Aviation Emission Control Market Size, Share & Industry Analysis, By Operations (Flight Operations and Airport Operations), By Emission Type (Scope 1 Emissions, Scope 2 Emissions, and Scope 3 Emissions), By Type (CO2 Emissions and Non-CO2 Emissions) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

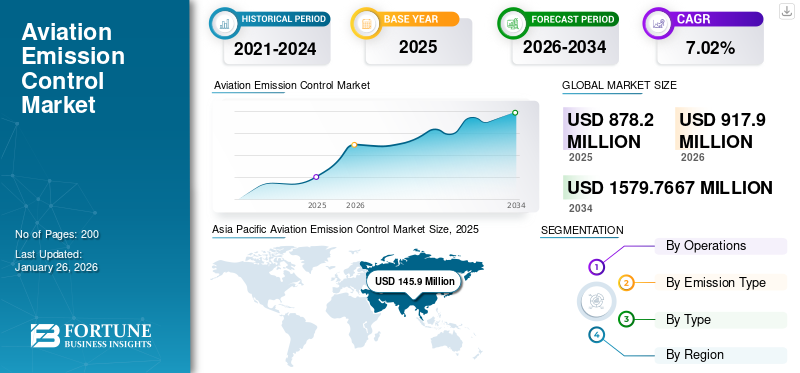

The global aviation emission control market size was valued at USD 878.2 million in 2025 and is projected to grow from USD 917.9 million in 2026 to USD 1579.7667 million by 2034, exhibiting a CAGR of 7.02% during the forecast period. Asia Pacific dominated the aviation emission control market with a market share of 16.61% in 2025.

The aviation emission control market refers to the sector focused on technologies, regulations, and strategies aimed at reducing carbon emissions, specifically from the aviation industry. This market is gaining greater attention due to the growing global emphasis on sustainability and compliance with international agreements, such as the Paris Accord, as well as stricter emissions regulations imposed by organizations, such as the International Civil Aviation Organization (ICAO).

Issues about the environmental impact of the aviation sector influence the market. A report from the ICAO indicated that in 2023, air traffic emissions represented 2.5% of the total radiative forces caused by human activities. Such reports propel research forward, thereby promoting market expansion. A significant hindrance to market growth is the higher funding required for researching and developing new technologies and techniques aimed at decreasing aviation emissions.

Industries globally faced significant challenges as a result of the COVID-19 pandemic. Since its beginning in the early weeks of 2020, the pandemic constrained numerous nations to implement nationwide lockdowns, resulting in a significant drop in manufacturing and leading to disruptions in supply chains. The aviation sector was among the most severely affected industries. Due to the travel restrictions imposed, airlines found themselves without any passengers or cargo to carry, necessitating the grounding of nearly their entire fleet. This action influenced the regulation of aviation emissions in the market. As the need for new aircraft reduced and the current production was put on hold, the necessity for alternative fuels also experienced a significant drop. Moreover, the market research was delayed as a result of the pandemic, and several large companies were experiencing financial difficulties. In general, the COVID-19 pandemic had a detrimental effect on the market.

Download Free sample to learn more about this report.

Aviation Emission Control Market Overview & Key Metrics

Market Size & Forecast

- 2025 Market Size: USD 878.2 million

- 2026 Market Size: USD 917.9 million

- 2034 Forecast Market Size: USD 1579.7667 million

- CAGR: 7.02% from 2026–2034

Market Share

- Asia Pacific dominated the aviation emission control market with a 16.61% share in 2025, driven by rapid air traffic growth, rising adoption of sustainable aviation initiatives, and government programs promoting alternative fuels and low-emission technologies.

- By emission type, Scope 3 emissions accounted for the largest market share in 2024, as airlines and stakeholders intensify efforts to address indirect emissions across the aviation value chain to meet global net-zero targets by 2050.

