Military Software Market Size, Share & Industry Analysis, By Software Layer (Embedded & Real-Time Software, Mission Systems Software, Middleware & Integration, Data Management, Analytics/AI/Autonomy, Cybersecurity Software, Network/Communications Software and Others), By Services and Others), By End User (Land Force, Air Force, Naval Force, Special Mission Forces and Government Agencies), And Regional Forecast 2026-2034

KEY MARKET INSIGHTS

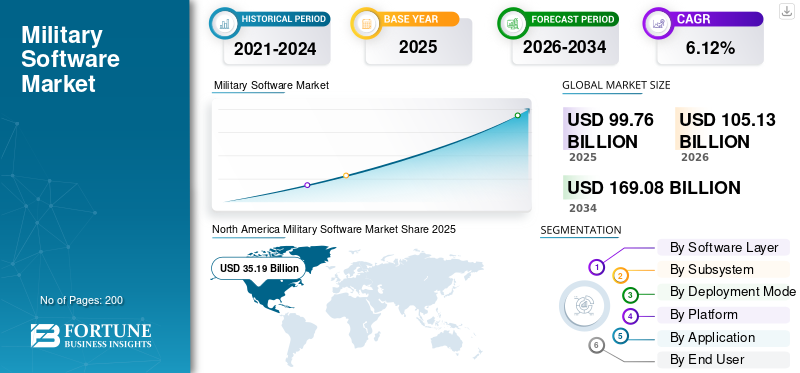

The military software market size was valued at USD 99.76 billion in 2025. The market is projected to grow from USD 105.13 billion in 2026 to USD 169.08 billion by 2034, exhibiting a CAGR of 6.12% during the forecast period. North America dominated the global market with a market share of 35.27% in 2025.

The primary factors accelerating the market growth include rising geopolitical tensions, border disputes and the need to upgrade military infrastructure using higher technology integration. The combination of artificial intelligence with machine learning is also accelerating market expansion owing to its ability to provide advanced decision-making algorithms, threat prediction analysis, automated system management and intelligent logistics analysis.

- For instance, Lockheed Martin received a USD 4.6 million contract from the Defense Advanced Research Projects Agency (DARPA) to create artificial intelligence tools for flexible, airborne operations under its Artificial Intelligence Reinforcements (AIR) initiative.

The industry is highly concentrated and competitive, led by large military contractors who integrate their own software into large military systems. Some of the key players operating include Lockheed Martin, Northrop Grumman, Raytheon Technologies, General Dynamics, Thales Group, Elbit Systems and IBM, among others.

Download Free sample to learn more about this report.

MILITARY SOFTWARE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 99.76 billion

- 2026 Market Size: USD 105.13 billion

- 2034 Forecast Market Size: USD 169.08 billion

- CAGR: 6.12% from 2026–2034

- North America dominated the market with a 35.27% share in 2025.

- The Mission Systems Software segment held the largest share of 23.69% in 2025.

- The Land Force segment accounted for the largest share of 33.78% in 2025.

North America

Held 35.27% of the global market in 2025, driven by high defense spending and rapid adoption of AI, autonomous systems, and advanced military technologies.

Europe

The market reached USD 26.85 billion in 2025 and is expected to register the fastest regional CAGR of 7.32%, supported by NATO defense initiatives and modernization programs.

Asia Pacific

The market is projected to grow at a 6.63% CAGR, fueled by rising geopolitical tensions and increasing investments in indigenous defense software capabilities.

U.S.

The market reached USD 32.78 billion in 2025, supported by strong defense spending and AI-driven military modernization.

Japan

The market reached USD 3.36 billion in 2025 and is projected to grow at a 6.39% CAGR, driven by increasing defense digitalization and software modernization initiatives.

