Autonomous Truck Market Size, Share & Industry Analysis, By Level of Autonomy (Level 1, Level 2, Level 3, and Level 4), By Propulsion Type (IC Engine and Electric), By Truck Type (Light-Duty Trucks, Medium-Duty Trucks, and Heavy-Duty Trucks), By Industry (Manufacturing, Construction & Mining, FMCG, Military, and Others), and Regional Forecasts, 2026-2034

(Offer valid till 15th Aug 2026)

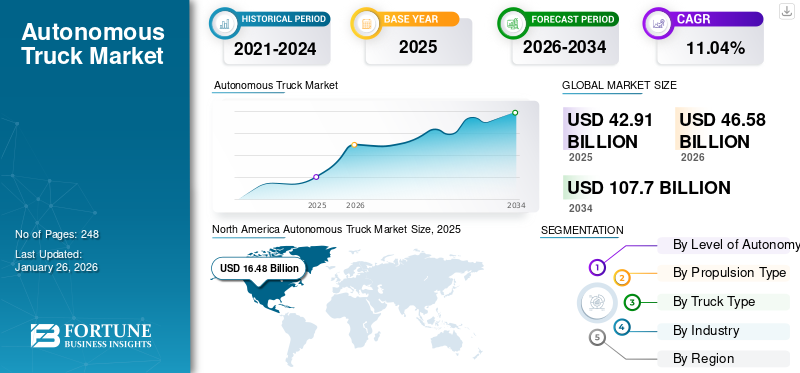

Autonomous Truck Market Size and Future Outlook

The global autonomous truck market size was valued at USD 42.91 billion in 2025 and is projected to grow from USD 46.58 billion in 2026 to USD 107.7 billion by 2034, exhibiting a CAGR of 11.04% during the forecast period. North America dominated the global market with a share of 38.4% in 2025.

Autonomous trucks, also known as self-driving trucks, are commercial vehicles that utilize advanced technologies such as AI, sensors, and GPS to operate without human intervention. These trucks employ a combination of cameras, radar, LiDAR, and ultrasonic sensors to navigate and respond to their environment. They aim to enhance safety, efficiency, and productivity in logistics by automating tasks such as long-haul deliveries and yard operations. They can operate at various levels of autonomy, from partial assistance to full automation, depending on the technology and regulatory framework.

The global autonomous truck market growth is witnessing significant advancements driven by technological innovations and industry pressures such as driver shortages and rising delivery demands. These trucks leverage artificial intelligence (AI) and high-performance computing to improve safety and efficiency in logistics. Key players are investing heavily in research and development to scale autonomous solutions, focusing on long-haul operations where autonomous vehicles can offer substantial benefits.

The market involves collaborations between technology developers, truck manufacturers, and logistics providers to overcome technical challenges and operational considerations. They are poised to transform the logistics sector by enhancing operational efficiency and reducing costs. Major players in the market include Waymo, Aurora Innovation, TuSimple, Embark Trucks, Kodiak Robotics, Daimler Trucks, and Volvo Autonomous Solutions. These companies are leading the industry with advanced AI-driven platforms, extensive real-world testing, and strategic partnerships with logistics and truck manufacturing giants. Their innovations focus on safety, scalability, and efficiency, positioning them at the forefront of the autonomous freight transport revolution.

The COVID-19 pandemic accelerated interest in such trucks as it highlighted the need for efficient and reliable logistics systems. During the pandemic, autonomous vehicles were observed as a potential solution to address labor shortages and maintain supply chain continuity. For instance, companies such as TuSimple and PlusAI continued their autonomous truck testing and deployment efforts, demonstrating the resilience of autonomous technology in challenging conditions. This momentum has continued post-pandemic, with ongoing investments in autonomous truck technology to meet the growing demand for efficient logistics solutions.

Download Free sample to learn more about this report.

