Aviation Cloud Market Size, Share & Industry Analysis, By Type (Private Cloud, Public Cloud, and Hybrid Cloud), By Architecture (SaaS (Software as a Service), PaaS (Platform as a Service), and IaaS (Infrastructure as a Service)), By End User (Airlines, Airports, and Aircraft Manufacturers), By Application (Flight Operations & Scheduling, Aircraft Maintenance & Engineering, Passenger Services & Customer Experience, Crew Management & Training, and Others), and Regional Forecast, 2026-2034

Aviation Cloud Market Size & Share

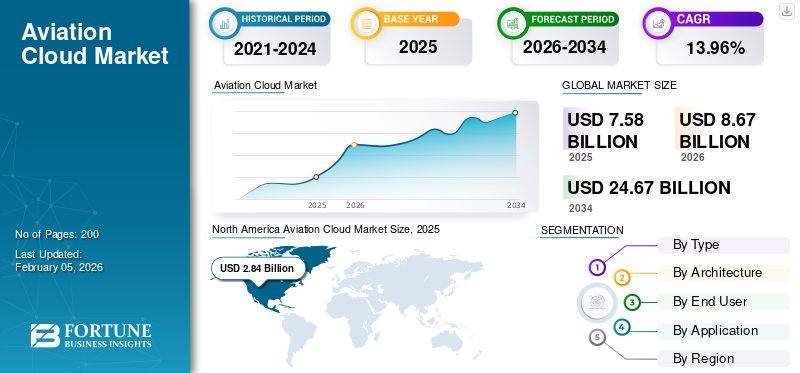

The global aviation cloud market size was valued at USD 7.58 billion in 2025 and is projected to grow from USD 8.67 billion in 2026 to USD 24.67 billion by 2034, exhibiting a CAGR of 13.96% during the forecast period. North America dominated the global aviation cloud market, accounting for 37.42% market share in 2025.

The aviation cloud market size growth is driven by rising volumes of operational data generated by connected aircraft, advanced sensors, and passenger-facing systems. Airlines increasingly rely on centralized cloud platforms to unify disparate legacy systems, enabling predictive analytics, dynamic scheduling, and fuel optimization. Airports adopt cloud solutions to improve capacity planning, asset utilization, and security coordination, while aircraft manufacturers embed cloud connectivity across digital twins and lifecycle management frameworks.

Aviation cloud is a cloud-based technology applied across the aviation sector, including airlines, airports, aircraft manufacturers, and air traffic management. It helps the aviation industry to perform real-time data sharing and scalable computing to support various operations such as flight planning, predictive maintenance, passenger services, baggage tracking, and security. The aviation cloud market is expected to grow significantly during the forecast period, as airlines face increasing pressure to modernize their operations.

The aviation cloud market share landscape is moderately concentrated, with global technology providers and aviation-specialist software vendors occupying leading positions. However, competitive dynamics continue to evolve as niche providers deliver specialized applications optimized for regulatory compliance, safety-critical environments, and industry-specific workflows. Software-as-a-service delivery models dominate new deployments, reflecting operator preference for scalability and reduced infrastructure ownership.

Aviation cloud market trends indicate accelerating migration toward hybrid and multi-cloud architectures. These models balance data sovereignty, latency management, and cybersecurity requirements. Artificial intelligence and advanced analytics are increasingly integrated within aviation cloud platforms, enhancing operational forecasting and disruption management.

Aviation cloud market growth is expected to remain structurally strong through the forecast period. Expansion is supported by fleet growth, digital regulation, and long-term efficiency imperatives. Regional adoption patterns vary, but cloud platforms are becoming foundational to aviation competitiveness and operational continuity.

Major players in the aviation cloud market include AWS, Microsoft Azure, Google Cloud, IBM, Oracle, SITA, and Salesforce. For instance, AWS powers airline platforms such as Ryanair’s digital services. Cloud technology is increasingly being adopted to improve operational efficiency and enhance customer experience. Key players such as AWS, Azure, and Google Cloud are forming strategic partnerships with airlines across the world to deliver AI, analytics, and infrastructure solutions.

Download Free sample to learn more about this report.

Aviation Cloud Market Takeaways

- 2025 Market Size: USD 7.58 billion

- 2026 Market Size: USD 8.67 billion

- 2034 Forecast Market Size: USD 24.67 billion

- CAGR: 13.96% from 2026–2034

- North America dominated the global aviation cloud market with a 37.42% share in 2025.

