Automotive Silicone Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUV, LCV and HCV), By Product Type (Silicon Elastomers, Silicone, Adhesives & Sealants, Silicone Fluids, Silicone Resins and Silicone Gels & Foam), By Application (Powertrain & Engine Components, Electrical & Electronics, Interior Applications, Exterior Applications and Thermal Management Systems), By Propulsion (ICE and Electric), and Regional Forecasts, 2026-2034

Automotive Silicone Market Size and Future Outlook

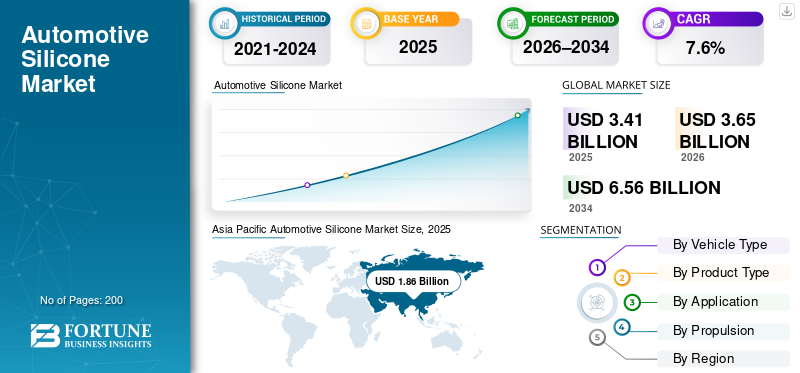

The global automotive silicone market size was valued at USD 3.41 billion in 2025. The market is projected to grow from USD 3.65 billion in 2026 to USD 6.56 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period. Asia Pacific dominated the Automotive silicone market with a market share of 54.55% in 2025.

The automotive silicone market represents the demand for silicone-based materials used across a wide range of automotive applications, including sealing, bonding, insulation, thermal management, and vibration control. These materials, such as elastomers, adhesives & sealants, fluids, resins, and gels, are valued for their thermal stability, durability, and superior electrical insulation properties, making them essential to modern vehicle design.

Growth of the automotive silicone industry is closely linked to rising vehicle production, increasing electronics integration, and the demand for high-performance materials within the automotive sector. Silicone materials are increasingly used in powertrain systems, battery packs, infotainment modules, sensors, and lighting systems, where resistance to heat, chemicals, and aging is critical. Their ability to maintain performance under extreme operating conditions supports long-term reliability and safety.

The market is growing, supported by electrification trends, stricter emission regulations, and the need for lightweight yet durable materials. Automakers are focusing on improving energy efficiency and component lifespan, driving the demand for silicones in gaskets, hoses, coatings, and thermal interface materials. Additionally, the shift toward advanced driver assistance systems (ADAS) and connected vehicles is accelerating silicon usage in electronic assemblies.

Key players in the global automotive silicone market, such as Wacker Chemie, KCC Corporation, and Henkel, are investing in advanced material R&D, expanding EV-focused product portfolios, and strengthening regional manufacturing and distribution networks. They are also partnering closely with OEMs and Tier-1 suppliers to develop application-specific silicone solutions for thermal management, sealing, and electronics protection.

Download Free sample to learn more about this report.

AUTOMOTIVE SILICONE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.41 Billion

- 2026 Market Size: USD 3.65 Billion

- 2034 Forecast Market Size: USD 6.56 Billion

- CAGR: 7.6% from 2026–2034

- Asia Pacific dominated the automotive silicone market with a 54.55% share in 2025.

- Silicone elastomers dominated the market due to their extensive use in gaskets, hoses, and insulation components.

- Hatchback/Sedan vehicles accounted for the largest share of automotive silicone demand globally.

Asia Pacific

Asia Pacific generated USD 1.86 billion in 2025 and maintained its position as the largest regional market.

North America

North America reached USD 0.66 billion in 2025, making it the second-largest regional market.

Europe

Europe is projected to reach USD 0.54 billion in 2026, growing at a CAGR of 7.4%.

U.S.

The automotive silicone market was valued at approximately USD 0.52 billion in 2025, representing 15.2% of global revenue.

Japan

Demand is supported by the country's advanced automotive manufacturing sector and increasing adoption of electric vehicle technologies.

Read More

AUTOMOTIVE SILICONE MARKET TRENDS

Shift Toward Advanced Thermal and Electrical Silicone Solutions

A key trend shaping market dynamics is the growing use of silicones for thermal management and electrical insulation. Automakers are prioritizing materials that enhance safety and efficiency in compact electronic architectures, supporting long-term growth of advanced silicone grades.

- For instance, Momentive Performance Materials highlights increased demand for thermal interface silicones in EV platforms.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Performance and Electrification-Ready Materials Drives Market Growth

The increasing demand for high-performance materials in the automotive sector is a major driver for the automotive silicone market size. Silicone’s ability to withstand extreme temperatures, vibration, and chemical exposure makes it indispensable for electrified and electronics-rich vehicles. As automakers enhance reliability and safety standards, silicone adoption across critical systems continues to rise.

- For instance, the IEA (International Energy Agency) highlights growing silicone usage in EV thermal and electrical systems as electrification accelerates globally.

