Automotive Tire Inflator Market Size, Share & Industry Analysis, By Product Type (Portable 12V DC Inflators, Cordless/Battery-Powered Inflators, AC-Powered Inflators and Heavy-Duty/Commercial Inflators), By Vehicle Type (Two Wheeler, Passenger Cars and Commercial Vehicles), By Distribution Channel (Online Retail and Offline Retail), By Power Source (12V DC (Vehicle-powered), Rechargeable Battery (Lithium-ion), AC Powered and Manual/Foot Pump), By Pressure Capacity (Up to 100 PSI, 100–150 PSI and Above 150 PSI) and Regional Forecast, 2026-2034

Automotive Tire Inflator Market Size and Future Outlook

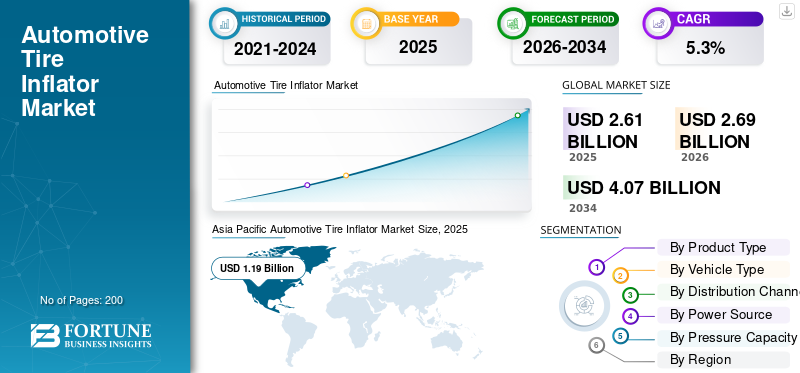

The automotive tire inflator market size was valued at USD 2.61 billion in 2025. The market is projected to grow from USD 2.69 billion in 2026 to USD 4.07 billion by 2034, exhibiting a CAGR of 5.3% during the forecast period. Asia Pacific dominated the automotive tire inflator market with a market share of 45.59% in 2025.

An automotive tire inflator is a compact air compressor used to inflate vehicle tires to the recommended pressure level. It operates by drawing in ambient air, compressing it through an internal motorized pump and delivering it into the tire via a connected hose and nozzle. Tire inflators can be powered by a vehicle’s 12V outlet, rechargeable batteries, or AC power sources.

Key drivers for the market include rising global vehicle parc, higher awareness of tire-pressure safety and fuel economy, growing SUV and fleet usage, and the shift toward spare-tire deletion and mobility services needing uptime. Strong e-commerce distribution and adoption of digital/cordless inflators also lift demand and average selling prices.

Major players in the market include VIAIR, Slime (ITW), Michelin, Bosch, Stanley Black & Decker, Makita, Ring/OSRAM, and Xiaomi/70mai. The key trend adopted by these companies are premiumisation, more cordless lithium-ion inflators with preset pressure, auto shut-off, faster fill rates, and compact designs. Brands also expand online sales and bundle inflators into emergency kits and mobility/fleet solutions.

Download Free sample to learn more about this report.

AUTOMOTIVE TIRE INFLATOR MARKET TRENDS

Premiumization and Cordless Innovation is Emerging Market Trend

The global market is witnessing a clear shift toward cordless, lithium-ion-powered and digitally controlled devices. Consumers increasingly prefer compact inflators with preset pressure settings, automatic shut-off, faster airflow and USB charging. This transition is raising the average selling price and expanding value share beyond basic 12V models. Premium inflators are particularly gaining traction in North America, Europe, and urban Asia, where convenience and multi-use functionality is significant. Integration into emergency mobility kits and EV accessory portfolios further strengthens this trend.

