Automotive Supervisory Market Size, Share & Industry Analysis, By Product Type (Voltage Monitors, Reset ICs, Watchdog ICs, and Others), By Vehicle Type (Hatchback/Sedan, SUV, Light Duty Vehicle, and Heavy Duty Vehicle), By Voltage (<3.3 V, 3.3 V – 5V, and More than 5V), By Application (Body Electronics, Infotainment & Telematics, Powertrain & Electrified Systems, ADAS & Safety Systems, and Others), By AEC Grade (AEC Grade 0, AEC Grade 1, and AEC Grade 2 & Below), By ASIL Level (QM/ASIL-A, ASIL-B, ASIL-C, and ASIL-D), By Propulsion Type (ICE and EV), and Regional Forecast, 2026-2034

Automotive Supervisory Market Size and Future Outlook

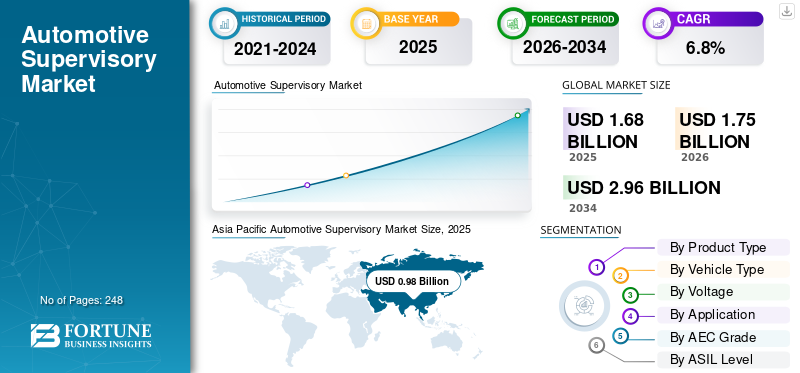

The global automotive supervisory market size was valued at USD 1.68 billion in 2025. The market is projected to grow from USD 1.75 billion in 2026 to USD 2.96 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period. Asia Pacific dominated the automotive supervisory market with a market share of 58.33% in 2025.

The global market refers to the ecosystem of systems, software, and solutions that oversee, coordinate, and manage multiple Electronic Control Units (ECUs) within a vehicle. These supervisory systems enable centralized decision-making, functional safety, and efficient communication across advanced vehicle architectures, particularly in connected, electric, and autonomous vehicles. The market includes middleware, domain controllers, and vehicle-level control platforms supporting enhanced performance, diagnostics, and real-time system integration.

Key drivers of the market include rising adoption of electric and autonomous vehicles, increasing vehicle electronics complexity, and demand for centralized vehicle architectures. Advancements in ADAS, need for real-time data processing, and regulatory focus on safety and cybersecurity further accelerate the adoption of supervisory control systems across modern vehicles.

Major players in the market include Bosch, Analog Devices, Inc, NXP Semiconductors N.V. and Infineon Technologies AG, competing through advanced vehicle computing platforms, centralized architectures, AI-driven software, and real-time data processing capabilities, while focusing on functional safety, scalability, and seamless integration across electric, connected, and autonomous vehicle ecosystems.

Download Free sample to learn more about this report.

AUTOMOTIVE SUPERVISORY MARKET TRENDS

Increasing Focus on Over-the-Air Updates to Enhance Vehicle Lifecycle Management Emerge as a Key Trend

The growing adoption of over-the-air (OTA) update capabilities is emerging as a key trend in the market. OEMs are increasingly leveraging OTA technologies to remotely update vehicle software, fix bugs, and introduce new features without requiring physical service visits. Supervisory systems play a crucial role in managing and coordinating these updates across multiple vehicle domains, ensuring seamless integration and minimal disruption to vehicle operations.

OTA capabilities significantly enhance vehicle lifecycle management by enabling continuous improvements post-sale. Supervisory controllers ensure that updates are deployed securely and efficiently across systems such as ADAS, infotainment, and powertrain. This not only improves performance and safety but also allows automakers to extend the functional lifespan of vehicles. As a result, vehicles remain technologically relevant for longer periods, increasing customer satisfaction and brand loyalty.