- The public cloud segment is projected to account for 51.03% of the market share in 2026.

- The airlines segment is expected to hold a dominant 64.34% market share in 2026.

North America

North America led the global market with USD 2.84 billion in 2025 and is projected to reach USD 3.24 billion in 2026, driven by rapid cloud adoption across aviation operations.

Europe

Europe accounted for USD 2.11 billion in 2025 and is expected to grow to USD 2.43 billion in 2026, supported by digital transformation initiatives across airports and airlines.

Asia Pacific

Asia Pacific held 23.90% of the global market in 2025, reaching USD 1.81 billion and projected to rise to USD 2.10 billion in 2026.

U.S.

The aviation cloud market is projected to reach USD 2.57 billion by 2026, driven by investments in passenger experience, operational efficiency, and cloud-based aviation platforms.

Japan

The market is projected to reach USD 0.40 billion by 2026, supported by increasing adoption of cloud technologies across airline and airport operations.

Read More

Aviation Cloud Market Trends

Emergence of Multi-Cloud and Hybrid Cloud Architectures is a Key Market Trend

Airlines and airports adopt multi-cloud technology to avoid vendor lock-in and ensure system reliability. The trend of using different cloud providers for specific tasks and improving the speed of the various operations has surged. By using multiple platforms in tandem, aviation companies gain flexibility, optimize costs, and tailor service to regional requirements.

As per the State of Multicloud Security Report by Microsoft, nearly 86% of organizations in 2024 had already adopted a multicloud technology due to the advantages provided by the approach, such as increased agility, flexibility, and choice. Furthermore, multi-cloud adoption has increased to maintain security and has made it easy for the airlines to shift from legacy IT systems to cloud-based solutions, boosting the aviation cloud market growth.

- For instance, in August 2024, Lufthansa Systems partnered with Google Cloud to expand its Global Aviation Cloud platform into a multi-cloud environment, complementing its existing Microsoft Azure services.

Aviation cloud market trends increasingly reflect the transition toward hybrid and multi-cloud strategies. Operators balance public cloud scalability with private environments to meet latency, resilience, and regulatory requirements. This approach supports gradual migration while protecting safety-critical workloads.

Software-as-a-service adoption continues to expand across aviation functions. Airlines favor modular cloud applications for crew management, maintenance planning, and disruption recovery. These platforms reduce customization complexity and accelerate deployment cycles. Artificial intelligence integration is a defining trend. Cloud-based analytics platforms process operational data to support predictive maintenance, fuel optimization, and demand forecasting. These capabilities enhance operational resilience and improve financial performance.

Digital twin technology is gaining traction. Aircraft manufacturers and airlines use cloud-hosted digital twins to simulate performance, manage lifecycle costs, and support engineering collaboration. This trend strengthens the cloud’s strategic role beyond operational systems. Cybersecurity enhancement represents another key trend. Aviation cloud platforms increasingly incorporate zero-trust architectures, encryption, and continuous monitoring. These measures address rising threat exposure and regulatory scrutiny, reinforcing trust in cloud adoption and shaping long-term aviation cloud market trends.

Market Growth Drivers

Increase in Demand for Digital Modernization and Operational Efficiency to Propel Market Growth

The most prominent driver of the market is the growing emphasis on upgrading outdated systems to advanced digital platforms for faster and more effective operations. The growing need for digital transformation in the aviation industry, combined with the demand for enhanced operational efficiency, is expected to propel the growth of the market during the forecast period.

Digital transformation across the aviation industry is the primary driver of the aviation cloud market. Airlines and airports face increasing operational complexity driven by traffic growth, cost pressure, and regulatory requirements. Cloud platforms enable centralized data management, real-time analytics, and scalable computing resources that legacy systems cannot support efficiently.

Operational efficiency imperatives further accelerate adoption. Cloud-based flight operations and maintenance systems improve scheduling accuracy, reduce delays, and enable predictive maintenance. These capabilities directly lower operating costs and enhance asset utilization, making cloud investment strategically necessary rather than discretionary.

Growth in connected aircraft ecosystems is another critical driver. Modern aircraft generate large volumes of telemetry and performance data. Cloud platforms provide the infrastructure required to ingest, process, and analyze this data across fleets and geographies. Integration with airline operations centers strengthens situational awareness and decision speed. Passenger experience expectations also influence adoption. Cloud-enabled customer platforms support personalization, real-time communication, and service recovery. Airlines leverage these capabilities to improve loyalty and revenue performance.

