Automotive Motors Market Size, Share & Industry Analysis, By Application (Traction Motors, Electric Power Steering Motors, Starter Motors, Thermal Management Motors, Body & Comfort Motors and Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles and Heavy Commercial Vehicles), By Propulsion (ICE and Electric), By Voltage (Low Voltage and High Voltage), By Sales Channel (OEM and Aftermarket) and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

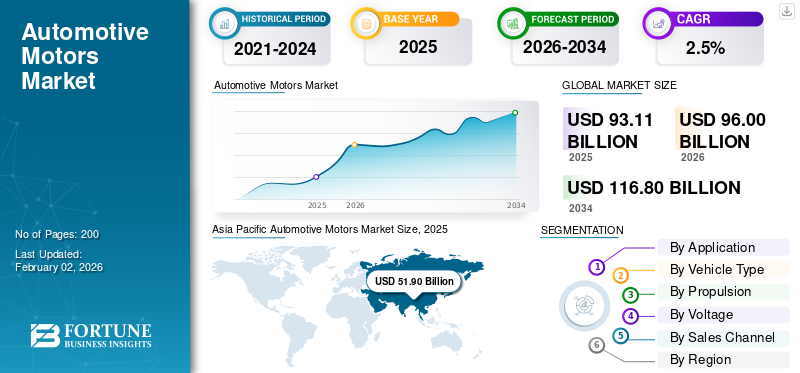

The global automotive motors market size was valued at USD 93.11 billion in 2025. The market is projected to grow from USD 96.00 billion in 2026 to USD 116.80 billion by 2034, exhibiting a CAGR of 2.5% during the forecast period. Asia Pacific dominated the global automotive motors market with a market share of 55.74% in 2025.

The global automotive motors market encompasses a wide range of electric motors used in modern vehicles to support comfort, safety, and performance-related functions. These motors operate essential systems such as power windows, seat adjustment, HVAC units, wipers, braking assistance, and electronic stability control. As vehicles become more feature-rich and technologically advanced, the market for automotive motors has grown from being a supporting component industry to a core enabler of vehicle functionality.

Growth in the market is closely linked to rising vehicle production and vehicles, particularly in developing countries, where personal mobility demand continues to rise. Modern vehicles now integrate a higher number of motors per unit, driven by increasing demand for comfort features and safety technologies such as advanced driver assistance systems ADAS. This trend directly contributes to the expansion of the global automotive motor market size.

Passenger vehicles, including passenger cars and light commercial vehicles, remain the primary contributors to motor demand due to their high production volumes and growing focus on interior comfort and fuel efficiency. At the same time, the rising demand for electric vehicles is reshaping motor design priorities, encouraging the use of compact, energy-efficient solutions such as stepper motors and brushless motors. Over the forecast period, continued innovation and regulatory pressure for efficient vehicles are expected to sustain steady growth across global markets.

Key players such as Bosch, Continental, and Nidec are increasingly focusing on technological innovation to improve efficiency, durability, and compactness. Manufacturers are investing in brushless DC motors, integrated motor-controller designs, and lightweight materials to meet evolving vehicle architecture requirements. Strategic partnerships with OEMs and continuous R&D in energy-efficient motor solutions are helping suppliers align with electrification and advanced feature integration trends across vehicle segments.

Download Free sample to learn more about this report.

AUTOMOTIVE MOTORS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 93.11 Billion

- 2026 Market Size: USD 96.00 Billion

- 2034 Forecast Market Size: USD 116.80 Billion

- CAGR: 2.5% from 2026–2034

- Asia Pacific dominated the automotive motors market with a 55.74% share in 2025.

- The traction motors segment is projected to grow at a CAGR of 4.5% during the forecast period.

- The passenger cars segment is expected to expand at a CAGR of 2.8% through 2034.

North America

North America records steady growth driven by rising adoption of ADAS, comfort features, and premium vehicle technologies.

Europe

Europe benefits from strict emission regulations and increasing use of energy-efficient automotive motor systems.

Asia Pacific

Asia Pacific leads the market due to high vehicle production and strong demand for passenger and electric vehicles.

U.S.

Strong pickup and SUV sales support higher motor demand across safety, comfort, and vehicle automation applications.

Japan

Advanced automotive manufacturing capabilities and growing focus on electrification support stable market growth.

Read More

AUTOMOTIVE MOTORS MARKET TRENDS

Adoption of Smart and Energy-Efficient Motor Technologies Gains Momentum

Automakers are increasingly adopting intelligent motor solutions, including stepper motors, to improve precision and reduce energy consumption. This trend supports regulatory goals for fuel efficiency while enhancing system responsiveness. As vehicles become software-defined, smart motors play a critical role in optimizing performance across vehicle type platforms.

- For instance, in 2023, Nidec introduced energy-efficient automotive motors designed for intelligent vehicle applications.

MARKET DYNAMICS

MARKET DRIVERS

Rising Integration of Comfort, Safety, and Automation Features Accelerates Automotive Motor Demand

The growing adoption of comfort features, electronic stability control, and advanced driver assistance systems ADAS is significantly increasing the demand for automotive motors. Each new function adds multiple motorized components, raising motor content per vehicle. As OEMs compete on safety and user experience, the global automotive motor market size continues to expand across all major vehicle type segments.