Key Country Highlights

- United States: Leading in sustainable aviation fuel (SAF) initiatives with tax credits under the Inflation Reduction Act and significant investments in hydrogen-powered aircraft research and electric propulsion technologies.

- France & U.K.: European Green Deal and ReFuelEU initiatives driving SAF mandates and emission reduction frameworks; Airbus and Rolls-Royce are key players advancing hybrid-electric aircraft and carbon reduction systems.

- China & India: Fastest-growing aviation markets, expanding fleets, and increasing regulatory pressure to align with ICAO emissions standards; strong government-backed programs to develop cleaner propulsion technologies.

- UAE & Middle East: Airlines such as Emirates and Etihad adopting biofuel and SAF pilot programs; modernization of airport infrastructure to support greener operations.

AVIATION EMISSION CONTROL MARKET TRENDS

Emergence of Sustainable Aviation Fuel (SAF) for Aircraft is a Growing Trend in the Market

The aviation emissions control market is undergoing a significant transformation driven by increasing regulatory pressures, technological advancements, and shifting consumer preferences toward sustainability. One of the key strategies for emission reduction includes the adoption of sustainable aviation fuels (SAFs), which are crucial for decarbonizing the aviation sector. Despite SAFs currently representing less than 0.1% of total aviation fuel consumption, initiatives such as the U.S. Inflation Reduction Act and the EU's ReFuelEU regulation aim to significantly increase their usage by providing financial incentives and regulatory frameworks.

- For instance, the U.S. has introduced a USD 1.75 per gallon credit for SAF production, while the EU mandates minimum SAF blend-in shares through 2050. However, challenges remain as current SAF production capacities are insufficient to meet anticipated demand; projections suggest that existing and planned SAF projects will only satisfy about 2-4% of jet fuel needs by 2030.

- Asia Pacific witnessed aviation emission control market growth from USD 129.9 Million in 2023 to USD 137.6 Million in 2024.

In addition to SAFs, innovations in aircraft design and engine efficiency are critical aspects of the emissions control strategy. The market is witnessing increased investment in electric and hybrid aircraft technologies, which promise to reduce reliance on traditional fossil fuels. Furthermore, optimization of flight operations through Artificial Intelligence (AI) and big data analytics is emerging as a significant avenue for reducing fuel consumption and emissions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Opportunities

Advancements in Electric and Hydrogen-Powered Aircraft Technology Present Substantial Opportunities

Advancements in electric and hydrogen-powered aircraft technology are transforming the aviation industry, offering significant opportunities for reducing emissions and improving operational efficiency. Below are key developments:

Fuel Cell Technology: Hydrogen fuel cells produce electricity via electrochemical reactions, emitting only water vapor as a byproduct. Advances in high-temperature fuel cells reduce system weight and complexity, enhancing payload capacity and range.

Liquid Hydrogen Storage: Liquid hydrogen offers higher volumetric energy density compared to gaseous hydrogen, addressing space constraints in aircraft designs. Novel heat exchangers optimize fuel consumption by leveraging hydrogen's low storage temperature to improve engine efficiency.

Applications Across Flight Ranges: Hydrogen combustion engines are being explored for long-haul flights, while fuel cells are suitable for mid-range distances.

MARKET DRIVERS

Environmental Concerns, Regulatory Pressures, and Technological Advancements in Aviation Industry to Stimulate Market Expansion

The aviation emission control market growth is experiencing significant growth driven by a combination of environmental concerns, regulatory pressures, and technological advancements. This sector focuses on reducing the pollutants emitted from aircraft engines, which are a major contributor to global greenhouse gas emissions.

The aviation industry is under increasing inspection due to its substantial contribution to global emissions. In 2022, aviation accounted for approximately 2% of global energy-related CO₂ emissions, with projections indicating that this figure could rise significantly without intervention. The ICAO has highlighted that air traffic emissions were responsible for about 2% of total radiative forcing from human activities as early as 2023, underscoring the urgent need for emission control measures. As awareness of climate change grows, both consumers and regulators are demanding more sustainable practices from airlines.

