Push-to-Talk (PTT) Market Size, Share & Industry Analysis, By Component (Devices, Software, and Services), By Network Type (Push-to-talk over Cellular, and Land Mobile Radio), By Enterprise Size (SMEs, and Large Enterprises), By Sector (Public Safety & Security, Government & Defense, Transportation & Logistics, Energy & Utility, Travel & Hospitality, and Others (Manufacturing, Construction)) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

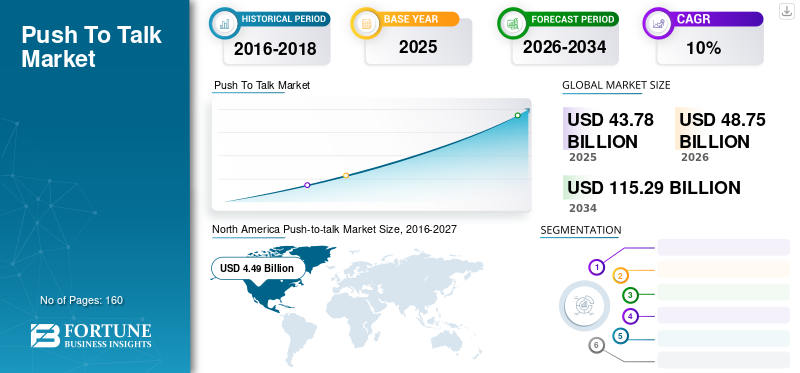

The global push-to-talk market size was valued at USD 43.78 billion in 2025. The market is projected to grow from USD 48.75 billion in 2026 to USD 115.29 billion by 2034, exhibiting a CAGR of 11.36% during the forecast period. North America dominated the push-to-talk market with a market share of 37.42% in 2025. This growth is supported by mission-critical communications modernization, broadband migration, public safety digitization, enterprise mobility needs, and interoperable voice services across regulated and commercial sectors worldwide.

The growth of this push-to-talk market is primarily owing to the rising adoption of cloud-based push-to-talk over Cellular (PoC) solutions among large enterprises. Cloud-based PoC helps to solve the gaps in communications by providing real-time & secured communication, increasing penetration of wireless PTT devices, and multimedia sharing features. Large enterprises are adopting PTT to leverage various benefits such as portable two-way communication, cost control, enhanced call management, and advanced safety & convenience, among others.

Also, technological advancements such as LTE and 5G infrastructure are likely to increase the demand for PTT. According to Fortune Business Insights, the global market value for 5G infrastructure was around USD 720.6 million in 2025 and is expected to reach a market value of USD 50,640.4 million by 2026, exhibiting a CAGR of 76.29%.

The push-to-talk market has evolved from narrowband radio-centric systems into a hybrid ecosystem combining broadband, software platforms, and mission-critical voice services. Adoption now extends beyond traditional public safety into utilities, transportation, manufacturing, and field service operations. Buyers increasingly evaluate solutions based on reliability, latency, coverage continuity, and interoperability across networks. This shift reflects operational digitization priorities rather than discretionary technology upgrades.

Market size expansion remains steady rather than speculative, supported by recurring service contracts, device refresh cycles, and workforce mobility requirements. Push-to-talk over cellular solutions gain share as enterprises leverage commercial networks, while land mobile radio retains relevance for resilience and guaranteed availability. Procurement decisions increasingly involve long-term total cost of ownership, security certification, and regulatory compliance considerations.

Public safety and government agencies continue to anchor demand, but private-sector adoption accelerates as operational teams require instant group communication without infrastructure ownership. Software-centric platforms enable features such as location awareness, dispatch integration, and cross-agency collaboration. These capabilities expand use cases while maintaining the simplicity central to push-to-talk workflows.

Regionally, North America and Europe represent mature markets with disciplined upgrade cycles, while Asia-Pacific shows stronger growth driven by urbanization and enterprise mobility. Competitive dynamics remain fragmented, with established radio vendors, network operators, and software specialists coexisting. Buyers prioritize vendor stability, ecosystem partnerships, and standards alignment. Overall, the push-to-talk industry demonstrates durable fundamentals supported by mission-critical dependence, incremental modernization, and expanding commercial relevance.

