Automotive Subframe Market Size, Share & Industry Analysis, By Subframe Position (Front Subframe and Rear Subframe), By Vehicle Type (Hatchback/Sedan, SUV, Light Duty Vehicle, and Heavy Duty Vehicle), By Material Type (Steel Subframes, Aluminum Subframes, and Others), By Propulsion (ICE, HEV, and EV), By Drive Type (Front-Wheel Drive, Rear-Wheel Drive, and All-Wheel Drive), and Regional Forecast, 2026-2034

Automotive Subframe Market Size & Future Outlook

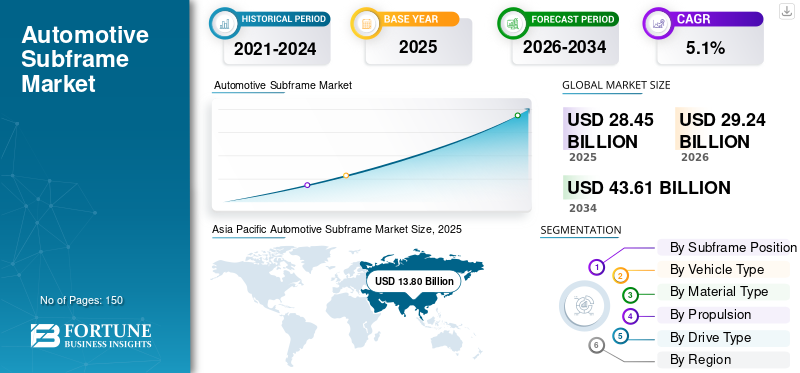

The global automotive subframe market size was valued at USD 28.45 billion in 2025. The market is projected to grow from USD 29.24 billion in 2026 to USD 43.61 billion by 2034, exhibiting a CAGR of 5.1% during the forecast period. Asia Pacific dominated the global automotive subframe market with a market share of 48.50% in 2025.

The automotive subframe market refers to the global industry engaged in the development, manufacturing, and supply of structural subframe assemblies used in passenger and commercial vehicles. Subframes are load-bearing components mounted to the vehicle body or unibody structure, designed to support critical systems, including the engine, transmission, suspension, and steering assemblies. These components play a vital role in enhancing structural rigidity, mitigating vibration and noise, and facilitating the development of modular vehicle architectures. The market primarily serves Original Equipment Manufacturers (OEMs), with limited participation from the aftermarket, and spans multiple vehicle categories, including passenger cars, light commercial vehicles, and electric vehicles, where subframe designs are increasingly optimized for weight reduction and packaging efficiency.

The market is characterized by the presence of established Tier 1 automotive suppliers with strong capabilities in metal forming, welding, casting, and integrating lightweight materials. Key players, such as Magna International Inc., BENTELER International AG, and Gestamp Automoción S.A., focus on long-term OEM contracts, platform-level supply agreements, and co-development models to align subframe designs with vehicle architecture and regulatory requirements.

Download Free sample to learn more about this report.

Automotive Subframe Market Key Takeaways

- 2025 Market Size: USD 28.45 billion

- 2026 Market Size: USD 29.24 billion

- 2034 Forecast Market Size: USD 43.61 billion

- CAGR: 5.1% from 2026-2034

- Asia Pacific dominated the automotive subframe market with a 48.50% share in 2025.

- The front subframe segment is expected to grow at a CAGR of 5.4% during the forecast period.

- The SUV segment is anticipated to grow at a CAGR of 5.8% during the forecast period.

Asia Pacific

Asia Pacific led the market due to high vehicle production, expanding EV manufacturing, and strong demand for passenger cars and SUVs.

North America

North America is supported by robust production of SUVs, pickup trucks, and electric vehicles, along with increasing adoption of lightweight materials.

Europe

Europe is driven by stringent emission regulations, advanced safety standards, and growing use of lightweight vehicle architectures.

U.S.

Strong demand for SUVs, pickup trucks, and EVs continues to support automotive subframe adoption.

Japan

High vehicle production volumes and the presence of major automakers contribute to sustained market growth.

