Battery Manufacturing Equipment Market Size, Share & Industry Analysis, By Battery Type (Lithium-Ion Batteries, Solid-State Batteries, Lead-Acid Batteries, and Others), By Equipment Type (Electrode Manufacturing Equipment, Cell Assembly Equipment, Formation & Testing Equipment, Module & Pack Assembly Equipment, and Others), By Application (Automotive, Consumer Electronics, Energy Storage Systems (ESS), Industrial Applications, and Others), and Regional Forecast, 2026 - 2034

Battery Manufacturing Equipment Market Size and Future Outlook

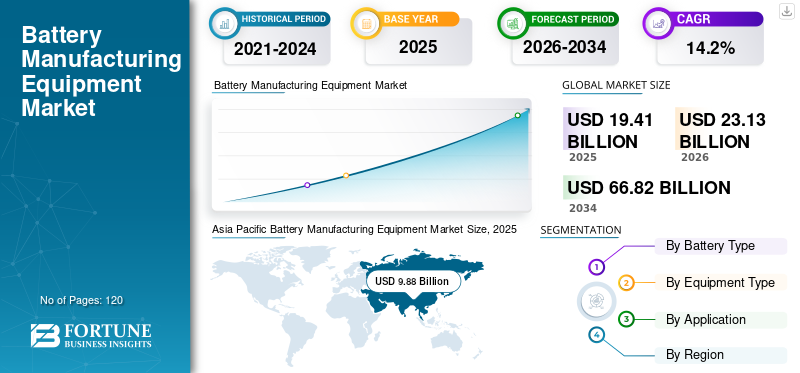

The global battery manufacturing equipment market size was valued at USD 19.41 billion in 2025. The market is projected to grow from USD 23.13 billion in 2026 to USD 66.82 billion by 2034, exhibiting a CAGR of 14.2% during the forecast period. Asia Pacific dominated the battery manufacturing equipment market with a market share of 50.90% in 2025.

Battery manufacturing equipment refers to specialized machinery used in electrode fabrication, cell assembly, formation, testing, and module integration processes for advanced battery technologies. These systems are essential for ensuring production scalability, quality control, and efficiency in battery giga factories worldwide.

The market is witnessing rapid expansion due to accelerating Electric Vehicle (EV) adoption, rising renewable energy storage deployment, and increasing demand for high-energy-density lithium ion batteries. Governments worldwide are supporting domestic battery production through incentives and localization policies, driving investments in gigafactory construction and advanced automated equipment.

Major players such as Wuxi Lead Intelligent Equipment, Manz AG, Hitachi High Tech Corporation, Koem Co., Ltd., Dürr AG, Tesla Inc., CATL, Siemens AG, PNT Co., Ltd., and Nordson Corporation are actively expanding production equipment capabilities to support large-scale battery manufacturing.

- For instance, in September 2023, Tesla began production at its lithium refinery facility in Texas, reinforcing vertical integration and strengthening battery supply chain infrastructure.

Download Free sample to learn more about this report.

BATTERY MANUFACTURING EQUIPMENT MARKET TRENDS

Gigafactory Expansion and Automation Integration Driving Equipment Demand

A major trend shaping the market is the rapid construction of battery gigafactories globally. OEMs and battery manufacturers are investing in highly automated electrode coating, calendaring, stacking, and formation systems to scale production efficiently.

Additionally, the integration of Industry 4.0 technologies such as AI-based quality inspection, predictive maintenance, and digital twin simulation is transforming battery manufacturing operations.

- For instance, in 2024, CATL announced the expansion of multiple gigafactory projects in China and Europe, increasing demand for advanced electrode and cell assembly equipment.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Surging EV Production and Energy Storage Deployment to Drive Market Growth

The rapid adoption of electric vehicles globally is a primary driver of battery manufacturing equipment demand. Increasing EV production requires large-scale lithium-ion battery cell manufacturing, which depends on high-precision electrode and assembly equipment.

In addition, the expansion of renewable energy systems is boosting demand for stationary energy storage solutions, further strengthening battery production capacity expansion.

- For instance, in 2024, BYD expanded its battery production capacity to support EV demand, reinforcing equipment investment across manufacturing lines.

MARKET RESTRAINTS

High Capital Investment and Technological Complexity Restricting Adoption

Battery manufacturing equipment requires substantial upfront capital expenditure and precision engineering capabilities. Smaller manufacturers may face financial and technological barriers when upgrading to advanced automated systems.

In addition, rapid technological evolution in battery chemistry creates integration challenges for equipment suppliers aiming to maintain compatibility with new battery formats.

- For instance, in 2024, Manz AG reported financial restructuring efforts amid market competition and capital intensity pressures, highlighting investment challenges within the industry.

MARKET OPPORTUNITIES

Solid-State and Advanced Battery Technology Development Creating New Equipment Demand

The development of solid-state batteries and next-generation chemistries presents significant growth opportunities for specialized manufacturing equipment. These batteries require modified electrode processing, stacking systems, and advanced testing solutions.

