Autonomous Mission Planning Software Market Size, Share & Industry Analysis, By Platform (UAVs, UGVs, Underwater Vehicles, Satellite Mission Systems, and Others), By Deployment Mode (On-Premise, Edge-Deployed Software, & Others), By End User (Defense Forces, Aerospace & Defense OEMs, Defense R&D Agencies, Commercial Drone Operators, Space Agencies, & Others), By Application (Surveillance Mission Planning, Logistics & Resupply, and Others), By Technology (AI / ML-Based Planning, Digital Twin & Simulation, Sensor-Fusion-Enabled, & Others), & Regional Forecast, 2026-2034

Autonomous Mission Planning Software Market Size and Future Outlook

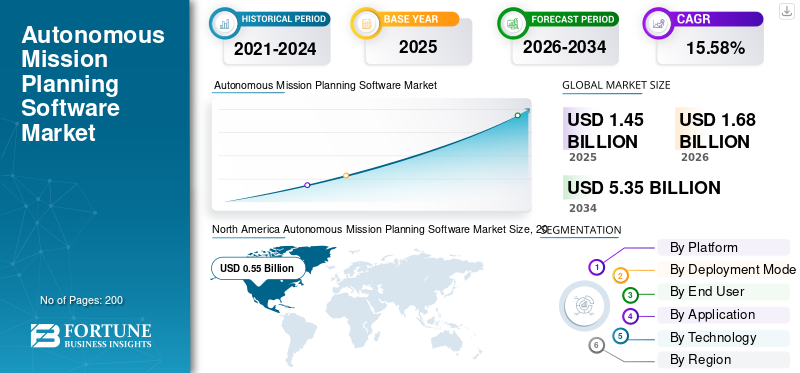

The global autonomous mission planning software market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.68 billion in 2026 to USD 5.35 billion by 2034, exhibiting a CAGR of 15.58% during the forecast period. North America dominated the autonomous mission planning software market with a market share of 37.93% in 2025.

The market comprises advanced software platforms that enable unmanned and crewed platforms to plan, replan, and execute complex missions in dynamic environments without constant human oversight. These systems integrate artificial intelligence, sensor fusion, and real‑time situational awareness to optimize flight paths, resource allocation, and threat adaptation across air, land, and maritime domains, thereby enhancing operational efficiency, force protection, and mission success in defense, aerospace, and homeland security applications. The market growth is driven by expanding fleets of unmanned systems, tighter integration of AI and real‑time data, and demand for mission planning software for safer, more efficient multi‑domain operations.

Key players in the market comprise Anduril Industries, Shield AI, Lockheed Martin, Northrop Grumman, Collins Aerospace, BAE Systems, Thales Group, Palantir Technologies, AeroVironment, and Auterion. These players are developing modular, AI‑enabled mission‑planning stacks for autonomous air, ground, and maritime platforms to support defended, networked, and scalable operations.

Download Free sample to learn more about this report.

Autonomous Mission Planning Software Market Takeaways

- 2025 Market Size: USD 1.45 billion

- 2026 Market Size: USD 1.68 billion

- 2034 Forecast Market Size: USD 5.35 billion

- CAGR: 15.58% from 2026–2034

- North America dominated the autonomous mission planning software market with a 37.93% share in 2025.

- The collaborative combat aircraft / loyal wingman platforms segment is projected to grow at a 16.39% CAGR during the forecast period.

- The containerized / modular open architecture software segment is expected to expand at a 16.27% CAGR over the forecast period.

North America

North America maintained its leading position, with the market increasing from USD 0.49 billion in 2024 to USD 0.55 billion in 2025.

Europe

Europe is projected to grow at a 15.63% CAGR and reach USD 0.39 billion by 2026, making it the second-largest regional market.

Asia Pacific

Asia Pacific is expected to reach USD 0.37 billion by 2026, emerging as the third-largest and fastest-growing regional market.

U.S.

