Barium Carbonate Market Size, Share & Industry Analysis, By Form (Powder and Granular), By Grade (Technical Grade, Industrial Grade, and Others), By Application (Bricks & Tiles, Specialty Glass, Chemical Compounds, Electro-Ceramic Materials {MLCC, Thermistors, and Others}, and Others), and Regional Forecast, 2026-2035

KEY MARKET INSIGHTS

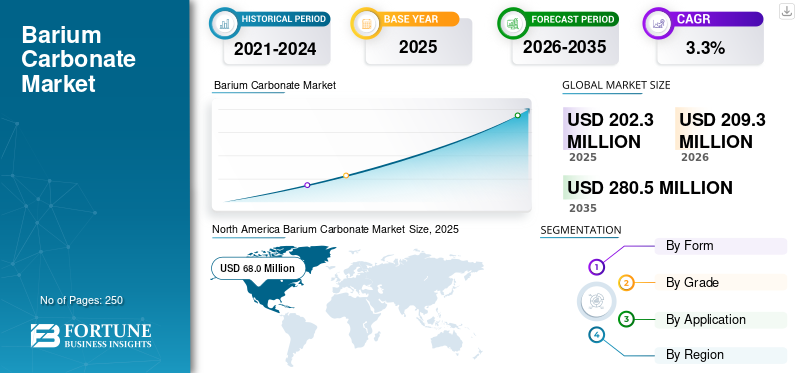

The global barium carbonate market size was valued at USD 202.3 million in 2025. The market is projected to grow from USD 209.3 million in 2026 to USD 280.5 million by 2035 at a CAGR of 3.3% during the forecast period. North America dominated the global barium carbonate market with a market share of 33.61% in 2025.

Barium carbonate (BaCO3) is a white, odorless, crystalline inorganic compound made from barium and carbonate ions. It is mostly insoluble in water and is used as a flux and purifier in ceramics and glazes, specialty glass, and brick or tile bodies to improve strength, brightness, and to prevent efflorescence by converting soluble sulfates into stable barium sulfate. The growth in product demand is supported by rising construction and infrastructure spending that increases brick, tile, and glass output. It is also driven by expanding ceramic sanitary ware and advanced ceramics production and growing electronics and ferrite uses that rely on barium based intermediates. Major operating companies include Solvay, Sakai Chemical Industry, Nippon Chemical Industrial, Hebei Xinji Chemical Group, and Hubei Jingshan Chutian Barium Salt Corporation.

Download Free sample to learn more about this report.

Barium Carbonate Market Key Takeaways

- 2025 Market Size: USD 202.3 million

- 2026 Market Size: USD 209.3 million

- 2035 Forecast Market Size: USD 280.5 million

- CAGR: 3.3% from 2026–2035

- North America dominated the market with a 33.61% share in 2025.

- Technical Grade segment held the largest market share in 2025.

- Bricks & Tiles segment is expected to dominate during the forecast period.

North America

North America led the market with USD 68.0 million in 2025.

Asia Pacific

Asia Pacific is expected to grow significantly, supported by construction and electronics demand.

Europe

Europe witnessed steady demand from specialty glass and technical ceramics.

Latin America

Growth is supported by rising residential construction and ceramic production.

Middle East & Africa

Demand is driven by infrastructure projects, housing programs, and expanding glass and tile manufacturing.

Read More

MARKET DYNAMICS

BARIUM CARBONATE MARKET TRENDS

Rising Electronics & Specialty Glass Demand to Drive a Shift to Higher-Purity (Technical-Grade) Barium Carbonate

The market is shifting toward higher-purity or technical grades as electronics and specialty glass grow faster than traditional bricks and tiles. High-purity BaCO3 is a preferred feedstock for barium titanate and related composite oxides used in MLCC capacitors, PTC thermistors, sensors, and ferrites, where even small traces of iron, alkalis, or sulfates can lower dielectric strength, increase defects, and hurt device reliability. With ongoing miniaturization and higher capacitance requirements, electronic-ceramics makers are tightening purity and particle-size specifications, pushing suppliers to invest in better refining, consistent lot control, and ultra-fine powders. This trend is the strongest in the Asia Pacific region, led by China, Japan, and South Korea, which dominate MLCC and electronic-ceramics manufacturing. Hence, most capacity upgrades and new electronic-grade offerings are concentrated there. Such factors will fuel the barium carbonate market growth during the forecasted timeframe.