AUTONOMOUS TRUCK MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 42.91 Billion

- 2026 Market Size: USD 46.58 Billion

- 2034 Forecast Market Size: USD 107.70 Billion

- CAGR: 11.04% from 2026–2034

- North America dominated the global autonomous truck market with a 38.40% share in 2025.

- The Level 1 segment is projected to account for the largest 87.99% market share in 2026.

- The IC engine segment is expected to hold a dominant 93.34% market share in 2026.

North America

North America accounted for 38.40% of the global market in 2025, reaching USD 16.48 billion, and is projected to grow to USD 17.57 billion in 2026.

Europe

Europe represented 34.52% of the global market in 2025, generating USD 14.81 billion, and is expected to reach USD 15.42 billion in 2026.

Asia Pacific

Asia Pacific captured 26.26% of the global market in 2025, reaching USD 11.27 billion, and is projected to grow to USD 13.19 billion in 2026.

U.S.

The market is projected to reach USD 16.68 billion by 2026, driven by rapid advancements in AI, autonomous driving technologies, and logistics automation.

Japan

The market is projected to reach USD 12.40 billion by 2026, supported by increasing investments in autonomous vehicle technologies and smart transportation initiatives.

Read More

Autonomous Truck Market Trends

Rapid Technological Advancements and Strategic Partnerships Among OEMs, Technology Firms, and Logistics Companies are Market Trending

These collaborations aim to accelerate the development and deployment of autonomous trucking solutions, enhancing operational efficiency and addressing challenges such as labor shortages and safety concerns. In January 2025, Aurora Innovation announced a pivotal partnership with Nvidia and Continental to advance self-driving truck technology. This collaboration involves integrating Nvidia's DRIVE Thor computing platform and DriveOS automotive operating system into Aurora's self-driving system. Continental is slated to commence mass production of this integrated system by 2027, facilitating widespread deployment of autonomous trucks. Aurora, which already collaborates with truck manufacturers such as PACCAR and Volvo, plans to launch its driverless trucking service in Texas by April 2025.

- In February 2025, Waabi, a self-driving technology company, partnered with Volvo's driverless systems unit to develop autonomous big rigs. This collaboration involves integrating Waabi's virtual driver system, which combines sensors and computing hardware, into Volvo VNL Autonomous trucks produced at Volvo's factory in Dublin, Virginia. Waabi plans to launch commercial pilots in Texas within four years through a partnership with Uber Freight. This initiative aims to address driver shortages and reduced operational costs by extending the operational hours of trucks.

Similarly, in January 2025, Aurora Innovation announced a partnership with Nvidia and Continental to deploy driverless trucks at scale. The collaboration plans to integrate Nvidia's Drive Thor system-on-a-chip into Aurora's SAE Level 4 autonomous driving systems, with mass production by Continental expected to begin in 2027. Prototype testing is set to commence in the coming months, aiming to enhance the safety and efficiency of autonomous trucking operations.

The ongoing global megatrend of automotive electrification is also influencing market growth. Increasing demand for emission-free commercial vehicles with advanced safety and driver assistant features for efficient trucking, logistics, and supply chain operations across major industries is anticipated to boost market growth. Major economies, such as China, the European Union, and the U.S., are enforcing stringent regulations for automotive emission control. For instance, in November 2022, the European Union introduced a new emission standard called Euro VII. As per the new standard, by 2035, the Nitric Oxide (NOx) emission from cars and vans is predicted to be reduced by 35% and buses & Lorries by 56% compared to Euro VI.

Therefore, surging new-generation electric truck sales with a significant level of autonomy are anticipated to boost the market growth in the years to come. Moreover, fleet managers' focus on deploying an emission-free autonomous fleet of trucks to reduce operation costs and improve efficiency is also anticipated to accelerate the demand for self-driving trucks in the coming years.

Download Free sample to learn more about this report.

