Apparel Market Size, Share & Industry Analysis, By Type (Casual Wear/Fashion Wear, Formal Wear, Swimwear, Outerwear, Sportswear & Activewear, Agricultural Work Clothing/Farm Apparel, Work Wear, Ethnic Wear, Sleepwear, and Others), By Material (Synthetic, Cotton, Wool, Leather, Denim, Satin, and Others), By End-User (Men, Women, Children, and Unisex), By Category (Mass/Economy, Premium, and Luxury), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores/Branded Stores, Department Stores, Online/E-commerce, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

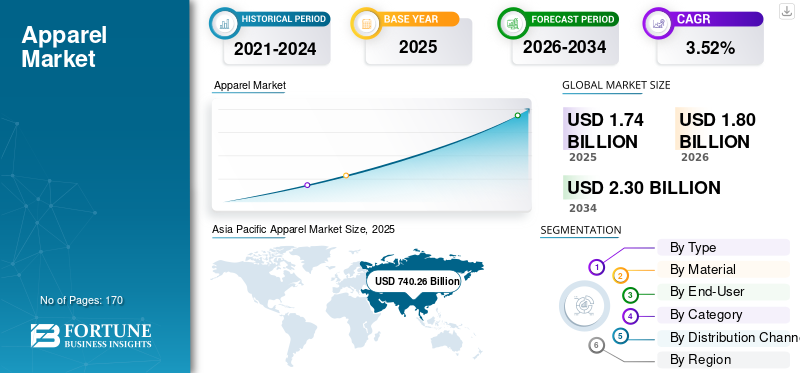

Apparel Market Size & Share

The global apparel market size was valued at USD 1,749.67 billion in 2025 and is projected to grow from USD 1,804.08 billion in 2026 to USD 2,307.04 billion by 2034, exhibiting a CAGR of 3.52% over the forecast period. Asia Pacific dominated the apparel market with a market share of 41.03% in 2025. The industry growth is driven by evolving consumer preferences, fast fashion dynamics, sustainability shifts, and omnichannel retail expansion across developed and emerging economies worldwide.

The global apparel market is a dynamic and expansive sector, encompassing a wide range of products from everyday casual wear to high-end fashion. Product lifecycle management in this market plays an important role as it allows clothing companies to manage and organize key information effectively. The global clothing market has witnessed robust growth, driven by several key factors, including the rise of fast fashion, increasing consumer spending, advancements in production technology, and the wide acceptance of e-commerce platforms as preferred distribution channels, among others.

As discretionary spending on clothing increased, shopping became a form of entertainment, which in turn has revolutionized the clothing industry. Companies such as Zara and H&M are leading the charge in bringing trendy, fashionable clothing to consumers at unprecedented speeds. This model caters to the increasing consumer demand for up-to-date styles, resulting in higher purchase frequency.

The growing middle class in emerging economies such as India, China, Brazil, Argentina, South Africa, and many Southeast Asian countries further significantly boosts clothing sales. The rise in the working population has increased consumer purchasing power, contributing to market expansion. For instance, according to the Periodic Labour Force Survey (PLFS), employment in India surged from 46.8% in 2017-18 to 56% in 2022-23, accompanied by a noteworthy rise in labor force participation from 49.8% to 57.9%. Simultaneously, the unemployment rate shrank from 6% to 3.2%, highlighting a favorable job market shift.

According to the report published by the Development Commissioner, Ministry of Micro, Small & Medium Enterprises in 2021, the COVID-19 pandemic affected the garment industry negatively, shrinking the market size by around 30%. The mass closure of public places and offices, along with the cancellation of big events and celebrations, caused garment sales to plummet, cited the head of Harry Rosen, one of Canada’s leading men’s clothing retailers. However, the long-term growth trend of clothing remains intact, and the industry is rebounding post-COVID-19 as restrictions have been lifted across countries.

The apparel market remains one of the most dynamic and globally interconnected consumer industries, shaped by shifting fashion cycles, evolving consumer preferences, and complex supply chain structures. The sector operates at the intersection of manufacturing efficiency, brand positioning, and retail innovation, making it highly sensitive to macroeconomic trends and consumer sentiment.

The apparel market size continues to expand, supported by population growth, rising disposable incomes in emerging economies, and increasing digital penetration. However, growth patterns vary significantly across segments. While premium and luxury apparel benefit from brand-driven demand, mass-market segments rely heavily on pricing strategies and supply chain efficiency.

The apparel market growth trajectory is increasingly influenced by digital transformation. Online retail channels have altered traditional distribution dynamics, enabling brands to engage directly with consumers while reducing reliance on intermediaries. This shift has improved margins for some players but intensified competition. Supply chain resilience has also become a strategic priority. Disruptions in global logistics and raw material sourcing have prompted companies to diversify manufacturing bases and invest in nearshoring strategies.

Download Free sample to learn more about this report.