Read More

Military Software Market Trend

Increasing Spending of Developing Nations on Advanced Technologies is an Emerging Market Trend

Developing nations are increasingly spending on cloud and cloud-related services, defence software for enabling edge-to-cloud connectivity, Cloud Edge Global Access (CEGA) architecture to implement Software-Defined Wide Area Network (SD-WAN) functionalities, Defence Operations Grid Mesh Accelerator (DOGMA), real time data processing and others. These technological trends showcases increased military investments in robust and modular networking designs that could maintain their operations even under a compromised communications environment that is common during military engagements.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Adoption of Artificial Intelligence and Machine Learning Integration Accelerates Market Growth

The inclusion of artificial intelligence and machine learning technologies in military software systems architecture is a major catalyst in military arena, transforming military capability development in a dramatic way by impacting the models adopted in deploying military autonomy. The new AI-based military systems are also being implemented in command control infrastructure to provide predictive threat analysis, target recognition, decision-making and combat strategies with a huge reduction in decision-making timelines, leading to a global military software market growth.

- For instance, in July 2024, Lockheed Martin contracted with DARPA for USD 4.6 million to develop new methodologies in modeling and simulation that utilize Artificial Intelligence/ Machine Learning algorithms in dynamic Multi-ship BVRA missions beyond visual ranges, with systems capable of processing unprecedented data volumes to facilitate faster decisions for the military.

Market Restraints

Regulatory Compliance Infrastructure and Cybersecurity Certification Mandates Hinder Market Growth

Defense industrial base functions under more complex regulatory regimes with strict cybersecurity certification norms, data security measures, and a means of evaluating for compliance, thus making the system more complicated or time-consuming for the development of military-grade software.

The U.S. Defense Department has introduced the Cybersecurity Maturity Model Certification (CMMC) in place of existing self-certification system for defense contractors and subcontractors through third-party reviews from designated CMMC assessment organizations for their adherence to strict cyber defense security practices including the growing adoption of the NIST-SP-800-171 protocol for Republic's Defense Industrial Base Secure Network.

Market Opportunities

Unmanned Autonomous Systems and Intelligent Battlefield Management Coordination Accelerates Market Growth Opportunities

The need to employ UASs has emerged as the most essential strategy that has materialized as a major market potential creating significant demand for special forces software that would address the coordination of autonomous vehicles and human-teaming algorithms. The increasing growth rate is attributed to higher government expenditure noticed within the AI-based Autonomous Platforms that include Unmanned Ground Vehicles (UGVs), Autonomous Aerial Vehicles (UAVs), and USVs.

- For instance, in July 2025, the U.S. Army had shown capabilities of self-guided quadruped robots. These robots are able to move along predetermined routes, carry military hardware, as well as broadcast battlefield management data in real time. This is noticeable within the military's focus on implementation of AI-controlled unmanned military actors that support troops instead of putting them on the front lines.

MARKET CHALLENGES

Software Development Lifecycle Complexity and Operator Involvement Deficits Hamper Market Growth

The military software development faces difficulties in systems acquisition processes that rely on outsourcing software development tools and techniques to contractor organizations. This is being outsourced with minimal end-user military operator engagement in design and architectures and pose inherently high risks of placing inefficient validated operational effectiveness and potential hidden vulnerability points in systems.

The traditional waterfall software development models adopted by companies that acquire defense systems, shrinks the military operator feedback mainly in systems testing and evaluation stages. This, due to high system design, change costs and feasibility, restrict organizational capabilities in discovering unforeseen operational scenarios and adjusting system architectures in response to identified vulnerabilities.

Segmentation Analysis

By Software Layer

Increased R&D Investments in Autonomous Weapon Systems Drives Analytics/AI/Autonomy Segmental Growth

Based on software layer the market is divided into Embedded & Real-Time Software, Mission Systems Software, Middleware & Integration, Data Management, Analytics/AI/Autonomy, Cybersecurity Software, Network/Communications Software, and Others.

Analytics/AI/Autonomy segment is estimated to be the fastest growing with a highest CAGR of 9.53% during the forecast period. The major driving factor for the segment growth is the increased R&D investments in autonomous weapon systems, counter-drone systems, unmanned platform synchronization and predictive analytics infrastructure for real-time threat evaluations and combat strategies.

The mission systems software segment is anticipated to rise with a CAGR of 4.89% and accounted for the largest market share with a 23.69% of share in year 2025.