Additionally, OTA updates support new revenue streams for automakers through feature-on-demand and subscription-based services. Supervisory systems enable selective activation of functionalities, allowing OEMs to offer personalized upgrades to customers. This shift transforms vehicles into upgradable platforms, aligning with the broader trend of software-defined mobility. It also helps manufacturers reduce recall costs by addressing issues remotely, improving operational efficiency and cost management.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Adoption of Software-Defined Vehicles to Accelerate Supervisory Systems Demand

The automotive industry is undergoing a major transformation with the increasing adoption of Software-Defined Vehicles (SDVs). In these vehicles, software plays a central role in controlling and managing core functionalities, replacing traditional hardware-centric architectures. This shift requires advanced supervisory systems that can coordinate multiple domains efficiently. As OEMs move toward unified vehicle platforms, supervisory controllers become essential for enabling seamless communication and centralized decision-making across various electronic and software components.

Software-defined vehicles rely heavily on continuous updates, feature enhancements, and system optimization through OTA capabilities. Supervisory systems act as the backbone for managing these updates, ensuring synchronization between different vehicle functions such as ADAS, infotainment, and powertrain. This capability not only improves vehicle performance but also extends product lifecycle. As a result, automakers are increasingly investing in supervisory technologies to support dynamic software deployment and real-time system monitoring.

MARKET RESTRAINTS

Limited Standardization Across Platforms to Hinder Seamless Integration

The lack of industry-wide standardization in software platforms and electrical/electronic architectures poses a significant restraint for the market. Different OEMs adopt varying system designs, operating systems, and communication protocols, making it challenging to develop universally compatible supervisory solutions. This fragmentation increases complexity for suppliers and limits the scalability of supervisory technologies across multiple vehicle platforms and brands.

As supervisory systems are designed to integrate and manage multiple domains, inconsistencies in standards create integration bottlenecks. Suppliers often need to customize solutions for each OEM, leading to increased development time and costs. This reduces efficiency and slows down innovation, as resources are diverted toward adapting systems rather than advancing core functionalities. Smaller players, in particular, face difficulties in keeping up with diverse and evolving requirement

MARKET OPPORTUNITIES

Integration of AI and Edge Computing to Unlock Advanced Vehicle Intelligence

The integration of artificial intelligence into automotive supervisory systems is unlocking new levels of vehicle intelligence and functionality. AI enables supervisory controllers to analyze large volumes of real-time data generated by sensors, cameras, and onboard systems. This capability supports advanced features such as predictive maintenance, driver behavior analysis, and adaptive system responses. As vehicles become more intelligent, AI-powered supervisory systems are increasingly critical for delivering enhanced safety, efficiency, and personalized driving experiences.

Edge computing further strengthens this opportunity by enabling data processing directly within the vehicle, reducing reliance on cloud infrastructure. Supervisory systems equipped with edge capabilities can process time-sensitive information with minimal latency, which is essential for applications such as autonomous driving and advanced driver assistance systems. This localized processing ensures faster decision-making and improved system responsiveness, enhancing overall vehicle performance and reliability under dynamic driving conditions.

MARKET CHALLENGES

Cybersecurity Risks in Centralized Systems to Pose a Critical Challenge

As vehicles adopt centralized supervisory architectures, cybersecurity emerges as a significant challenge. Supervisory systems act as the central control hub, making them a potential target for cyberattacks that could compromise multiple vehicle functions simultaneously. Ensuring robust security across software layers, communication networks, and external interfaces is increasingly complex. The growing use of over-the-air updates and connected services further expands the attack surface. Automakers and technology providers must implement advanced encryption, intrusion detection systems, and continuous monitoring mechanisms to safeguard vehicle operations. Additionally, evolving regulatory requirements around vehicle cybersecurity add to compliance pressures, making it essential for companies to invest heavily in secure system design and lifecycle management.

Segmentation Analysis

By Product Type

Critical Role in Power Stability and System Protection to Drive Voltage Monitors Segment Dominance

Based on product type, the market is segmented into voltage monitors, reset ICs, watchdog ICs, and others.

The voltage monitors segment dominates the automotive supervisory market share due to its essential role in ensuring stable power supply and protecting electronic systems from voltage fluctuations. With increasing electrification and rising integration of sensitive electronic components, voltage monitors are widely deployed across ECUs, battery management systems, and infotainment units. Their ability to prevent system failures, ensure functional safety, and support reliable vehicle operation drives consistent demand across both conventional and electric vehicles globally.

The watchdog ICs segment is projected to grow at a CAGR of 7.8% over the forecast period, driven by increasing need for system reliability and fault detection. These components enhance real-time monitoring and automatic recovery, particularly in ADAS and autonomous systems, supporting robust supervisory control architectures.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Rising Consumer Preference and Advanced Electronics Integration to Drive SUV Segment Dominance

In terms of vehicle type, the market is categorized into hatchback/sedan, SUV, light duty vehicle, and heavy duty vehicle.