Apparel Market Key Takeaways

- 2025 Market Size: USD 1,749.67 billion

- 2026 Market Size: USD 1,804.08 billion

- 2034 Forecast Market Size: USD 2,307.04 billion

- CAGR: 3.52% from 2026-2034

- Asia Pacific dominated the apparel market with a 41.03% share in 2025.

- The casual wear/fashion wear segment accounted for 35.85% of the market in 2026.

- The synthetic materials segment held a 56.23% share in 2026.

Asia Pacific

Asia Pacific generated USD 740.26 billion in 2025 and is projected to reach USD 769.67 billion in 2026.

North America

North America accounted for USD 466.78 billion in 2025, making it the second-largest regional market.

Europe

Europe reached USD 432.30 billion in 2025, supported by strong demand for premium and sustainable apparel.

U.S.

The apparel market is projected to reach USD 399.77 billion by 2026.

Japan

The apparel market is projected to reach USD 98.33 billion by 2026.

Read More

Apparel Market Trends

Sustainability and Ethical Fashion Accompanied by Increased Transparency

Sustainability and ethical fashion have become central pillars of the apparel industry. Consumers, particularly Millennials and Gen Z, are increasingly concerned about the environmental and social impact of their clothing choices. Consumers are keenly interested in knowing and understanding where their clothes come from and what and how they are made. As a result, brands are focusing on a transparent supply chain, eco-friendly materials, and ethical labor practices to meet this demand. This is driven by consumer willingness to pay more for eco-friendly and sustainable upcycled clothing. One of the key aspects of this trend is the rise of circular fashion, where garments are designed with their entire lifecycle in mind. This includes creating clothing from recycled materials, promoting repair and reuse, and developing business models centered on rental, resale, or upcycling.

Major brands such as H&M and Levi’s have introduced recycling programs and second-hand sales channels. This shift has led to greater transparency, with brands publishing reports on their supply chains, providing certifications, and engaging in responsible sourcing. For instance, in September 2023, Loro Piana, the Italian luxury apparel brand part of LVMH Group, announced the launch of a conscious and sustainable carryover capsule collection named “Loro”. The collection is made with recycled cashmere from the company’s knitwear surpluses and is available in a full-size range, from 8-year-old children to 4XL for women and men. In response to this trend, companies are rethinking traditional fashion models. While fast fashion remains popular, sustainable practices are becoming a competitive differentiator. This trend has accelerated post-pandemic, as consumers rethink their consumption patterns and seek purpose-driven brands that align with their values.

The apparel market is undergoing a structural transformation, driven by changing consumer behavior and technological advancements. One of the most prominent apparel market trends is the shift toward fast fashion, characterized by rapid product turnover and shorter design-to-retail cycles. This model enables brands to respond quickly to evolving consumer preferences but also increases operational complexity. Digitalization is another defining trend. E-commerce platforms and mobile applications are reshaping how consumers discover and purchase apparel. Social media platforms play a significant role in influencing purchasing decisions, particularly among younger demographics.

Sustainability has emerged as a critical focus area. Consumers are increasingly aware of environmental and social impacts, prompting brands to adopt sustainable materials and transparent supply chains. This trend is particularly strong in developed markets. Personalization is also gaining importance. Brands are leveraging data analytics to offer customized products and experiences, enhancing customer engagement and loyalty.

Download Free sample to learn more about this report.

Key Market Dynamics

Apparel Market Growth Factors

Increasing Technological Integration and Product Innovation are Driving Market Growth

The apparel industry has recorded significant growth in technological integration in recent years, a significant factor driving global market growth. The manufacturers are launching innovative product ranges, utilizing the rapidly changing technological landscape by integrating new and advanced technologies. These new product launches are driving the demand for an advanced product range. The changing technological landscape, with the launch of new innovative fabrics and product ranges, significantly influences consumer behavior, leading to global market growth.

For instance, in October 2023, Brooks, a well-known running shoe company, announced its partnership with Hewlett-Packard Company by releasing an Exhilarate-BL sneaker, incorporated with a 3D printed midsole technology called "3DNA". Furthermore, in June 2023, Nike unveiled Aerogami, its latest performance-apparel technology intended to improve breathability precisely when athletes need it.

Rising Participation in Sports and Outdoor Activities to Drive Apparel Market Growth

Participation in outdoor sports and recreational activities is not specific to a certain age group, as individuals of all ages participate. However, the participation of the geriatric and young age groups aged 65+ and 10-24 has shown significant growth since 2015 and has been driving the development of the apparel industry in North America. For instance, as per the Outdoor Industry Association, since 2019, the geriatric population in the U.S. has recorded a growth of 2.5 million or 16.8% in participation in outdoor recreational activities.

The apparel market growth is driven by a combination of demographic, economic, and technological factors. Population growth and urbanization in emerging markets are expanding the consumer base, creating new demand opportunities across multiple apparel segments. Rising disposable incomes, particularly in Asia-Pacific and Latin America, support increased spending on apparel. Consumers in these regions are transitioning from basic clothing needs to fashion-oriented purchases, contributing to market expansion.