Governments worldwide are implementing stricter regulations aimed at reducing aviation emissions. These include commitments under international agreements, such as the Paris Agreement, which compel nations to lower their carbon footprints. The establishment of incentives, such as the USD 1.75 per gallon SAF credit in the U.S., aims to encourage the adoption of cleaner fuels. These regulatory frameworks create a conducive environment for innovation and investment in emission control technologies.

Innovations in aerospace technologies play a critical role in the market. The development of alternative fuels—such as bio-jet fuel, hydrogen, and ammonia—aims to replace conventional jet fuels that contribute heavily to carbon emissions. Additionally, advancements in aircraft design and operational procedures are enhancing fuel efficiency and reducing overall emissions. For instance, replacing older aircraft with newer models that utilize advanced materials and designs can significantly lower emissions per flight.

MARKET RESTRAINTS

High Research and Development (R&D) Costs and Regulatory Complexities to Hinder Market Expansion

Developing innovative technologies and alternative fuels to reduce aviation emissions requires substantial financial investment. The costs associated with R&D include the development of new technologies and complex certification processes, which can be lengthy and expensive.

For instance, the incremental costs of implementing emission control technologies in aircraft engines can be considerable, encompassing both non-recurring production costs (such as development and initial production) and recurring production costs (related to manufacturing and materials). This financial burden can deter investment in necessary innovations, slowing the transition to more sustainable aviation practices.

The aviation sector is heavily regulated, with stringent international standards set by organizations, including the ICAO. These regulations are often complex and require extensive coordination among various stakeholders, including airlines, manufacturers, and environmental groups. The process of reaching a consensus on emissions standards can be time-consuming, leading to delays in implementing new regulations. Additionally, the evolving nature of these regulations allows companies to frequently adapt their strategies, which adds another layer of complexity and cost to compliance efforts.

SEGMENTATION ANALYSIS

By Operations

Technological Advancements and Government Initiatives in Green Propulsion Boosting the Growth of Flight Operations Segment

Based on the operations, the market is segmented into flight operations and airport operations.

The flight operations segment is anticipated to dominate the market with a share of 78.16% in 2026 and be the fastest-expanding segment throughout the forecast duration. The growth of this segment is attributed to technological advancements and government initiatives. Investment in research and development of green propulsion technologies such as hydrogen and electric propulsion is expected to grow in the next decade, with the aim of maintaining sustainable flight operations. Agreements such as the MoU between Airbus and the Japanese government are in place to develop hydrogen adoption in the aviation sector, including infrastructure for hydrogen use in flight and airport operations.

The demand for airport operations segment in the market is driven by the need for sustainability, technological innovation, and regulatory compliance. However, challenges such as high costs and slow technological advancements must be addressed to utilize these opportunities. The integration of advanced technologies, such as automation, IoT, and predictive analytics, helps airports optimize operations, reduce emissions, and enhance passenger experience.

By Emission Type

Growing Need to Meet Net Zero Emissions by the Aviation Industry has boosted the Scope 3 Emission Segment Growth

By emission type, the market is segmented into scope 1 emissions, scope 2 emissions, and scope 3 emissions.

The scope 3 emissions segment is expected to contribute the largest share of 64.45% to the aviation emission control market in 2026. The market is driven by factors such as stringent environmental regulations, rising fuel costs, and a growing preference for sustainable travel options. Addressing scope 3 emissions is critical for the aviation industry to meet its net zero emissions by 2050 target set by the International Energy Agency and Federal Aviation Administration. Successfully reducing these emissions requires the cooperation of various stakeholders, each of these having its own goals and climate targets.

- The scope 2 emissions segment is expected to hold a 18.54% share in 2024.