The SUV segment dominates the market due to strong global demand, higher electronic content, and increasing integration of advanced driver assistance and infotainment systems. SUVs typically incorporate more complex electrical architectures, requiring robust supervisory systems for centralized control and safety management. Growing consumer preference for premium features, electrification trends in SUVs, and their widespread adoption across developed and emerging markets further contribute to sustained demand for supervisory solutions in this segment.

The hatchback/sedan segment holds the second-largest share with a CAGR of 6.1% over the forecast period, supported by its extensive global vehicle parc and high production volumes. Consistent demand for cost effective vehicles and steady integration of electronic systems ensure continued adoption of supervisory technologies across mass-market passenger cars.

By Voltage

Widespread Use in Core Automotive Electronics to Drive 3.3 V – 5V Segment Dominance

In terms of voltage, the market is categorized into <3.3 V, 3.3 V – 5V, and more than 5V.

The 3.3 V – 5V segment dominates the market due to its extensive application across key vehicle electronics, including microcontrollers, sensors, infotainment systems, and control units. This voltage range offers an optimal balance between power efficiency and performance, making it the industry standard for most automotive electronic architectures. Its compatibility with a wide range of components and established design ecosystems ensures consistent demand across both conventional and electric vehicles, reinforcing its leading position.

The <3.3 V segment is projected to grow at the 7.6% CAGR during the study period, driven by rising adoption of low-power electronics and advanced semiconductor technologies. Increasing integration of compact, energy-efficient components in ADAS, IoT-enabled systems, and next-generation vehicle platforms is accelerating demand in this segment.

By Application

Increasing Electrified Powertrain Complexity to Drive Powertrain & Electrified Systems Segment Dominance

Based on application, the market is segmented into body electronics, infotainment & telematics, powertrain & electrified systems, ADAS & safety systems, and others.

The powertrain & electrified systems segment dominates the market due to the rapid shift toward electric and hybrid vehicles, which require advanced control and monitoring capabilities. Supervisory systems play a critical role in managing battery performance, energy distribution, thermal systems, and motor control. The growing complexity of electrified powertrains and the need for real-time coordination across multiple subsystems significantly drive demand. Additionally, stringent emission regulations and the global push for energy-efficient mobility further reinforce the adoption of supervisory solutions in this segment.

The ADAS & safety systems segment is projected to grow at the 8.2% CAGR over the study period, driven by increasing deployment of advanced driver assistance features and autonomous technologies. Rising safety regulations and demand for real-time system monitoring are accelerating the integration of supervisory systems in this segment.

By AEC Grade

High Adoption in Standard Automotive Applications to Drive AEC Grade 1 Segment Dominance

Based on AEC grade, the market is segmented into AEC Grade 0, AEC Grade 1, and AEC Grade 2 & below.

The AEC Grade 1 segment dominates the market due to its widespread use in standard automotive environments requiring reliable performance under moderate temperature ranges. These components are extensively deployed across passenger vehicles for applications such as infotainment, body electronics, and powertrain control. Their cost-effectiveness, proven reliability, and compatibility with existing vehicle architectures make them the preferred choice for high-volume production. Additionally, the growing integration of electronic systems in mass-market vehicles continues to sustain strong demand for AEC Grade 1 components globally.

The AEC Grade 0 segment is projected to grow at the 7.8% CAGR during the forecast period. Such growth is driven by increasing demand for high-performance components in extreme temperature environments. Rising adoption in ADAS, autonomous systems, and electric vehicles is accelerating the need for more robust and durable supervisory solutions.

By ASIL Level

High Volume Deployment in Non-Critical Systems to Drive QM/ASIL-A Segment Dominance

Based on ASIL level, the market is segmented into QM/ASIL-A, ASIL-B, ASIL-C, and ASIL-D.

The QM/ASIL-A segment dominates the market due to its extensive use in non-critical and moderately safety-relevant vehicle functions such as infotainment, body electronics, and basic control systems. These applications require reliable performance but do not demand the highest level of functional safety, making QM/ASIL-A components more cost-effective and widely adopted. High production volumes of passenger vehicles and increasing electronic integration in comfort and convenience features further sustain strong demand for this segment across global automotive platforms.