Technological advancements also contribute to growth. Data analytics and artificial intelligence enable better demand forecasting and inventory management, improving operational efficiency. These capabilities allow companies to respond more effectively to changing consumer preferences. The expansion of sportswear and activewear segments further supports growth. Health and wellness trends are increasing the demand for functional and performance-oriented apparel.

Restraining Factors

Increasing Competition from Local Brands Emphasizing Affordable Pricing May Threaten International Market Players’ Growth

International brands often face intense competition from domestic manufacturers due to regional fashion preferences and more affordable pricing factors, which hampers apparel market growth. Local manufacturers have a better understanding of regional tastes, cultural nuances, and traditional styles. They can design their products to meet local demand more efficiently than international brands.

In addition, local brands quickly adapt to changing trends and customer preferences within their region. In contrast, international brands may have longer lead times due to centralized decision-making, and global supply chains further pose challenges to market expansion. Furthermore, local manufacturers typically have lower production costs due to cheaper labor and materials, allowing them to offer more affordable pricing when compared to international brands, which may have high overhead and logistical costs. These factors restrain the further penetration of international brands into the local market, impeding market growth.

The apparel market faces several structural constraints that influence profitability and growth. One of the primary challenges is demand volatility, driven by changing consumer preferences and economic uncertainty. Apparel is often considered a discretionary purchase, making it sensitive to fluctuations in consumer spending. Supply chain complexity is another significant constraint. The apparel industry relies on global sourcing and manufacturing networks, which are vulnerable to disruptions. Logistics challenges, raw material price fluctuations, and geopolitical factors can impact production and distribution.

Cost pressures are particularly significant. Rising wages in manufacturing hubs and increasing costs of raw materials such as cotton and synthetic fibers affect margins. Companies must balance cost management with maintaining product quality. Inventory management also presents challenges. Overstocking and understocking can lead to financial losses, particularly in fast fashion segments where product lifecycles are short.

Market Opportunities

The apparel market presents several opportunities driven by evolving consumer preferences and technological innovation. One of the most significant opportunities lies in sustainable fashion. Brands that adopt environmentally friendly practices and transparent supply chains can differentiate themselves and capture growing consumer interest. E-commerce expansion represents another key opportunity. Online platforms enable brands to reach a global audience, reducing dependence on physical retail infrastructure. Direct-to-consumer models improve margins and enhance customer relationships.

Emerging markets offer substantial growth potential. Rising incomes and urbanization are increasing demand for apparel, particularly in the Asia-Pacific and Africa. These regions present opportunities for both global and local brands. Technological innovation also creates opportunities. Automation in manufacturing and digital design tools improves efficiency and reduces time-to-market. These advancements enable companies to respond quickly to changing trends.

Apparel Market Segmentation Analysis

By Type Analysis

Wide Selection of Sizes in Casual Wear/Fashion Wear to Favor Segmental Growth

By type, the market is divided into casual wear/fashion wear, formal wear, swimwear, outerwear, sportswear & active wear, agricultural work clothing/farm apparel, work wear, ethnic wear, sleepwear, and others.

Casual Wear / Fashion Wear

The casual wear/fashion wear segment is projected to dominate the type category, accounting for 35.85% of the market share in 2026, and is projected to maintain its leading position during the forecast period. The changing lifestyles of consumers, placing greater emphasis on comfort and utility, supplement the growth of the segment. In addition, the wide selection of designs, sizes, styles, and shades reflecting inclusivity enables consumers to match their clothing as per their taste and current fashion trends, leading to market expansion.

Casual and fashion wear represents the largest share of the apparel market, supported by high purchase frequency and continuous product refresh cycles. This segment operates on short lead times, requiring flexible sourcing and rapid inventory turnover. Demand is closely linked to evolving fashion trends, which are increasingly shaped by digital platforms and influencer-driven content. The Casual Wear/Fashion Wear segment is expected to hold a 35.68% share in 2024.

Urban consumers are prioritizing versatility, preferring garments that transition across social, professional, and leisure settings. This shift has expanded the relevance of casual wear beyond traditional boundaries, reinforcing its dominance in the apparel market. Brands are responding by integrating real-time data analytics into product design and assortment planning, improving alignment with consumer demand.

Margin pressures persist due to intense competition and discount-driven pricing strategies. At the same time, sustainability concerns are influencing purchasing decisions, prompting brands to introduce eco-conscious collections. This dual dynamic is reshaping apparel market share within the segment, as consumers balance affordability with environmental considerations.

Formal Wear

Formal wear demand is undergoing structural adjustment rather than expansion. The shift toward hybrid work models has reduced the frequency of traditional office attire purchases, particularly in developed markets. However, demand for semi-formal and business-casual apparel is increasing, reflecting evolving workplace expectations.