As manufacturers transition toward higher energy density and safer battery technologies, equipment suppliers are expected to benefit from new customization and system upgrade requirements. These factors drive the battery manufacturing equipment market growth.

- For instance, in 2024, Toyota announced progress in solid-state battery development, driving expectations for next-generation manufacturing line upgrades.

Segmentation Analysis

By Battery Type

Lithium-Ion Batteries Dominate Due to EV and Consumer Electronics Demand

Based on battery type, the market is segmented into lithium-ion batteries, solid-state batteries, lead-acid batteries, and others.

The lithium-ion batteries segment holds the largest battery manufacturing equipment market share, driven by strong demand from EV manufacturers and consumer electronics producers requiring high energy density and scalable manufacturing.

- For instance, CATL and LG Energy Solution continue expanding lithium-ion production capacity globally, reinforcing equipment demand.

The solid-state batteries segment is expected to register the highest CAGR of 20.4% during the forecast period, driven by increasing R&D investments and enhanced safety advantages over conventional lithium-ion batteries.

To know how our report can help streamline your business, Speak to Analyst

By Equipment Type

Electrode Manufacturing Equipment Segment Leads Due to Its Core Production Role

Based on equipment type, the market is segmented into electrode manufacturing equipment, cell assembly equipment, formation & testing equipment, module & pack assembly equipment, and others.

The electrode manufacturing equipment segment holds the highest market share, as electrode coating, drying, and calendaring represent critical production stages influencing battery performance and yield.

- For instance, Wuxi Lead Intelligent Equipment supplies large-scale electrode production systems for leading battery manufacturers, supporting high-volume output.

The electrode manufacturing equipment segment is projected to register the highest CAGR of 15.7%, driven by gigafactory expansion.

By Application

Automotive Segment Dominates Due to EV Production Scale

Based on application, the market is segmented into automotive, consumer electronics, Energy Storage Systems (ESS), industrial applications, and others.

The automotive segment holds the highest market share, as EV battery demand requires large-scale automated production facilities.

- For instance, Tesla and BYD continue scaling EV battery production, reinforcing equipment investment.

The Energy Storage Systems (ESS) segment is expected to record the highest CAGR of 15.8%, supported by grid modernization and renewable integration projects.

Battery Manufacturing Equipment Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East and Africa.

Asia Pacific

Asia Pacific Battery Manufacturing Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest market share and is expected to register the highest CAGR during the forecast period. The region leads due to concentrated battery supply chains, large-scale gigafactory footprints, and strong end-demand from electric vehicles and consumer electronics. Major battery producers and tier-1 suppliers in China, Japan, and South Korea continue to expand capacity, driving sustained procurement of electrode manufacturing, cell assembly, and formation & testing equipment.

Additionally, Asia Pacific benefits from a dense ecosystem of equipment makers, automation integrators, and upstream material suppliers, enabling faster plant commissioning and iterative equipment upgrades. Continuous process optimization, particularly for high-speed coating, calendaring, and advanced formation protocols, keeps equipment replacement and expansion cycles active.

Japan Battery Manufacturing Equipment Market

Japan’s market in 2026 is estimated at around USD 1.25 billion, representing approximately 5.4% of global revenues. Precision manufacturing strengths and advanced quality control requirements support higher adoption of automated formation/testing and inspection tools.

Growing focus on next-generation batteries, including solid-state development, is also encouraging equipment modernization and pilot-line investments.

China Battery Manufacturing Equipment Market

China’s market size in 2026 is estimated at around USD 7.04 billion, representing approximately 30.4% of global revenues. Gigafactory expansions and aggressive EV production targets continue to drive large-volume orders for electrode and cell assembly lines.

Strong domestic equipment supply capabilities and ongoing technology upgrades for higher energy-density cells further support demand.

India Battery Manufacturing Equipment Market

India’s market in 2026 is estimated at around USD 1.77 billion, representing approximately 7.6% of global revenues. Policy-led localization and new cell manufacturing projects are driving demand for turnkey production lines and formation/testing systems.

Rising EV penetration and the build-out of domestic battery ecosystems are accelerating equipment sourcing and integration.

North America

North America represents a fast-expanding market for battery manufacturing equipment, supported by accelerated localization of battery supply chains and large investments in EV and ESS manufacturing capacity. The region is adopting highly automated electrode manufacturing and cell assembly systems to improve yield, reduce scrap, and scale production efficiently, particularly for automotive batteries.

In addition, stricter compliance expectations and quality standards are pushing demand for advanced formation & testing equipment, inline metrology, and digital manufacturing controls. A strong ecosystem of automation and industrial software providers further supports equipment integration and plant ramp-up timelines.

U.S. Battery Manufacturing Equipment Market

The U.S. market in 2026 is estimated at around USD 3.63 billion, representing approximately 15.7% of global revenues. Large-scale gigafactory commissioning and automotive battery capacity additions are driving significant equipment installations.