The market is estimated to reach approximately USD 0.40 billion by 2026, expanding at a 15.83% CAGR during the forecast period.

Japan

The market is projected to reach around USD 0.07 billion by 2026, registering a 16.12% CAGR during the forecast period.

Read More

AUTONOMOUS MISSION PLANNING SOFTWARE MARKET TRENDS

Integration of Artificial Intelligence in Mission Planning Software is a Significant Market Trend

The integration of artificial intelligence into autonomous mission planning solutions is becoming a dominant trend, enabling platforms to generate, adapt, and execute mission plans with minimal human oversight. AI‑driven planners use machine learning and optimization algorithms to dynamically reroute paths, manage resources, and respond to evolving threats or environmental conditions in real time. Research and industry‑led initiatives show that AI‑based systems can tightly couple long‑term planning with on‑board reactive behavior for single and multi‑vehicle missions, improving safety, efficiency, and mission success in defense, aerospace, and unmanned‑systems domains.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Autonomous and Unmanned Systems in Defense to Drive Market Growth

The surging demand for autonomous and unmanned systems in defense is a key driver of investment in autonomous software for mission planning, as armed forces expand drone, unmanned ground, and maritime fleets to operate in high‑risk or contested environments. Governments are allocating tens of billions of dollars to autonomy and enabling software under new defense budgets, explicitly calling out autonomy as a separate line item to power coordinated, multi‑domain operations. This shift is motivated by the need to reduce human risk, increase operational tempo, and leverage AI‑driven coordination across platforms, which in turn increases the adoption of intelligent mission‑planning stacks for unmanned teams, driving autonomous mission planning software market growth.

MARKET RESTRAINTS

Limited Standardization across Mission‑Planning Interfaces is a Market Restraint

Limited standardization across mission‑planning interfaces is a significant restraint as differing formats, protocols, and data models hinder seamless interoperability between autonomous systems from different vendors or domains. Military and research‑led efforts highlight that heterogeneous unmanned platforms often require custom integration layers, which raise development cost, slow deployment, and complicate joint operations. NATO‑aligned work and maritime‑autonomy studies further note that non‑standard mission‑control and payload interfaces impede cohesive, multi‑vehicle mission planning, reinforcing the need for common standards to unlock scalable, interoperable autonomy.

MARKET OPPORTUNITIES

Modernization of Autonomous Fleets to Create New Market Opportunities

The modernization of autonomous fleets across defense, logistics, and industrial sectors is opening substantial market opportunities by the driving demand for advanced mission‑planning, fleet‑management, and AI‑enabled software stacks. As governments and operators upgrade to crew‑optional aircraft, UAV swarms, and unmanned surface or sub‑sea vehicles, they require scalable, interoperable planning tools that can coordinate multi‑platform operations, optimize resource use, and adapt to dynamic environments. This shift also stimulates adjacent opportunities in resilient navigation, cyber‑secure data links, and cloud‑connected command‑and‑control environments, making autonomous‑fleet software a strategic growth node in both military and commercial domains.

MARKET CHALLENGES

Cybersecurity Threats Present a Major Market Challenge

Cybersecurity threats present a major challenge for autonomous mission‑planning and fleet software, as connected, AI‑driven platforms expose large attack surfaces through command channels, data links, and onboard processing. Research on UAVs, unmanned vessels, and mission‑critical software highlights that adversaries can exploit firmware, communication protocols, and AI‑input pipelines to hijack platforms, disrupt swarm coordination, or corrupt mission plans. Protecting complex autonomous systems while maintaining real‑time performance and interoperability forces developers to balance stringent encryption, zero‑trust architectures, and secure‑coding practices against operational latency and integration costs, making cybersecurity a core constraint on growth.

Segmentation Analysis

By Platform

AI‑Driven Autonomy to Boost Unmanned Aerial Vehicles / Drones Segment Growth

Based on platform, the market is segmented into unmanned aerial vehicles / drones, collaborative combat aircraft / loyal wingman platforms, unmanned ground vehicles, unmanned surface & underwater vehicles, spacecraft / satellite mission systems, and others.