MARKET DRIVERS

Growing Construction Activities to Drive Higher BaCO3 Demand in Bricks and Tiles

The surging construction industry is fueling the demand for barium carbonate, as rapid urbanization, rising housing needs, and large infrastructure projects increase the production of bricks, roof tiles, wall tiles, and vitrified flooring. Moreover, builders and end users want cleaner, stain-free surfaces. Hence, manufacturers are focusing more on product consistency and lower rejection rates in large plants. In this setting, barium carbonate is added to clay mixes as it neutralizes soluble sulfates and turns them into stable barium sulfate, which helps prevent white salt stains, scumming, and efflorescence while improving fired color and durability. Additionally, wider market growth is supported by steady expansion in ceramic sanitaryware and tiles, gradual rise in specialty and technical glass, and growing electronic ceramics that use BaCO3 as a raw material. Overall, the product demand in strong and stable in the construction sector and the need for better quality building materials and electronics further drives market growth.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Toxicity and Regulatory Pressure to Restrain the Market Growth

Barium carbonate is classified as harmful/toxic if swallowed or inhaled, mainly as soluble barium ions can affect muscles and the nervous system. This hazard profile has led to stricter environmental and worker-safety rules for handling barium compounds, including requirements for dust control, PPE, controlled storage, labeling, and safe disposal. These measures raise compliance and operating costs for producers and downstream users. In construction materials, especially bricks and tiles, regulators and large buyers in some markets discourage the heavy use of toxic barium salts; hence, manufacturers limit dosage to the minimum effective level. In areas where rules or customer standards tighten further, plants may switch to lower-toxicity alternatives such as strontium carbonate or other anti-efflorescence additives. Overall, toxicity-linked regulation acts as a clear demand restraint by increasing costs and accelerating substitution risk in traditional applications.

MARKET OPPORTUNITIES

Expanding Electro-Ceramics and MLCC Production to Boost the Demand for High-Purity Barium Carbonate

Rising electro-ceramics demand is a strong opportunity for market players as BaCO3 is the main barium source used to make barium titanate and ferrites. These materials are essential in multilayer ceramic capacitors, PTC thermistors, sensors, actuators, and magnetic parts. As electronics volume increases across consumer devices, automotive systems, telecom hardware, and power equipment, the output of MLCCs and ferrites grows, lifting BaCO3 use. At the same time, component makers push for miniaturization and higher capacitance. Hence, they need very low-impurity BaCO3 with controlled particle size to avoid defects and maintain dielectric performance. This drives premium pricing for technical and electronic grades and encourages capacity upgrades.

MARKET CHALLENGES

Fluctuating Barite Supply and Energy Prices to Drive Cost and Margin Instability

Volatile raw-material and energy costs are a persistent challenge as barium carbonate production depends on mined barite and heat-intensive processing. Barite (or barium sulfide derived from it) is the main feedstock and often the biggest variable cost. Hence, shifts in mine supply, environmental rules, or competing demand quickly flow into BaCO3 pricing. Barite prices also track oil-and-gas drilling cycles and can spike when major mines are disrupted. Energy adds another layer. The black-ash route uses coal/coke kilns near 1100°C. Therefore, swings in coal, gas, or power tariffs squeeze margins and force price pass-throughs or output cuts.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade protectionism and geopolitics influence the market mainly by reshaping trade flows and destabilizing costs. The anti-dumping probes and duties on barium carbonate imports (such as recent EU actions targeting China and India) can raise landed prices, create regional price gaps, and force buyers to switch suppliers or localize sourcing. At the same time, barite feedstock supply is concentrated in a few countries. Hence, geopolitical friction, mining curbs, or shipping disruptions can tighten availability and lift raw-material and freight costs, leading to uneven supply and margin pressure across the value chain.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the market is moving toward higher-purity, more consistent products and cleaner production routes. Producers are refining precipitation and carbonization controls to cut iron, alkali, and sulfate impurities for electronic and optical uses. At the same time, work on ultra-fine, narrow particle-size powders is increasing since better morphology improves barium titanate and ferrite performance. Process research targets lower energy use and emissions in barite-to-BaCO3 conversion, including modified “black-ash” steps and alternative reducing agents, while also improving waste/slag treatment and recycling.

SEGMENTATION ANALYSIS

By Form

Powder Segment Led in 2025 Due to Uniform Blending in Ceramics and High Performance Needs in Electro-Ceramics

Based on form, the market is segmented into powder and granular.