The ASIL-D segment is projected to register the fastest growth, with a CAGR of 7.9% over the forecast period. It is driven by rising adoption of advanced safety-critical systems such as ADAS and autonomous driving technologies. Increasing regulatory focus on functional safety and system reliability is accelerating demand for high-integrity supervisory solutions in this segment.

By Propulsion Type

Large Installed Base and Continued Production to Drive ICE Segment Dominance

Based on propulsion type, the market is bifurcated into ICE and EV.

The ICE segment dominates the market due to its vast global vehicle parc and continued production across emerging and developed markets. Internal combustion engine vehicles rely on multiple electronic control units requiring supervisory systems for monitoring, coordination, and fault management. Cost advantages, established infrastructure, and slower electrification in certain regions sustain strong demand. Additionally, ongoing integration of electronics in ICE vehicles, including emission control and diagnostics, continues to reinforce the need for supervisory solutions.

The EV segment is projected to grow at the 16.1% CAGR during the forecast period, driven by rapid electrification, government incentives, and increasing adoption of battery electric vehicles. The complexity of battery management, power electronics, and real-time system coordination significantly boosts demand for advanced supervisory systems.

Automotive Supervisory Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Supervisory Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to its high vehicle production volumes, strong presence of leading OEMs, and rapid adoption of electric vehicles. Countries such as China, Japan, and South Korea are at the forefront of automotive innovation, integrating advanced electronics and centralized architectures. Government support for electrification, growing demand for connected vehicles, and increasing semiconductor manufacturing capabilities further accelerate automotive supervisory market growth. Additionally, cost-effective manufacturing and expanding middle-class vehicle ownership sustain long-term demand for supervisory systems.

China Automotive Supervisory Market

The China market in 2026 is estimated at around USD 0.61 billion, accounting for a dominant share of global market revenues. Growth is fueled by high vehicle production, rapid electrification, government support, and increasing integration of advanced electronics in domestic and export vehicles.

Japan Automotive Supervisory Market

The Japan market in 2026 is estimated at around USD 0.15 billion, accounting for a considerable share of global market revenues. Growth is driven by a strong automotive manufacturing base, focus on hybrid and electric technologies, and continuous innovation in vehicle electronics and safety systems.

North America

North America holds the second-largest market share, growing at a CAGR of 5.4%, driven by early adoption of advanced automotive technologies and strong focus on software-defined vehicles. The region has a high concentration of technology providers and OEMs investing in autonomous driving, ADAS, and connected vehicle platforms. Increasing demand for high-performance computing and centralized control systems boosts supervisory system adoption. Additionally, regulatory emphasis on vehicle safety and cybersecurity further supports steady market expansion across the U.S. and Canada.

U.S. Automotive Supervisory Market

The U.S. market in 2026 is estimated at around USD 0.17 billion, accounting for a notable share of global market revenues. Market growth is driven by early adoption of software-defined vehicles, strong R&D in autonomous systems, and increasing deployment of advanced supervisory architectures.

Europe

Europe represents the third-largest market, supported by stringent vehicle safety regulations and strong demand for premium vehicles with advanced electronic systems. Leading automakers in Germany, France, and the U.K. are heavily investing in electrification and digital vehicle architectures, increasing the need for supervisory solutions. The region’s focus on sustainability and carbon neutrality accelerates EV adoption, further driving system complexity. Additionally, well-established automotive R&D infrastructure and emphasis on functional safety standards contribute to consistent market growth.

U.K. Automotive Supervisory Market

The U.K. market in 2026 is estimated at around USD 0.01 billion, accounting for a modest share of global market revenues. Growth is driven by increasing adoption of connected vehicle technologies, strong regulatory focus on safety systems, and rising integration of advanced electronics across premium and electric vehicle segments.

Germany Automotive Supervisory Market

The Germany market in 2026 is estimated at around USD 0.09 billion, accounting for a significant share of global market revenues. Growth is supported by strong presence of leading OEMs, advancements in vehicle electronics, and increasing investments in electrification and autonomous driving technologies across the country.