The unmanned aerial vehicles / drones segment is anticipated to account for the largest market share. AI‑driven mission planning software enables drones to autonomously generate, adapt, and optimize flight paths and sensor tasks, increasing mission efficiency and reducing reliance on constant human oversight. This autonomy is accelerating UAV adoption in defense, border security, and logistics, directly fueling segment growth.

The collaborative combat aircraft / loyal wingman platforms segment is anticipated to rise at a CAGR of 16.39% over the forecast period.

By Deployment Mode

Secure, Localized Deployment to Boost On‑Premise / Secure Facility Segment Growth

Based on deployment mode, the market is segmented into on-premise / secure facility deployment, edge-deployed software, cloud-based mission planning software, hybrid cloud-edge deployment, containerized / modular open architecture software, and others.

In 2025, the on-premise / secure facility deployment segment dominated the global market. On‑premise and secure‑facility deployments keep sensitive mission‑planning data and algorithms within controlled environments, meeting strict security and data‑sovereignty requirements. These aspects are driving the growth of the segment.

The containerized / modular open architecture software segment is projected to grow at a CAGR of 16.27% over the forecast period.

By End User

Defense Modernization and Multi‑Domain Operations to Boost Defense Forces/Armed Services Segment Growth

Based on end user, the market is segmented into defense forces / armed services, aerospace & defense OEMs, defense R&D agencies and test organizations, commercial drone operators, space agencies & satellite operators, and others.

The defense forces / armed services segment is anticipated to witness the largest autonomous mission planning software market share over the forecast period. Defense forces are modernizing fleets with unmanned systems and AI‑enabled planning tools to conduct multi‑domain, high‑tempo operations more safely and efficiently. The rising demand for autonomous swarms, loyal‑wingman concepts, and joint‑force coordination is driving strong growth within this end‑user segment.

The aerospace & defense OEMs segment is projected to grow at a CAGR of 16.14% over the forecast period.

By Application

Increasing ISR Complexity to Boost Intelligence, Surveillance & Reconnaissance Mission Planning Segment Growth

Based on application, the market is segmented into intelligence, surveillance & reconnaissance, mission planning, combat / strike mission planning, manned-unmanned teaming mission planning, logistics & resupply mission planning, maritime surveillance & mine countermeasure planning, and others.

The intelligence, surveillance & reconnaissance mission planning segment dominated the global market share in 2025. Growing ISR complexity across sensors, platforms, and threat environments pushes users toward autonomous planning software that can dynamically allocate assets and adapt plans in real time. This need for agile, multi‑sensor ISR planning is expanding the application‑specific segment.

In addition, the manned-unmanned teaming mission planning segment is projected to grow at a CAGR of 16.27% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Payload Flexibility to Boost AI / Machine Learning‑Based Planning Segment Growth

Based on technology, the market is segmented into AI / machine learning-based planning, optimization algorithm-based planning, multi-agent coordination algorithms, digital twin & simulation-based planning, sensor-fusion-enabled planning, and others.

The AI / machine learning-based planning segment dominated the market share in 2025. AI and machine learning‑based planning provide the flexibility to shift between rule‑based and adaptive, learning‑driven mission strategies, improving effectiveness in contested and dynamic environments. As platforms demand higher autonomy and resilience, AI‑based planning is becoming the core growth engine of the technology segment.

In addition, the multi-agent coordination algorithms segment is projected to grow at a CAGR of 15.98% during the analysis period.

Autonomous Mission Planning Software Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Autonomous Mission Planning Software Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 0.49 billion, and also maintained the leading share in 2025, with a value of USD 0.55 billion. Autonomous mission‑planning software is advancing rapidly in North America, supported by large‑scale U.S. defense investments in drones and AI‑enabled autonomy, including multi‑billion‑dollar programs for autonomous systems and contested‑logistics platforms.

