Command and Control System Market Size, Share & Industry Analysis, By Solution (Hardware, Software, Services, and Licensing Models), By Networks & Connectivity (Tactical RF, Commercial/Private, Backbone, and QoS/Latency Classes), By Integration Architecture (Standalone, Vehicle-Mounted, Federated, Fully Integrated/Joint All-Domain, and Open Architecture), By Installation (New Installation and Upgradation), By System (Communications & Networks, Weapon Control Systems, Command Posts, Security Systems, & Others), By Technology, By Platform, By End User, and Regional Forecast 2026-2034

KEY MARKET INSIGHTS

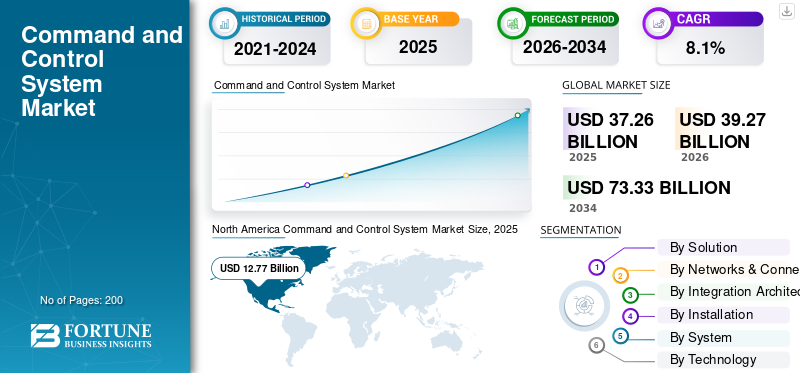

The global command and control system market size was valued at USD 37.26 billion in 2025. The market is projected to grow from USD 39.27 billion in 2026 to USD 73.33 billion by 2034, exhibiting a CAGR of 8.1% during the forecast period. North America dominated the command and control system market with a market share of 34.27% in 2025.

A C2 system is a centrally integrated technology infrastructure that provides aggregated, analyzed, and disseminated information in real-time to aid in strategic decision-making and operational coordination across heterogeneous sectors. These systems are the operational nexus, taking in heterogeneous streams of data emanating from sensors, communication networks, and personnel to create unified situational awareness.

C2 system serve critical functions across several domains such as military operations utilize these systems to facilitate coordination in troop movements, tracking of threats, and logistics with an enhanced understanding of situational awareness. Other domains include disaster response and emergency management utilize C2 systems to manage rescue operations and resource allocation in catastrophic events. Further, urban transportation infrastructure relies on these systems for monitoring and managing traffic and public transit, and industrial sectors utilize C2 solutions to maintain continuous operations through process automation, safety protocols, and incident responses.

The global command and control system market trend is experiencing remarkable growth and has significant growth momentum. Such growth is driven by a number of factors entwined together such as growing geopolitical tensions and regional security dynamics are raising the need for advanced situational awareness solutions. However, integrated military modernization programs across global defense establishments are increasing the demand for integrated C2 platforms. Further, transformative technologies such as artificial intelligence, machine learning, and Internet of Things enable predictive analytics and autonomous decision-making, the adoption of network-centric warfare doctrines places greater focus on information superiority and multi-domain operations, accelerating the deployment of unified command architectures. Moreover, growing cyber threats and critical infrastructure protection is boosting investments in secure and resilient communication networks.

The landscape of the global command and control systems market share is moderately consolidated, with only a few of the top key players being RTX Corporation (U.S.), Northrop Grumman Corporation (U.S.), BAE Systems plc (U.K.), Elbit Systems Ltd. (Israel), and Rheinmetall AG (Germany), among others. Established defense primes keep the edge in the competitive scenario through their capabilities in multi-domain integration, artificial intelligence-enabled decision support systems, cyber-hardened cloud infrastructure, and secure communications architectures.

Download Free sample to learn more about this report.