The powder segment held the largest market share in 2025. The segment growth is supported by strong use in ceramics and glazes, where fine powder disperses evenly and reacts faster, improving glaze smoothness and fired quality. The product demand is also rising from electro-ceramic and ferrite manufacturing as powder with controlled (often ultra-fine) particle size is preferred for uniform barium titanate/ferrite synthesis and higher dielectric performance. Producers are increasingly offering narrow particle-size and low-impurity powders to meet stricter technical-grade requirements, which lifts value and volume in advanced applications.

The granular segment is growing steadily with the scale-up of brick, tile, and specialty glass plants, where granules allow for easier dosing and more stable blending in high-throughput operations. Moreover, granules generate less dust, improving worker safety and reducing material loss during handling. Additionally, glass batch users value granular barium carbonate for consistent melting and batch behavior, supporting continued demand in display, crystal, and technical glass.

By Grade

Technical Grade Segment Dominated with Rising Demand in Specialty Glass and Electro-Ceramics Applications

Based on grade, the market is segmented into technical grade, industrial grade, and others.

Among these, the technical grade segment registered a dominant barium carbonate market share in 2025. Technical grade serves specialty glass and electro-ceramics applications where purity directly affects performance. This grade is used to produce barium titanate and ferrites for MLCC capacitors, thermistors, sensors, and magnets. Hence, tighter limits on iron, alkalis, and sulfates are now standard. Moreover, electronics makers want consistent particle size and low defect rates as devices become smaller and higher-capacity. Additionally, technical grade earns better margins; therefore, producers are upgrading refining and quality control to expand this portfolio.

The industrial grade segment is growing rapidly as it is widely consumed in bricks, tiles, and general ceramics. It is chosen for cost efficiency and reliable sulfate-removal in clay bodies, which prevents efflorescence and improves fired appearance. Moreover, rising housing and infrastructure output keeps baseline demand steady. Additionally, large brick and tile plants prefer long-term bulk supply of industrial grade for stable formulations.

The “others” segment includes non-standard or niche variants beyond industrial and technical grades. This typically covers high-purity or electronic grades with tighter impurity limits, laboratory/reagent grades for testing and R&D, and customized buyer-specific grades such as low-sulfate, low-iron, controlled particle-size, or low-moisture products. The volumes are small but value is higher.

By Application

To know how our report can help streamline your business, Speak to Analyst

Brick & Tiles Segment to Lead with Rising Demand in Infrastructure Projects

Based on application, the market is segmented into bricks & tiles, specialty glass, chemical compounds, electro-ceramic materials, and others.

The bricks & tiles segment is expected to dominate the market during the forecast period. Barium carbonate is added to clay bodies to stop white salt stains by removing soluble sulfates; hence, the demand closely follows brick and tile output. Growth is the strongest in areas where housing, urban development, and infrastructure projects are rising and where producers want cleaner finishes and fewer rejected batches. The segment is price-sensitive and mostly uses industrial grade, with steady, construction-linked demand.

The specialty glass segment is growing steadily, as BaCO3 improves glass clarity, durability, and chemical resistance, and is used in optical, display, and technical glass. The demand rises with the higher production of value-added glass and stricter quality needs. Moreover, many customers prefer more consistent, lower-impurity grades, creating scope for technical-grade supply.

In chemical compounds, BaCO3 acts mainly as a precursor to other barium salts and oxides. This segment is stable and tied to downstream chemical production cycles. The major opportunities come from local supply to specialty barium derivatives and niche chemical uses, but growth is moderate compared to ceramics and electronics.

The electro-ceramic materials segment is growing at a significant rate, as BaCO3 is used as a main input for barium titanate and ferrites used in MLCC capacitors, thermistors, sensors, actuators, and magnets. As electronics volumes rise and components get smaller, buyers demand high-purity and fine particle BaCO3, pushing technical and electronic grades.

The others segment includes general ceramic bodies and glazes such as tableware, pottery, porcelain, and sanitaryware, along with small-volume specialty uses such as custom barium intermediates, pigments or catalyst formulations, and laboratory or pilot-scale R&D consumption. The segment growth is supported by premium and decorative ceramics, tighter defect-control needs in niche ceramic products, and increasing demand for customized, high-purity batches for specialized industrial processes.