Airlines and airports are rapidly adopting cloud technology into their operations for real-time data access and automation to achieve improved efficiency and reduced costs.

- For instance, in June 2025, VirgiThe n Airlines signed a seven-year agreement with Tata Consultancy Services (TCS) for the modernization of core technology systems, including pricing, seat allocation, maintenance, and customer preferences forecasting. The partnership leverages advanced technologies such as AI and IoT to streamline operations.

Market Restraints

Data Security and Privacy Concerns to Restrict Market Expansion

Data security and privacy concerns are one of the major restraints for the market during the forecast period. Aviation companies handle highly sensitive information such as passenger data, flight operations, maintenance, repair, and overhaul MRO records.

There are risks of cyberattacks, hacking, and unauthorized access when the data is stored on cloud platforms. Moreover, the strict regulatory requirements and the need to protect critical infrastructure are expected to present restraints in the complete adoption of cloud technologies. Therefore, the concerns over potential data breaches continue to hamper the growth of the market.

- In addition, the migration of safety-critical and personal data to the cloud requires aviation companies to meet with evolving aviation-specific security rules; for instance, EASA information security standards and sector guidance from IARA, along with sovereignty requirements, such as the EU’s GDPR/NIS2 and other regional cloud mandates. These regulatory and security obligations are expected to restrict the market expansion during the forecast period.

Despite strong demand fundamentals, the aviation cloud market faces several structural restraints. Data security and sovereignty concerns remain paramount. Aviation systems handle safety-critical and sensitive passenger data, requiring rigorous compliance with national and international regulations. These requirements complicate cloud migration strategies, particularly across jurisdictions.

Legacy system integration presents another significant challenge. Airlines and airports operate complex technology stacks built over decades. Migrating mission-critical workloads to cloud platforms requires careful phasing, customization, and validation, increasing cost and implementation timelines.

Operational risk aversion within aviation also moderates adoption speed. Stakeholders prioritize system reliability and uptime, leading to cautious deployment of new architectures. Cloud outages or performance issues can have cascading operational impacts, reinforcing conservative procurement behavior.

Market Opportunities

Cloud-Native Transformation of Airline & Airport Operations to Create Lucrative Growth Opportunities

The aviation industry is facing pressure to improve passenger experience without exceeding costs. Thus, airlines and airports are actively migrating key operations, such as passenger service, retailing, and baggage handling, to cloud platforms. Cloud-native platforms are becoming popular tools for the migration and transformation of key operations. Airlines experience fluctuating demands, which are easily handled by cloud-native systems. For instance, SITA Flex allows airports and airlines to deploy passenger processing on mobile devices and kiosk systems, regardless of location. In addition, the rising trend of fast cloud migration is aimed at minimizing downtime and ensuring uninterrupted operations.

- For instance, in September 2024, IndiGo Airlines completed the cloud migration in under 18 months, closing all of its data centers to boost scalability and access to modern technologies. The airline now focuses majorly on the use of AI, machine learning, data analytics, and business intelligence to enhance its services.

Significant opportunities exist through the deeper integration of cloud platforms across airline value chains. End-to-end visibility from flight planning to post-flight analytics enables performance optimization and cost control. Vendors offering interoperable solutions can capture an expanded scope within customer accounts.

Airports present an underpenetrated opportunity. Cloud adoption supports smart airport initiatives, including predictive passenger flow management and asset monitoring. As airport operators modernize infrastructure, demand for scalable cloud platforms increases.

Emerging markets offer strong growth potential. Rapid traffic growth and infrastructure investment create favorable conditions for cloud-native aviation systems, bypassing legacy constraints. Local partnerships and compliant deployment models facilitate entry. Advanced analytics and artificial intelligence applications create incremental value. Cloud platforms that translate operational data into actionable insights strengthen customer retention and pricing power.

Market Challenges

High Integration Costs to Hamper Market Growth

Numerous airlines and airports continue to run mission-critical applications such as reservation, departure control, MRO, and ATC support on mainframes or highly customized technology stacks. The migration of these current technologies to cloud-based technologies requires re-engineering and staff retraining. Such a shift can cause high costs and lengthy timelines, which can slow adoption and hinder the complete integration of cloud technologies into aviation operations.

Download Free sample to learn more about this report.

Market Segmentation Analysis

By Type

High Demand for Cost-Efficient and Scalable Cloud Platform Contributed to Public Cloud Segment Growth

On the basis of type, the market is classified into private cloud, public cloud, and hybrid cloud.