U.S. Software Defined Satellite Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.40 billion in 2026. The market is anticipated to depict a CAGR of roughly 15.83% over the forecast period. The U.S. is the primary growth engine, with defense planners calling for tens of thousands of autonomous systems and investing heavily in AI‑driven mission planning, swarm control, and counter‑drone technologies. The Department of Defense’s AI strategy and related autonomy programs, along with significant R&D funding and test‑beds for autonomous combat aircraft, unmanned teams, and AI‑assisted targeting, are driving the demand for advanced, secure, and interoperable mission‑planning software for the U.S. military and its industrial partners.

Europe

The Europe market is projected to record a steady growth rate of 15.63% during the forecast period, which is the second highest among all regions. The market is anticipated to reach a valuation of USD 0.39 billion by 2026. Defense forces across Europe are investing in AI‑driven mission planning and autonomous systems to strengthen multi‑domain, NATO‑aligned operations while adhering to emerging AI‑ethics and regulatory frameworks.

U.K. Autonomous Mission Planning Software Market

The U.K. market is estimated to reach around USD 0.12 billion in 2026 and is poised to depict a CAGR of roughly 16.11% during the analysis period. The U.K. market is prioritizing robotics, autonomous systems, and AI in defense, with the Defence Science and Technology Laboratory (Dstl) and the Defence AI Centre actively developing autonomous platforms and AI‑assisted mission planning for air, land, and cyber operations.

Germany Autonomous Mission Planning Software Market

The Germany market is projected to reach approximately USD 0.11 billion in 2026. Germany is emerging as a core AI‑for‑defense hub in Europe, with national and EU‑level programs that emphasize AI‑driven mission planning, sensor fusion, and autonomous ground and maritime systems.

Asia Pacific

The Asia Pacific market is estimated to reach USD 0.37 billion in 2026 and secure the position of the third-largest and the fastest growing in the global market during the forecast period. The Asia Pacific region is witnessing strong growth, driven by rising defense budgets, regional security competition, and indigenous programs for unmanned aerial and maritime systems.

Japan Autonomous Mission Planning Software Market

The Japan market is estimated to touch around USD 0.07 billion in 2026 and showcase a CAGR of roughly 16.12% during the forecast period. Japan is formalizing AI‑driven mission planning and autonomous systems through new guidelines for AI‑integrated defense equipment and focused R&D on unmanned ground and aerial vehicles.

China Autonomous Mission Planning Software Market

The China market is projected to be one of the largest markets in Asia Pacific, with 2026 revenues estimated to be around USD 0.12 billion. China is advancing AI‑integrated mission planning and autonomous systems within the People’s Liberation Army, including AI‑driven ISR, autonomous targeting, and guidance for hypersonic and unmanned platforms.

India Autonomous Mission Planning Software Market

The India market is estimated to touch around USD 0.10 billion in 2026. India is expanding its autonomous mission‑planning ecosystem through AI‑driven ISR, drone swarms, and anti‑drone systems, supported by defense modernization and indigenization programs.

Rest of the World

The rest of the world includes the Middle East and Africa and Latin America. Across Latin America, the Middle East & Africa, defense modernization and sovereign‑wealth‑funded arms programs are accelerating the adoption of unmanned and AI‑enabled systems, which in turn boosts the demand for autonomous mission‑planning tools. The Middle Eastern states, in particular, are investing in indigenous drone, ISR, and AI‑based targeting capabilities. The Middle East & Africa and Latin America markets are set to reach USD 0.17 billion and USD 0.11 billion, respectively, in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships between Companies and Defense Agencies to Fuel Market Expansion

The autonomous mission planning software market is moderately consolidated, with specialized defense and aerospace technology leaders such as Anduril Industries, Shield AI, Lockheed Martin, Northrop Grumman, RTX (through Collins Aerospace), BAE Systems, Thales Group, Palantir Technologies, AeroVironment, and Auterion holding significant shares. This is due to their integrated AI‑driven mission‑planning stacks, compact autonomous control units, and modular software‑defined architectures tailored for multi‑domain defense, security, and logistics operations.