Market Drivers

Pursuit of Enhanced Fuel Efficiency and Resultant Cost Savings is Driving Market Growth

Autonomous trucking technology offers the potential to optimize driving behaviors, reduce fuel consumption, and lower operational expenses, making it an attractive solution for logistics and transportation companies worldwide. Autonomous trucks are equipped with advanced sensors, artificial intelligence, and machine learning algorithms that enable precise control over acceleration, braking, and speed. This precision leads to smoother driving patterns, minimizing unnecessary fuel consumption.

A study conducted by the University of California San Diego's Jacobs School of Engineering in collaboration with TuSimple, an autonomous trucking company, revealed that self-driving trucks can reduce fuel consumption by at least 10% compared to traditional manually operated trucks. The study highlighted that the most significant fuel-efficiency gains occurred at lower speeds, where complex driving conditions benefit more from autonomous control systems.

These findings underscore the potential for these trucks to deliver substantial fuel savings, particularly in urban environments with frequent stop-and-go traffic. By maintaining optimal speeds and reducing aggressive driving behaviors, such trucks can achieve better fuel economy, directly impacting the bottom line for fleet operators.

The reduction in fuel consumption translates to cost savings and contributes to a decrease in greenhouse gas emissions. TuSimple's study estimated that if all medium- and heavy-duty trucks in the U.S. adopted their autonomous technology, it could result in a savings of approximately 4 billion gallons of fuel annually, equating to USD 10 billion in cost reductions. Moreover, this shift could lead to a reduction of 42 million metric tons of CO₂ emissions per year, significantly mitigating the environmental impact of the trucking industry.

In addition to fuel savings, autonomous trucks can lower maintenance costs. The precise and controlled driving patterns reduce wear and tear on vehicle components, extending their lifespan and decreasing the frequency of repairs. Predictive maintenance systems, integrated into autonomous vehicles, can monitor the health of various components in real time, allowing for timely interventions before minor issues due to human error escalate into major problems. This proactive approach to maintenance enhances vehicle reliability and reduces downtime, further contributing to operational efficiency.

MARKET RESTRAINTS

Regulatory Environment for Autonomous Trucks is Critical Factor Influencing Industry's Trajectory

Regulatory challenges stem from safety concerns, potential job displacement, and national security issues, creating a multifaceted barrier to the widespread adoption of autonomous trucking technology. In the U.S., individual states have taken varied approaches to regulating autonomous trucks, often reflecting local priorities and concerns. California, a pivotal state for technological innovation, has been at the forefront of this regulatory discourse.

For instance, in September 2023, the California State Senate passed Assembly Bill 316, mandating that a trained human safety operator be present in self-driving, heavy-duty vehicles operating on public roads. This legislation effectively prohibits driverless autonomous trucks, underscoring the state's cautious stance on removing human oversight from heavy-duty vehicle operations. Proponents of the bill, including labor unions such as the Teamsters, argue that such measures are essential to ensure public safety and protect jobs. Conversely, industry stakeholders contend that these government regulations could stifle innovation and delay the deployment of potentially safer autonomous technologies.

In response to these legislative developments, the California Department of Motor Vehicles (DMV) issued draft regulations in August 2024, outlining a framework for the operation of such trucks on highways. These proposed rules initially require the presence of safety drivers for both light- and heavy-duty autonomous vehicle operations. The DMV's approach aims to balance innovation with safety, allowing for the gradual integration of such trucks into the state's transportation infrastructure while addressing public and legislative concerns.

Market Opportunities

Transformation of Long-Haul Logistics Through Hub-To-Hub Autonomous Operations Creates Growth Opportunities

This model, where self-driving trucks handle highway routes between logistics hubs and human drivers manage first- and last-mile delivery is rapidly gaining traction. Hub-to-hub operations enable incremental adoption, leveraging geofenced, controlled environments to maximize safety and operational efficiency. Companies such as Kodiak Robotics, Aurora Innovation, and Gatik are already piloting or deploying autonomous trucks on these routes in the U.S., while China’s Inceptio Technology recently delivered 400 autonomous heavy trucks to ZTO Express, highlighting large-scale commercial adoption.