Looking ahead, investment decisions emphasize interoperability, cybersecurity hardening, and service continuity during network congestion or emergencies. These evaluation criteria reinforce conservative purchasing behavior. As a result, growth trajectories remain predictable, favoring suppliers with proven deployments, regulatory familiarity, and long-term support capabilities. Such characteristics align closely with institutional procurement frameworks and risk-managed communications strategies globally, across public safety and enterprise environments, under regulated operating conditions, with defined accountability requirements worldwide adoption.

Also, evolving technologies such as Internet of Things (IoT), Artificial Intelligence (AI), natural language processing, and growing online applications are expected to create enormous opportunities for market players during the forecast period. Further, key players in the market are adopting various marketing strategies, such as mergers & acquisitions, to expand their business worldwide. For instance, in March 2019, Motorola Solutions acquired Avtec, Inc., a U.S.-based VoIP dispatch Communications Company. The acquisition was completed to expand Avtec’s public safety services and software portfolio by using an end-to-end PTT platform for its customers.

Download Free sample to learn more about this report.

Push To Talk MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 43.78 billion

- 2026 Market Size: USD 48.75 billion

- 2034 Forecast Market Size: USD 115.29 billion

- CAGR: 11.36% from 2026–2034

- North America dominated the push-to-talk market with a 37.42% share in 2025.

- The Public Safety & Security segment is expected to hold a 21.2% share in 2025.

- Land Mobile Radio (LMR) segment maintained a strong position in network type.

North American

North America led the market with 37.42% share in 2025, driven by public safety modernization and enterprise mobility demand.

Europe

Europe shows steady adoption supported by regulatory standards and strong public sector communication needs.

Asia Pacific

Asia Pacific is the fastest-growing region due to rapid 5G expansion and rising industrial digitization.

U.S.

Strong demand from public safety, defense, and enterprise communication systems supports market leadership.

Japan

Growth is driven by disaster-resilient communication systems and advanced enterprise adoption.

Read More

PUSH-TO-TALK MARKET TRENDS

Growing Deployment of Long-Term Evolution (LTE) Network-based PTT Solutions to Outgrow LMR Solutions

One of the emerging trends for the push-to-talk market is the shifting focus of enterprises towards the deployment of PTT solutions enabled by advanced LTE networks. The advent of LTE networks in mobile communication has substituted land-mobile-radio (LMR) communication technology. Various organizations are adopting LTE networks to enable enriched communication. This adoption has initiated the development of a large bandwidth architecture that supports mission-critical PTT, push-to-locate, push-to-message, and push-to-alert communication services.

The push-to-talk industry reflects several notable trends indicating gradual modernization rather than disruption. Hybrid deployments combining land mobile radio and push-to-talk over cellular gain traction. Organizations favor phased transitions that preserve mission-critical reliability while introducing broadband capabilities.

Software-defined platforms increasingly dominate innovation. Dispatch integration, location tracking, and application programming interfaces enable deeper operational integration. These capabilities extend push-to-talk beyond voice into coordinated workflow management.

Device convergence represents another trend. Rugged smartphones and multi-mode radios support both cellular and radio communications, reducing equipment fragmentation. This convergence simplifies fleet management and user training. Security enhancements receive growing attention. Vendors prioritize end-to-end encryption, secure identity management, and compliance with public sector security frameworks. These features influence vendor selection more than consumer-style functionality.

Commercial sectors adopt push-to-talk for safety and efficiency rather than regulatory necessity. This trend expands addressable markets without diluting mission-critical positioning. Overall, market trends favor incremental capability enhancement, interoperability, and operational resilience over rapid platform replacement.

Download Free sample to learn more about this report.

Push-To-Talk Market Growth Factors

Rising Adoption of Wireless Devices, Network Devices, and Software among Organizations to Aid Market Growth

One of the significant push-to-talk market drivers is the rising demand for wireless push-to-talk devices across various industries, such as enterprises & commercial, and aerospace & defense. Rising adoption of wireless devices helps boost overall safety and productivity as it provides end-to-end encryption. Also, the push-to-talk market demand for PTT software among smartphone users to connect groups and members over these communication mediums has significantly boosted the push-to-talk market growth.

Demand for push-to-talk solutions is driven by the critical need for instantaneous, reliable group communication in operationally intensive environments. Public safety agencies rely on push-to-talk to coordinate emergency response, disaster recovery, and daily patrol operations, where latency or network failure carries material risk. These requirements continue to sustain investment in both broadband-enabled and land mobile radio systems.