Rest of the World

The rest of the world region is experiencing steady growth in the market, driven by expanding automotive industries in Latin America, the Middle East, and Africa. Increasing urbanization, improving economic conditions, and rising vehicle ownership contribute to demand for vehicles with enhanced electronic capabilities. Although electrification adoption is gradual compared to other regions, growing investments in infrastructure and regulatory developments support future growth. Additionally, the expansion of global OEMs into these markets is fostering gradual adoption of supervisory systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Established Players and AI Advancements Drive Competitive Innovation in Automotive Supervisory Systems

The market is characterized by intense competition among established semiconductor companies, automotive suppliers, and emerging technology firms focusing on software-defined vehicle architectures. Key players such as Bosch, Renesas Electronic Corporation, Denso, Analog Devices, Inc, NXP Semiconductors, and Infineon Technologies are investing heavily in advanced supervisory ICs, centralized computing platforms, and integrated software solutions. These companies leverage strong R&D capabilities, strategic partnerships with OEMs, and global supply chains to strengthen their market position and expand their technological innovations portfolios.

In addition, competition is increasing with the entry of AI and high-performance computing players such as NVIDIA and Qualcomm, who are redefining supervisory control through scalable platforms and real-time data processing capabilities. Market participants are focusing on product innovation, functional safety compliance, and cybersecurity enhancements to differentiate their offerings. Mergers, acquisitions, and collaborations with software providers are also shaping the competitive dynamics, enabling companies to deliver end-to-end solutions tailored for electric, connected, and autonomous vehicle ecosystems.

LIST OF KEY AUTOMOTIVE SUPERVISORY COMPANIES PROFILED

- Infineon Technologies AG (Germany)

- NXP Semiconductors N.V. (Netherlands)

- STMicroelectronics N.V. (Switzerland)

- Texas Instruments Inc. (U.S.)

- Renesas Electronic Corporation (Japan)

- ON Semiconductor (onsemi) (U.S.)

- Analog Devices, Inc. (U.S.)

- Diodes Incorporated (U.S.)

- SG Micro Corp. (China)

- Robert Bosch GmbH (Germany)

- Microchip Technology Inc. (U.S.)

- ROHM Semiconductor (Japan)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Diodes Incorporated introduced the AL8859Q automotive multi-phase SPI boost controller for advanced headlight control units, emphasizing power density, EMI performance, and functional safety. This launch is relevant to supervisory IC demand as safety-oriented automotive power architectures increasingly require reliable monitoring, control, and protection around regulated rails.

- February 2026: Microchip and Hyundai Motor Group began collaborating to explore 10BASE-T1S Single Pair Ethernet for future automotive connectivity. This matters for supervisory ICs as more connected vehicle architectures require dependable reset, watchdog, voltage-monitoring, and protection functions to support increasingly distributed electronic control systems.

- January 2026: Microchip introduced a new 600V gate driver family for high-voltage power-management applications, reinforcing its role in robust power-control design. As automotive and industrial systems become more power-dense, the need grows for companion supervisory ICs that monitor rails, trigger resets, and maintain safe system operation.

- December 2025: The company, onsemi, announced development of next-generation GaN power devices with GlobalFoundries. While centered on power conversion, the move is relevant to supervisory ICs as more advanced power architectures require tighter voltage monitoring, reset control, and protection functions to ensure stable operation in compact, high-efficiency electronic systems.

- October 2025: Analog Devices launched ADI Power Studio, a web-based design environment that helps engineers model power architectures, compare components, and improve efficiency analysis. This is relevant to the supervisory IC market as it strengthens adoption of ADI’s power-monitoring, reset, and supervisory solutions within broader power-system designs.

- September 2025: Bosch announced a strategic initiative to integrate NVIDIA DRIVE AGX Thor into future compute and ECU architectures for software-defined vehicles. This development is important for supervisory ICs as centralized, high-performance automotive electronics require robust voltage monitoring, reset sequencing, watchdog supervision, and system protection.

- July 2025: Bosch advanced its automotive semiconductor portfolio with new radar and connectivity solutions, reflecting broader progress in vehicle electronics. This is relevant to supervisory IC demand as higher electronic complexity in ADAS and control architectures increases the need for dependable monitoring, reset, watchdog, and fail-safe power-support functions.

REPORT COVERAGE

The global automotive supervisory market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Vehicle Type, Voltage, Application, AEC Grade, ASIL Level, Propulsion Type, and Region |

| By Product Type |

|

| By Vehicle Type |

|

| By Voltage |

|

| By Application |

|

| By AEC Grade |

|

| By ASIL Level |

|

| By Propulsion Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.68 billion in 2025 and is projected to reach USD 2.96 billion by 2034.

In 2025, the market value stood at USD 0.98 billion.

The market is expected to exhibit a CAGR of 6.8% during the forecast period.

The SUV segment led the market by vehicle type.

The rising adoption of software-defined vehicles to accelerate supervisory systems demand.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 248

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us