COMMAND AND CONTROL SYSTEM MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 37.26 Billion

- 2026 Market Size: USD 39.27 Billion

- 2034 Forecast Market Size: USD 73.33 Billion

- CAGR: 8.1% from 2026–2034

- North America dominated the command and control system market with a 34.27% share in 2025.

- The defense segment accounted for 53.33% of the global market in 2025.

- The hardware segment held a dominant 32.07% share of the market in 2025.

North America

North America held the largest regional share of 34.27% in 2025, supported by extensive defense modernization programs.

Asia Pacific

Asia Pacific is projected to be the fastest-growing region, registering a CAGR of 9.8% during the forecast period.

Europe

Europe remains a key market driven by NATO-led command modernization and interoperability initiatives.

U.S.

The market is supported by large-scale Joint All-Domain Command and Control (JADC2) programs and advanced defense investments.

Japan

Growing regional security requirements and defense modernization initiatives continue to support demand for advanced command and control systems.

Read More

MARKET DYNAMICS

Market Drivers

Geopolitical Tensions and Defense Modernization Imperatives Catalyze Market Growth

The growth of the market is powered fundamentally by increased geopolitical tensions and accompanying imperatives for the modernization of defense at all levels in world military forces. Near-peer competition dynamics, especially involving China and Russia, have mandated wholesale reassessment of military capabilities, forcing defense ministries to invest in state-of-the-art command architectures able to coordinate operations in real time.

- In May 2024, Lockheed Martin unveiled an AI-driven command-and-control platform tailored for JADO; it demonstrated the ability to expedite decision-making processes using predictive modeling and real-time data integration.

The transformation of military doctrine toward network-centric warfare and multi-domain operations is a critical growth catalyst for C2 systems, with defense establishments recognizing that information superiority will determine the outcomes of operations; expect the market to grow accordingly.

Market Restraints

Cybersecurity Vulnerabilities and Compliance Complexities Can Hinder Market Growth

The vulnerability of C2 systems to sophisticated cyber threats is an escalating constraint on system deploy ability and operational effectiveness, especially in a more connected and information-sharing environment across networked architectures that expands the attack surface for adversarial cyber operations. Organizations struggle to stay compliant with international data protection regulations, including GDPR, while at the same time developing multi-layer cybersecurity in defense networks based on zero-trust security models, end-to-end encryption, intrusion detection systems, and breach response protocols.

The integration of legacy systems amplifies the complexity of cybersecurity, where outdated mechanisms for authentication, limited audit logging capabilities, and deficiencies in data protection expose sensitive command infrastructure to increased risks of breaches.

Market Opportunities

Autonomous Systems Integration and Swarm Intelligence Coordination Create Exceptional Market Growth Opportunity

The integration of unmanned aerial vehicles, unmanned ground vehicles, and autonomous maritime platforms into centralized command architectures presents significant revenue opportunities as military organizations across the world move toward multi-platform autonomous fleet operations. Advanced cloud-based integrated command and control platforms have AI-driven orchestration algorithms that enable seamlessly coordinated heterogeneous autonomous vehicle swarms operating across multiple domains, requiring sophisticated task delegation, path planning, and autonomous communication capabilities.

- In June 2024, Airbus Defense and Space unveiled its Wingman concept at the ILA Berlin aerospace exhibition, representing an unmanned fighter-type aircraft capable of receiving command directives from manned combat aircraft pilots while doing high-risk reconnaissance and engagement tasks.

Organizations such as Advanced Navigation have developed Cloud Ground Control platforms that enable multi-vehicle operations management through simplified browser interfaces, with edge AI processing capabilities that support real-time object detection and classification, creating differentiated market solutions. As future defense doctrines place greater emphasis on dispersed autonomous operations across contested environments, the command systems will need to be able to manage hundreds of coordinated autonomous assets with minimal human intervention-a development that opens up substantial architectural innovation opportunities.