Read More

AUTOMOTIVE SUBFRAME MARKET TRENDS

Increasing Shift Toward Lightweight and Multi-Material Subframe Architectures Emerges as a Market Trend

The increasing shift toward lightweight and multi-material subframe architectures has emerged as a prominent trend in the automotive subframe market. Automotive OEMs are increasingly prioritizing weight reduction and fuel efficiency targets amid stringent global emission and fuel economy regulations, prompting broader adoption of aluminum, high-strength steel, and hybrid material subframes. These advanced material strategies enhance vehicle performance and safety, while also supporting modular platform designs that can be shared across multiple vehicle models and powertrain types, including electric vehicles. As environmental and regulatory pressures intensify, subframe suppliers are accelerating material innovation and integration to meet the evolving requirements of vehicle architecture and achieve competitive differentiation. Such development drives the market growth.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growth in Electric Vehicle Production and Platform Diversification is Accelerating Market Growth

The rapid growth in Electric Vehicle (EV) production worldwide is a key factor driving the market. Unlike conventional internal combustion engine vehicles, electric vehicles require redesigned vehicle architectures to accommodate battery packs, electric drivetrains, and enhanced underbody protection. This shift has increased the demand for structurally optimized and lightweight subframes that can support higher loads while ensuring safety, rigidity, and noise isolation. Additionally, OEMs are increasingly adopting flexible and modular electric vehicle platforms that can be shared across multiple vehicle models and body styles, further strengthening the role of subframes as critical structural modules. As automakers expand their EV portfolios, the need for advanced subframe designs tailored to different platform configurations continues to rise, driving automotive subframe market growth.

- For instance, in August 2025, Ford Motor Company announced a new universal electric vehicle platform at an event in Louisville, Kentucky, intended to underpin future EV models, including an affordable mid-size electric pickup. This announcement highlights the company’s broader shift toward dedicated EV architectures, which drive demand for subframes.

MARKET RESTRAINTS

Volatility in Steel and Aluminum Raw Material Prices May Limit the Market Growth

Volatility in steel and aluminum raw material prices is a key restraining factor for the market, as these materials account for a significant share of overall production costs. Subframes are predominantly manufactured using high-strength steel and aluminum to meet structural, safety, and light-weighting requirements, making suppliers highly exposed to fluctuations in commodity pricing. Sudden increases in raw material costs can compress supplier margins, particularly under long-term OEM contracts with fixed pricing structures. Additionally, price instability complicates cost forecasting, procurement planning, and contract negotiations for both OEMs and Tier 1 suppliers. This volatility also limits manufacturers' ability to consistently invest in the adoption of lightweight materials and process innovation, thereby restraining market expansion and cost competitiveness across vehicle platforms.

MARKET OPPORTUNITIES

Technological Advancements in Forming, Welding, and Casting Processes to Offer Market Growth Opportunities

Technological advancements in forming, welding, and casting processes are creating significant growth opportunities in the market by enabling more efficient, precise, and lightweight production of structural components. Innovations such as integrated die casting enable manufacturers to produce large, complex subframes in fewer pieces, thereby reducing assembly steps, enhancing structural integrity, and lowering production costs while meeting stringent performance requirements. At the same time, the adoption of advanced welding techniques, such as laser welding and friction stir welding, enhances joint strength and supports the use of high-strength and lightweight materials in subframe assemblies, thereby improving vehicle performance and safety. This development drives the market growth during the forecast period.

MARKET CHALLENGES

Compliance with Evolving Crash, Safety, and NVH Regulations is a Key Market Challenge

Compliance with evolving crash, safety, and Noise, Vibration, And Harshness (NVH) regulations represents a significant challenge for the market. Subframes play a critical structural role in managing impact loads, energy absorption, and vibration isolation, making them subject to increasingly stringent regulatory standards across major automotive markets. As global safety norms continue to tighten, suppliers are required to invest heavily in advanced simulation, testing, and material optimization to ensure compliance without compromising weight reduction targets. Additionally, differing regional regulatory frameworks increase design complexity and development timelines for OEMs and Tier 1 suppliers. These regulatory pressures raise development costs and prolong validation cycles, thereby posing challenges to cost efficiency and time-to-market for new vehicle platforms.