Public Cloud:

The public cloud segment will account for the largest aviation cloud market share of 51.03% in 2026. Factors such as cost efficiency, scalability, and faster deployment are driving the growth of the segment. Airlines and airports are investing in the integration of public cloud technology for passenger service systems (PSS), departure control, retailing, and analytics. Key providers such as AWS, Microsoft Azure, and Google Cloud partner with different airlines and airports.

- For instance, in February 2023, Lincoln Airport in Nebraska awarded a contract with AeroCloud Systems, a U.K.-based airport management solutions provider, to implement a cloud-based airport operations platform aimed at improving airport operations and enhancing the passenger experience.

Public cloud adoption is expanding rapidly across non-safety-critical aviation functions. Airlines deploy public cloud platforms for analytics, passenger engagement, revenue management, and collaboration tools. The scalability and elasticity of public cloud services enable rapid experimentation and cost optimization. Public cloud providers increasingly tailor offerings for regulated industries, improving aviation suitability. This segment contributes significantly to the aviation cloud market size expansion, particularly through software-as-a-service adoption.

Hybrid Cloud:

Hybrid cloud is the fastest-growing segment in the market during the forecast period, as aviation companies require both security and control along with flexibility and global scalability, which is addressed by hybrid cloud technology. Hybrid cloud architectures represent the fastest-growing deployment model.

Aviation stakeholders combine private environments for mission-critical systems with public cloud resources for analytics and customer-facing applications. This approach balances security, flexibility, and cost efficiency. Hybrid cloud adoption reflects pragmatic migration strategies, allowing gradual transformation without operational disruption. As a result, hybrid deployments are central to aviation cloud market trends and future platform strategies.

Private Cloud:

Private cloud deployments remain prevalent among aviation stakeholders managing safety-critical and regulated workloads. Airlines and airports use private cloud environments to maintain control over sensitive operational data, flight systems, and regulatory reporting. This model supports strict compliance with aviation authorities and data sovereignty mandates. While private cloud adoption involves higher upfront and operating costs, it offers predictable performance and enhanced security. Large network carriers and hub airports favor private cloud for core operational systems, sustaining its relevance within the aviation cloud market.

By Architecture

Increasing Need for Subscription-based Cloud Solutions Fueled the Growth of the SaaS (Software as a Service) Segment

In terms of architecture, the market is categorized into SaaS (Software as a Service), PaaS (Platform as a Service), and IaaS (Infrastructure as a Service).

Software as a Service (SaaS):

The SaaS (Software as a Service) segment is expected to capture the largest share of the market of 44.49% in 2026. Airlines and airports are adopting SaaS (Software as a Service) solutions to avoid heavy capital investment in IT hardware and perpetual licenses. SaaS operates on a subscription-based pricing model, enabling easier budgeting, which is expected to further drive demand. Moreover, cloud solution providers offer SaaS solutions that can easily integrate with IoT sensors on aircraft, airport systems, and global data feeds (weather, traffic flow, and fuel prices), which allows faster deployment.

- For instance, in July 2024, Air India announced the adoption of iCargo, IBS Software, a fully integrated SaaS platform to digitize its entire cargo operations.

SaaS dominates aviation cloud adoption due to ease of deployment and reduced infrastructure burden. Airlines and airports increasingly select SaaS solutions for crew management, maintenance planning, and passenger services. Standardized functionality and subscription pricing improve cost predictability. SaaS providers embed regulatory compliance and industry best practices, accelerating adoption. This architecture accounts for a substantial share of the aviation cloud market in new deployments.

Platform as a Service (PaaS):

The PaaS (Platform as a Service) segment is expected to be the fastest-growing segment during the study period, as airlines and airports increasingly require custom-built applications developed on platforms to meet their highly specific needs, rather than solely relying on COTS (Commercial Off-The-Shelf) software.

PaaS adoption supports application development and integration across aviation ecosystems. Airlines and manufacturers use PaaS to build customized analytics, data pipelines, and operational tools. This architecture enables innovation while leveraging managed infrastructure and security services. PaaS demand is strongest among digitally mature organizations pursuing proprietary differentiation. Its role continues to expand as data-driven aviation strategies mature.