Enterprise adoption expands as organizations deploy mobile workforces across logistics, utilities, transportation, and construction. Push-to-talk supports operational efficiency by reducing call setup time, simplifying workflows, and enabling one-to-many communication without manual dialing. This efficiency directly affects productivity, making push-to-talk a functional necessity rather than an optional tool.

Network modernization also drives growth. Migration toward Long Term Evolution and fifth-generation networks enables push-to-talk over cellular solutions with enhanced coverage and feature sets. Enterprises benefit from leveraging existing commercial infrastructure instead of owning private radio networks.

Regulatory mandates reinforce demand. Many sectors require resilient communication systems with defined availability and security standards. Push-to-talk platforms aligned with these requirements remain embedded in procurement frameworks. Collectively, these drivers create structurally stable demand, anchored in mission-critical dependency, operational mobility, and regulatory compliance rather than cyclical technology adoption patterns.

RESTRAINING FACTORS

Presence of Latency and Gaps in Communication Proving to be an Inhibiting Factor for Market Growth

The presence of latency and minor communication gaps while engaging in two-way communication is restraining the demand for PTT. The users engaging in the conversation using LMR technology may face some time delays. For example, in areas where network infrastructure is absent or weak, users may experience delays or lags during communications.

Further, PTT technology implementation has affected network costs and pricing for users, which is on the higher side. These factors act as major restraints for the growth of the push-to-talk market. Besides, the lack of proper network infrastructure and the lack of awareness about PTT solutions are major hindrances to the growth of the market. However, with the advent of advanced networking technologies such as LTE and G, the latency and gaps in communication are expected to be minimized.

Despite strong fundamentals, the push-to-talk market faces practical constraints that moderate adoption rates. Network dependency represents a key concern, particularly for push-to-talk over cellular solutions. Performance varies based on coverage quality, congestion levels, and service prioritization, which can be problematic during large-scale incidents or remote operations.

Interoperability challenges persist across legacy land mobile radio systems and newer broadband platforms. Integrating mixed environments increases deployment complexity and cost, especially for agencies managing multi-vendor infrastructures. These challenges can delay purchasing decisions or extend transition timelines.

Cost considerations also affect adoption. While push-to-talk over cellular reduces infrastructure ownership, recurring service fees and device refresh requirements accumulate over time. Budget-constrained public agencies and small enterprises often require extended justification cycles.

Cybersecurity risks present another restraint. As push-to-talk platforms adopt software-centric architectures, exposure to cyber threats increases. Buyers demand robust encryption, authentication, and compliance assurance, which raises development and certification costs for vendors.

Organizational resistance to change slows modernization. Users accustomed to traditional radios may hesitate to adopt smartphone-based solutions, requiring training and cultural adjustment. These restraints shape cautious procurement behavior rather than preventing market growth.

Market Opportunities

Several opportunities support medium-term expansion within the push-to-talk market. Public safety broadband initiatives create demand for interoperable push-to-talk platforms capable of operating across agencies and jurisdictions. Vendors offering standards-aligned solutions benefit from these programs.

Private-sector digitization presents another opportunity. Utilities, transportation, and logistics operators increasingly prioritize workforce coordination and situational awareness. Push-to-talk platforms integrated with asset tracking and operational software align well with these needs.

Emerging markets offer incremental growth. Urbanization and infrastructure development increase demand for reliable field communications. Push-to-talk over cellular solutions provide cost-effective entry points where radio infrastructure is limited.

Technology partnerships also create opportunities. Collaboration between network operators, software providers, and device manufacturers accelerates deployment and expands feature sets. These ecosystems reduce integration risk for buyers.

Managed services represent an underdeveloped segment. Organizations increasingly outsource communication system management to reduce operational burden. Vendors offering end-to-end services, including provisioning, monitoring, and support, can strengthen recurring revenue and customer retention.

Push-To-Talk Market Segmentation Analysis

By Component Analysis

Devices Segment to Hold High Market Share

Based on component, the push-to-talk market is divided into devices, software, and services.

The devices segment is expected to hold the largest market share during the forecast period. The presence of key market players such as AT&T Intellectual Property, Bell Canada, ESChat, and Azetti Networks, among others, is significantly contributing to the growth of this segment. Also, the rising adoption of rugged push-to-talk devices with inventive technologies is anticipated to supplement the market growth.

