Banking as a Service Market Size, Share & Industry Analysis, By Service (Core Banking & Account, Payment & Transfers, Card Issuing & Processing, Lending & Credit, and Others), By Deployment (Public Cloud and Private Cloud), By Industry (E-Commerce & Marketplace, Mobility & Gig Economy, Retail, Travel & Transportation, Healthcare, and Others), and Regional Forecast, 2026-2034

BANKING AS A SERVICE MARKET SIZE AND FUTURE OUTLOOK

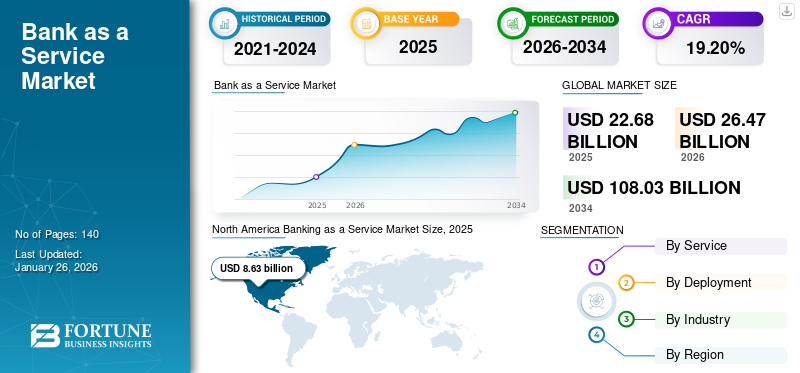

The global banking as a service market size was valued at USD 22.68 billion in 2025. The market is projected to grow from USD 26.47 billion in 2026 to USD 108.03 billion by 2034, exhibiting a CAGR of 19.20% during the forecast period. North America dominated the global market with a share of 38.10% in 2025.

Banking as a Service is a business model where different licensed financial institutions outsource their banking infrastructure as well regulated services to a third party company. It allows non-banking companies to provide financial products and services by integrating it with licensed banks and fintech via APIs.

The market is growing steadily through rapid digital shift, growing need for embedded finance, open banking regulations and demand for cost-effective solutions. Consumers are opting for personalized and integrated financial products, leading to a rapid market growth.

Key players are adopting strategies including partnerships between fintech firms and banks, global expansion to gain emerging markets, investments in advanced technologies including AP platforms and others to sustain the market competition. Few well known players include Tookitaki Holding Pte. Ltd, Finastra, Marqueta, Stripe, Inc., Solaris SE, and Mambu.

Download Free sample to learn more about this report.

Global Banking As A Service Market Takeaways

- 2025 Market Size: USD 22.68 billion

- 2026 Market Size: USD 26.47 billion

- 2034 Forecast Market Size: USD 108.03 billion

- CAGR: 19.20% from 2026–2034

- North America dominated the banking as a service market with a 38.10% share in 2025.

- The public cloud segment is projected to hold a 78.35% market share in 2026.

- The payment & transfers segment is projected to lead the market with revenue of USD 6.84 billion.

North America

North America generated USD 8.63 billion in 2025 and maintained its leading market position globally.

Europe

Europe contributed USD 6.17 billion in 2025, accounting for 27.20% of the global market, and is projected to reach USD 7.03 billion in 2026.

Asia Pacific

Asia Pacific generated USD 5.47 billion in 2025, representing 24.10% of the global market share, and is expected to reach USD 6.51 billion in 2026.

U.S.

The U.S. banking as a service market is projected to reach USD 8.15 billion by 2026.

Japan

The Japan market is witnessing steady growth due to increasing adoption of cloud-based banking platforms and embedded finance solutions.

Read More

MARKET DYNAMICS

Market Drivers

Lower Customer-Acquisition Costs Through Embedded Channels Drives Market Development

The lower customer acquisition cost (CAC) that is achieved through embedded financial channels is a prominent driver for banking as a service market growth. Through adoption of financial products directly into an existing customers experience including online checkout, gig economy platforms and payroll systems, companies are able to convey engaged users without a huge marketing expenditure. These end-users are highly active and rely on the platforms, thus leading to an increased conversion rates.

Moreover, embedded finance offers access to a valuable first party insights, enabling companies to offer banking (customized) products/services, enhance the customer retention and surge the lifetime value. This results in improved LTV/CAC ratio that helps in sustainable growth, allowing embedded finance an effective strategy for traditional institutions and fintechs adopting the baas model.

