Aviation Insurance Market Size, Share & Industry Analysis by Type (Hull and Liability Insurance, Loss of License Insurance, Passenger Legal Liability Insurance, and Others), By Distribution Channel (Brokers, Direct, Digital, and Others), By End User (Airlines, Aerospace, General Aviation, and Others), and Regional Forecast, 2026-2034

Aviation Insurance Market Size

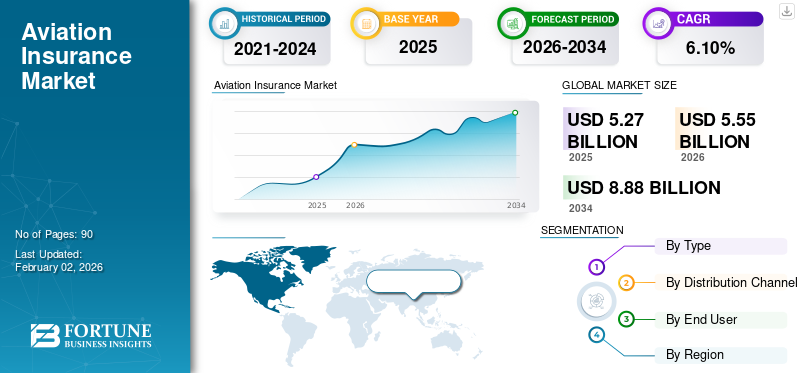

The global aviation insurance market size was valued at USD 5.27 billion in 2025. The market is projected to grow from USD 5.55 billion in 2026 to USD 8.88 billion by 2034, exhibiting a CAGR of 6.10% during the forecast period. North America dominated the aviation insurance market with a market share of 44.90% in 2025.

Aviation insurance services provide coverage for passengers, aircraft, crew, and third-party liabilities and upkeep operators against financial losses arising from damage, accidents, or operational disruptions. Aviation insurers team up with general aviation operators, airlines, and aerospace manufacturers to support risks related to hull damage, passenger liability, war and terrorism, and loss of license.

Increasing air traffic volumes, heightened regulatory compliance requirements, and fleet expansion are driving service adoption. The market is also expanding with the rising requirement for customized risk solutions for developing technologies such as urban air mobility (UAM) platforms, unmanned aerial vehicles, and sustainable aviation fuel programs.

Major companies in the market, including Allianz Global Corporate & Specialty (AGCS), AXA XL, Global Aerospace, Starr Companies, Tokio Marine HCC, and Swiss Re, are following capacity expansions, strategic partnerships, and digital innovation to support client reach and underwriting efficiency.

Download Free sample to learn more about this report.

Aviation Insurance Market Key Takeaways

- 2025 Market Size: USD 5.27 billion

- 2026 Market Size: USD 5.55 billion

- 2034 Forecast Market Size: USD 8.88 billion

- CAGR: 6.10% from 2026–2034

- North America dominated the aviation insurance market with a 44.90% share in 2025.

- The hull and liability insurance segment accounted for the largest market share of 64.14% in 2026.

- The brokers segment is projected to hold a 75.68% share in 2026.

North America

North America held 44.90% share in 2025, valued at USD 2.37 billion.

Asia Pacific

Asia Pacific market valued at USD 1.09 billion in 2025.

Europe

Europe market valued at USD 1.27 billion in 2025.

U.S.

The market in the U.S. is projected to reach USD 1.74 billion by 2026.

Japan

The market in Japan is projected to reach USD 0.09 billion by 2026.

Read More

MARKET DYNAMICS

Market Drivers

Rising Air Traffic and Fleet Expansion to Drive the Expansion of the Market

Increasing air traffic and fleet expansion act as twin engines, bolstering aviation insurance market growth. As cargo and passengers are increasing globally, airlines are adding flights, routes, and larger aircraft that increases the value at risk on each aircraft and the number of flight hours to be insured. This means insurers support hull exposure and higher liability exposure as routes multiply and networks densify. For instance,

- In June 2023, IndiGo’s record order for 500 A320neo-family aircraft magnified the narrow-body fleet for the next decade, lifting both liability and hull demand.