Devices form the foundational layer of the push-to-talk market. This category includes rugged handheld radios, dedicated push-to-talk terminals, and hardened smartphones designed for mission-critical environments. Device procurement decisions emphasize durability, battery life, audio clarity, and environmental resistance. In public safety and industrial sectors, devices must withstand extreme temperatures, vibration, and moisture exposure. While device replacement cycles are relatively long, periodic refresh driven by technology upgrades and network transitions sustains steady demand. Device interoperability across radio and cellular networks increasingly influences purchasing decisions.

Software represents the fastest-evolving component within the push-to-talk industry. Push-to-talk software platforms enable voice session management, user authentication, group configuration, and dispatch functionality. Enterprises and agencies value software flexibility, particularly the ability to integrate with command-and-control systems, geographic information systems, and workforce management platforms. Software-based push-to-talk allows over-the-air updates, feature scalability, and cross-device compatibility. As organizations prioritize operational intelligence, software becomes a key differentiator rather than a supporting element.

Services complete the component landscape and account for a growing share of market value. These include system integration, network provisioning, training, maintenance, and managed services. Public safety agencies and large enterprises increasingly outsource lifecycle management to reduce internal complexity. Services also support hybrid environments, ensuring seamless operation between land mobile radio and cellular platforms. As systems become more software-driven, demand for specialized support and cybersecurity services continues to rise.

By Network Type Analysis

Push-to-Talk over Cellular (PoC) Segment to Gain Traction

The network type segment is categorized into PoC and land mobile radio (LMR). The land mobile radio segment is likely to hold a high push-to-talk market share, owing to the growing focus on improving communication technologies among public safety organizations and law enforcement agencies. To cater to the rising customer needs, leading players are focusing on developing customized applications and solutions. LMR systems are mainly used in law enforcement, defense, and public safety, among others. Rising demand for LMR systems in emerging economies in regions such as Latin America, the Middle East, and Africa (LAMEA) and Asia-Pacific, coupled with increased safety measures during terrorist activities and natural disasters, is expected to supplement the push-to-talk market growth.

Push-to-talk over cellular solutions have gained significant traction as enterprises leverage commercial broadband networks. These solutions utilize Long Term Evolution and fifth-generation networks to deliver wide-area coverage without dedicated infrastructure ownership. Enterprises benefit from scalability, lower upfront costs, and rapid deployment. Push-to-talk over cellular platforms also supports advanced features such as multimedia sharing, location services, and cloud-based dispatch. However, performance depends on network availability and prioritization, which remains a consideration for mission-critical users.

Land mobile radio remains indispensable for sectors requiring guaranteed availability, direct mode operation, and independence from commercial networks. Public safety agencies, defense organizations, and critical infrastructure operators rely on land mobile radio for resilience during disasters and network outages. While capital-intensive, land mobile radio offers deterministic performance and regulatory protection. Modernization efforts focus on digital radio standards, spectrum efficiency, and integration with broadband systems rather than outright replacement.

Hybrid network models represent an increasingly common approach. Organizations deploy push-to-talk over cellular for routine operations while retaining land mobile radio for fallback and high-risk scenarios. This hybrid strategy balances cost efficiency with reliability. Vendors supporting seamless handoff and unified user management across networks gain a competitive advantage. As network technologies evolve, coexistence rather than displacement defines market structure.

By Enterprise Size Analysis

Implementation of Cost-Effective PoC Solutions to Maximize Productivity to Boost Adoption of PTT in SMEs

Based on enterprise size, the market is segmented into small & medium-sized enterprises (SMEs) and large enterprises. Reduced cost and maximum productivity are vital factors for the adoption across small & medium-sized organizations as they have low budgets and spending. Thus, these organizations implement cost-effective PoC solutions that eliminate the cost associated with setting up a wide communication infrastructure. Moreover, PoC solutions help the field workers by providing secure and real-time communication across multiple geographies and enabling workers to share field-related videos or images that can be crucial for business outcomes.

Large enterprises constitute the dominant share of push-to-talk market revenue. These organizations operate dispersed workforces and complex operational environments that require reliable group communication. Large enterprises often deploy customized solutions integrated with enterprise resource planning, asset management, and safety systems. Procurement cycles are lengthy, emphasizing total cost of ownership, vendor stability, and long-term support commitments. Once deployed, systems exhibit high switching costs, contributing to vendor retention.