Command and Control System Market Trends

Cloud-Native Architecture and Edge Computing Integration Anticipate Technological Trend in Upcoming Market Trajectory

Defense organizations increasingly adopt cloud-native command and control architectures that support distributed operations, remote accessibility, and scalable computational capacity required for managing large-scale multi-domain operations. Multi-access edge computing architectures position computational resources proximate to tactical edge units, significantly reducing communication latency and enabling time-sensitive decision support functions essential for autonomous system coordination and rapid threat response.

- In March 2025, Lockheed Martin demonstrated its self-funded CJADC2 Interoperability Factory, incorporating generative AI throughout the technology stack to enable AI-infused services capable of orchestrating thousands of battlefield entities in real time through an open and automated integration of existing weapon systems and sensors.

The integration of 5G connectivity with edge computing creates distributed intelligence architectures where sophisticated data analysis algorithms execute locally on forward-deployed platforms, reducing dependencies on rear-area joint operations command centers while maintaining centralized strategic oversight. Software-defined network architectures dynamically allocate resources and provide network slicing capabilities, which enable mission-critical applications to receive prioritized bandwidth and computational resources. Further, ensuring resilience and responsiveness in contested electromagnetic environments.

Download Free sample to learn more about this report.

Market Challenges

Supply Chain Vulnerabilities, Regulatory Compliance, and Semiconductor Component Constraints Hamper Market Growth

Large, complex supply chains form the backbone of most defense C2 systems, utilizing specialized semiconductor components, such as microcontrollers, advanced processors, memory devices, and RF components. Many are in sustained supply shortage, driven by geopolitical tensions and industrial capacity concentration.

Taiwan and South Korea concentrate critical semiconductor manufacturing capacity for components integral to defense systems, creating strategic vulnerabilities that could be disrupted by natural disasters, political instability, or deliberate supply chain manipulation. The Trump Administration's tariffs on electronic components and semiconductors greatly impact the production cost and continuity of supply chains of defense contractors. Consequently, the large investment required for expanding domestic manufacturing capacity and diversifying suppliers was needed.

SEGMENTATION ANALYSIS

By Solution

AI-Enabled Analytics and Cloud-Native Architecture Acceleration in Software Segment Anticipate Segmental Growth

The global market is segmented by solution is further classified into hardware, software, services, and licensing models

The software segment is projected to be the fastest-growing in the global market size, recording compound annual growth rates of 8.5% during the forecast period. Further, reflecting a basic market transformation toward intelligent decision-support systems and away from traditional fixed-function infrastructure. Advanced software platforms with built-in artificial intelligence, machine learning, and real-time data fusion capabilities allow commanders to process exponentially expanding sensor data streams from heterogeneous sources-satellite imagery, unmanned aerial vehicle feeds, signals intelligence, and terrestrial reconnaissance-with substantially reduced cognitive burden on human operators while accelerating observation-orientation-decision-action cycle execution so essential for tactical communication networks advantage in contested environments.

- In April 2024, the NATO Communications and Information Agency contracted Systematic GmbH to provide SitaWare Headquarters command and control software solutions valued at USD 28.21 million to fulfill NATO's Future Land Command and Control capability requirement under Project DEMETER, representing institutional commitment to modern software-defined command architecture across alliance structures.

The hardware segment keeps dominant market positioning with a share of 32.07% in the global market share, driven by a continued need for advanced, mission-critical physical components to provide the foundational infrastructure that enables real-time data acquisition, processing, transmission, and secure communication across multi-domain operations. Hardware modernization pertains to displays, communication terminals, computing systems, and sensors, forming an essential architectural foundation for C2 systems. Specialized ruggedized computing platforms, high-performance display modules, and encrypted transmission equipment require substantial capital investment to justify the dominance of the hardware segment in the market, in spite of the higher growth velocity of software.