- In June 2025, Riyadh Air placed firm orders for 25 A350-1000s (with purchase rights for 25 more) and up to 72 Boeing 787-9s.

In conclusion, a rise in global air traffic with the continuous modernization and expansion of aircraft fleets is primarily uplifting both the volume and value of insurable aviation assets, thereby driving the constant growth of the market.

Market Restraints

Reinsurance Capacity and High Volatility in Premium Cycles to Restrict the Market Growth

The aviation insurance market faces significant challenges due to limited reinsurance capacity and high volatility in premium cycles, which together act as major restraints on sustainable growth. The industry functions in a cyclical environment, where large-scale losses stemming from natural disasters, aircraft accidents, or geopolitical events trigger reductions in underwriting capacity and sharp increases in reinsurance rates.

- For instance, the aftermath of the Russia-Ukraine conflict resulted in billions of dollars in potential aviation losses linked to stranded leased aircraft, prompting reinsurers to tighten terms and advance premiums across liability, hull, and war-risk segments.

Thus, such hard market conditions result in pricing declines and margin compression.

Market Opportunities

Growth in Sustainable Aviation Fuel (SAF) Adoption to Create Major Market Opportunity in Coming Years

As aircraft operators shifting toward greener operations to meet net-zero carbon emission targets, the integration of SAF into general aviation fleets leads new operational, technical, and financial risks that need specialized insurance coverage. SAF usage affects multiple parts of the value chain from transportation to fuel production and to aircraft engine performance and certification compliance, generating a need for policy to address potential liabilities such as supply-chain disruptions, fuel quality issues, and infrastructure adaptation at airports. For instance,

- As per an IATA study, there is enough SAF feedstock available for airlines to achieve net zero CO2 emissions by 2050, using sources that meet strict sustainability criteria and do not cause land use changes.

This shift will support the aviation sector’s decarbonization journey with profitability and sustainability.

Aviation Insurance Market Trends

Integration of Data Analytics and AI in Underwriting is a Significant Market Trend

Traditionally, underwriting in aviation is dependent heavily on manual risk assessments, historical loss data, and limited visibility into complete aircraft performance. Insurers are progressively using AI-driven telematics, predictive models, and data analytics platforms to optimize premium pricing, boost risk evaluation accuracy, and develop claims forecasting. Modern aircraft produces vast amounts of operational data ranging from engine telemetry and flight hours to weather patterns and maintenance cycles, which are analyzed through AI algorithms. For instance,

- In April 2024, insurers such as Global Aerospace and Allianz Global Corporate & Specialty (AGCS) started integrating digital platforms for pilot behavior, real-time monitoring, and maintenance trends. This allows companies to adjust coverage pricing and terms.

Such a data-centric approach helps maintenance lapses, identify high-risk flight routes, and operational anomalies that can expect potential claims.

SEGMENTATION ANALYSIS

By Type

Complete Coverage of Third-Party Liabilities accelerated the Hull and Liability Insurance Segment Growth

Based on type, the market is divided into a hull and liability insurance, loss of license insurance, passenger legal liability insurance, and others (aircraft war and peril insurance).

The hull and liability insurance segment is expected to capture the largest aviation insurance market share of 64.14% in 2026. owing to its complete coverage of third-party liabilities and high-value aircraft assets. The rise in global fleet modernization programs, aircraft deliveries, and increasing aircraft replacement costs expressively amplified hull values and exposure levels, compelling operators and lessors to maintain extensive insurance coverage. Moreover, the rising complexity of international air routes and regulatory mandates under ICAO and regional aviation authorities (such as FAA and EASA) have reinforced the demand for high-limit liability policies, principally among major cargo operators and commercial airlines.

The passenger legal liability insurance segment is anticipated to grow at the highest CAGR of 8.4% during the forecast period. This is owing to a rapid increase in passenger traffic, growing compensation frameworks, and firmer safety regulations across global markets.

By Distribution Channel

Rising Global Network Reach to Boost the Brokers Segment Growth

Based on distribution channel, the market is divided into brokers, direct, digital, and others.