Small and medium enterprises represent a growing adoption segment, particularly for push-to-talk over cellular solutions. These organizations value simplicity, predictable pricing, and minimal infrastructure requirements. Cloud-based platforms and subscription models lower entry barriers. While smaller deployments generate lower per-customer revenue, volume growth contributes meaningfully to overall market expansion. Vendors offering scalable packages and simplified onboarding are well-positioned within this segment.

By Sector Analysis

To know how our report can help streamline your business, Speak to Analyst

Public Safety & Security Sector to Witness the Highest Adoption of PTT Devices

Based on sector, the push-to-talk market scope includes public safety & security, government & defense, transportation & logistics, energy & utility, travel & hospitality, and others. Among these, the public safety & security segment held the largest market share in 2025.

The growing adoption of these devices, such as specialized ultra-rugged devices, feature phones, and smartphones in the public safety & security domain, is expected to drive the market. Several public safety companies across the globe, such as Phoenix Health and Safety, Honeywell, and 3M, are utilizing push-to-talk solutions owing to their innovative benefits and features. Moreover, public authorities are communicating using these devices, such as walkie-talkies, during emergencies. The Public Safety & Security segment is expected to hold a 21.2% share in 2025.

The government & defense sector is progressively implementing PTT amid growing concerns for border safety, and the evolvement of advance monitoring systems. Government and defense applications emphasize secure, resilient communication across civilian and military operations.

Push-to-talk supports command coordination, facility security, and logistics. Defense organizations often integrate push-to-talk with broader tactical communication systems. Security certification and domestic sourcing considerations influence vendor selection. Further, transportation & logistics, energy & utility, travel & hospitality segments are expected to significantly grow during the forecast period.

The primary factors responsible for the growth of these segments are the need for cost-effective services, the adoption of cloud-based PTT solutions, and government initiatives. Also, improved compliance, such as DOT compliance, and rising investment and R&D activities conducted to upgrade push-to-talk solutions are expected to drive the market growth. The need for reliable and constant communication between dispatchers, field workers, among others, is surging the demand.

Key players in the market, including Motorola Solutions, Azetti Networks, RugGear, and Airbus DS Communications, among others, are focusing on providing services across these sectors. For instance, in 2019, Azetti Networks was focused on implementing PoC technology based on cloud services for the transportation & logistics and travel & hospitality industries.

REGIONAL INSIGHTS

North America Push-to-talk Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America Push-to-talk Market Analysis

North America is expected to lead the market share during the forecast period, which is attributable to the rising penetration of core technologies and the presence of telecom service providers and PoC vendors such as Motorola Solutions and AT&T. Rising demand for efficient and cost-effective solutions is considered one of the key push-to-talk market drivers in the region.

North America represents a mature push-to-talk market supported by public safety modernization and enterprise mobility adoption. Hybrid network deployments are common. Regulatory oversight and funding programs sustain investment. Vendors compete on interoperability, security, and long-term support rather than pricing.

The United States leads regional demand, driven by public safety agencies and large enterprises. Push-to-talk over cellular adoption grows alongside land mobile radio modernization. Procurement emphasizes standards compliance, cybersecurity, and vendor reliability. Growth remains steady and predictable.

The US holds the majority share of the North America market owing to the rising adoption of push-to-talk solutions among various end-use industries such as public safety organizations, government and defense, healthcare, and others. Thus, key players in this market are focused on adopting product expansion strategies to cater to the rising demands for efficient and cost-effective solutions.

Asia-Pacific Push-to-talk Market Analysis

Asia-Pacific exhibits strong growth driven by urbanization and enterprise mobility. Push-to-talk over cellular adoption accelerates as infrastructure expands. Public safety modernization programs support long-term demand. Japan emphasizes reliability and disaster preparedness. Push-to-talk supports public safety, transportation, and utilities. Integration with broadband networks progresses cautiously, maintaining resilience as a priority. China’s market expands through industrial, logistics, and municipal deployments. Domestic vendors play a significant role. Cellular-based solutions dominate due to scale and infrastructure availability.

The market in the Asia-Pacific is anticipated to grow at the highest CAGR during the forecasted period. This growth is attributed to the advancement in IT infrastructure and rising collaboration between distributors and key players. China and India are the fastest-growing economies of Asia, which are continuously investing in arming public safety institutions, such as the police and the military, with these devices. Key players are focused on launching new products to gain a competitive edge in the market. For instance, in November 2018, Kyocera Corporation, a Japan-based electronics manufacturer and supplier, launched military-grade, ultra-rugged, waterproof "DuraForce PRO 2", a 4G LTE Android smartphone with Verizon Wireless. This device is designed for various industries such as construction and transportation. As a result, market growth in the region is proliferating.