MARKET RESTRAINTS

Volatility in Raw Material Prices Limits Short-Term Profitability

Fluctuating prices of silicon metal and energy inputs create cost instability for silicone manufacturers, restraining short-term market growth. These price variations can disrupt procurement planning and affect margins, particularly for suppliers with limited pricing flexibility. Such volatility adds uncertainty to long-term contracts in the automotive silicone industry.

- For instance, silicon metal price volatility has been cited as a cost challenge by chemical producers.

MARKET OPPORTUNITIES

Expansion of Electric and Hybrid Vehicles Unlocks New Silicon Applications

The rapid growth of electric and hybrid vehicles presents a strong opportunity for the global automotive silicone market. EVs require significantly higher silicone content for battery sealing, power electronics, and thermal control. This shift enables suppliers to introduce premium formulations and expand value per vehicle.

- For instance, Elkem ASA reports increasing demand for EV-focused silicone materials.

MARKET CHALLENGES

Balancing Performance Requirements with Cost Pressures

Meeting increasingly stringent performance specifications while controlling costs remains a challenge for the automotive silicone industry. OEMs demand high durability and compliance with regulatory standards, but cost sensitivity in mass-market vehicles can limit the adoption of premium silicone solutions.

- For instance, Automotive suppliers continue to face cost-performance trade-offs amid rising material standards.

Segmentation Analysis

By Vehicle Type

Large Production Base and Widespread Use of Hatchback/Sedan Leads the Segmental Growth

To know how our report can help streamline your business, Speak to Analyst

On the basis of vehicle type, the market is divided into Hatchback/Sedan, SUV, LCV, and HCV.

Hatchback and sedan vehicles dominate silicone demand due to their large global production base and widespread use across developed and emerging markets. These vehicles require silicones for sealing, vibration damping, and thermal protection, supporting steady growth.

- For instance, hatchbacks and sedans continue to account for the largest share of the global vehicle production parc.

The SUV segment is expected to grow at a CAGR of 9.3% over the forecast period.

By Product Type

Versatile Performance of Silicone Elastomers Fuels Segmental Growth

Based on product type, the market is segmented into silicon elastomers, silicone, adhesives & sealants, silicone fluids, silicone resins, and silicone gels & foam.

Silicone elastomers dominate due to flexibility, heat resistance, and long service life. Their extensive use in gaskets, hoses, and insulation components drives consistent demand growth.

- For instance, automotive-grade elastomers are widely used due to durability and heat resistance, as highlighted by Wacker Chemie AG in its automotive materials portfolio.

Silicon gels & foams is growing at a CAGR of 9.7% over the forecast period.

By Application

Critical Functional Role Drives Powertrain and Engine Segmental Dominance

Based on application, the market is segmented into powertrain & engine components, electrical & electronics, interior applications, exterior applications, and thermal management systems.

Powertrain and engine components rely heavily on silicones for sealing and heat resistance. Despite electrification, ICE and hybrid systems continue to sustain strong silicone demand.

- For instance, silicone materials remain critical in powertrain sealing and thermal applications, as emphasized in automotive material solutions by Dow Inc.

The thermal management systems segment is expected to grow at a CAGR of 10.8% over the forecast period.

By Propulsion

Large Global Fleet and Ongoing Production of ICE Vehicles Boosts Segment’s Growth

On the basis of propulsion, the market is segmented into ICE and Electric.

ICE vehicles dominate due to their large global fleet and ongoing production, sustaining demand for silicones in engines, exhaust systems, and drivetrains.

- For instance, the European Automobile Manufacturers’ Association (ACEA) reports that internal combustion vehicles still dominate the global vehicle fleet.

The electric segment is expected to grow at a CAGR of 12.4% over the forecast period.

Automotive Silicone Market Regional Outlook

By region, the global automotive silicone market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Automotive Silicone Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 1.86 billion, and also maintained the leading share in 2024, with USD 1.77 billion. Asia Pacific dominates the global automotive silicone market due to its large-scale vehicle production, expanding EV manufacturing, and strong regional supply chain ecosystem. Countries such as China, India, and South Korea drive sustained demand for silicones across powertrain, electronics, and thermal applications.

- For instance, in 2024, China’s EV production growth continues to boost demand for automotive materials.

China Automotive Silicone Market

China’s automotive silicone market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 1.15 billion, representing roughly 33.7% of the market.

India Automotive Silicone Market

India automotive silicone market in 2025 is estimated at around USD 0.23 billion, accounting for roughly 6.7% of global revenues.

Europe

Europe is projected to record a growth rate of 7.4% in the coming years, which is the second highest among all regions, and reach a valuation of USD 0.54 billion by 2026. Europe’s automotive silicone demand is driven by stringent emission regulations and the region’s focus on vehicle safety and efficiency. Automakers increasingly rely on silicone materials for durability and thermal stability, supporting moderate but consistent market expansion across passenger and commercial vehicles.

Germany Automotive Silicone Market

The German automotive silicone market in 2025 is estimated at around USD 0.18 billion, accounting for roughly 5.3% of global revenues.