Occasion-driven consumption remains a critical demand driver, particularly for events, ceremonies, and professional engagements. This has allowed the segment to maintain relevance despite declining everyday usage. Product innovation is increasingly focused on comfort, incorporating stretch fabrics and lightweight materials to align with modern preferences. Regional variations are significant, with formal wear maintaining a stronger demand in markets where workplace norms remain traditional. The segment’s contribution to apparel market growth is therefore uneven, requiring brands to adapt region-specific strategies.

Swimwear

Swimwear operates as a seasonal segment with demand closely tied to tourism and leisure activities. Growth is concentrated in regions with expanding middle-class populations and increasing travel frequency. Product differentiation is driven by design, fit, and material performance. Sustainability is becoming a defining factor, with brands incorporating recycled fabrics and environmentally responsible production processes. Premiumization is evident, particularly in developed markets where consumers prioritize quality and design over price.

Inventory management remains a critical challenge due to demand variability, requiring precise forecasting and regional alignment. Despite its niche position, swimwear contributes to apparel market trends through innovation and lifestyle-driven consumption.

Outerwear

Outerwear represents a high-value segment characterized by longer product lifecycles and higher average selling prices. Demand is influenced by climatic conditions, making regional dynamics particularly significant. In colder markets, outerwear remains essential, while in temperate regions it functions as both a functional and fashion-driven category.

Technological advancements in fabric development are enhancing product performance, including water resistance, insulation, and lightweight construction. These innovations support premium pricing and brand differentiation. Consumers are increasingly evaluating outerwear based on durability and functionality rather than purely aesthetic considerations. The segment’s stability contributes to consistent revenue streams within the apparel market, offsetting volatility in more trend-sensitive categories.

Sportswear & Activewear

The sportswear & active wear segment is forecast to grow at the fastest CAGR during the study period 2024-2032. The increasing need for sports and fitness activities owing to the growing health consciousness and hectic work routines fuels the demand for sportswear & athletic apparel. Moreover, active lifestyles and increased participation of the population in outdoor and social activities accelerate the demand for sports apparel and activewear, or other outdoor apparel globally. Golf apparel, basketball apparel, and snow sports apparel are among the fastest-growing segments within the sportswear & activewear apparel category.

While the increasing demand for surgical apparel fuels the growth of the workwear segment, the increasing adoption of motorcycle apparel and intimate clothing favors the expansion of the other segment. Given the intensifying competition in the dominant product categories, including casual wear and ethnic wear, prospective market players will likely focus on penetrating the high-growth intimate apparel market in the coming years.

Sportswear and activewear continue to demonstrate strong apparel market growth, supported by structural shifts toward health-conscious lifestyles. The integration of athletic wear into everyday fashion has expanded its addressable market, reinforcing its position as a key growth driver. Performance innovation remains central, with advancements in moisture management, stretchability, and durability enhancing product appeal. Brands are also leveraging digital ecosystems, including fitness applications and wearable technology integration, to strengthen consumer engagement.

The segment benefits from higher margins compared to traditional apparel categories, attracting significant investment from both established players and new entrants. Its influence extends beyond functionality, shaping broader apparel market trends through the normalization of comfort-oriented clothing.

Agricultural Work Clothing / Farm Apparel

Agricultural work clothing remains a function-driven segment, with demand concentrated in rural economies. The segment emphasizes durability, protection, and practicality, with limited influence from fashion trends. Growth remains stable but region-specific, reflecting agricultural activity levels and workforce size. Product innovation is focused on improving comfort and resilience under demanding conditions. While its contribution to the overall apparel market size is limited, it provides consistent demand in targeted geographies.

Work Wear

Workwear serves the industrial and service sectors, including construction, manufacturing, and hospitality. Demand is closely tied to employment levels and regulatory requirements related to workplace safety. The segment is evolving through the incorporation of advanced materials that enhance durability and comfort while meeting compliance standards. Corporate branding and uniform standardization are also influencing purchasing patterns, particularly among large enterprises.

Workwear offers relatively predictable demand compared to fashion-driven segments, contributing to stability within the apparel market.

Ethnic Wear

Ethnic wear reflects cultural identity and tradition, with strong demand in regions such as Asia-Pacific and the Middle East. Consumption patterns are closely linked to festivals, ceremonies, and social events, creating cyclical demand peaks. The segment is evolving through the fusion of traditional and contemporary designs, expanding its appeal to younger consumers. Digital platforms are enabling broader market access, allowing regional styles to reach global audiences.

Ethnic wear contributes to the apparel market share through its strong regional presence and cultural relevance, supporting sustained demand despite global fashion convergence.

Sleepwear

Sleepwear is transitioning from a basic necessity to a lifestyle-oriented category. Consumers are placing greater emphasis on comfort, fabric quality, and design, particularly in premium segments. The segment benefits from stable demand, with growth supported by increasing interest in home-centric lifestyles. Product innovation includes the use of breathable and sustainable materials, aligning with broader apparel market trends.