Europe Push-to-talk Market Analysis

Europe shows disciplined adoption shaped by regulatory harmonization and public safety coordination. Cross-border interoperability and spectrum efficiency influence deployment decisions. Enterprises increasingly adopt cellular-based solutions for logistics and utilities.

Germany emphasizes industrial and public safety applications. Manufacturing, utilities, and transportation drive enterprise demand. High quality and security standards guide vendor selection. Hybrid communication architectures dominate deployments. The United Kingdom market balances public safety modernization with commercial adoption. Emergency services prioritize interoperability, while enterprises deploy push-to-talk for logistics and facility management. Managed services gain traction.

Europe held a significant position in the market in 2025, owing to the presence of major players operating in this market, such as International Ltd., IPTT, and Azetti Networks. These key players are focusing on adopting strategies such as new product launches to expand their business and related offerings. For instance, in June 2019, International Push to Talk, a UK-based telecommunications equipment supplier, launched the “iPTT P500” hand portable PTT-over-cellular (PoC) radio designed for various sectors such as hospitality, traffic management, construction, public safety, and transportation.

Push-to-talk Middle East & Africa and Latin America Market Analysis

The Middle East & Africa and Latin America are expected to grow moderately during the forecast period. This growth is owing to the growing trend of wireless technology and the advent of technological advancements in cloud, IoT, and AI across these regions. The push to talk platforms have huge opportunities in Brazil and Mexico owing to rising internet penetration. Further, the natural disasters, cross-border terrorism, and rising criminal activities are some of the key factors driving the need for public safety, which is increasing the demand for these services in the region.

Latin America represents an emerging market with growing enterprise adoption. Public safety and utilities drive demand. Cost sensitivity favors cellular-based solutions with subscription pricing. The Middle East & Africa market develops gradually. Oil and gas, security, and transportation sectors drive adoption. Investment focuses on reliability and ruggedization.

Key players in these regions are focusing on offering new services to strengthen their market position. For instance, in July 2019, Motorola Solutions launched WAVE Radio: the TLK 100, a cloud-based network-independent multimedia communication subscription service across Europe, the Middle East, and Africa regions (EMEA). This launch has accelerated the adoption of cloud-based services across the EMEA region.

Competitive Landscape

Leading Market Players Are Emphasizing Expanding Product Portfolio to Strengthen Market Position

AT&T Intellectual Property is a US-based communications holding company. The company provides media, technology, and telecommunications services worldwide and functions through four segments: the WarnerMedia segment, the Xandr segment, the communication segment, and the Latin America segment. The communications segment offers wireline and wireless video, broadband, and telecom services to its customers.

The push-to-talk market remains fragmented, with established radio manufacturers, network operators, and software specialists competing across segments. No single vendor dominates globally, reflecting diverse regulatory environments and use cases. Competitive positioning depends on reliability, interoperability, and lifecycle support.

Traditional land mobile radio vendors maintain strong positions in public safety and defense markets. These companies leverage long-standing relationships, certified equipment, and proven resilience. They increasingly expand into broadband-enabled solutions to protect installed bases.

Network operators play a critical role in push-to-talk over cellular deployments. By bundling communication services with connectivity, operators offer integrated solutions to enterprises. Partnerships with software providers enhance feature depth and scalability. Software-centric vendors focus on application-layer innovation. These firms differentiate through cloud-based dispatch, analytics, and integration capabilities. Agility allows rapid feature development, appealing to enterprise customers.

Niche players address specialized sectors such as construction, hospitality, or logistics. These vendors emphasize ease of use and sector-specific workflows. While smaller in scale, they capture targeted demand.

Strategic partnerships shape the competitive landscape. Device manufacturers collaborate with software developers and network operators to deliver end-to-end solutions. These ecosystems reduce integration risk and strengthen customer retention. Overall, competition favors vendors with proven deployments, regulatory familiarity, and long-term commitment to mission-critical communications.