- In March 2024, Bosch highlighted its EasyPump cordless inflator with digital pressure sensors display and auto-stop functionality as part of its expanding DIY power tool portfolio, reinforcing the premium cordless shift.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expanding Global Vehicle Parc and Fleet Activity Drives Market Expansion

The steady expansion of the global vehicle parc, combined with growth in commercial fleets and ride-hailing services, is driving automotive tire inflator market growth. Proper tire pressure directly affects fuel efficiency, tire longevity and operational uptime which are critical factors for private owners and fleet operators alike. As spare tire deletion becomes more common, inflator kits serve as primary roadside solutions. Additionally, increased long-distance logistics activity surges demand for higher-capacity inflators in commercial vehicles. The growing number of vehicles on the road is expanding the installed base, requiring periodic inflator replacements or upgrades.

- In July 2021, the U.S. Energy Information Administration reported that the global light-duty vehicle fleet stood at 1.31 billion in 2020 and is projected to reach 2.21 billion by 2050, indicating sustained vehicle growth.

MARKET RESTRAINTS

Price Sensitivity and Low-Cost Imports Limits Margin Expansion

Intense price competition, particularly from low-cost automotive manufacturer, remains a restraint the market growth. Entry-level 12V models are widely available at low price points across e-commerce platforms, creating downward pressure on margins for branded players. In developing markets, purchasing decisions are often driven by price rather than advanced features. This limits rapid premium adoption and compresses profitability in the mass segment. Furthermore, the commoditization of portable tire inflators reduces product differentiation in basic categories, making it challenging for manufacturers to sustain strong pricing power without continuous innovation.

MARKET OPPORTUNITIES

Growth in Electric Vehicles and Spare-Tire Deletion Creates an Aftermarket Opportunity

Electric vehicles increasingly eliminate spare tires to reduce weight and optimize space, replacing them with tire repair kits that often include compact inflators. This structural shift creates long-term aftermarket opportunities for both OEM-supplied inflators and consumer upgrades. EV owners are more receptive to portable, battery-powered devices compatible with digital ecosystems. As EV penetration rises globally, the need for reliable, compact inflators becomes embedded within vehicle safety expectations.

- In October 2023, Michelin introduced updated tire repair and inflator solutions for modern vehicles, emphasizing compact emergency kits suitable for space-constrained platforms, supporting the growing role of inflators in mobility solutions.

MARKET CHALLENGES

Product Reliability, Safety Compliance and Performance Expectations Intensify Competitive Pressure

Meeting safety, durability and performance standards presents an ongoing challenge for manufacturers. Inflators must deliver accurate pressure readings, withstand overheating risks and maintain consistent airflow under varying climatic conditions. Failure can lead to safety concerns, reputational damage and product recalls. Additionally, regulatory and consumer expectations for reliable emergency equipment are rising. Manufacturers must invest in testing, quality control, and certifications while balancing cost competitiveness. As product complexity increases with digital components and lithium-ion batteries, technical reliability becomes a key differentiator and operational challenge in the global market.

Segmentation Analysis

By Product Type

Widespread Vehicle Compatibility Sustains Portable 12V DC Inflator Leadership

Based on product type, the market is segmented into portable 12V DC inflators, cordless/battery-powered inflators, AC-powered inflators and heavy-duty/commercial inflators.

By product type, portable 12V DC inflators segment held the highest automotive tire inflator market share due to their affordability, universal compatibility with vehicle cigarette lighter sockets, and ease of storage. These inflators are widely preferred for emergency roadside use and are commonly included in basic vehicle safety kits. Their cost-effective positioning makes them highly attractive in both developed and emerging markets, particularly among first-time car buyers.

The cordless/battery-powered Inflators segment is projected to grow at a 7.9% CAGR over the forecast period.

- In January 2023, VIAIR highlighted the continued demand for its portable 12V compressor series designed for everyday vehicle owners and light trucks.

By Vehicle Type

Expanding Global Passenger Car Parc Reinforces Segment Dominance

Based on vehicle type, the market is segmented into two wheelers, passenger cars, and commercial vehicles.