By Networks & Connectivity

Private 5G and Satellite Connectivity Acceleration Aids the Segmental Growth for Commercial/Private Sub-Segment

The global market is segmented by networks & connectivity is further classified into tactical RF, commercial/private, backbone, and QoS/latency classes

The Commercial/Private Networks sub-segment represents the fastest-growing within the broader networks and connectivity infrastructure, at compound annual growth rates of 9.8% during forecast period of 2026-2034 within the private 5G networks market specifically, dramatically exceeding traditional tactical RF communication expansion. Private 5G networks with cellular grade ultra-reliable low-latency communication, network slicing capabilities that allow mission-critical applications to be prioritized, and deterministic connectivity characteristics are transforming command and control architectures beyond conventional dependency on public cellular, with global spending on private LTE and 5G network infrastructure continuing to grow at a significant rate.

- In October 2024, the Department of Defense, U.S., officially released its Private 5G Deployment Strategy that provided institutional guidance on implementing and operating a private fifth-generation network at military installations while maximizing Open Radio Access Network ecosystems. Private networks may augment or supplement commercial services to fulfill the DoD's mission, security, coverage, and performance requirements that cannot be independently satisfied by commercial 5G infrastructure.

The tactical RF sub-segment remains dominating the global market representing the valued USD 11.96 billion in 2025 across global command and control system market share, reflecting enduring requirements for specialized RF communications platforms that form an essential backbone of battlefield command and control architectures across land, air, maritime, and special operations domains.

By Integration Architecture

Multi-Domain Sensor-to-Shooter Network Revolution and Coalition Interoperability Acceleration Anticipate the Market Growth

The global market is segmented by integration architecture is further classified into standalone, vehicle-mounted, federated, fully integrated/joint all-domain, and open architecture.

The fully integrated architecture/JADC2 sub-segment is estimated to be the fastest-growing and is expected to exhibit a CAGR of 9.6% from 2026 - 2034. Fully integrated architecture unifies what has traditionally been a fragmented service-branch set of command systems into common sensor-to-shooter networks with seamless real-time information exchange across the land, air, maritime, space and satellite command systems, and cyber domains via artificial intelligence-driven decision support algorithms, cloud-native software platforms, and distributed edge computing nodes that eliminate legacy command stovepipes and enable decision cycles measured in mere seconds rather than minutes.

- In March 2025 The US Army reached a critical milestone in Project Convergence Capstone 5 at the National Training Center: soldiers put the Next Generation Command and Control-NGC2 system into operation in realistic scenarios that validated the federated-to-fully-integrated transition approach to architecture. As Colonel Michael Kaloostian confirmed, requirements documentation is running parallel with the strategy of development for rapid market solicitation after proof-of-principle validation.

The federated architecture sub-segment maintains dominant market positioning, accounting for about 26.94% of the global market share. Dominance reflects the persistent organizational requirement for loosely coupled command architectures that allow the preservation of legacy systems, phased modernization approaches, and service-branch autonomy while achieving minimum viable interoperability across essential operational functions. Federated architecture allows independently operated command systems by different military services, government agencies, and allied nations to maintain autonomous governance and technical control while creating intermediate integration layers that allow the selective sharing of data through standardized message formats, common operational picture feeds, and coordination protocols without wholesale adoption of unified system infrastructure.

By Installation

Greenfield Facility Development and Multi-Domain Architecture Deployment Creates Significant Demand for New Installation Systems

The global market is segmented by installation is further classified into new installation and upgradation.

The new installation sub-segment represents both the fast-growing and dominating in the market, commanding about 51.38% of the share in 2025, while showing a compound annual growth rate of 8.4% 2026-2034, reflecting the continued need of organizations for modern command infrastructure that supports evolved operational needs. Similarly, defense agencies and homeland security command systems departments across different parts of the world pursue new comprehensive command center deployment initiatives equipped with advanced communication networks, AI-powered visualization interfaces, real-time data analytics in defense fusion capabilities, and cloud-native architecture frameworks that allow unparalleled situational awareness and decision velocity across multi-domain operations in land, air, maritime, space, and cyber. Greenfield installation opportunities arise from evolving threat landscape characterization, including asymmetric warfare, terrorism proliferation, and cyber-attack sophistication, which requires modern command infrastructure that is fundamentally impossible to retrofit into legacy systems, thus creating a continued market need for new facilities purposefully built to incorporate contemporary cybersecurity standards, distributed architecture principles, and autonomous system management capabilities.