The business units of the communication segment include the entertainment group, business wireline, and mobility. In the mobility business unit, AT&T’s Enhanced EPTT service provides highly secure messaging, virtually instant voice communications, and location features over 3G, 4G, 4G LTE, & Wi-Fi. It also provides fast call setup times, and it is based on 3GPP Mission Critical standards. This service uses VoIP technology to send the conversation over an AT&T Wi-Fi network. The company is currently investing in the development of its services all across the globe. AT&T Intellectual Property is one of the key players in this push-to-talk market.

Push-to-talk Industry Key Developments

- February 2024: Motorola Solutions expanded its broadband push-to-talk portfolio to enhance interoperability between land mobile radio and cellular networks, supporting public safety transition strategies.

- May 2024: Ericsson partnered with enterprise software providers to strengthen push-to-talk over cellular capabilities, focusing on low-latency voice services across private and public networks.

- September 2024: Nokia introduced enhanced mission-critical push-to-talk features within its private wireless offerings, targeting utilities and transportation operators requiring secure group communication.

- January 2025: AT&T expanded its push-to-talk service integration for enterprise customers, improving priority access and network resilience for critical operations.

- April 2025: Hytera launched multi-mode push-to-talk devices supporting both digital radio and cellular connectivity, enabling hybrid deployments across industrial and public safety sectors.

List of Top Push-To-Talk Companies:

- Motorola Solutions Inc. (US)

- Zebra Technologies Corporation (US)

- AT&T Intellectual Property (US)

- Verizon Wireless (US)

- Qualcomm Technologies, Inc. (US)

- Harris Corporation (US)

- ICOM Inc. (Japan)

- Kyocera

- Siyata Mobile (Canada)

- ECOM Instruments GmbH (US)

- RugGear (US)

- Telefonaktiebolaget LM Ericsson (Sweden)

- Sonim Technologies (US)

- Simoco (India)

- Airbus DS Communications (US)

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The push-to-talk market report offers qualitative and quantitative insights on the industry and a detailed analysis of market size & growth rate for all possible segments in the market. The market is quantitatively analyzed from 2020 to 2027 to provide financial competency. The information gathered in the report has been taken from several primary and secondary sources.

Along with this, the report provides an elaborative study of market dynamics, emerging trends, opportunities, and competitive landscape. Key insights offered in the report are the adoption trends of this market, recent industry developments such as partnerships, mergers & acquisitions, consolidated SWOT analysis of key players, business strategies of leading market players, macro and micro-economic indicators, and key industry trend analysis.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021 – 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 – 2034 |

|

Historical Period |

2021 – 2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Component

|

|

By Network Type

|

|

|

By Enterprise Size

|

|

|

By Sector

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global push-to-talk market size was valued at USD 43.78 billion in 2025 and is projected to grow to USD 115.29 billion by 2034, exhibiting a robust CAGR of 11.36% during the forecast period.

The market growth is primarily driven by the increasing adoption of cloud-based push-to-talk over cellular (PoC) solutions, expansion of 5G & LTE infrastructure, and rising demand for real-time communication across industries such as public safety, defense, and logistics.

The market is expected to grow at a CAGR of 11.36% in the forecast period (2026-2034).

North America dominated the push-to-talk market with a market share of 37.42% in 2025, attributed to early adoption of advanced PTT technologies, strong public safety infrastructure, and the presence of key players like Motorola Solutions, AT&T, and Verizon.

The Asia Pacific region is expected to grow at the highest CAGR, driven by expanding 5G infrastructure, increased industrial digitization, and rising investments in mission-critical communication across China, India, and Japan.

Major companies in the push-to-talk market include Motorola Solutions Inc., AT&T Intellectual Property, Verizon Wireless, Qualcomm Technologies, Zebra Technologies, Ericsson, Kyocera, Sonim Technologies, Siyata Mobile, and Airbus DS Communications.

The rollout of 5G infrastructure is significantly boosting the PTT market, enabling ultra-low latency, high-speed communication essential for mission-critical operations, autonomous systems, and smart city applications.

Push-to-talk solutions are widely used in public safety & security, government & defense, transportation & logistics, energy & utilities, travel & hospitality, and construction, with public safety & security being the largest segment.

Key trends include the shift from LMR to LTE & 5G-based PTT, growing adoption of cloud-based PoC, integration with AI and IoT, deployment of rugged & wearable PTT devices, and increasing strategic mergers & acquisitions.

The market faces challenges such as latency and communication gaps in low network areas, high implementation costs, and lack of robust network infrastructure in developing regions, although advancements in LTE and 5G are helping to mitigate these issues.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us