This shift addresses persistent challenges, such as driver shortages and rising labor costs, while optimizing fleet utilization and reducing transit times. Autonomous trucks also improve supply chain reliability, as evidenced by successful trials in Germany and expanded operations in U.S. oilfield logistics. Governments are supporting these developments through evolving regulations that enable testing and deployment, such as the U.S. Department of Transportation’s pilot programs and China’s proactive regulatory framework. As automation continues to redefine logistics, hub-to-hub autonomous trucking stands out as a scalable, cost-saving, and efficiency-boosting opportunity for the industry’s future.

Market Challenges

Regulatory Fragmentation and Compliance Barriers are Marked as a Critical Challenge.

The most critical challenge for the global autonomous truck market is regulatory fragmentation, which creates inconsistent safety standards, delays deployment, and increases compliance costs. For instance, the U.S. lacks a unified federal framework, with states such as California and Texas adopting divergent rules. Waymo’s 2025 expansion delays in Northern California due to local government opposition exemplify how fragmented regulations disrupt scalability. Similarly, the EU’s member states enforce varying interpretations of autonomous vehicle safety, complicating cross-border operations. Manufacturers such as Aurora and Kodiak Robotics must navigate these disparities while adhering to evolving guidelines from bodies such as NHTSA and FMCSA.

In China, despite proactive policies supporting autonomous freight, regional pilot programs face delays due to uneven infrastructure and approval processes. Recent updates include FMCSA’s 2024 pilot programs for autonomous trucking, yet gaps in liability frameworks and cybersecurity standards persist. Technological advancements, such as Geely’s autonomous heavy trucks in China and Embark Trucks’ highway-focused systems, are outpacing regulatory harmonization. Without global standardization, manufacturers face costly retrofits and limited market access. For example, Daimler’s autonomous trucks comply with EU-specific safety protocols but require redesigns for U.S. operations. Resolving this challenge demands coordinated policy efforts, such as the EU’s upcoming 2025 autonomous vehicle legislation and U.S. bipartisan proposals for federal oversight. Until then, regulatory uncertainty remains the primary bottleneck for widespread adoption.

Segmentation Analysis

By Level of Autonomy

Increasing Demand for Pickup Trucks to Dominate Adoption of Level 1 Trucks

By level of autonomy, the market is segmented into level 1, level 2, level 3, and level 4.

The level 1 segment will account for 87.99% market share in 2026. Demand for pickup trucks equipped with semi-autonomous driving features, such as basic parking assistance and lane departure warning, is increasing in the U.S. Furthermore, truck-related fatalities have continued to increase, specifically in Europe, China, and India, which boosted the adoption of level 1 automated trucks. Hence, these factors are likely to augment the growth of this segment.

Level 3 has a considerable growth rate as autonomous trucks can manage most driving tasks independently but require human intervention under certain conditions, making it the growing market segment. Successful pilot programs and favorable regulatory developments propel the growth of this segment. In 2023, Daimler Trucks, in collaboration with Torc Robotics, announced plans to deploy Level 3 autonomous Freightliner Cascadia trucks in selected U.S. states, leveraging advanced sensor systems and artificial intelligence to navigate complex driving environments.

Testing of level 4 trucks on public roads, especially in the U.S. and Germany, has increased considerably over the last few years. Additionally, several manufacturers, such as Volvo, Navistar, and Ford, are bypassing level 3 automation and focusing on developing level 4 driverless trucks. The increasing focus of leading auto manufacturers on developing and deploying autonomous technology in vehicles is further expected to drive industry growth. Hence, the level 4 segment is anticipated to show significant growth in the market during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Type

IC Engine Segment to Dominate Due to Strong Established Fueling Infrastructure

By propulsion type, the market is classified into IC engine and electric.