To know how our report can help streamline your business, Speak to Analyst

By Material Analysis

Superior Functional Characteristics to Bolster Demand for Synthetic Clothing

Synthetic

Synthetic materials dominate due to cost efficiency and adaptability across various apparel types. Their widespread use in sportswear and fast fashion supports large-scale production and competitive pricing. Environmental concerns are prompting gradual shifts toward recycled synthetics, influencing product development strategies and regulatory compliance.

The synthetic materials segment is expected to lead the material category, representing 56.23% of the market share in 2026, and is projected to maintain its strong position throughout the forecast years. Synthetic fiber has gained prominence for its versatility, durability, ease of dyeing and printing, wrinkle resistance, and quick-drying nature. These properties make synthetic materials highly suitable for a variety of applications. The segment is expected to dominate the market share of 56.37% in 2025 and to exhibit a CAGR of 4.23% during the forecast period. In addition, due to enhanced properties, synthetic materials find extensive applications in casual wear or fashion wear, sportswear, active wear, work wear, and sleepwear, among others.

Cotton

The cotton segment is forecast to witness rapid growth throughout the projected timeframe. Factors contributing to the segment’s growth include the materials' natural attributes, such as breathability, comfort, hypoallergenic nature, and timeless appeals to consumers of all age groups. Furthermore, the increasing demand for eco-friendly and sustainable fabric materials among environment-conscious consumers is likely to support the segment’s growth over the coming years.

Cotton remains a core material due to its comfort and versatility. It is widely used across multiple apparel categories, supporting consistent demand. Price volatility linked to agricultural output introduces supply-side uncertainty, although consumer preference for natural fibers sustains its relevance.

Wool

Wool is primarily associated with premium apparel and outerwear. Its insulating properties and durability support demand in colder regions, while its premium positioning contributes to higher margins.

Leather

Leather remains concentrated in premium segments, with demand influenced by fashion trends and ethical considerations. The rise of synthetic alternatives is gradually reshaping this segment.

Denim

Denim continues to be a foundational category within casual wear. Its durability and adaptability support sustained demand, with ongoing innovation in finishes and sustainable production methods.

Satin

Satin is used in niche and premium categories, particularly sleepwear and formal apparel. Demand is driven by aesthetic appeal and comfort.

By End-User Analysis

Availability of a Diverse Range of Options to Fuel Demand for Women’s Wear

Women

The women end-user segment dominated the global apparel market with a market share of 41.03% in 2026, and is projected to retain its dominant position during the forecast period. The female fashion industry has experienced a surge in demand compared to men, owing to accessibility to a wide array of clothing collections, including dresses, jeans, skirts, blouses, shorts, leggings, crop tops, bralettes, and scarves, among many others.

The increased demand prompts designers and retailers to prioritize women's fashion, catering to the ever-altering preferences of a large audience. Moreover, their willingness and tendency to invest more in clothing and accessories make women's fashion a more lucrative sector. The segment is expected to dominate the market share of 40.89% in 2025.

Men

Men’s apparel demand is stabilizing with gradual premiumization. Product diversity is expanding, particularly in casual and activewear segments.

Children

Children’s apparel demonstrates steady demand driven by demographic factors and replacement cycles. Growth remains consistent across regions.

Unisex

Unisex apparel is gaining traction, reflecting changing consumer attitudes and simplifying product design strategies. The unisex segment is expected to exhibit the fastest CAGR of 4.41% over the forecast timeframe. The expanding young generation, including Gen Z and Millennials, seeking clothing options that blur the lines between traditional gender categories, boosts the demand for unisex clothing. This transition in customers' preferences has generated a strong demand for unisex clothing across various age groups and demographics.

By Category Analysis

Wide Range of Patterns and Designs to Create Significant Demand for Mass Garments

Based on category, the market is segmented into mass/economy, premium, and luxury.

Mass / Economy

The mass/economy category segment held a market value of 1015.19 in 2026, and is poised to grow continuously over the forecast period. Mass garments are produced in a variety of patterns and designs with shorter turnaround times and affordable pricing, which contributes to higher revenue generation by the segment. The mass segment dominates volume, characterized by affordability and high competition. Efficient supply chains are critical to maintaining margins.

In addition, their easy availability and accessibility encourage consumers to visit stores more often, leading to increased purchases. Fascinatingly, in a mass category, rather than restocking inventory, retailers swap sold-out items with new arrivals, which further prompts purchasing frequency. Moreover, mass options have made fashionable clothing more convenient, offering innovative and stylish options. The segment is expected to dominate the market share of 54.55% in 2025.

Premium

The premium segment is set to flourish at the highest CAGR of 3.98% during the projected years, owing to the growing middle-class population. The growing interaction between consumers and brands through social media platforms and online retail channels is a crucial aspect driving market expansion. Premium apparel is expanding due to rising incomes and aspirational consumption. Product differentiation and brand value drive demand.

Luxury

The luxury segment is estimated to grow at a significant CAGR during the forecast period, owing to the rising number of millionaires and the growing perception among consumers that luxury goods contribute to greater social acceptance. Luxury apparel remains a high-margin segment driven by exclusivity and brand heritage. Demand is concentrated among affluent consumers.

