regions.

- In April 2025, SIAM data showed India produced 31.0 million vehicles in fiscal year 2024–25, up from 28.4 million; domestic vehicle sales reached 25.6 million units, including 19.6 million two-wheelers and 4.3 million passenger vehicles, expanding the number of vehicles on the road and long-term service demand.

MARKET RESTRAINTS

High Initial Investment and Maintenance Costs to Restrain Adoption of Modern Technologies

Automotive service often involves high upfront capital expenditure, particularly for advanced diagnostic systems, automated lifts, precision alignment equipment and technical training. Small and independent workshops frequently face budget limitations, restricting their ability to invest in modern technologies. In addition, recurring expenses related to calibration, software licensing, and routine maintenance increase total ownership costs. These financial pressures slow replacement cycles, delay technological upgrades, and ultimately restrain broader market penetration across cost-sensitive regions, limiting overall investment momentum further significantly.

MARKET OPPORTUNITIES:

Rising Electrification and ADAS Complexity to Create Growth Opportunities

Rising electrification and increasing integration of advanced driver assistance systems are creating strong growth opportunities for the market. Electric and hybrid vehicles require specialized diagnostic tools, battery servicing equipment, and enhanced safety infrastructure within workshops. Similarly, ADAS-equipped vehicles demand precise calibration systems and software-driven alignment solutions. Service providers that proactively upgrade capabilities can access new revenue streams, differentiate offerings, and strengthen competitiveness as adoption accelerates across passenger and commercial vehicle service ecosystems globally.

- In June 2023, at Automechanika Birmingham, Launch Tech UK showcased its latest ADAS calibration and diagnostic tools, including ADAS Pro+ and ADAS Mobile, attracting thousands of garages and technicians and highlighting rising workshop demand for advanced calibration solutions.

MARKET CHALLENGES

Skilled Labor Shortage and Training Requirements to Challenge Market Adoption

Shortage of skilled technicians and rising training requirements present a critical challenge for the market. Advanced automotive service demands expertise in electronics, software diagnostics, EV systems, and ADAS calibration. Many service centers struggle to continuously upskill their workforce due to time and cost constraints. Insufficient technical proficiency may limit equipment utilization, reduce service quality, and weaken return on investment. This challenge persists despite growing demand in the automotive service market across both independent and OEM-authorized workshops, particularly during rapid technological advancements and transition phases that are increasingly visible across the industry.

Automotive Service Market Segmentation Analysis

By Vehicle Type

Extensive Passenger Car Parc and High Service Frequency to Lead the Segment

Based on vehicle type, the market is segmented into passenger cars, LCVs, and HCVs.

The passenger cars segment dominates the market due to its extensive global vehicle parc and consistent servicing requirements. Routine maintenance activities such as tire replacement, wheel alignment, lifting operations, diagnostics, and fluid management drive continuous equipment utilization. High ownership levels across urban and semi-urban areas, coupled with widespread use in personal mobility and shared fleets, sustain strong aftermarket demand. Service centers prioritize passenger-car-compatible equipment, supporting steady replacement cycles and incremental technological upgrades rather than disruptive shifts.

- According to OICA, around 67.5 million passenger cars were sold in 2024, representing a growth of 3% compared to 2023.

The light commercial vehicles segment is the fastest-growing, expanding at a CAGR of 4.0% over the forecast period. The segment’s growth is driven by rising e-commerce activity, last-mile delivery expansion, and increasing urban logistics fleets, which intensify servicing frequency and demand for durable, higher-capacity service equipment.

By Service Type

High Replacement Frequency and Predictable Maintenance Cycles to Dominate Wear & Tear Parts Replacement Segment

Based on service type, the market is segmented into periodic maintenance services, wear & tear parts replacement, mechanical & electrical repairs, diagnostics & software-related services, body & paint & collision repair services.

The wear & tear parts replacement segment dominates the market due to the recurring nature of component degradation and routine maintenance requirements. Frequent replacement of tires, brakes, filters, fluids, and suspension components ensures consistent workshop activity and sustained utilization of service equipment. The predictable servicing cycles associated with wear prone parts support steady aftermarket volumes across vehicle categories. Service centers continue prioritizing equipment that supports high-throughput replacement tasks, reinforcing long-term segmental dominance.