By vehicle type, passenger cars dominate the global market owing to the massive global passenger vehicle parc and frequent urban usage. Passenger car owners increasingly rely on compact inflators as spare tires are being removed from many models. Regular tire pressure maintenance for fuel efficiency and safety further supports recurring purchases in this segment. The large installed base ensures steady replacement demand worldwide.

The two-wheeler segment is projected to grow at a CAGR of 6.4% over the forecast period.

- In May 2024, OICA reported that passenger cars account for the majority of global motor vehicle production, underscoring the scale of this segment.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

Established Retail Networks Led to Offline Channel Segment Dominance

Based on distribution channel, the market is segmented into online retail and offline retail (auto stores, mass merchandisers, workshops).

By distribution channel, offline retail dominates due to strong consumer preference for physical inspection, immediate availability, and workshop recommendations. Automotive accessory stores and service centers frequently upsell inflators during tire replacement or maintenance visits. In many developing markets, physical retail remains the primary channel for purchasing automotive accessories, reinforcing the offline channel's share.

The online retail segment is projected to grow at a CAGR of 8.8% over the forecast period.

By Power Source

Universal 12V Socket Availability Strengthens Demand for 12V DC Power Sources

Based on power source, the market is segmented into 12V DC (Vehicle-powered), rechargeable battery (Lithium-ion), AC-powered, and manual/foot pump.

By power source, 12V DC (Vehicle-powered) inflators dominate due to compatibility with nearly all passenger vehicles equipped with auxiliary power outlets. Their dependable power supply and straightforward operation make them a preferred emergency solution. Price accessibility also supports strong penetration across both mature and developing markets.

The rechargeable battery (Lithium-ion) segment is projected to grow at a 9.1% CAGR over the forecast period.

- In September 2022, Stanley Black & Decker emphasized expanding its cordless automotive accessory portfolio under the BLACK+DECKER brand, highlighting growing demand for battery-powered products.

By Pressure Capacity

UV and LCV Expansion Elevates 100–150 PSI Inflator Segment Growth

Based on pressure capacity (PSI range), the market is segmented into Up to 100 PSI (Cars & Bikes), 100–150 PSI (SUVs & LCVs), and Above 150 PSI (HCV & Commercial Use).

By pressure capacity, 100–150 PSI inflators dominate, driven by increasing adoption of SUVs and light commercial vehicles globally. These vehicles require higher tire pressures than standard sedans, underscoring demand for mid-range capacity inflators that balance power and portability.

The Above 150 PSI (HCV & Commercial Use) segment is projected to grow at a 7.3% CAGR over the forecast period.

AUTOMOTIVE TIRE INFLATOR MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

Asia Pacific Automotive Tire Inflator Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Strong vehicle ownership levels, high road travel frequency, and increasing adoption of cordless automotive accessories support steady growth in North America market. The region benefits from a mature aftermarket ecosystem, a strong DIY culture, and high SUV and light-truck penetration, which drive demand for mid to high-PSI inflators. Growing e-commerce sales channels and the adoption of premium cordless products further elevate average selling prices. Fleet operators and ride-hailing drivers increasingly invest in compact inflators to reduce downtime. Product innovation, particularly in lithium-ion-powered and digital preset inflators, continues to strengthen regional market expansion.

U.S. Automotive Tire Inflator Market

The U.S. dominates the North American market with USD 0.42 billion in 2025, driven by its large passenger vehicle parc and strong pickup/SUV penetration. A DIY maintenance culture and the widespread adoption of cordless power tools are accelerating demand for battery-powered inflators. Growth in e-commerce automotive accessory sales and fleet logistics activity further supports mid- to high-PSI inflator demand across consumer and commercial segments.