Infrastructure as a Service (IaaS):

IaaS supports foundational computing, storage, and networking requirements. Aviation stakeholders deploy IaaS for legacy system migration and high-performance computing workloads. While less visible to end users, IaaS underpins broader cloud adoption. Its importance lies in enabling scalability and disaster recovery, contributing indirectly to the aviation cloud market growth.

To know how our report can help streamline your business, Speak to Analyst

By End User

Airlines Segment Led due to Rising Spending on Upgrading IT Infrastructure

Based on end user, the market is segmented into airlines, airports, and aircraft manufacturers.

Airlines:

The airlines segment is projected to hold the dominating position with 64.34% of market share in 2026. Airlines are modernizing flight operations, crew management, and maintenance through platform services. Moreover, airlines are making huge investments in upgrading their IT infrastructure and shifting to cloud solutions, which is driving the growth of the segment.

- For instance, in 2024, airline IT spend reached about USD 37 billion, while airport IT spend was around USD 9 billion, with most carriers and airports planning further increases.

Airlines represent the largest end-user segment within the aviation cloud market. They deploy cloud platforms across flight operations, maintenance, revenue management, and customer experience. Adoption behavior prioritizes reliability, scalability, and regulatory compliance. Network carriers lead investment due to operational complexity, while low-cost carriers adopt cloud to support lean operations. Airline demand anchors overall market expansion.

Airports:

The airports segment is expected to be the fastest-growing segment during the study period, owing to regulatory and cybersecurity requirements that are encouraging airports to adopt managed cloud solutions for analytics and security monitoring.

- For instance, in February 2025, Noida International Airport partnered with Kyndryl to build and manage its entire IT infrastructure, achieving 24/7 support and secure, technology-driven operations.

Airports increasingly adopt cloud platforms to manage capacity, assets, and passenger flows. Cloud-based systems support real-time coordination across stakeholders, improving operational resilience. Adoption is strongest at major hubs, where complexity and volume justify investment. As smart airport initiatives expand, airport-driven demand contributes to the aviation cloud market growth.

Aircraft Manufacturers:

Aircraft manufacturers use cloud platforms for design collaboration, digital twins, and lifecycle management. Cloud adoption supports engineering efficiency and aftermarket services. While smaller in volume, this segment drives high-value use cases and long-term platform partnerships.

By Application

Passenger Services & Customer Experience Segment Led due to Growing Need for Cloud-Based Personalization

Based on application, the market is segmented into flight operations & scheduling, aircraft, maintenance & engineering, passenger services & customer experience, crew management & training, and others.

Passenger Services & Customer Experience:

In 2026, the global market is estimated to dominate market share of 36.95% by the passenger services & customer experience segment in terms of market share, with a market share of 36.95%. This is due to an increase in demand for cloud-based personalization, self-service kiosks, and real-time travel updates aimed at enhancing passenger experience.

This segment is also expected to be the fastest-growing segment during the forecast period. Numerous airlines leverage AWS to handle real-time fare search demand across their website and mobile apps, ensuring that customers can easily book flights during peak traffic periods. Cloud platforms support personalization, communication, and service recovery. Airlines prioritize these applications to enhance loyalty and ancillary revenue.

- For instance, in June 2025, Iberia Airlines migrated its mission-critical systems to AWS to boost operational efficiency and reliability. The airline aimed at integrating AI to improve passenger experiences and accelerate innovation.

Flight Operations & Scheduling:

Cloud-based flight operations systems enable dynamic scheduling, disruption management, and fuel optimization. Airlines rely on real-time data integration to improve punctuality and cost control. Adoption is widespread due to measurable operational benefits.

Aircraft Maintenance & Engineering:

Maintenance applications leverage cloud analytics for predictive maintenance and parts planning. These systems reduce downtime and extend asset life, supporting strong adoption across fleets.

Regional Insights

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Aviation Cloud Market Analysis:

North America Aviation Cloud Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 2.84 billion in 2025, representing 37.42% of the global market share, and is projected to reach USD 3.24 billion in 2026. Factors driving the dominance include the adoption of advanced IT infrastructure, big data analytics, and cloud technology by carriers and airlines to optimize operations and increase efficiency.

Airlines such as Southwest Airlines have migrated critical workloads to AWS to improve operational efficiency, while Alaska Airlines uses AI-driven flight optimization tools hosted in the cloud to enhance routing and fuel efficiency. Leading cloud providers such as AWS, Microsoft Azure, and Google Cloud are focusing on designing aviation-focused solutions for airlines and airports in the region. The U.S. market is projected to reach USD 2.57 billion by 2026.