Diagnostics and software-related services segment represents the fastest-growth, expanding at a CAGR of 4.9% during the forecast period. Increasing vehicle electrification, software-driven architectures, and ADAS integration are accelerating demand for advanced diagnostic tools, calibration systems, and regular software updates across modern vehicle fleets.

- In November 2025, Revv raised USD 20 million to expand its AI-driven auto repair platform, enhancing predictive diagnostics, repair estimates, and workflow automation to streamline shop operations and improve customer service.

To know how our report can help streamline your business, Speak to Analyst

By Service Nature

Scheduled Services Dominate Due to Preventive Maintenance Emphasis and OEM-Advised Intervals

By service nature, the market is divided into scheduled and unscheduled.

Scheduled services dominate the market due to increasing emphasis on preventive maintenance and adherence to OEM-recommended service intervals. Regular inspections, fluid changes, diagnostics, and component checks drive predictable workshop visits and consistent equipment utilization. Rising vehicle complexity and warranty-linked servicing further encourage scheduled maintenance adoption. Additionally, fleet operators and mobility service providers increasingly rely on planned servicing to minimize downtime, making scheduled services both the largest and fastest-growing service in the market.

- In August 2024, West Coast Tire & Services expanded its auto repair operations into the San Clemente market, adding comprehensive maintenance, tire, and diagnostic services to strengthen its regional service footprint.

Unscheduled services are anticipated to grow at a CAGR of 2.8% over the forecast period. This segment’s demand is primarily driven by unexpected breakdowns, accident repairs, and component failures, supporting steady but comparatively slower growth than planned maintenance activities.

By Service Provider Type

Broad Service Coverage and Cost Competitiveness to Anchor Independent Aftermarket Garages’ Dominance

By service provider type, the market is categorized into authorized OEM/dealer workshops, independent aftermarket garages, and specialist service chains.

Independent aftermarket garages dominate due to their widespread presence, cost-competitive service offerings, and ability to cater to diverse vehicle brands and models. These garages handle high volumes of routine maintenance, wear and tear replacements, and basic diagnostics, ensuring steady utilization of service equipment. Strong penetration across urban and semi-urban regions, coupled with customer preference for flexible pricing and quicker turnaround times, reinforces their dominant market share and sustained equipment demand.

Specialist service chains are the fastest-growing segment, expanding at a CAGR of 4.1% during the forecast period. The segment’s growth is driven by standardized service quality, advanced diagnostic capabilities, and increasing consumer trust in branded, multi-location service networks.

- In September 2024, Clays Automotive Service Center launched a specialized transmission repair service, expanding its maintenance portfolio with expert diagnostics, advanced repair capabilities, and trained technicians to address growing demand for complex drivetrain servicing in passenger vehicles.

By Propulsion

Extensively Installed Vehicle Base and Established Servicing Infrastructure to Sustain ICE Segment Dominance

By propulsion, the market is bifurcated into ICE and electric.

The ICE segment dominates the market due to its large installed vehicle base and well-established servicing ecosystem. Internal combustion engine vehicles require frequent maintenance, including oil changes, exhaust servicing, diagnostics, and mechanical repairs, resulting in consistent workshop visits. Extensive availability of trained technicians and compatible service equipment further supports high utilization rates. Despite gradual electrification, internal combustion engine ICE vehicles continue to generate significant aftermarket activity, reinforcing their dominance in market revenues.

Electric is the fastest-growing segment, registering a CAGR of 8.8% over the forecast period. Rapid EV adoption is driving demand for specialized diagnostics, battery servicing equipment, and high-voltage safety tools across service networks in the automotive sector.

- In 2024, the International Energy Agency reported global electric car sales exceeded 17 million, accounting for over 20% of all new cars sold worldwide, with China dominating and EVs continuing strong growth.

Automotive Service Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Service Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is also the fastest-growing region owing to rapid vehicle parc expansion, rising urbanization, and growing middle-class income levels. Increasing ownership of passenger cars and light commercial vehicles is driving higher servicing frequency. The region also benefits from a dense network of independent garages, expanding service as well as supply chains. Strong growth rate in the adoption of electric vehicles and digital diagnostics further accelerates equipment demand.

