Bicycle Gear Shifter Market Size, Share & Industry Analysis, By Product (Trigger (Rapidfire) Shifters, Twist (Grip) Shifters, Bar-End Shifters, Electronic, and Others), By Technology (Mechanical, Electronic, and Hydraulic), By Bicycle Type (Mountain, Road, Hybrid, Cargo, and Others), By Material (Aluminum, Steel, and Others) and Regional Forecast, 2026-2034

Bicycle Gear Shifter Market Size and Future Outlook

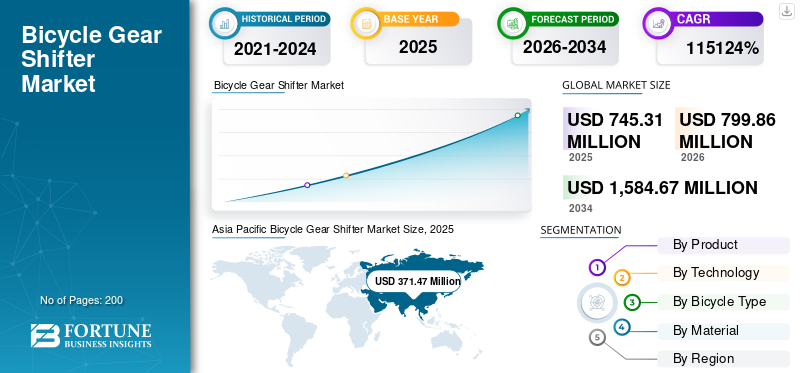

The global bicycle gear shifter market size was valued at USD 745.31 million in 2025. The market is projected to grow from USD 799.86 million in 2026 to USD 1,584.67 million by 2034, exhibiting a CAGR of 8.9% during the forecast period. Asia Pacific dominated the bicycle gear shifter market with a market share of 49.84% in 2025.

The bicycle gear shifter market refers to the global industry that designs, manufactures, and sells precise gear shifting systems for bicycles to control drivetrain gear changes. It includes mechanical and electronic shifters, such as trigger, twist, and thumb shifters, as well as integrated brake-shift levers. The market serves road, mountain, hybrid, gravel, and e-bikes across OEM and aftermarket channels, driven by cycling adoption, performance innovation, and demand for precision shifting technologies.

Key market drivers include rising global cycling participation for fitness and commuting, growing demand for high-performance and lightweight components, increasing adoption of e-bikes, technological advancements such as electronic shifting systems, expanding urban mobility initiatives, and strong aftermarket demand for upgrades, replacements, and performance customization.

Key players in the market include Shimano Inc., SRAM LLC, Campagnolo S.r.l., MicroSHIFT, FSA (Full Speed Ahead), Rotor Bike Components, and Box Components, competing through precision engineering, lightweight designs, electronic shifting technologies, drivetrain integration, and performance-focused innovations to enhance durability, responsiveness, and rider experience across road, mountain, gravel, and e-bike segments.

Download Free sample to learn more about this report.

BICYCLE GEAR SHIFTER MARKET TRENDS

Integration of Wireless and Smart Shifting Technologies to Transform Rider Experience

A prominent trend in the market is the integration of wireless and smart shifting technologies. Leading manufacturers are increasingly introducing battery-powered, app-connected systems that offer precise, low-maintenance, and customizable shifting performance. Wireless designs reduce cable clutter, improve aerodynamics, and simplify installation. Some advanced systems enable firmware updates, shift mapping customization, and performance tracking through companion mobile applications. Integration with e-bike drive units and power meters is further enhancing system intelligence. As digital ecosystems expand in cycling, riders are showing greater interest in connected components that enhance both performance analytics and user friendly convenience. This technological evolution is redefining drivetrain architecture, encouraging premiumization, and setting new benchmarks for precision, efficiency, and seamless gear transitions.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Cycling Participation and E-Bike Adoption to Accelerate Component Demand

The growing global shift toward cycling experiences for fitness, recreation, and daily commuting is a primary driver of the market. Urban congestion, fuel price volatility, and growing environmental awareness are encouraging consumers to adopt bicycles as a sustainable mobility alternative. Additionally, the rapid expansion of the e-bike segment is significantly boosting demand for technologically advanced, durable gear shifting systems capable of handling higher torque and varied terrain. Governments across Europe, North America, and parts of Asia are investing in cycling infrastructure, further supporting bicycle sales. As participation in road, mountain, and gravel cycling disciplines increases, demand for reliable, precise, and lightweight gear shifters continues to rise across both OEM and aftermarket channels, strengthening long-term bicycle gear shifter market growth prospects.