By Subsystem

Increased Adoption of Fusion Technologies Leads to Fusion & Track Management Segment Growth

Based on subsystem the market is divided into Sensor Software, Fusion & Track Management, Navigation / Timing, Communications & Datalinks, and Others

The fusion & track management segment is estimated to be the fastest growing with a highest CAGR of 7.98% during the forecast period. The segment is growing due to increased adoption of fusion technologies, enabling military organizations to synthesize intelligence from heterogeneous sensor sources into coherent situational awareness architectures, supportive of rapid tactical decision-making. Tactical edge sensor fusion represents fundamental transformation in military intelligence gathering and battlefield awareness infrastructure, enabling orchestration of millions of distributed sensors into coherent intelligence pictures, providing unprecedented operational advantages spanning from reconnaissance to targeting, tracking, and engagement operations across contested domains.

The sensor software sub-segment is projected to grow at a CAGR of 5.23% and accounted for the largest market share in the global market with around 28.96% market share.

By Deployment Mode

Multi-Cloud Architecture and Tactical Edge Integration Accelerate Cloud-Based Segment Growth

Based on deployment mode the market is divided into On-Platform, Tactical Edge Servers, On-Premise, Cloud Based, and Hybrid (Edge + Enterprise).

The cloud based segment is estimated to be the fastest growing with a CAGR of 9.08% during the forecast period. This reflects accelerating adoption of sovereign defense cloud systems, allied collaborative defense networks and AI-powered decision support platforms requiring massive computational resources. Military operations are driving the need for hybrid tactical-cloud architectures wherein workloads move seamlessly between forward-deployed edge nodes performing time-critical processing to centralized cloud infrastructure that conducts large-scale analytics and model training in tactical force operations across disconnected, intermittent and limited communication environments.

On-Platform sub-segment is projected to grow at a CAGR of 4.24% during 2026-2034 and accounted for the largest market share of 34.74% in 2025 year.

By Platform

Increasing Use of Autonomous Aerial Vehicles Leads to Unmanned Systems Segment Growth

Based on platform the market is divided into dismounted/soldier-worn, ground platforms, air platforms, naval platforms, unmanned systems, and space platforms.

The unmanned systems segment is anticipated to be the fastest growing with a highest CAGR of 8.21%. The growth is driven by increasing use of autonomous aerial vehicles, ground vehicles, and underwater vehicles which are significantly changing the war paradigm. Regulatory evolution will drive UAVs from reconnaissance support roles to autonomous combat systems, positioning them as equal contributors in multi-platform military operations rather than force-multipliers to manned assets.

The air platforms segment is projected to grow at a CAGR of 6.72% and accounted for the largest market share with 26.80% in 2025.

To know how our report can help streamline your business, Speak to Analyst

By Application

Increasing Use of Artificial Intelligence-Assisted Threat Response Capabilities Leads to Electronic Warfare (EW) Segment Growth

Based on application the market is divided into C4ISR, Surveillance, Reconnaissance & Tracking, Targeting, Fires & Weapons Employment, Electronic Warfare (EW), Training, Simulation & Mission Rehearsal, Logistics & Transportation, Military Medical & Health Services and others.

Electronic Warfare (EW) is estimated to be the fastest growing segment with highest CAGR of 8.84% during the forecast period. The growth is driven by increasing use of artificial intelligence-assisted threat response capabilities, intelligent jamming algorithms and autonomous response to electromagnetic warfare in operations of spectrum dominance. Spectrum control solutions with artificial intelligence and electromagnetic superiority are imperative for multi-domain operations of armed forces currently. Electronic Warfare Operating Systems are quickest-growing segment of EW in the market.

C4ISR sub-segment is projected to grow at a CAGR of 7.86% and accounted for the largest market share of 22.36% in year 2025.

By End User

Cognitive Electronic Warfare and Adaptive Spectrum Operations Catalyze the Segmental Growth

Based on end user the market is divided into Land Force, Air Force, Naval Force, Special Mission Forces and Government Agencies.

The special mission forces segment is estimated to be the fastest growing with a highest CAGR of 7.47% during the forecast period of 2026-2034. The growth is driven by special operations forces operating in contested environments with degraded traditional infrastructure are driving adoption of advanced IT services, multi-cloud capabilities, and zero-trust security architectures.

The land force segment is projected to grow at a CAGR of 5.46% and accounted for the largest market share of 33.78% in year 2025.

Military Software Market Regional Outlook

The global market is divided into North America, Europe, Asia Pacific, Middle East & Africa and Latin America.