Market Restraints

Regulatory Fragmentation and Onboarding/AML Burdens Hampers the Market Growth

One of the major restraint for the market is regulatory fragmentation across various regions. Financial regulations tend to vary based on country, thus creating obstacles for the market players operating globally. Various licensing needs, compliance frameworks, and data protect laws increasing the costs, complexity and limits the scalability.

Moreover, onboarding and Anti-Money Laundering (AML) obligations also pose significant operational burdens. It demands different requirements often reduces the process of customer onboarding, raise operational expenses and increase the administrative workload.

Market Opportunities

Growing Automated Compliance as a Service Offers Lucrative Growth Opportunities

Automated compliance as a service offers a major market opportunity. It addresses company’s regulatory burdens effectively. Automated KYC, transaction monitoring and regulatory reporting APIs tends to streamline compliance processes, thus reducing the manual workload and human error. These technologies allow real time risk management, more accurate audit trails, and faster onboarding thus enhancing trust and operational efficiency for the companies.

With intensification of regulatory inspection, the demand for automated and integrated compliance tools is growth. Banking as a service platform that incorporate such solutions provides seamless and compliant services while reducing the costs and enhancing scalability.

BANKING AS A SERVICE MARKET TRENDS

Rapid Shift to Embedded Finance Via API-First Stacks Has Emerged as a Prominent Market Trend

A crucial trend reshaping the market is a rapid shift toward embedded finance that is enabled by API first architecture. Companies are currently integrating different digital banking services, including lending, payments and digital wallets, directly into its platforms via modular APIs. This dynamically reduces the development time, cutting the product launches duration from months to weeks.

Additionally, seamless integration of different financial features improves the user engagement, convenience, and loyalty, while adding new revenue streams through financial service monetization. With more non-financial companies adopting rooted finance, the need for compliant, scalable, and customizable BaaS solutions increases.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Service

Growth Demand for Payment and Transfer Services Across Different Sectors Boosts Segment Growth

Based on the service, the market is segmented into core banking & account, payment & transfers, card issuing & processing, lending & credit, and others.

In 2026, the payment & transfers segment is projected to lead the market with a 6.84 share and with a revenue of USD 6.84 billion in 2024. The segment also held a highest CAGR of 20.8% in 2024 owing to the higher use of these services across different cases including payouts, remittances, and wallets. These are easy to embed through APIs and need less banking licenses as compared to lending. Other prominent drivers for the segment growth are progress in direct rails including RTP or UPI, payout-heavy platforms ranging from micro-merchant to creator economies and surge in cross border transactions.

By Deployment

Increasing Deployment of API-Native to Drive Public Cloud Segment Growth

The market is divided into public cloud and private cloud, based on deployment.

Among these, the public cloud segment dominated the market with a revenue share of USD 15.05 billion in 2024. The public cloud segment is projected to dominate the market with a share of 78.35% in 2026. It is also growing rapidly with a CAGR of 19.6% in 2024. This growth is attributed to the increasing deployment of API-native and growing demand for compliance tooling. This offers elastic scaling and decreases the total cost versus private or on premise setups. Additionally, the increasing adoption of cloud data or AI services, regulatory comfort with sovereign cloud options and global availability zones.

By Industry

Expansion of Gross Merchandise Volume Augments the E-commerce & Marketplace Segment Growth

Based on the industry, the market is divided into e-commerce & marketplace, mobility & gig economy, retail, travel & transportation, healthcare, and others.

The E-commerce & marketplace segment is expected to lead the market, contributing 29.24% globally in 2026. E-commerce & marketplace segment held the highest market share with a revenue of USD 5.78 billion in 2024. This growth is attributed to the increase in gross merchandise volume demanding escrow, split payouts, KYB at scale and integrated checkout or financing. Additionally, user convenience, operational efficiency and increased revenue generation promotes the segment’s growth.

Consequently, the mobility and gig economy segment held highest CAGR of 23.6% in 2024. This growth is majorly driven by the constant worker payouts, access to instant earning and integration of initiatives including card or wallets into apps.

To know how our report can help streamline your business, Speak to Analyst

BANKING AS A SERVICE MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America Banking as a Service Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America market generated USD 8.63 billion in 2025, representing 38.10% of the global market landscape, and is expected to reach USD 10.26 billion in 2026. This growth is driven by the presence of mature sponsor bank ecosystem across the region. Additionally, increase in card based spending, favorable partnership frameworks and fintech funding majorly across the U.S., contributes to the market growth. The U.S. leads the North American market with an expected revenue share of USD 8.15 billion in 2026.