For instance, in October 2025, the European Commission published its first progress report on the European Declaration on Cycling, signaling sustained momentum on cycling policies and infrastructure that support ridership growth.

MARKET RESTRAINTS

High Cost of Advanced Electronic Shifting Systems to Limit Mass Adoption

While technological advancements have improved shifting precision and rider experience, the high cost of electronic and wireless gear shifting systems remains a key restraint. Premium drivetrains equipped with electronic shifters significantly increase the overall bicycle price, limiting adoption among price-sensitive consumers, particularly in developing regions. Maintenance and replacement costs for advanced systems can also be higher than those of mechanical alternatives, discouraging entry-level and mid-range buyers. Furthermore, compatibility concerns between drivetrain components may restrict upgrades without replacing entire groupsets, adding to consumer expenses. Although professional and enthusiast cyclists continue to adopt these innovations, affordability barriers prevent widespread penetration across commuter and recreational segments. This pricing challenge slows volume growth in cost-conscious markets despite strong technological progress and product differentiation strategies by leading manufacturers.

MARKET OPPORTUNITIES

Expansion of Aftermarket Upgrades and Customization to Create Revenue Opportunities

The growing culture of bicycle customization and performance enhancement presents a significant opportunity for gear shifter manufacturers. Enthusiasts increasingly seek lightweight, high-precision, and aesthetically appealing components to improve riding performance and personalize their bicycles. The aftermarket segment allows riders to upgrade from entry-level mechanical shifters to premium mechanical or electronic systems without buying a new bicycle. Additionally, gravel cycling, bikepacking, and competitive amateur racing are encouraging component-level upgrades. E-commerce platforms and direct-to-consumer sales channels are further expanding access to premium drivetrain components globally. As cycling communities expand and digital product awareness improves, manufacturers can capitalize on modular upgrades, enhanced compatibility solutions, and mid-range electronic systems tailored to performance-focused yet value-conscious riders.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Supply Chain Volatility and Component Standardization Issues to Pressure Manufacturers

The bicycle gear shifter market faces ongoing challenges related to supply chain volatility and limited standardization across drivetrain systems. Fluctuations in raw material prices, semiconductor shortages for electronic systems, and global logistics disruptions can impact production timelines and profit margins. Additionally, proprietary drivetrain standards among major manufacturers restrict cross-brand compatibility, complicating inventory management for retailers and limiting flexibility for consumers. Smaller manufacturers may struggle to scale production while maintaining quality and competitive pricing. As innovation cycles shorten and product complexity increases, companies must balance R&D investments with supply stability. Managing cost efficiency while ensuring consistent product availability remains critical to sustaining competitiveness in an increasingly technology-driven, globally distributed market landscape.

Segmentation Analysis

By Product

Widespread OEM Integration and Performance Versatility to Strengthen Trigger (Rapidfire) Shifters Segment Dominance

Based on product, the market is divided into trigger (rapidfire) shifters, twist (grip) shifters, bar-end shifters, electronic and others.

Trigger (rapidfire) shifters held the largest bicycle gear shifter market share due to their widespread adoption across mountain, hybrid, and entry-to-mid-range road bicycles. Their ergonomic design, quick multi-gear shifting capability, and compatibility with leading drivetrain systems make them the preferred choice among OEM manufacturers. Strong penetration in performance and recreational cycling segments ensures steady replacement demand and consistent volume sales across global markets.

Electronic shifters represent the fastest-growing segment, projected to expand at a CAGR of 10.2% over the forecast period. Increasing demand for wireless precision shifting, premium bicycles, and growing e-bike integration are accelerating adoption, particularly in competitive cycling and high-end enthusiast segments worldwide.

By Technology

Cost Efficiency and Wide Compatibility to Sustain Mechanical Shifters Segment Dominance

In terms of technology, the market is categorized into mechanical, electronic and hydraulic.

Mechanical shifters dominate the market due to their affordability, reliability, and broad compatibility across entry-level to mid-range bicycles. They require minimal maintenance, are easy to service, 11 in commuter, recreational, and developing markets. Strong OEM penetration and replacement demand across mountain, road, and hybrid bicycles continue to support stable volume sales globally.