By Distribution Channel Analysis

Availability of Sizable Discounts to Accelerate Product Sales through Supermarkets & Hypermarkets

By distribution channel, the market is segregated into supermarkets & hypermarkets, specialty stores/branded stores, department stores, online/e-commerce, and others.

Supermarkets & Hypermarkets

These channels provide accessibility and competitive pricing, particularly for basic apparel categories. The supermarkets & hypermarkets segment accounted for the largest share of the market in 2023. The availability of sizable discounts makes supermarkets & hypermarkets a prominent distribution platform for apparel worldwide. Brick-and-mortar stores and offline retail formats enable face-to-face interaction, imparting a more personalized experience.

Sales executives present in such stores offer tailored assistance, suggesting styling advice and complementary items, and address any related concerns that further add to the experience. Consumers can touch and feel the fabric's quality, examine the craftsmanship, and have a trial experience to assess the clothing. The segment is expected to dominate the market share of 32.73% in 2025.

Specialty Stores / Branded Stores

Specialty stores support brand positioning and customer experience, particularly in premium and luxury segments.

Department Stores

Department stores remain relevant but face declining market share due to changing retail dynamics.

Online / E-commerce

E-commerce is the fastest-growing channel, enabling global reach and personalized shopping experiences. It is reshaping the apparel market growth and competitive dynamics. The online/e-commerce segment is forecast to grow tremendously. This segment is anticipated to exhibit a CAGR of 4.42% during the forecast period. Online shopping platforms have made it easier for consumers to access a wide variety of clothing and shop from the comfort of their homes. The shopping experience has become hassle-free by offering the convenience of adding a list of shipping addresses and varying payment options, thus further intensifying the growth of the market. Along with traditional retail channels, brands are focusing on expanding in the online apparel retailing market and direct-to-consumer models in order to establish a direct relationship with customers, enabling personalized marketing and better consumer insights and feedback.

REGIONAL INSIGHTS

Geographically, the market is divided into North America, South America, Europe, Asia Pacific, and the Middle East & Africa.

Asia Pacific Apparel Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia-Pacific Apparel Market Analysis

Asia Pacific accounted for the largest market share and gained the highest revenue in 2023. The regional market value in 2024 was USD 712.76 billion, and in 2023, the market value led the region by USD 687.72 billion. The large audience base is the primary reason driving the regional growth. Growing disposable income, increasing middle-class population, increase in the number of working women professionals, and rising participation of individuals in sports and other outdoor activities are among the few factors fueling the Asia Pacific market growth.

A significant number of young individuals embrace online shopping, leading to a substantial increase in garment sales by giants such as Tokopedia, Lazada, and Shopee. This trend highlights the evolving consumer demands and underscores the pivotal role of technology in shaping the industry landscape. The Japanese market is projected to reach USD 98.33 billion by 2026. The Chinese market is projected to reach USD 376.81 billion by 2026. The Indian market is projected to reach USD 141.06 billion by 2026.

Various cultures and styles influence the Asian market, offering lucrative growth opportunities for manufacturers to innovate their product offerings. Furthermore, the rapidly evolving trend of minimalist fashion creates an opportunity for fashion brands known for their simple yet elegant designs to stay competitive, favoring global market growth.

- In the Asia Pacific, the Casual Wear/Fashion Wear segment is estimated to hold a 36.36% market share in 2024.

Asia-Pacific represents the fastest-growing apparel market, driven by urbanization, rising disposable incomes, and expanding middle-class populations. Demand is highly diverse, reflecting regional cultural influences and varying economic conditions. E-commerce adoption is accelerating, particularly in emerging markets. The region contributes significantly to global apparel market growth, supported by large-scale manufacturing capabilities and increasing consumer spending across multiple apparel categories. In 2025, Asia Pacific generated USD 740.26 billion, contributing 41.03% to global market revenue, and is projected to grow to USD 769.67 billion in 2026.

Japan Apparel Market

Japan’s apparel market is mature, with demand driven by quality, design, and brand reputation. Consumers prioritize craftsmanship and functional innovation, supporting premium segments. Aging demographics influence purchasing patterns, shifting focus toward comfort and practicality. The market maintains stability despite limited population growth, with brands emphasizing product differentiation and efficient retail strategies to sustain apparel market share within a competitive landscape.

China Apparel Market

China represents a major contributor to the global apparel market size, supported by rapid urbanization and an expanding consumer base. Demand is shifting toward premium and branded products, reflecting rising incomes and evolving preferences. Domestic brands are gaining market share alongside international players. E-commerce dominance and digital ecosystems are reshaping retail strategies, enabling companies to scale efficiently and capture growth opportunities across diverse consumer segments.