- For instance, in 2023, Euro NCAP emphasized wider ADAS adoption, indirectly increasing motor demand for braking, steering, and sensing systems.

MARKET RESTRAINTS

Volatility in Raw Material Prices Constricts Profit Margins for Motor Manufacturers

Automotive motors rely heavily on copper, rare earth magnets, and electronic components. Price volatility and supply constraints negatively affect cost structures, limiting profitability and pricing flexibility. These challenges are amplified across global markets, particularly for suppliers operating in cost-sensitive developing countries, slowing capacity expansion despite strong vehicle production growth.

- For example, in 2024, global copper price fluctuations raised cost pressures across automotive component suppliers.

MARKET OPPORTUNITIES

Electrification of Auxiliary Systems Creates New Growth Avenues for Motor Suppliers

The rising demand for electric vehicles is accelerating the electrification of auxiliary functions previously driven mechanically. This shift increases opportunities for low-voltage motors supporting HVAC, steering, and braking systems. As OEMs redesign platforms for efficient vehicles, suppliers offering compact and energy-efficient motors gain strong growth potential during the forecast period.

- For example, in 2024, Hyundai highlighted increased electrification of auxiliary vehicle systems across its EV lineup.

MARKET CHALLENGES

Complex Integration Requirements Increase Development and Validation Costs

Integrating motors with vehicle electronics, software, and safety systems, such as advanced driver assistance systems ADAS increases development complexity. OEM validation cycles are longer, and customization requirements differ across markets. These challenges can delay product launches and strain supplier engineering resources.

Download Free sample to learn more about this report.

Segmentation Analysis

By Application

Body & Comfort Motors Dominate Due to Increasing Demand for Premium Features Across All Vehicles

On the basis of application, the market is divided into traction motors, electric power steering motors, starter motors, thermal management motors, body & comfort motors, and others.

Body and comfort systems require multiple motors per vehicle, supporting windows, seats, mirrors, and HVAC. Rising consumer expectations and increasing demand for premium features across passenger cars and light commercial vehicles sustain high volumes, making this the largest application segment.

- For instance, in February 2025, Lear Corporation announced the integration of its ComfortMax seating systems with General Motors vehicles, improving passenger comfort and convenience with advanced thermal/motorized seating technologies.

The traction motors segment is expected to grow at a CAGR of 4.5% over the forecast period.

By Vehicle Type

To know how our report can help streamline your business, Speak to Analyst

On the basis of vehicle type, the market is segmented into passenger cars, light commercial vehicles, and heavy commercial vehicles.

Passenger cars dominate automotive motors market share due to their high vehicle production, growing feature density, and strong vehicle sales in developing countries. Comfort, safety, and efficiency upgrades continue to increase motor count per unit.

- For instance, in November 2025, SAIC’s IM Motors launched the new IM L6 sedan globally, expanding its passenger car lineup with advanced comfort and adaptive control features.

The passenger cars segment is expected to grow at a CAGR of 2.8% over the forecast period.

By Propulsion

ICE Vehicles Segments Lead Due to Vast Installed Base and Continued Production in Cost-Sensitive Markets

On the basis of propulsion, the market is segmented into ICE and electric.

ICE vehicles continue to dominate due to their vast installed base and continued production in cost-sensitive markets. These vehicles require numerous low-voltage motors supporting fuel efficiency and emissions compliance systems.

- For example, in May 2024, Horse Powertrain joint venture launched hybrid and efficient ICE powertrain platforms, reinforcing continued ICE vehicle relevance while integrating motor systems for improved fuel efficiency.

The electric segment is growing at a CAGR of 6.8% over the forecast period.

By Voltage

Low-Voltage Motors Dominate Due to their Cost Efficiency and Compatibility in Architectures

On the basis of voltage, the market is segmented into low voltage and high voltage.

Low-voltage motors are widely used across body, comfort, and safety systems, making them essential regardless of propulsion type. Their cost efficiency and compatibility with existing architectures drive sustained dominance.

- For instance, in July 2025, YASA Limited announced a prototype 550 kW electric motor with high power density suitable for low-voltage automotive applications, enhancing performance and efficiency in passenger vehicles.

The high voltage segment is expected to grow at a CAGR of 5.3% over the forecast period.

By Sales Channel

OEM Channel Leads the Market Owing to Long-term Supply Contracts

On the basis of sales channel, the market is segmented into OEM and Aftermarket.

OEMs dominate motor sourcing as integration begins at vehicle design stages. Long-term supply contracts and platform standardization strengthen OEM-led demand across global markets.

- For instance, in February 2025, BorgWarner secured four new electric motor supply contracts with major Chinese OEMs for hybrid and electric vehicle platforms, strengthening OEM integration and production.

The OEM segment is expected to grow at a CAGR of 2.7% over the forecast period.

Automotive Motors Market Regional Outlook

By region, the global automotive motors market is categorized into North America, Europe, Asia Pacific, and the Rest of the world.