Europe

Europe market growth is supported by a large installed vehicle base, rising awareness of the link between proper tire pressure and improving fuel efficiency, and the increasing adoption of compact inflators driven by spare tire reduction. Premiumization trends are evident, particularly in Western Europe, where consumers favor digitally controlled, rechargeable devices. Expanding SUV and light commercial vehicle sales support mid-range PSI demand. Additionally, strong automotive accessory retail networks and developing online platforms contribute to consistent revenue growth across major European economies.

U.K. Automotive Tire Inflator Market

The U.K. market benefits from high urban vehicle density and growing e-commerce penetration for automotive accessories. Consumers increasingly prefer compact, portable inflators due to space-saving vehicle designs. Growth in hybrid and electric vehicles, which often lack spare tires, further supports demand for compact inflator kits. U.K. was valued at USD 0.09 billion in 2025.

Germany Automotive Tire Inflator Market

Germany’s strong automotive base and high vehicle ownership underpin stable inflationary demand, with a CAGR of 4.6%. The country’s emphasis on vehicle maintenance standards and premium automotive accessories supports higher adoption of advanced cordless and digital inflators. Growth in commercial transport and light logistics vehicles also sustains demand for higher-PSI-capacity products.

Asia Pacific

It holds a significant share in the global growth due to its large vehicle production footprint and expanding vehicle parc. Rising middle-class incomes, strong two-wheeler penetration, and increasing SUV sales are contributing to inflationary pressures. Portable 12V models remain popular, but cordless adoption is accelerating in urban markets. Rapid e-commerce expansion across China and India enhances product accessibility. Commercial fleet growth in emerging Southeast Asian markets further supports higher-capacity inflator demand, making APAC both the largest and one of the fastest-growing regions globally.

China Automotive Tire Inflator Market

China leads the Asia Pacific market and held 44.4% share in 2025, driven by massive passenger vehicle production and growing SUV penetration. The growing adoption of digital automotive accessories and the strong online retail ecosystem are driving demand for cordless inflators. Expansion of logistics and delivery fleets further supports mid- and high-PSI inflator usage.

Japan Automotive Tire Inflator Market

Japan’s mature automotive market emphasizes compact, high-quality inflators with precision pressure control. Limited parking space and compact vehicle designs drive demand for small, efficient inflators. Stable passenger vehicle ownership and light commercial transport activity support consistent aftermarket sales. Japan was valued at USD 0.15 billion in 2025.

India Automotive Tire Inflator Market

India’s fastest growth, with a 7.8% CAGR, is driven by its extensive two-wheeler base and rising passenger car ownership. Increasing highway travel and urban mobility demand affordable portable inflators. Rapid digital retail growth and improving consumer awareness about tire safety further accelerate market expansion.

Rest of the World

The Rest of the World region, including Latin America, the Middle East, and Africa market, shows emerging growth potential driven by rising motorization and expanding commercial transport activity. Portable, price-sensitive 12V inflators dominate due to affordability, while heavy-duty inflators gain traction in logistics-heavy economies. Improving road infrastructure and the gradual penetration of e-commerce are expected to enhance accessibility. Although the base is smaller than in Asia Pacific or North America, higher commercial vehicle intensity supports long-term growth, particularly in freight- and construction-driven markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Product Innovation, Cordless Expansion, and E-Commerce Leadership Define Competitive Intensity

The global market is characterized by strong competition among established compressor specialists, diversified tool manufacturers, and emerging consumer electronics brands. Key players such as VIAIR Corporation, Slime (ITW Global Brands), Michelin Lifestyle, Bosch, Stanley Black & Decker (BLACK+DECKER, Craftsman), Makita, Ring Automotive (OSRAM), and Xiaomi/70mai compete through portability, faster inflation rates, preset digital displays, auto shut-off functions, and lithium-ion battery integration. Companies increasingly differentiate through compact design, multi-nozzle compatibility, noise reduction, and bundled emergency kits. Strategic focus areas include expanding online distribution, strengthening aftermarket partnerships, and leveraging cordless tool ecosystems to cross-sell inflators. Premium brands emphasize durability and heavy-duty applications for SUVs and commercial vehicles, while value-focused brands compete aggressively on price in emerging markets.