These players focus on advancing edge‑based AI, real‑time replanning engines, swarm‑control frameworks, and secure data‑link integration to address the evolving demand for high‑tempo, distributed missions and interoperability across heterogeneous unmanned platforms. Strategic partnerships are accelerating market expansion as Anduril Industries collaborates with the U.S. and allied defense agencies on AI‑driven command‑and‑control ecosystems for autonomous teams and Shield AI partners with NATO members on tactical AI‑pilot software for UAVs.

LIST OF KEY AUTONOMOUS MISSION PLANNING SOFTWARE COMPANIES PROFILED

- Anduril Industries (U.S.)

- Shield AI (U.S.)

- Lockheed Martin (U.S.)

- Northrop Grumman (U.S.)

- Collins Aerospace (U.S.)

- BAE Systems (U.K.)

- Thales Group (France)

- Palantir Technologies (U.S.)

- AeroVironment (U.S.)

- Auterion (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: The U.S. Army awarded Anduril Industries a deal worth up to USD 20 billion to purchase the defense startup's hardware, software, and services, which the Defense Department claims will expedite the delivery of technology to soldiers.

- February 2026: Shield AI, a deep-tech startup that develops cutting-edge autonomy software and aircraft, reported that Hivemind, its mission autonomy software, successfully finished its maiden flying test on Anduril's YFQ-44A aircraft. To support Technology Maturity and Risk Reduction (TMRR) initiatives, the U.S. Air Force recently chose Shield AI as a mission autonomy supplier for its Collaborative Combat Aircraft (CCA) program following a competitive examination. This flying test builds on that decision.

- December 2025: The FAST LabsTM research, development, and manufacturing division of BAE Systems received a USD 16 million Phase 2 contract for the Oversight program from the U.S. Defense Advanced Research Projects Agency (DARPA). The goal of the Oversight initiative is to develop an autonomous system that uses new satellite constellations to continuously monitor, a large number of terrestrial assets.

- August 2025: Boston-based Merlin revealed that the Scaled Composites Model 437 (M437) aircraft used in Northrop Grumman's Beacon testbed project will incorporate its Merlin Pilot autonomous software. According to the company, it will participate in regular planning sessions, provide engineering integration for software-in-the-loop testing and flight test operations, contribute to the creation of test procedures and documentation, and deploy staff on-site for flight tests.

- March 2025: Anduril was awarded a USD 86 million contract by the U.S. Special Operations Command to assist in the development and implementation of autonomy software capable of coordinating the actions of several drones and other robotic platforms in combat.

REPORT COVERAGE

The global autonomous mission planning software industry analysis includes a comprehensive study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, Porter’s Five Forces Analysis, company profiles, and retrofitting programs. Additionally, it details partnerships, mergers, and acquisitions, as well as key aviation industry developments and prevalence by key regions. The global market report includes an in-depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.58% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Platform, Deployment Mode, End User, Application, Technology, and Region |

| By Platform |

|

| By Deployment Mode |

|

| By End User |

|

| By Application |

|

| By Technology |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at 1.45 billion in 2025 and is projected to reach USD 5.35 billion by 2034.

In 2025, the North America market value stood at USD 0.55 billion.

The market is expected to exhibit a CAGR of 15.58% during the forecast period of 2026-2034.

By platform, the unmanned aerial vehicles / drones segment is expected to dominate the market.

The rising demand for autonomous and unmanned systems in defense is a key factor anticipated to drive market growth.

Anduril Industries, Shield AI, Lockheed Martin, Northrop Grumman, Collins Aerospace, BAE Systems, Thales Group, Palantir Technologies, and AeroVironment are key players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us