- For instance, in June 2024, Southwest Airlines contracted with AWS to modernize its outdated IT systems and enhance operational efficiencies and passenger experience. This decision was made after the airline’s December 2022 IT meltdown, which caused over 16,700 flight cancellations. With this upgrade, the airline aims to improve passenger services and prevent future disruptions.

North America represents a leading Aviation Cloud market supported by early digital adoption and advanced regulatory frameworks. Airlines and airports invest heavily in cloud platforms to improve operational resilience and data-driven decision-making. Strong technology ecosystems and established cloud providers enable rapid deployment. The region maintains a high Aviation Cloud market share through continuous innovation and enterprise-scale adoption across commercial aviation stakeholders regionally.

United States Aviation Cloud Market:

The United States Aviation Cloud market is driven by complex airline networks and dense airport operations. Cloud adoption focuses on flight operations optimization, predictive maintenance, and passenger experience platforms. Regulatory oversight encourages secure, compliant architectures. High digital investment levels and strong vendor competition support sustained Aviation Cloud market growth across major commercial aviation stakeholders nationwide, including airlines, airports, service providers, and technology partners operating nationally.

Europe Aviation Cloud Market Analysis:

The European market was valued at USD 2.11 billion in 2025, capturing 27.90% of global revenue, and is estimated to reach USD 2.43 billion in 2026. Europe is anticipated to witness a notable growth in the coming years, driven by strong regulatory pressure for digitalization under EU programs such as SESAR (Single European Sky ATM Research), which requires airlines and airports to modernize operations.

Major European carriers such as Lufthansa Group and Air France–KLM are investing heavily in cloud platforms to streamline flight scheduling, enhance predictive maintenance, and improve passenger services. The UK market is projected to reach USD 0.58 billion by 2026, and the German market is projected to reach USD 0.8 billion by 2026.

The European Aviation Cloud market is shaped by regulatory harmonization and strict data protection requirements. Airlines prioritize hybrid cloud architectures to balance compliance, scalability, and latency management. Airports deploy cloud platforms to enhance capacity planning, sustainability reporting, and stakeholder coordination. Coordinated regulatory frameworks and cross-border initiatives support consistent Aviation Cloud market growth across regional aviation ecosystems, serving multiple national carriers, airport operators, and service providers.

Germany Aviation Cloud Market:

Germany’s Aviation Cloud market emphasizes efficiency, reliability, and compliance-driven digital transformation. Airlines and airports deploy cloud platforms for maintenance optimization, data integration, and operational planning. Strong engineering standards and regulatory discipline influence procurement strategies. Investment in secure cloud environments supports steady Aviation Cloud market growth aligned with safety performance and system resilience priorities across airline, airport, and aviation infrastructure organizations nationally and regionally integrated.

United Kingdom Aviation Cloud Market:

The United Kingdom Aviation Cloud market benefits from advanced digital infrastructure and innovation-oriented policy frameworks. Airlines adopt cloud solutions for disruption management, crew scheduling, and customer engagement. Airports invest in cloud-based coordination systems to improve throughput and situational awareness. Supportive regulatory initiatives sustain consistent Aviation Cloud market growth across commercial aviation operations, including airlines, airports, ground handlers, service providers, and aviation authorities nationwide.

Asia-Pacific Aviation Cloud Market Analysis:

In 2025, the Asia Pacific held 23.90% of the global market, reaching a valuation of USD 1.81 billion, and is projected to grow to USD 2.1 billion in 2026. The market in the Asia Pacific is growing significantly due to an increase in fleet expansion to meet rising air traffic and surging demand for operational efficiency and cost-effective management. For instance, in June 2025, China Airlines announced its plans to invest approximately USD 2 billion to acquire up to 13 new aircraft, including five Airbus A350-900s and eight A321neos.

Moreover, airlines across the region are deploying cloud-based systems to efficiently handle large volumes of passengers. The Japan market is projected to reach USD 0.4 billion by 2026, the China market is projected to reach USD 0.75 billion by 2026, and the India market is projected to reach USD 0.56 billion by 2026.

- For instance, in July 2023, the Airports Authority of India (AAI) contracted with SITA to integrate cloud-based passenger and baggage processing technologies at 43 airports, with scalability to 40 more over seven years. The initiative upgraded over 2,700 passenger touchpoints, improving efficiency and self-service options while processing over 500 million passengers.