- In April 2025 Integration Center (EPIC) in Madison, Alabama, representing a USD 20 million investment in manufacturing infrastructure to support accelerated production of the Integrated Battle Command System for new Army installations and foreign military sales deliveries. Facility expansion doubles previous integration capacity and incorporates advanced digital manufacturing approaches that enable rapid fielding of new command center components supporting U.S. military modernization and allied force transformation initiatives.

The upgradation sub-segment represents the second-fastest installation category, continually showing market growth driven by organizational requirements to modernize existing joint operations command centers with enhanced capability while preserving substantial historic infrastructure investments and operational continuity across active command facilities managing critical functions of national defense.

By System

Multi-Domain Connectivity Infrastructure Leadership and Satellite Communications Expansion and Network Resilience Architecture Drives the Segmental Growth

The global market is segmented by system is further classified into communications & networks, weapon control systems, command posts, security systems, transportation management systems, health & public services systems, emergency management system, and others.

The communications & networks sub-segment represents both the fastest-growing and simultaneously dominating component within the market, dominating about 23.83% of share and exhibiting sustained expansion driven by comprehensive network-centric warfare transformation initiatives across global defense establishments. Military communication networks form an essential backbone infrastructure for command and control operations across all domains, reflecting institutional recognition that resilient, secure, and interoperable communications represent non-negotiable prerequisites for modern multi-domain operations success. Advanced tactical radio systems incorporating software-defined architectures, Link 16 resilient communication protocols, high-frequency extended-range capabilities, and satellite communication terminals enable seamless information exchange across heterogeneous platforms including manned aircraft, unmanned vehicles, naval vessels, ground combat systems, and space-based assets requiring standardized waveforms and encrypted transmission methodologies supporting coalition force interoperability.

- In November 2024, L3Harris Technologies was awarded an Indefinite-Delivery/Indefinite-Quantity contract valued at $999 million by the U.S. Navy in support of Multifunctional Information Distribution System Joint Tactical Radio System Terminals that provide software-defined Link 16 resilient communication radios supporting air, ground, and maritime platforms across U.S. and coalition forces over a five-year delivery period, continuing the company's 24-year support record for delivering standard communications interoperability solutions to all U.S. armed services and 57 allied nations.

The emergency management system sub-segment is the second-fastest-growing in the market, recording a compound annual growth rate of 9.8% and indicating an increased organizational emphasis on coordinated crisis response capabilities that address natural disasters, terrorist threats, industrial accidents, and public health emergencies. Advanced C2 systems installed in emergency response management systems centers allow coordination among multiple agencies through unified command infrastructure in support of collaborative decision-making, resource deployment optimization, and real-time situational awareness in crisis scenarios that demand rapid response and sustained coordination across diverse stakeholder organizations.

By Technology

Intelligent Decision Support and Autonomous System Coordination Revolution Anticipated Segmental Growth Opportunities

The global market is segmented by technology is further classified into architecture & hosting, data & fusion, AI/autonomy, edge & networking, interoperability & links, and others.

The AI/autonomy segment is considered to be the fastest growth attribute with phenomenal compound annual growth rates of 10.0% through 2026-2034. Integration of AI fundamentally changes the command and control architecture as it enables autonomous threat prediction, real-time anomaly detection, and sophisticated sensor-to-shooter pairing optimization without requiring intervention by a human operator; machine learning algorithms analyze exponentially expanding data streams from satellite imagery, feeds from unmanned aerial vehicles, signals intelligence, and terrestrial reconnaissance, consolidating disparate information sources into a unified operational picture that allows the commander to act faster than adversarial forces.

- In May 2024, Northrop Grumman revealed advanced AI-enabled command modules that would significantly enhance battlefield management systems and infrastructure monitoring for better operational coordination in multi-domain operations scenarios, while reaffirming their institutional commitment to integrating autonomous decision support capabilities into existing battle management platforms.