To know how our report can help streamline your business, Speak to Analyst

Europe Apparel Market Analysis

Europe is growing rapidly as the third-largest market with a value of USD 432.30 billion in 2025, driven by multiple factors, including the rising emphasis on sustainability, shifting fashion trends, expansion of e-commerce channels, and innovation in manufacturing and design techniques. The UK market is projected to reach USD 94.77 billion by 2026. The German market is projected to reach USD 83.51 billion by 2026. Europe maintained a strong presence in the global market, reaching USD 432.3 billion in 2025, accounting for 23.96% share, and is expected to reach USD 445.03 billion in 2026.

Europe’s apparel market is characterized by diverse consumer preferences and strong regulatory emphasis on sustainability. Demand is influenced by fashion innovation, particularly in premium and luxury segments. Environmental compliance and circular economy initiatives are reshaping production and sourcing strategies. The region maintains a stable apparel market share, supported by established brands and evolving retail models integrating physical and digital channels across multiple countries.

Germany Apparel Market

Germany represents a key European apparel market, driven by strong purchasing power and structured retail networks. Demand trends emphasize quality, durability, and sustainability, with consumers demonstrating cautious spending behavior. The market shows steady growth, supported by both domestic brands and international players. E-commerce expansion and logistics efficiency are enhancing distribution capabilities, enabling companies to maintain competitive positioning within the broader European apparel market.

United Kingdom Apparel Market

The United Kingdom apparel market reflects a dynamic retail environment shaped by fast fashion and digital transformation. Consumer demand is highly trend-driven, with rapid adoption of new styles and online purchasing channels. Economic uncertainties influence pricing sensitivity, encouraging discount-driven sales strategies. Despite these challenges, the market maintains stable growth, supported by innovation in retail formats and the strong presence of global and domestic fashion brands.

South America

The South America market was valued at USD 4.71 billion in 2025, capturing 11.08% of global revenue, and is estimated to reach USD 5.04 billion in 2026.

North America Apparel Market Analysis

North America is anticipated to grow significantly over the forecast period, led by the U.S. North America is anticipated to account for the second-highest market size of USD 466.78 billion in 2025, exhibiting the second-fastest growing CAGR of 2.8% during the forecast period. The emergence of the athleisure trend positively influences the North American market trends. At a macro level, the increasing demand for sportswear and active wear fuels the regional market growth. The U.S. market is projected to reach USD 399.77 billion by 2026. The North America region captured 25.87% of the global market in 2025, generating USD 466.78 billion in revenue, and is projected to reach USD 478.58 billion in 2026.

North America maintains a mature yet resilient apparel market, supported by high consumer spending and strong retail infrastructure. Demand is shaped by premiumization, sustainability awareness, and rapid digital adoption. E-commerce penetration continues to expand, influencing distribution strategies. The region demonstrates steady apparel market growth, with brands focusing on supply chain optimization and direct-to-consumer models to sustain market share amid evolving consumer expectations and pricing pressures.

United States Apparel Market

The United States dominates the regional apparel market size, driven by a large consumer base and high discretionary spending. Demand reflects a strong preference for casual wear and activewear, alongside growing interest in sustainable products. Digital retail channels continue to reshape purchasing behavior. Market competition remains intense, with both global brands and emerging direct-to-consumer players competing on pricing, innovation, and customer experience differentiation strategies across segments.

Middle East & Africa and Latin America Apparel Market Analysis

Latin America’s apparel market demonstrates moderate growth, influenced by economic variability and evolving consumer behavior. Demand is concentrated in mass and mid-range segments, reflecting price sensitivity. Retail infrastructure is improving, supporting the gradual expansion of organized retail and e-commerce channels. Despite economic challenges, the market offers growth potential through urbanization and increasing adoption of digital retail platforms across key countries. Middle East & Africa recorded a market size of USD 96.23 billion in 2025, capturing 5.33% of the global market share, and is projected to reach USD 99.33 billion in 2026.

South America and the Middle East & Africa are growing at a considerable rate due to the increasing popularity of sustainable clothing. The Middle East & Africa is expected to be USD 96.23 billion in 2025 as the fourth-largest market. The UAE market size is likely to be valued at USD 28.85 billion in 2025. Furthermore, increasing apparel imports make these regional markets attractive for international businesses to penetrate in the coming years.

The Middle East and Africa apparel market is characterized by diverse consumption patterns and strong cultural influences. Demand varies significantly across regions, with premium segments expanding in urban centers. Retail development and e-commerce adoption are supporting market growth. However, economic disparities and supply chain challenges continue to influence overall apparel market dynamics and expansion potential.

Competitive Landscape

KEY INDUSTRY PLAYERS

Key Players Employ Multiple Growth Strategies to Stay Competitive

The global market is highly competitive and fragmented, with a large number of domestic and international players. Market players are undertaking several organic and inorganic growth strategies to compete and have a strong foothold within the industry. These strategies include geographical expansion, product innovation and launch, merger, partnership agreement, or acquisition, among many others. The deeply rooted distribution network of global brands influences the international market but faces steep competition from local manufacturers. Some industry players also invest in digital capabilities and increase their reach through social media and other online platforms to stay competitive. Celebrity and influencer marketing are one of their strengths, enabling them to reach a wider audience.