Asia Pacific is the fastest-growing Aviation Cloud market, driven by traffic expansion, fleet growth, and infrastructure modernization. Airlines deploy cloud native systems to manage operational scale and complexity. Airports adopt digital platforms to improve efficiency, passenger flow, and asset utilization. Government support and rapid technology uptake accelerate Aviation Cloud market growth across emerging and developed economies, serving airlines, airports, manufacturers, service providers, and regulators.

Japan Aviation Cloud Market:

Japan’s Aviation Cloud market prioritizes operational reliability, automation, and data accuracy across airline and airport systems. Airlines deploy cloud platforms to enhance maintenance planning, flight scheduling, and safety analytics. Airports use cloud solutions to improve passenger flow and coordination. Strong technology readiness and disciplined oversight support sustained Aviation Cloud market growth aligned with efficiency objectives for national carriers, airport operators, service providers, regulators, and partners.

China Aviation Cloud Market:

China’s Aviation Cloud market is driven by rapid air traffic growth, large-scale airport expansion, and state-backed digital initiatives. Airlines and airports deploy cloud platforms to manage data integration and operational coordination. Preference for domestic cloud providers shapes competitive dynamics. High investment intensity supports accelerating the Aviation Cloud market size expansion nationwide across airlines, airports, manufacturers, service providers, technology firms, regulators, and aviation authorities.

Latin America Aviation Cloud Market Analysis:

The Latin America region captured 4.22% of the global market in 2025, generating USD 0.32 billion in revenue, and is projected to reach USD 0.35 billion in 2026. Over the forecast period, the Latin America and Middle East & Africa regions would witness a moderate growth. Soaring investments in cloud technology due to an increase in demand for low-latency and high-reliability cloud services drive market growth in the region. For instance, in May 2025, AWS announced a major investment to build its first data centers and cloud infrastructure in Chile, marking its third cloud region in Latin America after Brazil and Mexico.

Latin America represents an emerging Aviation Cloud market supported by gradual digitalization and infrastructure upgrades. Airlines adopt cloud solutions to improve scheduling, maintenance, and cost control. Airports deploy cloud platforms selectively to enhance coordination. Regulatory development varies by country, influencing adoption pace, but long-term Aviation Cloud market growth potential remains positive across regional airlines, airports, service providers, technology partners, regulators, and aviation stakeholders broadly.

Middle East & Africa Aviation Cloud Market Analysis:

Middle East & Africa contributed approximately USD 0.5 billion to the global market in 2025, accounting for 6.57% share, and is expected to reach USD 0.56 billion in 2026. In the Middle East & Africa, airports such as Dubai International (DXB), Hamad International (DOH), and King Abdulaziz International (JED) are increasingly using cloud technology to handle a large number of passengers and flight data. National strategies such as Saudi Vision 2030 and the UAE’s smart airport initiatives are accelerating the adoption of digital infrastructure, including biometric-enabled passenger services built on cloud platforms. Airlines across the region are working with cloud providers to boost operational efficiency and elevate passenger experiences.

- For instance, in January 2024, Saudia became the first airline in Saudi Arabia to adopt RISE with SAP on Google Cloud, aimed at enhancing operational efficiency, safety, and cost optimization through cloud-based aviation solutions.

The Middle East and Africa Aviation Cloud market adoption is driven by airport expansion, airline modernization, and national digital initiatives. Airlines deploy cloud platforms for operations and customer systems. Airports invest in cloud-based coordination and security tools. Market growth depends on regulatory alignment, investment continuity, and partnership-driven capability development across airlines, airports, service providers, governments, regulators, investors, and operators.

Aviation Cloud Industry Competitive Landscape

Key Players Focus on Partnerships with Aviation Companies to Modernize IT Systems

The global market is shaped by leading cloud technology and service providers that constantly assist the operations of various airlines, airports, and MROs, enabling them to digitize operations and scale efficiently.

Public cloud providers such as AWS, Microsoft Azure, and Google Cloud provide core infrastructure, AI, and analytics, while companies such as SITA, Amadeus, and Lufthansa Systems deliver aviation-specific platforms for flight ops, passenger services, and maintenance. These companies actively partner with global and regional airlines to modernize IT systems and enhance resilience. Cloud computing services such as Microsoft Azure also power predictive maintenance programs for aircraft OEMs.

Providers are increasingly leveraging technologies such as AI and IoT, and edge computing to improve decision-making, safety, and customer experience. These companies are undertaking various strategic initiatives, such as investments in R&D and partnerships with airports to enhance their market presence.