Within the market, the edge & networking sub-segment maintains dominant positioning and is demonstrating substantial growth momentum during the forecast period. The growth reflects an institutional recognition that distributed processing architecture represents the essential foundation to enable real-time multi-domain command and control operations in contested electromagnetic environments where centralized processing infrastructure becomes vulnerable to disruption. Multi-access edge computing positions computational resources proximate to tactical communication networks, significantly reducing communication latency from traditional cloud processing delays down to milliseconds that enable time sensitive autonomous system coordination, rapid threat response, and management of distributed sensor networks without depending upon potentially vulnerable rear-area command center connectivity to adversarial jamming, frequency denial, or electronic warfare disruption.

By Platform

Remote Operations and Distributed Command Architecture Transformation Drives Segmental Growth

The global market is segmented by platform is further classified into land, maritime, air, space, and cyber/cloud/enterprise.

The cyber/cloud/enterprise sub-segment represents the fastest growth component within the Platform category, recording extraordinary compound annual growth rates of 10.1% through 2026-2034. Growth reflects institutional operational movement toward scalable, resilient, and cost-effective cloud-native command and control architectures, driven by organizational preference for flexible, scalable solutions that enable remote access by dispersed teams in support of collaborative command decision-making, real-time situational awareness consolidation, and seamless information exchange across organizational hierarchies without a physical colocation of command staffs.

- In February 2024, Rockwell Automation announced an extended strategic relationship with Microsoft focused on speeding up industrial digital transformation with Azure and edge computing. This combines FactoryTalk operational technology data with cloud services to enhance command center operations through native cloud integration, supporting real-time data analytics in defense, scalable processing capacity, and advanced artificial intelligence-driven decision support capabilities.

Land sub-segment retains its dominant market position in Platform category with a market share of around 29.06% share, which indicates that land-based C2 systems are recognized universally as the very basic building block of military, emergency response management systems, critical infrastructure protection, and public safety coordination in all dimensions of an organization. Land-based command systems offer high data throughput, centralized control, and security operations supported by traditional command and control applications, where colocation of physical infrastructure is essential.

To know how our report can help streamline your business, Speak to Analyst

By End User

Emergency Services Modernization and Smart City Integration Accelerate Demand of Segmental Growth

The global market is segmented by end user is further classified into defense, homeland security, public safety, critical infrastructure operators, and enterprise GSOC/NOC.

The public safety sub-segment emerges as the fastest-growing end-user category of C2 systems, recording CAGRs of 10.1% during 2026-2034. This growth is underpinned by the scale of smart city initiatives, further urbanization, and growing threats to security; it is also a factor of investments by governments across metropolitan areas in integrated command and control facilities to support law enforcement, emergency response management systems, and critical infrastructure protection.

- In May 2025, the infrastructure development contract of Chatham County, Georgia was awarded to Reeves Young for comprehensive construction of an emergency operations center near Savannah-Hilton Head International Airport, an important public safety investment reflecting the increased demand for preparedness in case of emergencies and multi-agency coordination in highly critical infrastructures.

The defense sub-segment retains dominant end-user market positioning through commanding about 53.33% in the global system market share, driven by the institutional priority of military organizations for advanced architectures of command modernization that support multi-domain operations, adoption of network-centric warfare technology, and enhanced situational awareness for quick decision-making relative to adversarial forces.

Command and Control System Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

North America Command and Control System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region is projected to be the fastest growing region during the forecast period with a highest CAGR of 9.8% in the global C2 system market. The adoption, driven by strengthening geopolitical tensions in territorial disputes in the South China Sea, continuous border conflicts along the Line of Actual Control, and increasing maritime security concerns that demand advanced C2 infrastructure for coordinated response capabilities.

Dominant regional positioning is maintained by China, with about 33.41% market share, driven by pan-domain military modernization initiatives laying emphasis on network-centric warfare technology, artificial intelligence integration across multi-domain operations platforms, and substantial research investments supporting indigenous C2 system market growth development capabilities. India's accelerated defense transformation through the Make in India initiative has catalyzed domestic manufacturing of military C2 systems , wherein 145 projects under the MAKE framework involving 171 participating industries have been undertaken and have achieved a total defense production value of USD 127.26 million in fiscal year 2023-24.