Segmentation Analysis

By Subframe Position

Front Subframe Segment Dominates Due to Structural Importance, Crash Safety, NVH Control, and Lightweight EV Compatibility

Based on subframe position, the market is segmented into front subframe and rear subframe.

The front subframe segment is expected to account for the largest share of the market due to its fundamental structural role in supporting key vehicle systems, including the engine, suspension, steering assembly, and electric drivetrain modules. Front subframes are critical for load distribution, crash energy management, and NVH performance, making them essential across passenger cars, SUVs, and EVs alike. In addition, the ongoing industry trend toward lightweight and multi-material architectures, particularly those utilizing aluminum and hybrid composites, has reinforced the prominence of the front subframe segment as OEMs seek greater fuel efficiency, reduced emissions, and improved driving dynamics. These lightweight front subframes also enhance battery range and safety performance in electric vehicles, further strengthening their market dominance.

The front subframe segment is expected to grow at a CAGR of 5.4% over the forecast period.

By Vehicle Type

Rising Preference for SUVs to Propel SUV Segmental Growth

Based on vehicle type, the market is segmented into hatchback/sedan, SUV, light-duty vehicle, and heavy-duty vehicle.

The SUV segment is expected to dominate the market due to a strong global shift in consumer preference toward sport utility vehicles across both developed and emerging economies. SUVs require robust and reinforced subframe structures to support higher vehicle weight, elevated ground clearance, larger suspension systems, and enhanced crash safety requirements compared to hatchbacks and sedans. Additionally, the growing penetration of electric SUVs has further strengthened demand, as these vehicles require structurally optimized front and rear subframes to accommodate battery packs while maintaining ride comfort and NVH performance. OEMs are also increasingly standardizing SUV platforms across multiple models, which increases the volume demand for subframe assemblies and reinforces the segment’s dominant market position.

- For instance, in July 2025, Tesla announced that the company is set to make its much-anticipated India debut on July 15, 2025, and is expected to launch the Model Y electric SUV. The Model Y will be Tesla’s first offering in India and will be sold as a Completely Built Unit (CBU), likely imported from the company’s Gigafactory in Shanghai. In preparation for its launch, Tesla has brought in vehicles, Superchargers, and accessories worth nearly USD 1 million into India, primarily sourced from China and the U.S. The imports include six units of the popular Model Y SUV.

To know how our report can help streamline your business, Speak to Analyst

The SUV segment is anticipated to grow at a CAGR of 5.8% over the forecast period.

By Material Type

Strong Cost–Performance Balance of Steel Subframes to Propel Segmental Growth

Based on material type, the market is segmented into steel subframes, aluminum subframes, and others.

The steel subframes segment is expected to hold the dominant automotive subframe market share, primarily due to its favorable cost–performance balance, high strength, and proven durability across a wide range of vehicle types. Steel subframes, particularly those manufactured using high-strength and advanced high-strength steel (HSS/AHSS), offer superior load-bearing capacity, crash energy absorption, and fatigue resistance, making them highly suitable for mass-market passenger vehicles, SUVs, and commercial vehicles. Additionally, steel subframes benefit from established manufacturing processes, lower raw material costs compared to aluminum, and strong recyclability, which collectively support large-scale OEM adoption.

The aluminum subframes segment is anticipated to grow at a CAGR of 5.7% over the forecast period.

By Propulsion

ICE Segment Dominance Supported by High Vehicle Production and Platform Upgrades

Based on propulsion, the market is segmented into ICE, EV, and HEV.