The IC engine segment is expected to account for 93.34% of the market in 2026. The durability and reliability of ICE trucks make them suitable for long-haul operations across diverse terrains and climates. While the industry is gradually shifting toward electrification, the existing dominance of ICE autonomous trucks ensures a stable and continuous movement of goods, thereby sustaining the global supply chain and contributing to the market share during this transitional period.

The electric truck segment is expected to show the fastest CAGR of 8.70% in the market owing to the introduction of stringent emission regulations, particularly in the U.S. and Europe. For example, the European Union's Green Deal aims to reduce carbon emissions significantly by 2030, encouraging the shift to electric transportation sector. OEMs are responding with innovative electric autonomous truck models. Tesla's Semi, equipped with autonomous driving capabilities, has been adopted by companies such as PepsiCo to reduce their carbon footprint.

By Truck Type

Heavy-Duty Trucks to Gain Traction with Rising Shortage of Drivers

By truck type, the market is categorized into light-duty trucks, medium-duty trucks, and heavy-duty trucks.

The heavy-duty trucks segment is anticipated to exhibit a high CAGR of 13.40% owing to the continued shortage of drivers, particularly in the U.S. Companies such as TuSimple, Daimler Trucks, and Volvo have been at the helm of fully autonomous truck trials. In December 2023, TuSimple completed a fully autonomous, 80-mile freight run in Texas without a human safety driver, marking a milestone in level 4 truck deployment.

The light-duty trucks segment is anticipated to hold a dominant market share of 73.42% in 2026, owing to the increasing demand for last-mile delivery solutions, urban logistics, and e-commerce growth. Companies such as Gatik and Nuro have launched multiple pilot programs across the U.S. and Canada, partnering with retailers such as Walmart to optimize autonomous goods transport in urban areas. In 2023, Walmart expanded its partnership with Gatik, rolling out driverless middle-mile deliveries in Texas and Arkansas. Similarly, Nuro’s R3 autonomous vehicle has been deployed in California and Arizona for automated grocery and parcel delivery.

By Industry

Demand for Automated Trucks to Increase in Logistics & Transportation of FMCG Products

By industry, the market is categorized into manufacturing, construction & mining, FMCG, military, and others.

The FMCG segment is expected to account for 34.3% of the market in 2026 and is likely to continue its dominance throughout the forecast period. The rising demand from various end-users in the market for raw materials and finished goods is leading to the increased frequency of logistics delivery in various regions. This has led to a demand for efficient transportation of FMCG products coupled with the growing adoption of e-commerce platforms post-pandemic. This is expected to drive the segment’s growth during the forecast period.

The construction & mining segment is also anticipated to witness the highest CAGR of 12.00% during the forecast period. Major mining companies in Australia, the U.S., and Europe are focused on utilizing fully autonomous trucks for their mining activities in the pursuit of eliminating casualties and tackling the skilled worker shortage in developed economies. Manufacturing and military segments are also expected to witness a considerable growth rate in the future. This growth is driven by the need to improve the efficiency of transportation, support high-risk military missions, and reduce the risk for combat troops in operation. Military, manufacturing, and other segments with significant growth are increasingly adopting such trucks for logistics and battlefield operations.

Autonomous Truck Market Regional Outlook

Technological Advancements to Drive North America Market Growth

Regionally, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Autonomous Truck Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America maintained a strong presence in the global market, reaching USD 16.48 billion in 2025, accounting for 38.40% share, and is expected to reach USD 17.57 billion in 2026, which is also investing heavily in autonomous trucking, with Loblaw Companies deploying Level 2 and Level 3 trucks for long-haul logistics. The region’s dominance in the market is fueled by high technological adoption, government support, and increasing demand for driverless freight solutions. The regional market is characterized by the presence of several startups, such as Embark Trucks and Waymo, which have accelerated the adoption of highly automated trucks in freight operations. For instance, in April 2023, Aurora, one of the leading self-driving technology companies, announced its plans to roll out a self-driving trucking service between Dallas and Houston to test its autonomous freight-hauling services. Several major companies and startups are actively developing autonomous trucking technologies and conducting trials in North America. They are investing in advanced sensors, AI algorithms, and connectivity to enable these vehicles to navigate highways and perform various tasks autonomously.