Electronic shifters represent the fastest-growing segment, projected to expand at a CAGR of 11.0% during the forecast period. Rising demand for wireless precision shifting, improved drivetrain efficiency, and premium bicycle adoption especially in e-bikes and competitive cycling are accelerating electronic system integration across developed markets.

To know how our report can help streamline your business, Speak to Analyst

By Bicycle Type

Urban Commuting Expansion and Versatile Usage to Reinforce Hybrid Bicycle Segment Dominance

Based on bicycle type, the market is segmented into mountain, road, hybrid, cargo, and others.

The hybrid bicycle segment dominates the market due to its versatility for urban commuting, recreational riding, and light touring. Hybrid bicycles combine comfort and performance, attracting a broad consumer base including daily commuters and fitness riders. High global sales volumes, especially in urban markets, ensure steady OEM demand for durable and cost-effective gear shifters. Their widespread adoption in rental fleets and shared mobility programs further strengthens consistent replacement and servicing demand, supporting sustained segmental leadership.

The road segment is the fastest growing, projected to expand at a CAGR of 10.1% over the forecast period. The segmental growth is driven by rising participation in endurance cycling and competitive events. Increasing demand for lightweight performance components and premium drivetrains is expected to propel the segment at a strong CAGR over the forecast period.

By Material

Lightweight Performance and Corrosion Resistance to Drive Aluminum Segment Dominance

Based on material, the market is segmented into aluminum, steel and others.

The aluminum segment dominates the market owing to its superior strength-to-weight ratio, corrosion resistance, and cost-effectiveness. Manufacturers widely prefer aluminum for shifter bodies and levers to ensure durability while maintaining lightweight performance, particularly in road, mountain, and hybrid bicycles. Its machinability and compatibility with precision engineering processes further support large-scale OEM production. Growing consumer preference for lightweight components in both mid-range and premium bicycles continues to reinforce aluminum’s leading market share globally.

Steel represents the second-largest segment, supported by its high tensile strength and durability. It is commonly used in internal components and entry-level shifters where cost efficiency and structural robustness are prioritized over weight reduction.

Bicycle Gear Shifter Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Bicycle Gear Shifter Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to its strong bicycle manufacturing base in China, Japan, and Taiwan, as well as expanding cycling adoption across India and Southeast Asia. The region benefits from high OEM production volumes and growing urban commuting trends. Government initiatives promoting sustainable mobility and the rapid expansion of the e-bike market further strengthen demand. Rising middle-class income levels and increasing participation in recreational cycling position the Asia Pacific as the fastest-growing region over the forecast period.

China Bicycle Gear Shifter Market

China’s market in 2026 is estimated at around USD 140.00 million, accounting for a significant share of global market revenues. Strong EV production, expanding automotive manufacturing capacity, and rising demand for advanced electrical architectures continue to drive relay integration across passenger and commercial vehicles.

India Bicycle Gear Shifter Market

The Indian market in 2026 is estimated at around USD 109.64 million, accounting for a notable share of global market revenues. Rapid vehicle electrification, growing domestic manufacturing, and increasing adoption of safety and comfort electronics position India as the fastest-growing regional market.

Europe

Europe holds the second-largest share of the market, supported by a well-established cycling culture and strong demand for high performance bicycles. Countries such as Germany, the Netherlands, France, and Italy drive consistent sales across road, mountain, and e-bike categories. Robust cycling infrastructure, environmental regulations, and government incentives for e-bikes support steady market expansion. Premium component adoption and technological upgrades are prominent in this region. Europe is projected to grow at a CAGR of 7.8% during the forecast period.

Germany Bicycle Gear Shifter Market

The Germany market in 2026 is estimated at around USD 23.54 million, accounting for a steady share of global market revenues. Strong premium vehicle production, advanced automotive electronics integration, and focus on EV innovation sustain consistent relay demand across OEM platforms.

Italy Bicycle Gear Shifter Market

The Italian market in 2026 is estimated at around USD 37.55 million, accounting for a moderate share of global market revenues. Growth is supported by specialized automotive manufacturing, rising hybrid vehicle adoption, and increasing demand for compact electrical control systems.