- For instance, in September 2025, Australia signed a sustainment contract with Kellogg Brown and Root, valued at USD 33.6 million, to upgrade the Air and Space Operations C2 system by bringing all existing sustainment activities together under a single arrangement to simplify governance processes and achieve an accelerated capability delivery against Australian Defense Force air operations planning and execution.

North America

North America continues to dominate the global command and control system market growth, with a share of about 34.27% in 2025. The growth is driven by higher defense-related spending, established acquisition infrastructure, and extensive plans for the adoption of transformative Joint All-Domain Command and Control systems over the coming decade that will work to connect sensors, shooters, and platforms across land, air, sea, space, and cyber into unified network architectures informed by artificial intelligence. The U.S. Department of Defense is focused on the rapid development and fielding of resilient and interoperable military C2 system that can rapidly convert decisions into coordinated action with reduced latency across all domains, such as Northrop Grumman's USD 99.1 million contract in August 2025 for Initial Providence Distributed Battle Management C2 system prototypes in support of Combined JADC2 operational requirements.

- For instance, in September 2025, RTX's Collins Aerospace won a contract for NATO Electronic Warfare Planning and Battle Management, developing Recognized Electromagnetic Pictures by fusing operational data and intelligence systems to improve commanders' visualization of electronic threats throughout alliance structures.

Middle East & Africa

The growth in the Middle East & Africa is much faster, underpinned by higher defense spending that has often been linked to broader-based national transformation projects. Regional interest in interoperability and technology transfer could open up more prospects for collaborative acquisition programs, such as Egypt's USD 625 million program to upgrade its Fast Missile Craft with Lockheed Martin COMBATSS-21 combat management systems and L3Harris electronic warfare architectures.

Department of Defense approved sale of 220 AIM-9X Block II Sidewinder tactical missiles to Saudi Arabia valued at USD 252 million in October 2024, complementing ongoing modernization of Royal Saudi Air Force capabilities supported by technical training programs.

Europe

Europe represents a key growth region, given the underlying modernization initiatives led by NATO, putting focus on interoperability standards, enhancing collective defense capability, and collaborative research programs to further reinforce the land-based operational capabilities of alliance member states. The NATO Communications and Information Agency declared Initial Operating Capability in June 2025 for the project DEMETER when it deployed SitaWare Headquarters across NATO command structures in Izmir, Turkey, and Brunssum, Netherlands, with Final Operating Capability targeted for March 2026 in support of additional installations at Joint Warfare Centre, Joint Force Command Naples, and Joint Force Command Norfolk.

Latin America

Latin America's growth in the C2 system market is moderate, with varied defense priorities, budgetary constraints that restrain large-scale procurement programs, and selective modernization addressing very specific internal security threats, border surveillance requirements, and disaster response operational capabilities.

COMPETATIVE LANDSCAPE

Key Market Players

Market Structure and Consolidation Dynamics Leads to Market Key Players in Industry Concentration and Strategic Positioning within Market

The command and control systems market is at a stage of moderate consolidation, wherein a handful of top competitors holds a large amount of global market share as of 2024. This could mean a fragmented competitive landscape with substantial opportunities for differentiation and market penetration. Significant vertical integration by dominant players characterizes the market, with leading defense primes consolidating sensor development, defense communication systems and infrastructure, software platforms, and integration services within unified corporate structures to ensure interoperability, reduce supply chain risks, and enhance customer lock-in through proprietary architectures.

Mid-tier competitors such as L3Harris Technologies, Boeing, Thales Group, Lockheed Martin, Rheinmetall, and BAE Systems have pursued targeted consolidation strategies through selective acquisitions of specialized software firms, emerging technology startups, and regional suppliers to accelerate technology adoption and geographic market expansion without the requirement for comprehensive transformation of legacy business models.