The brokers segment is expected to account for the largest share of 75.68% in 2026. owing to its global network reach, specialized expertise, and major role in structuring complex risk placements for lessors, airlines, and aerospace manufacturers. Aviation insurance includes multi-layered and highly technical coverages such as liability, hull, war-risk, and product liability that often need policy wording and coordination with international reinsurers. Major global brokerage firms such as Aon, Marsh, WTW, Lockton, and Gallagher dominate this space, leveraging their long-standing relationships with underwriters at Swiss Re, Lloyd’s, and Munich Re providing risk advisory services and negotiate competitive terms.

The direct distribution channel segment is anticipated to grow at the highest CAGR of 8.7% during the forecast period. This surge is driven by the growing digitalization of underwriting, general aviation coverage, rising demand for small-scale, and regulatory encouragement of localized risk placement.

By End User

Airlines Segment to Grow with the Higher Demand for Aviation Insurance Solutions

Based on end-user, the market is analyzed into airlines, aerospace, general aviation, and others (contingent, government).

The airlines segment is expected to capture the largest aviation insurance market share of 52.79% in 2026. as airlines has extensive operational networks, high-value fleets, and major exposure to cargo and passenger and liabilities. Commercial airlines operate most expensive aircraft such as the Boeing 787, Airbus A350, and A320neo families which requires complete hull and liability insurance to safeguard against operational accidents, damage, and third-party risks. The increase in global air traffic, fleet expansion programs by major carriers including Qatar Airways, Emirates, Turkish Airlines, Air India, Delta, and growing regulatory mandates under ICAO and national aviation authorities have further accelerated insurance requirements.

The general aviation segment is anticipated to grow at the highest CAGR of 8.7% during the forecast period. This is propelled by the increasing number of air taxis, business jets, private aircraft, and unmanned aerial vehicles (UAVs) across emerging and developed economies.

To know how our report can help streamline your business, Speak to Analyst

AVIATION INSURANCE MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

The North America market held a dominant share in 2025, valuing at USD 5.27 billion, and also took the leading share in 2026 with USD 5.55 billion. The growth is primarily driven by the region’s early adoption of advanced aviation technologies and the strong presence of major global insurers and brokers such as AIG, Allianz Global Corporate & Specialty (AGCS), Marsh, AXA XL, Aon, and WTW. The region profits from a highly developed aviation infrastructure, including one of the largest commercial and general aviation fleets, well-established maintenance, repair, and overhaul (MRO) networks, and sophisticated reinsurance mechanisms.

In 2026, the U.S. aviation insurance market is estimated to have reached USD 1.74 billion, driven by rising air traffic volumes and a sustained surge in passenger and cargo activity. According to the Federal Aviation Administration (FAA), domestic passenger enplanements are expected to continue increasing steadily through 2032, reflecting the country’s strong aviation recovery and expanding network capacity.

Download Free sample to learn more about this report.

Europe

In 2025, the Europe market stood at USD 1.27 billion, representing 24.00% of global demand, and is projected to grow to USD 1.32 billion in 2026. which is the second highest amongst all the regions and touch the valuation of USD 1.27 billion in 2025. The market is experiencing rapid growth, fueled by increasing air passenger traffic and strong regulatory oversight under the European Union Aviation Safety Agency (EASA). Major carriers such as Air France-KLM, Lufthansa, Ryanair, and British Airways are upgrading and escalating their fleets with next-generation aircraft such as the A350 and Airbus A320neo, motivating hull values and insurance coverage needs.

The region has mature markets such as the U.K. with high-growth opportunities in insurance sector. Backed by these factors, countries including the U.K., Germany, and France are anticipated to record the valuation of USD 0.3 billion, USD 0.25 billion in 2026, and USD 0.20 billion in 2025.

Asia Pacific

The Asia Pacific region captured 20.60% of the global market in 2025, generating USD 1.09 billion in revenue, and is projected to reach USD 1.16 billion in 2026. and secure the position of the third-largest region in the global market. In the region, India and China both are estimated to reach USD 0.24 billion and USD 0.35 billion respectively in 2025. A sharp rise in general aviation, business jets, pilot training schools, and UAV operations is expanding the insurance demand beyond commercial airlines. Governments and regulators, such as India’s DGCA and Civil Aviation Administration of China (CAAC), are enforcing stricter safety and liability mandates, further expanding insurance penetration.