The ICE segment is expected to dominate the market due to the continued high production volume of internal combustion engine vehicles across key automotive markets. Despite the accelerating transition toward electrification, ICE vehicles, particularly in emerging economies and cost-sensitive segments, remain the primary contributors to global vehicle output. ICE-based architectures require robust front subframes to support engines, transmissions, exhaust systems, and suspension assemblies, driving consistent demand for steel-intensive and cost-optimized subframe designs. Moreover, OEMs continue to invest in upgrading ICE platforms to meet tightening emission and fuel efficiency regulations, which sustains the need for redesigned and lightweight subframe solutions within existing ICE vehicle portfolios.

The HEV segment is anticipated to grow at a CAGR of 6.7% over the forecast period.

By Drive Type

Widespread Adoption of Front-Wheel Drive Platforms to Propel Segmental Growth

Based on drive type, the market is segmented into Front-Wheel Drive (FWD), Rear-Wheel Drive (RWD), and All-Wheel Drive (AWD).

The Front-Wheel Drive (FWD) segment is expected to dominate the market due to its extensive adoption across mass-market passenger cars, compact SUVs, and crossover vehicles. FWD architectures rely heavily on integrated front subframe assemblies to support the engine, transaxle, steering system, and front suspension within a compact layout. This configuration offers advantages such as lower manufacturing cost, improved fuel efficiency, reduced vehicle weight, and enhanced interior space utilization, making it highly attractive for high-volume vehicle platforms. Additionally, most entry-level and mid-segment electric vehicles continue to adopt FWD layouts, further reinforcing demand for front subframes optimized for FWD architectures. The dominance of FWD platforms in emerging markets and urban mobility segments continues to strengthen this segment’s leading position.

The All-Wheel Drive (AWD) segment is anticipated to grow at a CAGR of 5.5% over the forecast period.

Automotive Subframe Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Subframe Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market in terms of production volume, driven by high vehicle manufacturing output in countries such as China, Japan, India, and South Korea. The region benefits from strong demand for passenger cars, compact SUVs, and cost-effective vehicles, which supports large-scale adoption of steel subframes. Rapid urbanization, rising disposable incomes, and expanding EV production, particularly in China, are further accelerating market growth. Additionally, the presence of a large supplier base, cost-efficient manufacturing capabilities, and increasing localization of global OEM platforms make the Asia Pacific a critical growth engine for the market.

North America

North America represents a mature and technology-driven market for automotive subframes, supported by strong vehicle production volumes, particularly in SUVs, pickup trucks, and electric vehicles, in major countries such as the U.S. OEMs in the region emphasize structural safety, crash performance, and NVH compliance, which drives demand for robust front and rear subframe systems. The region is also witnessing a growing adoption of lightweight materials and advanced manufacturing processes to meet fuel economy and emission standards. This development drives the regional growth.

Europe

Europe is a key market for automotive subframes, driven by stringent emission regulations, advanced safety standards, and strong adoption of lightweight vehicle architectures. OEMs in the region increasingly focus on aluminum and multi-material subframes to reduce vehicle weight and improve fuel efficiency. The high penetration of premium vehicles and electric cars further supports demand for advanced subframe designs with superior structural and NVH performance. Moreover, Europe’s strong emphasis on sustainability, recyclability, and modular vehicle platforms encourages continuous innovation in subframe materials and manufacturing processes, reinforcing the region’s strategic importance in the global market.

Rest of the World

The rest of the world region, comprising Latin America, the Middle East & Africa, represents an emerging market for automotive subframes. Growth in this region is primarily supported by the gradual expansion of vehicle production, increasing SUV adoption, and rising investments by global OEMs to establish localized manufacturing facilities.

COMPETITIVE LANDSCAPE

Leading Rental Providers, Equipment Manufacturers, and Fleet Technology Integrators Strengthening Competitiveness in the Market

The global automotive subframe market exhibits a semi-consolidated competitive structure, led by established Tier 1 automotive suppliers with strong engineering, manufacturing, and OEM integration capabilities. Key players such as Magna International Inc., Gestamp Automoción, Benteler International, ZF Friedrichshafen AG, and Hyundai Mobis, hold significant market positions due to their long-standing relationships with global OEMs and their ability to deliver platform-specific front and rear subframe assemblies at scale. These companies focus on co-development models, modular subframe architectures, and advanced material integration to align with evolving vehicle platforms, including ICE and electric vehicles. Strategic investments in lightweight materials, automation, and regional manufacturing footprints remain central to maintaining competitiveness.