Asia Pacific

Asia Pacific Automotive Motors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global automotive motors market due to high vehicle production, strong vehicle sales, and expanding manufacturing ecosystems in China, India, and Southeast Asia. Rising income levels, urban mobility demand, and localization strategies by global OEMs drive motor consumption across ICE and EV platforms.

- For instance, in August 2025, Vietnamese EV maker VinFast opened a $500 million manufacturing plant in Tamil Nadu, India, aiming to serve Asia Pacific markets with electric vehicles and related components.

North America

North America shows steady growth supported by demand for advanced safety systems and premium vehicle features. The U.S. market benefits from strong pickup and SUV sales, driving higher motor content per vehicle, especially for comfort and ADAS-related applications.

Europe

Europe’s automotive motors market growth is shaped by stringent emission norms and safety regulations. Increasing adoption of electrified auxiliary systems and energy-efficient motors supports gradual expansion across passenger vehicle platforms.

Rest of the World

The rest of the world regions benefit from rising motorization rates and localized vehicle assembly. Latin America, and the Middle East & Africa show growing demand for cost-effective motor solutions aligned with entry-level vehicle production.

COMPETITIVE LANDSCAPE

Key Industry Players

Electrification Focus and Global Manufacturing Shape Market Competition

The competitive landscape of the global automotive motors market includes a mix of global Tier-1 suppliers and specialized motor manufacturers that serve OEMs across multiple vehicle type segments. Competition is largely driven by technological capability, cost efficiency, and the ability to support high-volume vehicle production in major automotive hubs across North America, Europe, and the Asia Pacific.

Key market players focus on supplying reliable and compact motors that support comfort features, safety systems, and advanced driver assistance systems ADAS. As automakers increase the number of motor-driven functions per vehicle, suppliers are investing in quieter, more efficient designs that improve performance while supporting fuel efficiency targets. Many companies are also expanding their portfolios to include intelligent motor solutions for electronic stability control and automated vehicle functions.

Strategic partnerships with OEMs play a key role in gaining a competitive advantage. Suppliers often align closely with vehicle development cycles, enabling early-stage integration and long-term supply agreements. In parallel, manufacturers are expanding production facilities closer to high-growth global markets to reduce costs and improve supply reliability. While ICE platforms still dominate volumes, companies are actively preparing for rising demand for electric vehicles, ensuring their motor offerings remain relevant throughout the forecast period.

- For instance, in September 2025, logistics provider Manfreight deployed 100 new Schmitz Cargobull S.KO COOL Automotive Motors, underscoring strong OEM demand and customer confidence in quality and telematics performance.

LIST OF KEY AUTOMOTIVE MOTORS COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Denso Corporation (Japan)

- Nidec Corporation (Japan)

- Continental AG (Germany)

- Valeo SA (France)

- Johnson Electric (Hong Kong)

- Mitsubishi Electric (Japan)

- Panasonic Automotive (Japan)

- Hitachi Astemo (Japan)

- ZF Friedrichshafen AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Denso expanded its motor development program for auxiliary automotive systems, focusing on energy-efficient designs supporting HVAC, steering, and safety-related vehicle functions.

- January 2025: ZF began series production of electric motors at its Hangzhou facility to supply Chinese OEMs, strengthening localized motor production amid rising vehicle production in the Asia Pacific.

- September 2024: Continental introduced next-generation low-voltage automotive motors optimized for electronic braking and electronic stability control, supporting both ICE and electric vehicle platforms.

- June 2024: Nidec launched a new series of compact automotive motors designed for body, comfort, and braking applications, targeting improved efficiency and reduced noise in passenger vehicles.

- March 2024: Bosch announced the expansion of its automotive electric motor manufacturing line in China to support growing demand from comfort systems and advanced driver assistance systems ADAS applications.

REPORT COVERAGE

The global automotive motors market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 2.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Application, Vehicle Type, Propulsion, Voltage, Sales Channel, and Region |

|

By Application |

· Traction Motors · Electric Power Steering Motors · Starter Motors · Thermal Management Motors · Body & Comfort Motors · Others |

|

By Vehicle Type |

· Passenger Cars · Light Commercial Vehicles (LCVs) · Heavy Commercial Vehicles (HCVs) |

|

By Propulsion |

· ICE · Electric |

|

By Voltage |

· Low voltage · High Voltage |

|

By Sales Channel |

· OEM · Aftermarket |

|

By Region |

· North America (By Application, Vehicle Type, Propulsion, Voltage, Sales Channel, and Country) o U.S. o Canada o Mexico · Europe (By Application, Vehicle Type, Propulsion, Voltage, Sales Channel, and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Application, Vehicle Type, Propulsion, Voltage, Sales Channel, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Application, Vehicle Type, Propulsion, Voltage, Sales Channel, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 93.11 billion in 2025 and is projected to reach USD 116.80 billion by 2034.

In 2025, the market value stood at USD 51.90 billion.

The market is expected to exhibit a CAGR of 2.5% during the forecast period of 2026-2034.

The Passenger Cars segment led the market by vehicle type.

Rising integration of comfort, safety, and automation features is driving the global automotive motors market.

Bosch, Denso, Nidec, and Continental are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us