The U.S. market is projected to reach USD 16.68 billion by 2026., is witnessing rapid expansion, driven by advancements in AI, sensor technology, and strong demand for efficient logistics solutions. Heavy-duty autonomous trucks dominate the sector primarily due to their suitability for long-haul freight and significant cost-saving potential. In 2024, the U.S. self-driving cars and trucks market volume reached approximately 100,890 units, with projections to surpass 4 million units by 2034. Major players such as Tesla, Volvo, and Paccar are investing in R&D, while supportive government initiatives and evolving regulations are accelerating adoption and innovation

Asia Pacific

The Asia Pacific market accounted for USD 11.27 billion in 2025, representing 26.26% of the global industry, and is expected to reach USD 13.19 billion in 2026 and expected to exhibit the fastest CAGR over the forecast period owing to the introduction of road safety norms by several countries and the rapid advancement of autonomous vehicles in Japan and China, mainly for last-mile delivery and mining trucks. China, Japan, South Korea, and Singapore are actively investing in the research & development of autonomous vehicle technologies, including autonomous trucks. They recognize the potential benefits of these vehicles in terms of improved efficiency, reduced costs, and enhanced logistics operations. In China, for example, the government has identified autonomous vehicles, including self-driving trucks, as a strategic industry. It has set ambitious goals to become a global leader in autonomous driving technology. Chinese companies, such as TuSimple, Pony.ai, and FAW, are already conducting trials and developing autonomous trucking solutions. The Japan market is projected to reach USD 12.4 billion by 2026, the China market is projected to reach USD 15.06 billion by 2026, and the India market is projected to reach USD 13.29 billion by 2026.

Europe

In 2025, Europe generated USD 14.81 billion, contributing 34.52% to global market revenue, and is projected to grow to USD 15.42 billion in 2026. The market in Europe is characterized by initiatives, such as the EU-funded ENSEMBLE project that aims to implement multi-brand truck platooning (level 3 automation) in Europe over the next three years to improve traffic safety and fuel economy. Furthermore, the stringenacy of safety regulations is higher in this region than in other regions, such as Lane Keep Assist (LKA) and advanced emergency braking systems, which have been made mandatory for all trucks in this region since 2015. These factors are propelling the growth of the market in Europe. The UK market is projected to reach USD 0.5 billion by 2026, while the Germany market is projected to reach USD 4.28 billion by 2026, France likely to account for USD 4.00 billion in 2025.

Rest of the World

Rest of the World accounted for USD 0.35 billion in 2025, representing 0.82% of the global market share, and is projected to reach USD 0.4 billion in 2026. The rest of the world, which covers South America, the Middle Eastern, and African countries, is estimated to hit USD 0.35 billion in 2025 and expected to witness considerable CAGR in the upcoming years owing to governments’ focus on creating a knowledge-based economy, developing human capital, and digitalization. The adoption of self-driving trucks will reduce the region’s reliance on emigrant labor and improve road safety.

COMPETITIVE LANDSCAPE

Key Market Players

AB Volvo to Emerge as One of Leading Market Players Due to its Strategic Collaborations and Technological Advancements

AB Volvo is a prominent player in the global market, holding a significant share alongside Daimler AG. Volvo's leadership in this sector is attributed to its extensive experience in safety and technology, combined with strategic partnerships and innovative offerings. For instance, Volvo Autonomous Solutions unveiled the Volvo VNL Autonomous, a production-ready autonomous truck that integrates Volvo's commercial vehicle expertise with Aurora Innovation's autonomous driving technology. This collaboration highlights Volvo's commitment to advancing autonomous solutions, particularly in North America, where it aims to enhance freight capacity and contribute to sustainable transportation. Volvo's focus on both freight and mining operations, along with trials in real-world environments, further solidifies its position. The company's emphasis on safety, sustainability, and efficiency aligns with the growing demand for autonomous vehicles, making it a top choice for customers seeking reliable autonomous truck solutions.