Further, the competitive landscape reflects sharp evolution toward software-defined command and control architectures, with emerging startups and specialized technology firms disrupting traditional defense contractor dominance through rapid innovation cycles, modular software capabilities, and AI-enabled autonomous decision support systems.

List of Key Command and Control System Companies Profiled

- Lockheed Martin Corporation (U.S.)

- RTX Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- BAE Systems plc (U.K.)

- Thales S.A. (France)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- Elbit Systems Ltd. (Israel)

- Israel Aerospace Industries Ltd. (IAI) (Israel)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Rheinmetall AG (Germany)

- NEC Corporation (Japan)

- Fujitsu Limited (Japan)

- Parsons Corporation (U.S.)

- Mitsubishi Electric Corporation (Japan)

KEY DEVELOPMENTS

- November 2025: TYSONS, Va., a prominent provider of technology-driven government services, has announced that it has received a new Joint Cyber Command & Control (JCC2) Readiness (JCC2-R) contract from the U.S. Air Force Life Cycle Management Center (AFLCMC/HNCJ) Cryptologic and Cyber Systems Division (CCSD) to improve interoperability and provide innovative solutions.

- November 2025: The U.S. Defense and Beijing will create direct communication channels for military interactions. A contract has been established for regional security discussions, and both parties have concurred that maintaining peace, stability, and positive relations is the optimal approach for our two powerful and prominent nations.

- October 2025: Initial releases of the U.S. Army's new command software are impressing artillery units during exercises. The new software, AXS, is a component of the broader Next-Generation Command-and-Control (NGC2) system, which is designed to enhance all battlefield operations for the Army.

- September 2025: The Space Development Agency commenced its first set of operational satellites, initiating a 10-month effort to launch over 150 satellites into low Earth orbit. These satellites are part of the SDA’s Transport Layer, aimed at delivering rapid and secure communication services to military personnel. After conducting initial health and safety assessments of the payload, the satellites could begin offering operational capabilities to combatant commands and other users in about four to six months.

- February 2025: Saab has secured a contract from a NATO member for its air C2 system known as 9AIR C4I. The value of the contract is around 250 MSEK. Deliveries are set to commence in 2025. This order was recorded in the fourth quarter of 2024. Saab's 9AIR enables users to oversee the air and space domains. Its offering includes the 9AIR C4I system, which offers flexibility and scalability for the management of weapons, sensors, and communications in air and space operations.

REPORT COVERAGE

The global command and control system market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the global market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2025 |

|

Growth Rate |

CAGR of 8.1% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Solution · Hardware · Software · Services · Licensing Models By Networks & Connectivity · Tactical RF · Commercial/Private · Backbone · QoS/Latency Classes By Integration Architecture · Standalone · Vehicle-Mounted · Federated · Fully Integrated/Joint All-Domain · Open Architecture By Installation · New Installation · Upgradation By System · Communications & Networks · Weapon Control Systems · Command Posts · Security Systems · Transportation Management Systems · Health & Public Services Systems · Emergency Management System · Others By Technology · Architecture & Hosting · Data & Fusion · AI/Autonomy · Edge & Networking · Interoperability & Links · Others By Platform · Land · Maritime · Air · Space · Cyber/Cloud/Enterprise By End User · Defense · Homeland Security · Public Safety · Critical Infrastructure Operators · Enterprise GSOC/NOC By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 37.26 billion in 2025 and is projected to reach USD 73.33 billion by 2034.

In 2025, the market value stood at USD 10.96 billion

The market is expected to exhibit a CAGR of 8.1% during the forecast period.

The software sub-segment is expected to hold the highest CAGR over the forecast period.

Geopolitical tensions, defense modernization imperatives, integration of advanced technologies and network-centric operations catalyze the market growth.

Lockheed Martin Corporation (U.S.), RTX Corporation (U.S.), Northrop Grumman Corporation (U.S.), L3Harris Technologies, Inc. (U.S.), BAE Systems plc (U.K.), among others are top players in the market.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us