North America

North America represents the third-largest market, driven by increasing participation in mountain biking, gravel cycling, and endurance road events. The U.S. leads regional demand, supported by growing interest in outdoor recreation and fitness-oriented lifestyles. The rising penetration of high-end bicycles and e-bikes encourages adoption of advanced mechanical and electronic shifting systems. Additionally, strong aftermarket sales and customization trends contribute to stable growth across enthusiast and professional rider segments.

U.S. Bicycle Gear Shifter Market

The U.S. market in 2026 is estimated at around USD 111.36 million, accounting for a considerable share of global market revenues. Expanding EV production, advanced driver assistance systems, and strong light truck and SUV sales continue driving relay integration across vehicle platforms.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, presents emerging opportunities in the market. Growing urbanization, rising awareness of affordable mobility solutions, and expanding sports cycling communities support gradual demand growth. While adoption remains comparatively low compared to developed regions, improvements in distribution networks and increased availability of mid-range bicycles are strengthening market penetration. Infrastructure development and tourism-driven cycling activities further contribute to long-term expansion potential.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Brand Strength Intensifying Competitive Rivalry in the Market

The bicycle gear shifter market is moderately consolidated, with global leaders such as Shimano Inc., SRAM LLC, and Campagnolo S.r.l. holding significant market share due to strong brand recognition, integrated drivetrain ecosystems, and extensive distribution networks. These companies compete through continuous innovation in lightweight materials, wireless electronic shifting, and improved drivetrain compatibility. Their ability to offer complete groupsets enhances customer loyalty and OEM partnerships. Mid-tier players such as MicroSHIFT and Box Components compete by providing cost-effective yet performance-oriented alternatives, particularly targeting entry-level and value-conscious segments across emerging markets.

Competition is increasingly driven by technological differentiation, supply chain resilience, and expansion into e-bike-compatible shifting systems. Companies are investing heavily in research and development to enhance precision, durability, and smart connectivity features while maintaining cross-platform compatibility. Strategic partnerships with bicycle manufacturers strengthen OEM penetration, while growing e-commerce platforms support direct-to-consumer aftermarket growth. Price competitiveness shapes emerging markets, whereas premiumization and wireless system integration define mature regions. Innovation speed and brand positioning remain decisive for sustaining long-term competitive advantage.

LIST OF KEY BICYCLE GEAR SHIFTER COMPANIES PROFILED

- Shimano Inc. (Japan)

- SRAM LLC (U.S.)

- Campagnolo S.r.l. (Italy)

- MicroSHIFT (U.S.)

- SunRace (Taiwan)

- LTWOO (China)

- Box Components (U.S.)

- Rohloff GmbH & Co. KG (Germany)

- Sturmey-Archer (U.K.)

- Paul Components (Paul Component Engineering) (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Shimano Inc. expanded its mid-range wireless Di2 portfolio, introducing updated 12-speed electronic shifting systems targeting performance road and gravel bicycles to strengthen its premium component positioning globally.

- November 2025: SRAM LLC launched an enhanced AXS wireless firmware platform, enabling improved shift customization and battery optimization across its road and mountain electronic drivetrain systems.

- October 2025: Campagnolo S.r.l. unveiled an upgraded Super Record wireless groupset with aerodynamic refinements and expanded gravel compatibility, reinforcing its presence in the high-performance cycling segment.

- August 2025: MicroSHIFT introduced a new lightweight 11-speed mechanical shifter series designed for urban and trekking bicycles, focusing on durability and affordability in emerging markets.

- June 2025: Shimano announced the expansion of its Deore XT Di2 lineup for mountain bikes, integrating enhanced wireless communication and improved e-bike drivetrain compatibility.

- March 2025: Box Components launched a performance-focused trigger shifter upgrade kit targeting competitive BMX and mountain biking segments across North America.

- December 2024: Campagnolo expanded distribution partnerships in the Asia Pacific to increase availability of its electronic road shifters amid rising regional cycling demand.

REPORT COVERAGE

The global bicycle gear shifter market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.9% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Product, By Technology, By Bicycle Type, By Material, and By Region |

| By Product |

|

| By Technology |

|

| By Bicycle Type |

|

| By Material |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 745.31 million in 2025 and is projected to reach USD 1,584.67 million by 2034.

In 2025, the Asia Pacific’s market value stood at USD 371.47 million.

The market is expected to exhibit a CAGR of 8.9% during the forecast period.

The hybrid segment is leading the market by bicycle type.

Rising global cycling participation and e-bike adoption are the key factors driving the market growth.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us