Daimler AG is another major player in the global market, also holding a significant share. Daimler has been actively testing autonomous trucks using Level 4 technology, focusing on long-haul trucking. The company partners with various technology providers and works closely with governments to align with regulations. Daimler's autonomous trucks leverage its expertise in commercial vehicles, advanced driver assistance systems, and AI to ensure safety and efficiency. By integrating autonomous technology into its fleet and offering services to logistics companies, Daimler aims to expand its share in the autonomous truck industry.

LIST OF KEY AUTONOMOUS TRUCK COMPANIES PROFILED:

- Daimler AG (Germany)

- AB Volvo (Sweden)

- Waymo LLC (U.S.)

- Continental AG (Germany)

- Tesla (U.S.)

- PlusAI Inc. (U.S.)

- Caterpillar (U.S.)

- ai (U.S.)

- TATA Motors (India)

- Waabi AI (Canada)

KEY INDUSTRY DEVELOPMENTS:

- February 2025: Volvo Group Venture Capital AB invested in the Canadian company Waabi Innovation Inc. to develop the next generation of autonomous trucking technology. Waabi is developing next-generation artificial intelligence technology to solve autonomy at scale. The company recently unveiled the Waabi Driver, its core autonomous trucking solution, designed for large-scale commercialization and safe deployment.

- January 2025: Aurora, Continental, and NVIDIA join teams to launch driverless Trucks across the U.S., marking the first partnership in the states to scale these vehicles in the automotive industry. Continental aims to accelerate the development and deployment of driverless trucks across the U.S.

- January 2025: Torc Robotics, a Virginia-based independent subsidiary of Daimler Truck AG and a pioneer in commercializing self-driving vehicle technology, leased a facility in Hillwood’s AllianceTexas development in Fort Worth that will serve as its autonomous truck hub in the Dallas-Fort Worth area. Daimler Truck AG aims to accelerate its autonomous trucking capabilities and prepare for scaling the business to meet customer needs. This move aligns with the company's objective to lead in autonomous trucking technology and provide an efficient transport solution

- December 2024: Volvo Autonomous Solutions (V.A.S.) and DHL Supply Chain launched autonomous trucking operations in Texas using the Volvo VNL Autonomous, powered by Aurora Driver technology. Initial operations will cover Dallas to Houston and Fort Worth to El Paso routes, with safety drivers present during this validation phase.

- November 2024: Caterpillar Inc. successfully demonstrated the fully autonomous operation of its Cat 777 off-highway truck. The debut of this latest model of Cat MineStar Command for hauling at Luck Stone’s Bull Run plant in Chantilly, Virginia, U.S., marks a significant milestone in Caterpillar’s objective to deliver an autonomous hauling solution for the quarry and aggregates sector.

REPORT COVERAGE

The global autonomous truck market research report provides detailed market analysis and focuses on key aspects such as leading companies, vehicle types, design, and technology. Besides this, it offers insights into the latest market trends and highlights key industry developments. In addition to the factors mentioned above, it encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.04% from 2026 to 2034 |

|

Unit |

Value (USD Billion) and Volume (Thousand Units) |

|

Segmentation |

By Level of Autonomy

By Propulsion Type

By Truck Type

By Industry

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market was valued at USD 46.58 billion in 2026 and is projected to record a valuation of USD 107.7 billion by 2034.

The market is expected to register a CAGR of 11.04% during the forecast period of 2026-2034.

Increasing demand for efficient logistics operations is predicted to drive the global market growth.

North America led the market in 2026.

Daimler AG, AB Volvo, Waymo LLC, Continental AG, and Tesla are among the key market players.

- 2021-2034

- 2025

- 2021-2024

- 248

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us