North America

North America Military Software Market Share 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America region is accounted for largest global military software market share of 35.27% in 2025 due to its commitment to heavy defense expenditure and swift pace of technology advancement led by the U.S. Department of Defense spending authority. North American military bodies are aggressively integrating technological supremacy in their efforts to fully integrate artificial intelligence and machine learning technologies into their military software infrastructure and in autonomous system development projects that could reshape modern warfare and market dynamics.

U.S. Military Software Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at USD 32.78 billion in 2025, with a growth rate of 5.29% CAGR.

Europe

Europe has estimated to be the fastest growing region at a highest CAGR of 7.32% during the forecast period of 2026-2034 and valued at a USD 26.85 billion in 2025. The growth is driven by strategic reset by NATO that has established gross domestic product-based defense spending targets and initiatives aimed at building the strength of defense industry to achieve technological sovereignty and avoid reliance on other nations for key military capabilities.

U.K. Military Software Market

The U.K. market share in 2025 reached at USD 5.03 billion and estimated to register a CAGR of 6.79% during the forecast period.

Germany Military Software Market

Germany’s market is reached USD 5.20 billion in 2025, and is projected to grow at a CAGR of 7.15% during the forecast period.

Asia Pacific

The Asia Pacific is the second-fastest-growing with a CAGR of 6.63% over the forecast period, driven largely by rising levels of geopolitical tensions among nations and a deliberate strategy to move away from reliance on foreign sources for their military software needs.

China Military Software Market

China’s market growth projected to be one of the largest in the region, within 2025 revenue to be USD 8.47 billion, representing a 4.42% of CAGR during the forecast period.

India Military Software Market

India’s market in 2025 reached USD 3.76 billion estimated with roughly 9.67% growth rate over the forecast period.

Japan Military Software Market

Japan’s market in 2025 estimated at around USD 3.36 billion with a growth rate of 6.39% during the forecast period.

Middle East & Africa

The Middle East & Africa region is an important market that is influenced by increasing military security competition, advanced defense systems procurement programs and regional defense industry base development strategies focused on domestic tech production and reduced reliance on external sources.

Israel Military Software Market

Israel’s market in 2025 estimated at around USD 1.38 billion accounting with roughly 14.29% of market share.

Latin America

Latin America is a moderately growing market that is generally characterized by resource-prescriptive budgets, competing development ambitions and defense modernization projects specifically focusing on indigenous tech development and a leading capability within Latin America.

COMPETATIVE LANDSCAPE

Key Market Players

Traditional Industry Leaders Maintain Dominance while Specialized Tech Firms Generating Market Growth Opportunities

The competitive landscape of the market is characterized by development of proprietary platforms, vertical integration of software systems into weapon platforms and collaborative partnerships among defense contractors to integrate operation capabilities.

The military software industry includes major defense contractors such as Lockheed Martin, Northrop Grumman, Raytheon Technologies, BAE Systems, and General Dynamics that have retained leadership through integration of proprietary military software solutions and comprehensive defense solutions offered through these companies.

These companies currently compete based on advanced AI, cybersecurity maturity, command and control system performance and sensor-to-shooter timelines. Emerging disruptive companies in the military software space are currently posing a threat to above leadership as they focus on unmanned military solutions and military communications via cloud computing solutions.

List of Key Global Military Software Company Profile

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- BAE Systems plc (U.K.)

- Thales S.A. (France)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- Airbus SE (Netherlands)

- Rheinmetall AG (Germany)

- Indra Sistemas, S.A. (Spain)

- Elbit Systems Ltd. (Israel)

- ASELSAN A.S. (Turkey)

- EDGE Group PJSC (UAE)

- L3Harris Technologies, Inc. (U.S.)

- Israel Aerospace Industries Ltd. (Israel)

- General Dynamics Corporation (U.S.)

KEY DEVELOPMENTS

- December 2025: V2X, Inc. announced that it has secured a USD 72 million contract to deliver engineering services and support for the Gateway Mission Router (GMR). The GMR is a cyber-defense secure solution designed to improve air-to-ground operations and is adaptable to changing mission requirements via open-standard interfaces. By effectively managing datalinks and platform capabilities, the GMR facilitates a comprehensive common operating picture that integrates situational awareness and command-and-control information across various formats.