U.K. Automotive Silicone Market

The U.K. automotive silicone market in 2025 is estimated at around USD 0.11 billion, accounting for roughly 3.2% of global revenues.

North America

North America is estimated to reach USD 0.66 billion in 2025 and secure the position of the second-largest region in the market. The North America automotive silicone market is expected to grow steadily, supported by higher silicone usage per vehicle and rising adoption of advanced automotive applications. Strong R&D capabilities and early adoption of electrified platforms support value growth. The U.S. market, in particular, benefits from increasing use of silicone-based thermal and electrical insulation materials in EVs and premium vehicles.

U.S. Automotive Silicone Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.52 billion, representing roughly 15.2% of the market.

Rest of the World

The rest of the world market is expected to grow gradually due to rising vehicle ownership, localized manufacturing expansion, and improving automotive infrastructure. Emerging markets in Latin America and the Middle East contribute to incremental demand, particularly for durable silicone materials used in harsh operating environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation-Driven Competition Shapes Long-Term Market Positioning

The competitive landscape of the global automotive silicone market is characterized by the presence of multinational chemical companies and specialty material suppliers focusing on innovation, scale, and long-term OEM partnerships. Key players compete by expanding automotive-grade product portfolios, strengthening regional manufacturing footprints, and launching application-specific silicone solutions.

Leading companies invest heavily in R&D to develop materials that meet evolving thermal, electrical, and durability requirements. Strategic collaborations with OEMs and Tier-1 suppliers help manufacturers embed their products deeper into vehicle platforms. Sustainability initiatives, such as low-VOC formulations and energy-efficient production processes, are also becoming differentiators.

Mergers, acquisitions, and product launches are frequently used to gain access to advanced technologies and emerging markets. Players with strong global supply chain networks benefit from faster response times and localized customer support, giving them a competitive edge in high-volume automotive programs.

- For instance, in 2024, Wacker Chemie AG expanded its automotive silicone portfolio for EV battery applications, focusing on thermal management and durability.

LIST OF KEY AUTOMOTIVE SILICONE COMPANIES PROFILED

- Dow Inc. (U.S.)

- Wacker Chemie AG (Germany)

- Elkem ASA (Norway)

- Shin-Etsu Chemical (Japan)

- KCC Corporation (South Korea)

- Henkel AG & Co. KGaA (Germany)

- 3M Company (U.S.)

- B. Fuller (U.S.)

- Sika AG (Switzerland)

- Bluestar (China)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Brenntag signed a new distribution agreement that broadens access to Momentive’s silicone and specialty portfolio (e.g., CoatOSil additives, Silquest silanes) for coatings/adhesives/sealants customers in the Philippines, extending earlier SEA coverage. This strengthens downstream availability of silicone chemistries used across automotive applications and industrial supply chains.

- September 2025: Dow introduced DOWSIL EG-4175 Silicone Gel designed for next-gen IGBT modules, emphasizing temperature resistance up to 180°C alongside dielectric protection, important as EV architectures move toward higher voltage systems. This is a classic silicone value-add in EV inverters and related power electronics packaging.

- September 2025: Wacker Chemie AG showcased next-generation thermally conductive silicone adhesives for EV battery assembly at The Battery Show, targeting improved heat dissipation and long-term durability in electrified vehicles.

- September 2025: Momentive Performance Materials expanded its European silicone elastomers distribution partnership with Safic-Alcan, improving regional availability of automotive-grade silicone materials for molding and sealing applications.

- October 2024: Dow Inc. partnered with Carbice to co-develop advanced thermal interface materials combining silicones and carbon nanotube technology for automotive electronics and electric vehicle thermal management systems.

- October 2024: Elkem ASA highlighted its silicone-based battery thermal management and insulation solutions at The Battery Show North America, addressing heat dissipation and safety requirements in electric vehicle battery packs.

- May 2024: KCC Corporation completed the full acquisition of Momentive Performance Materials, strengthening its global silicone portfolio and expanding capabilities across automotive, electronics, and specialty materials markets.

REPORT COVERAGE

The global automotive silicone market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, Product Type, Application, Propulsion, and Region |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · LCV · HCV |

|

By Product Type |

· Silicon Elastomers · Silicone Adhesives & Sealants · Silicone Fluids · Silicone Resins · Silicone Gels & Foam |

|

By Application |

· Powertrain & Engine Components · Electrical & Electronics · Interior Applications · Exterior Applications · Thermal Management Systems |

|

By Propulsion |

· ICE · Electric |

|

By Region |

· North America (By Vehicle Type, Product Type, Application, Propulsion, and Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, Product Type, Application, Propulsion, and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, Product Type, Application, Propulsion, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Vehicle Type, Product Type, Application, Propulsion, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.41 billion in 2025 and is projected to reach USD 6.56 billion by 2034.

In 2025, the market value stood at USD 1.86 billion.

The market is expected to exhibit a CAGR of 7.6% during the forecast period of 2026-2034.

The hatchback/Sedan segment led the market by vehicle type.

Rising demand for high-performance and electrification-ready materials is driving the global automotive silicone market.

Dow, KCC Corporation, Wacker Chemie and H.B. Fuller are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us