- In July 2024, East Auto showcased new advanced diagnostic systems, digital service workflows, and connected workshop tools aimed at enhancing repair accuracy, reducing turnaround times, and integrating software-driven maintenance for modern vehicles.

China Automotive Service Market

China is estimated to reach around USD 106.74 billion in 2026, accounting for roughly 13.8% of global market revenue, driven by a massive vehicle parc, dense garage networks and high servicing frequency.

Japan Automotive Service Market

Japan is estimated to reach around USD 45.37 billion in 2026, accounting for roughly 5.9% of the global market revenue, supported by an aging vehicle fleet, strict inspection norms, and a scheduled maintenance culture.

India Automotive Service Market

The Indian market is estimated at around USD 64.40 billion in 2026, accounting for roughly 8.3% of global market revenue, owing to rapid vehicle ownership growth, expanding urban garages, and rising preventive servicing adoption.

North America

North America represents the second-largest automotive service market share, growing at a CAGR of 2.3% over the forecast period. The region’s well-established automotive ecosystem, high vehicle ownership per capita, and aging vehicle fleet support consistent service and replacement demand. Advanced workshop infrastructure and high penetration of diagnostic and alignment equipment sustain revenues. Growth remains steady, as market maturity limits new installations, with demand largely driven by equipment upgrades and technological replacements across service centers.

- In April 2025, Launch Tech USA introduced AI-powered PredictaFix integration into its diagnostic tools, using CarTechIQ’s AI to analyze DTCs, prioritize root causes, and offer precise repair suggestions, accelerating diagnostics and improving first-time fix accuracy.

U.S. Automotive Service Market

The U.S. is estimated to achieve USD 170.69 billion in 2026, accounting for roughly 22.1% of global market revenue, supported by high vehicle ownership, mature workshop infrastructure, and steady replacement-driven servicing demand.

Europe

Europe accounts for the third-largest market share, driven by strict vehicle safety regulations, emission norms, and a strong preventive maintenance culture. High penetration of scheduled servicing and regular inspections sustain demand for diagnostics, alignment, and testing equipment. The region also showcases growing adoption of electric vehicles, increasing the need for specialized service tools. However, slower vehicle parc growth and economic uncertainties in select countries moderate overall market expansion compared to Asia Pacific.

- In May 2024, Eurorepar Car Service, operated by Stellantis, reported continued double-digit global growth, driven by network expansion, rising multi-brand servicing demand, and strengthened parts availability across Europe, Latin America, and emerging automotive service markets.

Germany Automotive Service Market

Germany is estimated to hit USD 31.90 billion in 2026, accounting for roughly 4.1% of the global revenue, supported by strong regulatory compliance, advanced diagnostics usage, and high scheduled servicing penetration.

U.K. Automotive Service Market

The U.K. will account for USD 25.79 billion in 2026, which represents 3.3% of global revenue, driven by an aging vehicle fleet, strong aftermarket networks, and growing digital diagnostics adoption.

Rest of the World

The rest of the world is witnessing gradual growth supported by increasing motorization, improving service infrastructure, and expanding vehicle fleets across Latin America, the Middle East, and Africa. Their growth is driven by rising demand for basic maintenance and repair services as vehicle ownership increases. Although equipment penetration remains lower than in developed regions, investments in organized service centers and expanding urban mobility are steadily improving long term market potential.

- In July 2025, Stellantis Middle East launched the Zofeur pick-up and drop-off service, enhancing customer convenience by enabling seamless vehicle maintenance through doorstep collection, servicing, and return across selected regional markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Product-Service Ecosystem Integration and Network Expansion to Shape Competitive Intensity

The market features a moderately fragmented competitive landscape, structured around a mixed product and service ecosystem. Competition spans global service network operators, aftermarket distributors, and technology and equipment providers. Leading players such as Robert Bosch GmbH, Bridgestone Corporation, Michelin Group, Mobivia Groupe, and Goodyear Tire & Rubber Company, among others, compete through service network expansion, bundled maintenance offerings, advanced diagnostics, EV- and ADAS-ready solutions, and digital workflow integration. Tire-led service companies leverage recurring replacement demand, while technology-focused players strengthen positioning through software-enabled platforms and training support. Strategic partnerships, acquisitions, and localization strategies remain key to expanding geographic reach and addressing diverse vehicle servicing requirements across mature and emerging markets.