- August 2025: Palantir has signed a contract with the U.S. Army valued at up to USD 10 billion to address increasing modern warfare requirements over the next ten years. Under this agreement, which provides a "comprehensive framework for the Army's future software and data needs," Palantir will assist the military in enhancing efficiencies while gearing up for potential threats, merging a total of 75 contracts into a single enterprise agreement.

- September 2025: Anduril Industries has announced that it received a USD 159 million contract from the U.S. Army for an initial prototyping stage to create a night vision and mixed reality system as part of the Soldier Borne Mission Command (previously known as IVAS Next) program. This contract marks the most extensive initiative to provide every soldier with enhanced perception and decision-making abilities by integrating the best aspects of night vision, augmented reality, and AI into one system.

- September 2025: Lockheed Martin Rotary and Mission Systems received a prototype agreement to collaborate with the U.S. Army, taking on the role of Team Lead to create a data-driven Next Generation Command and Control (NGC2) prototype. Lockheed Martin will lead a joint effort with the U.S. Army, utilizing its expertise in C2 systems engineering and project management.

- February 2025: Northrop Grumman Corporation has been awarded two major contracts worth USD 1.4 billion aimed at enhancing air and missile defense systems for the U.S. Army and Poland. These contracts bolster Northrop Grumman’s status as a frontrunner in cutting-edge integrated battle management solutions, promoting innovation through AI and model-based systems engineering to reinforce global security.

REPORT COVERAGE

The global military software market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product type launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating major players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.12% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Software Layer · Embedded & Real-Time Software · Mission Systems Software · Middleware & Integration · Data Management · Analytics / AI / Autonomy · Cybersecurity Software · Network / Communications Software · Others By Subsystem · Sensor Software · Fusion & Track Management · Navigation / Timing · Communications & Datalinks · Others By Deployment Mode · On-Platform · Tactical Edge Servers · On-Premise · Cloud Based · Hybrid (Edge + Enterprise) By Platform · Dismounted / Soldier-Worn · Ground Platforms · Air Platforms · Naval Platforms · Unmanned Systems · Space Platforms By Application · C4ISR · Surveillance, Reconnaissance & Tracking · Targeting, Fires & Weapons Employment · Electronic Warfare (EW) · Training, Simulation & Mission Rehearsal · Logistics & Transportation · Military Medical & Health Services · Others By End User · Land Force · Air Force · Naval Force · Special Mission Forces · Government Agencies By Region North America (By Software Layer, Subsystem, Deployment Mode, Platform, Application, End User and Country) · U.S. (By End User) · Canada (By End User) Europe (By Software Layer, Subsystem, Deployment Mode, By Platform, Application, End User and Country) · U.K. (By End User) · France (By End User) · Germany (By End User) · Nordic Countries (By End User) · Eastern Europe (By End User) · Rest of Europe (By End User) Asia Pacific (By Software Layer, Subsystem, Deployment Mode, Platform, Application, End User and Country) · China (By End User) · India (By End User) · Japan (By End User) · South Korea (By End User) · Southeast Asia (By End User) · Rest of Asia Pacific (By End User) Middle East & Africa (By Software Layer, Subsystem, Deployment Mode, Platform, Application, End User, and Country) · Israel (By End User) · Saudi Arabia (By End User) · UAE (By End User) · Turkey (By End User) · South Africa (By End User) · Rest of Middle East & Africa (By End User) Latin America (By Software Layer, Subsystem, Deployment Mode, Platform, Application, End User and Country) · Brazil (By End User) · Mexico (By End User) · Argentina (By End User) · Rest of Latin America (By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 99.76 billion in 2025 and is projected to reach USD 169.08 billion by 2034.

In 2025, the Europe market value stood at USD 26.85 billion.

The market is expected to exhibit a CAGR of 6.12% during the forecast period of 2026-2034.

The Electronic Warfare (EW) segment is expected to hold the highest CAGR over the forecast period.

Adoption of Artificial Intelligence and Machine Learning Integration Accelerates the Market Growth.

Lockheed Martin, Northrop Grumman, Raytheon Technologies, General Dynamics, Thales Group, Elbit Systems, and IBM, among others.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us