- In January 2024, Milwaukee Tool expanded its M12 cordless inflator portfolio, reinforcing the growing emphasis on battery-powered automotive accessories within professional and consumer segments.

LIST OF KEY AUTOMOTIVE TIRE INFLATOR COMPANIES PROFILED

- VIAIR Corporation (U.S.)

- Slime (ITW Global Brands) (U.S.)

- Michelin Lifestyle Limited (U.K.)

- Robert Bosch GmbH (Germany)

- Makita Corporation (Japan)

- Stanley Black & Decker, Inc. (U.S.)

- Black+Decker (Stanley Black & Decker) (U.S.)

- Ring Automotive Ltd. (Osram) (U.K.)

- AstroAI (U.S.)

- Kensun Inc. (U.S.)

- GSPSCN (Ningbo Gaishi Photoelectric Co., Ltd.) (China)

- EPAuto (E-POWER International Co., Ltd.) (China)

- Anker Innovations (eufy brand – portable inflators) (China)

- Ryobi Limited (Techtronic Industries) (Japan)

- Goodyear (Licensed Automotive Accessories Division) (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Slime announced the Tire Inflator XL, positioned for faster inflation of larger, modern tire sizes. The launch messaging emphasized quick fill times, longer reach from a 12-V accessory connection, and added protection features, reflecting the market shift toward higher-capacity consumer inflators for SUVs and crossovers.

- January 2026: MVT Solutions (MVTS) reported certified track-test results showing that Aperia Technologies’ Halo automatic tire inflator delivered measurable fuel savings (1.19 gallons per 1,000 miles) during controlled testing on a 2026 Kenworth T680 tractor-trailer setup, supporting fleets’ ROI cases for automatic inflation to reduce underinflation losses.

- November 2025: Transense Technologies said it would launch the Translogik TLGi Digital Handheld Tyre Inflator at SEMA 2025 (Las Vegas). The product was positioned as a connected handheld tool for truck/bus applications, illustrating ongoing innovation around digital pressure accuracy, connectivity, and workflow efficiency in commercial tire inflation equipment.

- September 2025: Pressure Systems International (P.S.I.) launched TireView LIVE Pre-Check, using scan-to-view QR tags that enable drivers and maintenance teams to access real-time tire pressure and temperature data in a mobile browser. This release underscores the convergence of tire inflation/management with TPMS and telematics-driven inspection workflows.

- March 2025: Aperia announced an exclusive agreement with Goodyear to support Goodyear’s Tires-as-a-Service (TaaS) offering using Aperia’s Halo Connect i3 automatic tire inflation solution. The partnership demonstrates how inflator technology is being bundled into service-based fleet tire programs to achieve predictable uptime and cost control.

REPORT COVERAGE

The automotive tire inflator market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The automotive tire inflator market forecast provides a comprehensive competitive landscape, encompassing the largest market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.3% from 2026 to 2034 |

| Unit | Value (USD billion) |

| Segmentation | By Product Type, By Vehicle Type, By Distribution Channel, By Power Source, By Pressure Capacity, and By Region |

| By Product Type |

|

| By Vehicle Type |

|

| By Distribution Channel |

|

| By Power Source |

|

| By Pressure Capacity (PSI Range) |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.61 billion in 2025 and is projected to reach USD 4.07 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.19 billion.

The market is expected to grow at a CAGR of 5.3% during the forecast period of 2026-2034.

The offline retail segment led the market in the distribution channel segment.

Expanding global vehicle parc and fleet activity strengthens replacement demand.

Key market players include VIAIR, Slime (ITW), Michelin, Bosch, Stanley Black & Decker, and Makita.

Asia Pacific accounted for the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us