- In September 2025, Bosch introduced an AI-enabled diagnostic platform for multi-brand workshops, enabling faster fault detection, remote software updates, and improved compatibility with electric and software-defined vehicles, enhancing productivity for independent and authorized service centers globally.

LIST OF KEY AUTOMOTIVE SERVICE COMPANIES PROFILED:

- Robert Bosch GmbH (Germany)

- Bridgestone Corporation (Japan)

- Michelin Group (France)

- Mobivia Groupe (France)

- Goodyear Tire & Rubber Company (U.S.)

- Snap-on Incorporated (U.S.)

- 3M Company (U.S.)

- ZF Friedrichshafen AG (Germany)

- Continental AG (Germany)

- LKQ Corporation (U.S.)

- Genuine Parts Company (U.S.)

- AutoZone, Inc. (U.S.)

- O’Reilly Automotive, Inc. (U.S.)

- Driven Brands Holdings Inc. (U.S.)

- Belron International Ltd. (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- January 2026: Bemer Motor Cars launched a newly redesigned website featuring improved navigation, enhanced service scheduling tools, and expanded vehicle information, aiming to strengthen customer engagement and streamline access to sales and automotive service offerings.

- December 2025: ASE and WrenchWay launched ASE Connects, a digital platform designed to address the automotive technician shortage by connecting employers, educators, and technicians, while promoting certification awareness, career pathways, and workforce development across the automotive service industry.

- October 2025: Slate Auto partnered with RepairPal to integrate verified repair and maintenance services into its digital platform, enhancing transparency, trusted service access, and customer convenience for vehicle owners seeking reliable automotive maintenance solutions.

- September 2025: Instant Car Fix launched a technology-driven automotive repair platform, enabling digital service bookings, transparent pricing, and streamlined workshop coordination, aimed at improving customer experience and operational efficiency in vehicle maintenance and repair services.

- July 2025: ServiceUp raised USD 55 million to expand its digital platform for fleet vehicle repairs, aiming to simplify maintenance workflows, improve repair transparency, and enhance efficiency for commercial fleet operators and service providers.

- February 2025: Stellantis announced plans to launch a mobile repair service program 2025, enabling on-site vehicle repairs and maintenance, aimed at improving customer convenience, reducing workshop visits, and supporting evolving service delivery models.

- December 2024: AAPEX 2024 highlighted innovations driving the global automotive aftermarket forward, showcasing advancements in diagnostics, EV servicing, digital tools, and supply chains solutions, while bringing together global manufacturers, service providers, and technology leaders to address evolving maintenance and repair needs.

REPORT COVERAGE

The global automotive service market analysis provides an in-depth study of the market size & forecast by all segments. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.0% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type, Vehicle Type, Service Nature, Service Provider Type, Propulsion, and Region |

|

By Vehicle Type |

|

|

By Service Type |

|

|

By Service Nature |

|

|

By Service Provider Type |

|

|

By Propulsion |

|

|

By Geography |

North America (By Service Type, By Vehicle Type, By Service Nature, By Service Provider Type, By Propulsion, and By Country)

Europe (By Service Type, By Vehicle Type, By Service Nature, By Service Provider Type, By Propulsion, and By Country)

Asia Pacific (By Service Type, By Vehicle Type, By Service Nature, By Service Provider Type, By Propulsion, and By Country)

Rest of the World (By Service Type, By Vehicle Type, By Service Nature, By Service Provider Type, and By Propulsion) |

Frequently Asked Questions

As per Fortune Business Insights, the global market value stood at USD 750.12 billion in 2025 and is projected to reach USD 978.15 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 269.80 billion.

The market is expected to exhibit a CAGR of 3.0% during the forecast period of 2026-2034

The passenger cars segment leads the market in terms of vehicle type.

Expanding vehicle parc and aging fleet to drive service equipment demand.

Key players in the market include Robert Bosch GmbH, Bridgestone Corporation, Michelin Group, Mobivia Groupe, and Goodyear Tire & Rubber Company, among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us