The aviation cloud industry's competitive landscape is defined by a combination of global hyperscale cloud providers, aviation-specialized software vendors, and niche digital solution providers. Competition centers on regulatory compliance, system reliability, domain expertise, and the ability to integrate cloud platforms with safety-critical aviation operations. Vendors differentiate less on infrastructure and more on aviation-specific functionality and service depth.

Large global cloud providers hold a strong position by offering scalable infrastructure, advanced analytics, and artificial intelligence capabilities. Their aviation cloud market share is reinforced through partnerships with airlines, airports, and original equipment manufacturers. However, these providers typically rely on aviation-focused software partners to address regulatory, operational, and safety requirements unique to the sector.

Aviation software specialists play a central role in the ecosystem. These vendors deliver cloud-native applications for flight operations, maintenance, crew management, and passenger services. Their competitive advantage lies in deep industry knowledge, certification experience, and long-standing relationships with aviation authorities. Software-as-a-service delivery models support recurring revenue and customer retention.

Emerging players focus on analytics, artificial intelligence, and data integration. They target specific operational pain points such as disruption management, predictive maintenance, and passenger experience optimization. While their scale remains limited, they influence innovation and accelerate digital adoption.

Strategic partnerships are a defining competitive strategy. Vendors collaborate with cloud providers, aircraft manufacturers, and system integrators to deliver end-to-end solutions. Competitive success increasingly depends on ecosystem alignment, security credibility, and the ability to support mission-critical aviation operations, shaping long-term aviation cloud market growth.

TOP AVIATION CLOUD COMPANIES PROFILED:

- Amazon Web Services, Inc. (U.S.)

- Microsoft Corporation – Azure (U.S.)

- IBM Cloud (U.S.)

- Accenture plc (Ireland)

- Salesforce, Inc. (U.S.)

- Google LLC (U.S.)

- SITA (Switzerland)

- Collins Aerospace, a Raytheon Technologies Company (U.S.)

- Oracle Corporation (U.S.)

- Amadeus IT Group (Spain)

Latest Aviation Cloud Industry Developments:

- July 2025: Accenture and Google Cloud were selected by Air France-KLM to build a generative AI factory aimed at accelerating scalable AI adoption on the cloud.

- June 2025: TCS signed a seven-year deal with Virgin Atlantic to modernize its core systems using AI and cloud platforms, enhancing agility and scalability.

- August 2024: Lufthansa Systems partnered with Google Cloud to expand its Global Aviation Cloud into a multi-cloud platform, building on its existing support with Microsoft Azure.

- October 2024: Adani Airport Holdings Ltd partnered with Thales to deploy the Fly to Gate biometric cloud solution and an Airport Operations Control Centre across its airports in India.

- November 2023: Qatar Airways partnered with Google Cloud to use AI, machine learning, and data analytics for personalized passenger services. The collaboration would help analyze vast structured and unstructured data to improve travel experiences and optimize airline and airport operations.

REPORT COVERAGE

The global aviation cloud market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 13.96% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type · Private Cloud · Public Cloud · Hybrid Cloud |

|

By Architecture · SaaS (Software as a Service) · PaaS (Platform as a Service) · IaaS (Infrastructure as a Service) |

|

|

By End User · Airlines · Airports · Aircraft Manufacturers |

|

|

By Application · Flight Operations & Scheduling · Aircraft Maintenance & Engineering · Passenger Services & Customer Experience · Crew Management & Training · Others |

|

|

By Geography · North America (By Type, Architecture, End User, Application, and Country) o U.S. o Canada · Europe (By Type, Architecture, End User, Application, and Country) o Germany o U.K. o France o Russia o Rest of Europe · Asia Pacific (By Type, Architecture, End User, Application, and Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Latin America (By Type, Architecture, End User, Application, and Country) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Type, Architecture, End User, Application, and Country) o UAE o Saudi Arabia o Egypt o South Africa · Rest of Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.67 billion in 2026 and is projected to reach USD 24.67 billion by 2034.

In 2025, the market value stood at USD 2.84 billion.

The market is expected to exhibit a CAGR of 13.96% during the forecast period of 2026-2034.

The public cloud segment led the market by type.

The key factors driving the market are an increase in demand for digital modernization and operational efficiency.

Amazon Web Services, Inc. (U.S.), Microsoft Corporation Azure (U.S.), IBM Cloud (U.S.), Accenture plc (Ireland) are some of the prominent players in the market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us