Scope 1 emission segment had the highest growth rate during the forecast period. Scope 1 emissions refer to direct greenhouse gas emissions from sources owned or controlled by an organization, such as fuel combustion in manufacturing or company vehicles. In aviation, the majority of scope 1 emissions come from the combustion of jet fuel. Airlines, airports, and manufacturers are the primary end-users in this market. Significant opportunities lie in the development and commercialization of sustainable aviation fuels (SAFs) and innovations in electric and hybrid aircraft technology. Optimizing flight operations using AI and big data could present significant advantages in reducing fuel consumption and carbon emissions.

To know how our report can help streamline your business, Speak to Analyst

By Type

Increasing Demand For Medium-Haul And Short-Haul Flights to Boost CO2 Emissions Segment Growth

The market has been segmented into CO2 emissions and non-CO2 emissions, based on type.

In 2026, the CO2 segment is projected to lead the market with a 78.08% share and is experiencing the highest CAGR during the forecast period. The increasing demand for medium-haul and short-haul flights drives the demand for CO2 emissions control in the market. Narrowbody medium-haul flight operations and widebody long-haul emissions highly contribute to global aviation emissions from commercial flights. They are vital for global connectivity and contribute significantly to the aviation industry's revenue from commercial flights.

The demand for addressing non-CO2 emissions in the market is increasing due to growing concerns about its impact on climate change. Non-CO2 emissions, including nitrogen oxides (NOx), water vapor, particulate matter, and contrails, contribute substantially to global warming, with some estimates suggesting that the total climate impact of aviation is two to four times higher than its CO2 emissions.

Aviation Emission Market Regional Outlook

The global aviation emission control market is divided into North America, Europe, Asia Pacific, and the Rest of the World, based on region.

North America

Asia Pacific Aviation Emission Control Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America contributed approximately USD 392 million to the global market in 2025, accounting for 44.64% share, and is expected to reach USD 408.9 million in 2026. The North American market is projected to maintain a strong presence due to stringent environmental regulations and the adoption of advanced emission control technologies. The U.S. is a major contributor, with significant investments in sustainable aviation fuels and emission reduction technologies across the country. The U.S. market is projected to reach USD 347.9 million by 2026.

Europe

In 2025, the Europe market stood at USD 186.7 million, representing 21.26% of global demand, and is projected to grow to USD 194.5 million in 2026. Europe is a leading region in the aviation emissions control market, with countries including Germany, France, and the U.K. spearheading initiatives for emissions reduction. The European Union's Green Deal and other regulations are pushing for substantial reductions in aviation emissions, contributing to market growth. The UK market is projected to reach USD 68.7 million by 2026, while the Germany market is projected to reach USD 48 million by 2026.

Asia Pacific

The Asia Pacific region is the fastest growing in the market with highest CAGR, fueled by increasing air travel demand and government initiatives aimed at sustainability. Countries such as China, India, and Japan are focusing on enhancing their aviation infrastructure with cleaner technologies. The Asia Pacific region captured 16.61% of the global market in 2025, generating USD 145.9 million in revenue, and is projected to reach USD 153.6 million in 2026. The Japan market is projected to reach USD 45 million by 2026, the China market is projected to reach USD 42 million by 2026, and the India market is projected to reach USD 45.4 million by 2026.

Rest of the world

In 2025, Rest of the World represented USD 153.6 million, accounting for 17.49% of the worldwide market, and is projected to grow to USD 160.9 million in 2026. In the Rest of the world region, the Middle East & Africa region has an emerging market for aviation emissions control, with investments in modernizing airport facilities and fleet upgrades to comply with international standards. Countries, including the UAE, are taking proactive measures to reduce aviation emissions. Latin America is gradually recognizing the importance of emission control in aviation, with Brazil and Mexico leading efforts to implement cleaner technologies and practices in their aviation sectors.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Prominent Market Players Are Aiming To Adopt Alternative Fuels To Reduce Greenhouse Emissions

The aviation emissions control market includes aircraft manufacturers, subsystem manufacturers, and airline operators. Key players include Airbus SE, Embraer S.A., General Electric Company, and others. These companies are developing innovative profiles and technologies aimed at reducing greenhouse gas emissions from aircraft and related activities, including the adoption of alternative fuels and improvements to aircraft design and engine efficiency. Most of these participants are involved in partnerships and collaborations across other industries to distribute research costs and expedite technological advancements.