Other notable players operating in the market include CIE Automotive, Aisin Corporation, Martinrea International, Tower International (part of the Autokiniton Group), and JBM Auto. These companies are expected to prioritize capacity expansion, localized production, and process innovation to strengthen their market presence and support next-generation vehicle architectures during the forecast period.

LIST OF KEY AUTOMOTIVE SUBFRAME COMPANIES PROFILED

- Magna International Inc. (Canada)

- BENTELER International AG (Austria)

- Gestamp Automoción S.A. (Spain)

- Hyundai MOBIS (South Korea)

- Martinrea International Inc. (Canada)

- Aludyne (U.S.)

- ZF Friedrichshafen AG (Germany)

- CIE Automotive S.A. (Spain)

- YOROZU Corporation (Japan)

- JBM Group (India)

- Linamar Corporation (Canada)

- Nemak, S.A.B. de C.V.(Mexico)

- KSM Castings Group GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS

- In December 2025, Samsung announced a planned acquisition of ZF Friedrichshafen’s ADAS unit a move that could reshape investment priorities and supplier capabilities within chassis and structural technology ecosystems.

- In May 2025, Mitsubishi Logisnext Co., Ltd. opened a 73,500 sq ft electrification fabrication facility at its Houston campus to ramp up production of electric forklifts and counterbalance trucks, aligning with growing demand for electrified fleets.

- In April 2025, Cosma Magna launches large die-cast front subframe production. Cosma’s Michigan facility began producing a large front subframe using a 4,400-ton die-casting press, enabling significant weight reduction and cost efficiency in high-volume chassis production.

- In February 2025, Sarginsons Industries unveiled designs for an automotive subframe that was originally optimized for weight in 2022 and has now been reduced from 28kg to 15kg. The designs were formulated using new AI-driven software currently under development, and represent the initial results of the Performance Integrated Vehicle Optimisation Technology (PIVOT) project, which Sarginsons is leading in collaboration with its partners. The project was made possible by a £6m (US$7.5m) matched grant from the Advanced Propulsion Centre and Innovate U.K.

- In January 2025, Gestamp sets new benchmarks for automotive components at Bharat Mobility Global Expo. Gestamp is leading the development of solutions for a new mobility era, where multiple powertrains coexist, including combustion engines, hybrids, plug-in hybrids, and pure electric vehicles.

- In January 2025, Laser Tools Launched Subframe Alignment Pins for the VW T7. Laser Tools introduced new subframe alignment pins (part no. 8911) designed to precisely realign the front subframe on Volkswagen T7 Transporter vehicles, thereby improving service accuracy.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.1% from 2025-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Subframe Position, By Vehicle Type, By Material Type, By Propulsion, By Drive Type, and By Region |

|

By Subframe Position |

· Front Subframe · Rear Subframe |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · Light Duty Vehicle · Heavy Duty Vehicle |

|

By Material Type |

· Steel Subframes · Aluminum Subframes · Others |

|

By Propulsion |

· ICE · EV · HEV |

|

By Drive Type |

· Front-Wheel Drive · Rear-Wheel Drive · All-Wheel Drive |

|

By Geography |

· North America (By Subframe Position, By Vehicle Type, By Material Type, By Propulsion, By Drive Type, and by Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Subframe Position, By Vehicle Type, By Material Type, By Propulsion, By Drive Type, and by Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Subframe Position, By Vehicle Type, By Material Type, By Propulsion, By Drive Type, and by Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Subframe Position, By Vehicle Type, By Material Type, By Propulsion, By Drive Type, and by Country ) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 28.45 billion in 2025 and is projected to reach USD 43.61 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 13.80 billion.

The market is expected to exhibit a CAGR of 5.1% during the forecast period of 2026-2034

The SUV segment led the market by vehicle type.

Growth in electric vehicle production and platform diversification are the key factors driving the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us