South America

Over the forecast period, South America is expected to witness moderate growth in the global market, reaching a valuation of USD 0.19 billion in 2025. The market is supported by gradual fleet modernization, steady recovery in air traffic, and increasing insurance awareness among regional carriers. However, growth remains influenced by ongoing geopolitical and economic challenges across the region.

Middle East & Africa

In 2025, Middle East & Africa generated USD 0.37 billion, contributing 6.90% to global market revenue, and is projected to grow to USD 0.38 billion in 2026. The Middle East & Africa market is also projected to grow moderately, with the GCC region expected to reach USD 0.18 billion in 2025. Growth is driven by active fleet expansion programs from major airlines such as Emirates, Qatar Airways, Etihad Airways, and Saudia, along with the emergence of new carriers like Riyadh Air.

COMPETITIVE LANDSCAPE

Key Industry Players:

Rising AI-Driven Underwriting, Digital Transformation, and Strategic Partnerships by Key Players to Propel the Market Growth

Prominent players in the market are focusing on AI-driven underwriting, digital transformation, and strategic partnerships to enhance risk assessment accuracy and operational efficiency. Companies such as Allianz, AXA XL, Starr, EAA Company and Global Aerospace are investing in predictive analytics and automation to streamline claims and improve pricing models.

Long List of Aviation Insurance Companies Studied:

- AXA XL (U.S.)

- Travers & Associates Aviation Insurance Agency, LLC (U.S.)

- USAIG (U.S.)

- Starr International Company, Inc (U.S.)

- Global Aerospace, Inc. (U.S.)

- EAA Company Ltd (U.S.)

- Tokio Marine HCC (U.S.)

- BWI Aviation Insurance (U.S.)

- American International Group, Inc (U.S.)

- Chubb (Switzerland)

- Munich Re Specialty (Germany)

- Swiss RE (Switzerland)

- HDI Global (Germany)

- Beazley (U.K.)

- Hallmark Financial Services (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In October 2025, Chubb launched Travel Pro, a new suite of travel insurance products designed to address the most common challenges faced by global travelers. Travel Pro streamlines travel insurance and offers peace of mind by mitigating disruptions such as baggage issues and flight delays, medical emergencies, and unpredictable weather.

- In September 2025, 5x5 Aviation Insurance introduced a data-driven, pilot-focused, direct-to-customer insurance platform. The platform has been designed specifically for aircraft owners and pilots, offering personalized coverage based on real operational insights and flying behavior.

- In July 2025, TITAN Aerospace Insurance (TAI) partnered with an A rated insurance provider to offer an exclusive general liability insurance program for TITAN-branded FBOs. This program provides deep expertise in insurance and aviation to offer significant value beyond traditional coverage, providing both cost savings and operational advantages.

- In June 2025, Skyward Specialty Insurance Group, Inc. launched a new aviation underwriting unit, announcing its entry into the specialized aviation industry. The expansion follows the company’s takeover of the assets of Acceleration Aviation Underwriters.

- In December 2024, Redline Underwriting launched a General Aviation Insurance solution, developed in collaboration with Allianz Commercial from their U.K. region. This solution is designed explicitly for the Caribbean and Latin American markets.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ARRTIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.10% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Distribution Channel

By End User

By Region

|

|

Companies Profiled in the Report |

|

Frequently Asked Questions

According to Fortune Business Insights, the market is projected to reach USD 8.88 billion by 2034.

In 2025, the market was valued at USD 5.27 billion.

The market is projected to grow at a CAGR of 6.10% during the forecast period.

By type, the hull and liability insurance segment led the market in 2026.

Rise in air traffic and fleet expansion are key factors driving the growth of the market.

AXA XL, Travers & Associates Aviation Insurance Agency, LLC, and USAIG are the top players in the market.

North America held the highest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 90

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us