Europe

Europe contributed 27.20% to the global market in 2025, with a valuation of USD 6.17 billion, and is projected to reach USD 7.03 billion in 2026. This is attributed to the strong regulatory support, widespread fintech adoption and rapid digital transformation. Additionally, the U.K., Germany, and France are few major contributors to the market growth with an expected revenue share of USD 1.48 billion, USD 1.2 billion in 2026, and USD 0.66 billion respectively by 2025.

Asia Pacific

Asia Pacific accounted for USD 5.47 billion in 2025, representing 24.10% of the global market share, and is projected to reach USD 6.51 billion in 2026. This regional growth is due to growing rapid increase in real-time/QR payment rails, super-apps, huge underbanked segments, and pro-digital guidelines in key markets across China, India, Southeast Asia, and Japan. India and China are expected to contribute to a revenue share of USD 1.63 billion and USD 1.66 billion respectively in 2026.

South America and Middle East & Africa

In 2025, Middle East & Africa held 5.80% of the global market, reaching a valuation of USD 1.32 billion, and is projected to grow to USD 1.46 billion in 2026.

South America maintained a strong presence in the global market, reaching USD 1.08 billion in 2025, accounting for 4.80% share, and is expected to reach USD 1.21 billion in 2026.

The markets of South America and Middle East & Africa are growing due to growing fintech ecosystem, rapid digitalization and strong smartphone penetration. Moreover, GCC countries are predicted to have a market share of USD 0.55 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Focus of Key Players on Innovation and New Launches Leads to their Dominating Market Positions

The global banking as a service industry is highly dynamic, showcasing a mix of fintech firms, traditional banks, and technology providers. Key players operating in the market include Tookitaki Holding Pte. LTD, Finastra, Marqueta, Stripe, Inc., Solaris SE, Mambu, and others. These companies offer API driven platforms which allows seamless integration of different financial services.

LIST OF KEY BANKING AS A SERVICE COMPANIES PROFILED:

- Tookitaki Holding Pte. Ltd (Singapore)

- Finastra (U.K.)

- Marqueta (U.S.)

- Stripe, Inc. (Ireland)

- Solaris SE (Germany)

- Mambu (Netherlands)

- OpenPayd (U.K.)

- ClearBank (U.K.)

- Green Dot Corporation (U.S.)

- Weavr (U.K.)

- Wolters Kluwer (Netherlands)

- Advapay (Estonia)

- Oliver Wyman (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In July 2025, Safaricom Ethiopia’s mobile money platform M-Pesa and Awash Bank signed a strategic partnership to roll out digital financial products, starting with an overdraft service that allows customers to complete M-Pesa transactions even when their wallet balance is low.

- In May 2025, Oracle introduced new cloud services aimed at assisting retail financial institutions in modernizing their lending and collections processes. The newly launched Oracle Banking Retail Lending Servicing Cloud Service and Oracle Banking Collections Cloud Service are designed to enhance operational efficiency and risk management for financial organizations.

- In April 2025, Kraken, one of the longest-standing, most liquid and secure cryptocurrency exchanges, announced the launch of Kraken Embed, a new Crypto-as-a-Service (CaaS) solution for neobanks, fintechs, traditional banks to seamlessly provide clients with direct access to cryptocurrency.

- In April 2025, PNC Bank announced its offering of cryptocurrency services to its clients through a newly established partnership with Coinbase, marking a significant move following the recent signing of federal crypto legislation.

- In December 2024, BNP Paribas’ Securities Services business announces the launch of new post-trade data management services, leveraging the Investment Data Solution (IDS) of NeoXam, a market leader in financial data technology solutions, to support clients’ decision-making across the investment value chain.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the Banking as a Service market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 19.20% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Segmentation |

By Service

By Deployment

By Industry

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 26.47 billion in 2026 and is projected to reach USD 108.03 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 19.20% during the forecast period.

Lower customer-acquisition costs through embedded channels growth drives the market growth.

Tookitaki Holding Pte. Ltd, Finastra, Marqueta, Stripe, Inc., Solaris SE, and Mambu are some of the top players in the market.

North America dominated the global market with a share of 38.10% in 2025.

North America was valued at USD 8.63 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us