High emphasis on yield improvement and automation is accelerating the adoption of high-speed coating, stacking/winding, and advanced testing systems.

Europe

Europe is steadily expanding battery manufacturing equipment demand as it scales regional cell production to support EV transition targets and reduce import dependency. The region’s equipment needs are strongly shaped by automotive OEM-driven gigafactory investments, where electrode manufacturing and formation/testing systems are prioritized to meet high safety and traceability requirements.

Furthermore, Europe’s focus on sustainable manufacturing and energy efficiency is pushing plants toward advanced process control, emissions reduction in solvent recovery, and automation-heavy production layouts. This is strengthening demand for integrated, digitally monitored manufacturing lines.

U.K. Battery Manufacturing Equipment Market

The U.K. market in 2026 is estimated at around USD 0.87 billion, representing approximately 3.8% of global revenues. Localized battery supply chain development and EV manufacturing needs are supporting investments in cell assembly and testing infrastructure.

Growing emphasis on domestic capability building and scale-up programs is contributing to demand for modular production equipment.

Germany Battery Manufacturing Equipment Market

Germany’s market size is estimated to be valued at USD 1.77 billion in 2026, representing approximately 7.7% of global revenues. The country’s automotive base and high-volume EV production targets continue to drive gigafactory-related equipment procurement.

High engineering standards and process consistency requirements are strengthening the adoption of advanced electrode manufacturing and inline inspection systems.

South America and Middle East & Africa

Middle East & Africa and South America collectively represent emerging markets for battery manufacturing equipment, driven by early-stage localization efforts, renewable energy storage expansion, and gradual EV adoption. While large-scale cell manufacturing is still developing, the regions are witnessing increasing interest in battery pack assembly, testing infrastructure, and localized value-chain buildouts.

Additionally, government-led industrial diversification initiatives and resource-linked strategies are encouraging investment discussions around battery production ecosystems. Demand growth is expected to strengthen as ESS deployment scales and regional manufacturing capabilities expand.

GCC Battery Manufacturing Equipment Market

The GCC market in 2026 is estimated at around USD 0.37 billion, representing approximately 1.6% of global revenues. Energy transition programs and grid-scale storage investments are supporting demand for module/pack assembly and testing equipment.

Industrial diversification strategies and partnerships aimed at localized manufacturing further contribute to gradual equipment adoption.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Gigafactory Partnerships Strengthening Competitive Positioning

The battery manufacturing equipment market is highly competitive, driven by rapid gigafactory construction and increasing automation requirements. Companies are focusing on high-speed electrode coating systems, automated cell assembly platforms, and integrated formation testing solutions to enhance throughput and yield rates.

Strategic partnerships between battery OEMs and equipment suppliers are central to scaling production efficiently and maintaining quality standards across evolving battery chemistries.

LIST OF KEY BATTERY MANUFACTURING EQUIPMENT COMPANIES PROFILED

- Wuxi Lead Intelligent Equipment Co., Ltd. (China)

- Manz AG (Germany)

- Hitachi High-Tech Corporation (Japan)

- Dürr AG (Germany)

- PNT Co., Ltd. (South Korea)

- Koem Co., Ltd. (South Korea)

- Nordson Corporation (U.S.)

- Siemens AG (Germany)

- CATL (China)

- Tesla Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2025: CATL announced plans to build a new battery manufacturing facility in Hungary, expanding European production capacity.

- January 2025: LG Energy Solution expanded its joint venture battery production operations in the U.S., increasing demand for manufacturing equipment.

- November 2024: Tesla continued the expansion of its Texas gigafactory battery cell production lines to scale 4680 cell manufacturing.

- August 2024: Siemens strengthened partnerships with battery manufacturers to deploy digital factory automation solutions for gigafactories.

- September 2023: Tesla began lithium refinery operations in Texas to strengthen vertical battery supply chain integration.

REPORT COVERAGE

The global report on battery manufacturing equipment market analysis includes a comprehensive study of market size and forecast across all key segments included in the report. It provides insights into market trends, drivers, restraints, opportunities, and challenges expected to influence the market growth over the forecast period The report also covers technological advancements in digital identity and verification platforms, compliance considerations, and key strategic developments, including partnerships and mergers & acquisitions activity, alongside regional insights and competitive landscape analysis. Additionally, it includes regional insights and competitive landscape analysis, highlighting the market positioning and strategic initiatives of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Battery Type, Equipment Type, Application, and Region |

| By Battery Type |

|

| By Equipment Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 19.41 billion in 2025 and is projected to reach USD 66.82 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 9.88 billion.

The market is expected to exhibit a CAGR of 14.2% during the forecast period.

By application, the automotive segment is leading the market.

Surging EV production and energy storage deployment are the key factors driving the market growth.

Wuxi Lead Intelligent Equipment Co., Ltd., Manz AG, Hitachi High-Tech Corporation, and Dürr AG are among the major players in the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us