LIST OF KEY AVIATION EMISSION CONTROL COMPANIES PROFILED

- Rolls-Royce PLC (U.K.)

- Pratt & Whitney (RTX Corporation) (U.S.)

- Safran S.A. (France)

- Airbus SE (France)

- Textron Aviation Inc. (U.S.)

- British Airways (U.K.)

- Embraer S.A (Brazil)

- General Electric Company (GE Aerospace) (U.S.)

- Gulfstream Aerospace Corporation (U.S.)

- Air Canada (Canada)

KEY INDUSTRY DEVELOPMENTS

- October 2024 – DHL Express and DHL Global Forwarding are advancing their sustainability goals through a contract renewal with IAG Cargo, the cargo handling division of International Airlines Group (IAG), to use an additional 60 million liters of Sustainable Aviation Fuel (SAF) on behalf of DHL. The new contract covers 2024 and 2025 emissions and will result in a reduction of greenhouse gas emissions of approximately 165,000 metric tons of CO2e.

- October 2024 – California has achieved a groundbreaking agreement with the top passenger and cargo airlines in the country to significantly speed up the adoption of sustainable aviation fuel for flights operating within the state. In a statement issued by the California Air Resources Board (CARB) and Airlines for America (A4A), an industry trade group that represents nearly ten major airlines, pledged to raise the supply of sustainable aviation fuel (SAF) in California to 200 million gallons by 2035, which would account for roughly 40% of intrastate travel demand—a more than tenfold rise from present levels.

- September 2024 – TotalEnergies and Air France-KLM have reached an agreement for TotalEnergies to deliver as much as 1.5 million tons of more sustainable aviation fuel (SAF) to Air France-KLM Group airlines over the next 10 years through 2035. This contract represents one of the biggest SAF purchase agreements made by Air France-KLM so far. In both 2022 and 2023, Air France-KLM was the top SAF consumer globally, accounting for 17% and 16% of worldwide production, respectively

- July 2024 – HIF Global has declared the signing of a Memorandum of Understanding with Airbus to promote the worldwide advancement of e-fuels for aviation ("e-Sustainable Aviation Fuel" or "e-SAF") through the methanol to jet fuel ("MTJ") route. The MoU establishes a structure for negotiating final agreements concerning four essential workstreams: technical, project development, commercial, and advocacy.

- February 2024 – Airbus and TotalEnergies have established a strategic alliance to address the challenges of decarbonizing aviation through sustainable aviation fuel. Aligned with the goal of reaching net carbon neutrality in aviation by 2050, this collaboration seeks to aid in decreasing the sector's CO2 emissions, where Sustainable Aviation Fuels (SAF) are essential. SAF provided by TotalEnergies can decrease CO2 emissions by up to 90% over its lifecycle when compared to equivalent fossil fuels

REPORT COVERAGE

The research report delivers an in-depth market analysis, which focuses on technologies aimed at reducing greenhouse gas emissions from aviation activities, driven by increasing environmental regulations and the demand for sustainable travel options. Key opportunities lie in the development of sustainable aviation fuels (SAFs) and innovations in electric aircraft. However, challenges include high R&D costs and regulatory hurdles that may impede progress.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.02 % from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Operations

|

|

By Emission Type

|

|

|

By Type

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market size was USD 878.2 million in 2025 and is anticipated to reach USD 1579.7667 million by 2034.

Registering a CAGR of 7.02%, the market will exhibit steady growth over the forecast period.

During the forecast period, the flight operations segment will likely be the fastest-growing segment in this market.

North America dominated the market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us