BARIUM CARBONATE MARKET REGIONAL OUTLOOK

By region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Barium Carbonate Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America currently holds the leading share in the market, helped by strong demand from specialty and technical glass, advanced ceramics, and electronic-ceramic materials that need consistent, low-impurity feedstock. Mature but high-value manufacturing and steady renovation activity keep consumption stable. Buyers also emphasize compliant handling and supply reliability as many barite and barium inputs are imported; hence, price swings in feedstock and freight quickly influence regional purchasing.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe shows steady demand shaped by specialty glass, technical ceramics, and regulated construction materials. Refurbishment and energy-efficient building upgrades sustain tile and architectural glass output, supporting industrial-grade volumes. Stricter chemical safety and environmental norms encourage precise dosing and preference for controlled-purity grades, which supports technical-grade uptake. Trade measures, including anti-dumping actions, can shift sourcing toward regional suppliers, improving local producers’ positioning.

Asia Pacific

The Asia Pacific market is growing at a significant rate, backed by large-scale housing, urban infrastructure, and industrial expansion that drives heavy bricks, tiles, and general ceramics production. These applications need barium carbonate to prevent efflorescence and surface defects, keeping volumes high. The region also has strong specialty glass and electronic-ceramic manufacturing, raising technical and high-purity consumption. Proximity to major barite sources and integrated barium chemical capacity supports cost-competitive supply.

Latin America

The Latin America market is expanding gradually, mainly as residential construction and urban development lift brick, tile, and ceramic output. Producers use barium carbonate to improve fired finish quality and reduce sulfate-related defects, leading to a rise in the demand for organized ceramics manufacturing. Regional barite availability, including supply from Mexico, offers some feedstock support. However, the market remains sensitive to import prices, currency movement, and inland logistics costs.

Middle East & Africa

The Middle East and Africa depicts growing consumption tied to infrastructure megaprojects, housing programs, and new ceramic tile and glass plants. Barium carbonate is used in clay bodies to control efflorescence and in glass batches for quality consistency, making project-led building activity the key pull. The region’s barite resources, notably in North Africa, add strategic supply relevance, though imports and shipping costs still shape availability.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Companies to Invest in Product Development to Strengthen Industry Positions

Solvay, SAKAI CHEMICAL INDUSTRY CO., LTD., Nippon Chemical Industrial CO., LTD., Hubei JingshanChutianBarium Salt Corp. Ltd, and ThermoFisher Scientific Inc. are the key players in the market. Companies are making major investments toward developing products that address the evolving demands for sustainability and performance.

LIST OF KEY BARIUM CARBONATE COMPANIES PROFILED

- Solvay (Belgium)

- SAKAI CHEMICAL INDUSTRY CO., LTD. (Japan)

- Nippon Chemical Industrial CO., LTD. (Japan)

- Hubei JingshanChutianBarium Salt Corp.Ltd (China)

- ThermoFisher Scientific Inc. (U.S.)

- American Elements (U.S.)

- FUJIFILM Wako Pure Chemical Corporation (Japan)

- Kandelium (Germany)

- Vishnu Chemicals (India)

- Akshya Chemicals Pvt Ltd. (India)

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, form, grade, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2035 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2035 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Million), Volume (Kiloton) |

|

Growth Rate |

CAGR of 3.3% from 2026 to 2035 |

|

Segmentation |

By Form, By Grade, By Application, By Region |

|

By Form |

· Powder · Granular |

|

By Grade |

· Technical Grade · Industrial Grade · Others |

|

By Application |

· Bricks & Tiles · Specialty Glass · Chemical Compounds · Electro-Ceramic Materials o MLCC o Thermistors o Others · Others |

|

By Region |

· North America (By Form, By Grade, By Application, By Country) o U.S. (By Application) o Canada (By Application) · Europe (By Form, By Grade, By Application, By Country) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Rest of Europe (By Application) · Asia Pacific (By Form, By Grade, By Application, By Country) o China (By Application) o India (By Application) o Japan (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Form, By Grade, By Application, By Country) o Mexico (By Application) o Brazil (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Form, By Grade, By Application, By Country) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 202.3 million in 2025 and is projected to reach USD 280.5 million by 2034.

Recording a CAGR of 3.3%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

By form, the powder segment led the market in 2025.

North America holds the highest market share.

A rise in construction activities is driving BaCO3 demand in bricks and tiles, propelling industry expansion.

- 2021-2035

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us