The apparel market is highly fragmented, characterized by the coexistence of global conglomerates, regional brands, and emerging direct-to-consumer players. Competitive positioning varies significantly across segments, with scale, brand equity, and supply chain efficiency serving as primary differentiators.

Global players maintain strong apparel market share through diversified portfolios and extensive distribution networks. These companies leverage vertical integration, enabling tighter control over sourcing, production, and retail operations. Their ability to respond quickly to shifting fashion trends supports sustained market leadership, particularly in fast fashion and premium segments.

Mid-sized and regional players compete through localized strategies, focusing on cultural relevance, pricing flexibility, and targeted product offerings. These firms often demonstrate stronger adaptability to regional demand patterns, allowing them to capture niche market segments. However, limited scale can constrain their ability to compete on cost and global brand visibility.

The emergence of direct-to-consumer brands is reshaping the competitive landscape. These players prioritize digital engagement, data-driven decision-making, and lean operational models. By bypassing traditional retail channels, they improve margin structures while gaining direct access to consumer insights. This model is particularly effective in premium and niche segments where brand differentiation is critical.

Strategic partnerships and collaborations are increasingly used to enhance competitive positioning. Apparel companies are partnering with technology providers, logistics firms, and sustainability-focused organizations to strengthen supply chains and improve product offerings. Collaborations with designers and influencers also play a role in driving brand visibility and consumer engagement.

Competition is intensifying as sustainability and transparency become central to purchasing decisions. Companies that invest in ethical sourcing, circular production models, and digital transformation are better positioned to capture long-term apparel market growth. At the same time, pricing pressure and inventory management challenges continue to influence profitability across the industry.

List of Top Apparel Companies:

- VF Corporation (U.S.)

- Burberry Group plc (U.K.)

- Puma SE (Germany)

- Adidas AG (Germany)

- Nike Inc. (U.S.)

- H&M Hennes & Mauritz AB (Sweden)

- LVMH (France)

- KERING (France)

- PVH Corp. (U.S.)

- Inditex (Spain)

Recent Apparel Industry Key Developments

- January 2025: Nike, Inc. expanded its digital retail ecosystem by integrating advanced demand forecasting tools to improve inventory allocation and reduce overproduction, supporting operational efficiency and enhancing direct-to-consumer capabilities through data analytics and artificial intelligence-driven merchandising systems.

- March 2025: Inditex S.A. accelerated its nearshoring strategy by increasing production capacity in Europe to reduce lead times and improve supply chain responsiveness, leveraging advanced manufacturing processes and digital supply chain integration technologies to align with fast-changing consumer demand patterns.

- September 2024: H&M Group introduced a circular fashion initiative focused on large-scale garment recycling and resale platforms, aiming to strengthen its sustainability positioning while incorporating textile recycling technologies and digital traceability systems to enhance transparency across its supply chain.

- June 2024: Adidas AG launched a new line of performance apparel utilizing bio-based and recycled materials, targeting reduced environmental impact while maintaining product performance standards through material innovation and advanced textile engineering techniques.

- November 2024: PVH Corp. implemented an enterprise-wide digital transformation program to enhance omnichannel capabilities, integrating customer data platforms and advanced analytics tools to improve personalization, inventory visibility, and overall retail efficiency across global operations.

REPORT COVERAGE

The research report provides a detailed analysis of the market and focuses on key aspects such as the competitive landscape, regional analysis, and leading product types. Besides this, the report offers market insights and highlights key industry developments. In addition to the aforementioned factors, the market report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

CAGR of 3.65% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Material

|

|

|

By End-User

|

|

|

By Category

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global apparel market size was valued at USD 1,862.36 billion in 2026 and is projected to reach USD 2,481.51 billion by 2034, growing at a CAGR of 3.65% during the forecast period.

The market will exhibit a CAGR of 3.65% during the forecast period (2026-2034).

Key growth drivers include the rise of fast fashion, increased e-commerce penetration, a growing middle-class population in emerging economies, and a strong consumer shift toward sustainable and ethical clothing.

The Asia Pacific region leads the global apparel market, accounting for over 41.03% of the global share in 2025, fueled by rising disposable income, youth demographics, and rapid digital adoption in countries like China and India.

The market is segmented by type (casual wear, formal wear, sportswear), material (cotton, synthetic, wool), end-user (men, women, unisex), category (mass, premium, luxury), and distribution channel (offline retail, e-commerce, supermarkets).

Sportswear and activewear is the fastest-growing apparel segment, driven by rising health awareness, gym culture, and demand for athleisure that blends performance and fashion.

Sustainability is transforming the apparel industry, with brands investing in eco-friendly materials, ethical supply chains, clothing recycling, and secondhand/resale platforms to meet consumer expectations and regulatory standards.

Technology enables innovation through smart textiles, 3D printing, AI-powered design tools, and virtual try-ons, improving customer experience, product customization, and supply chain efficiency.

- 2021-2034

- 2025

- 2021-2024

- 170

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us