Biofortification Market Size, Share & Industry Analysis, By Crop Type (Cereals & Grains [Rice, Wheat, Corn, Millets, and Others], Roots & Tubers, Pulses & Legumes, and Oilseeds), By Target Nutrient (Zinc, Iron, Vitamins, Amino Acids, and Others), By Technology (Conventional Breeding, Agronomic Practices, and Genetic Engineering), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

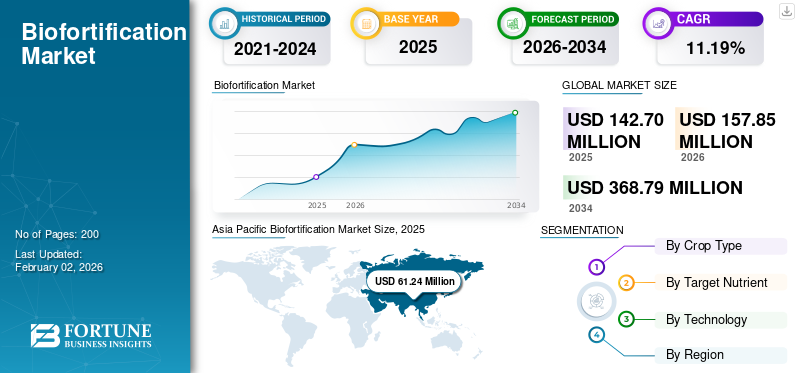

Biofortification Market Size and Future Outlook

The global biofortification market size was valued at USD 142.70 million in 2025. The market is projected to grow from USD 157.85 million in 2026 to USD 368.79 million by 2034, exhibiting a CAGR of 11.19% during the forecast period. Asia Pacific dominated the global biofortification market with a market share of 42.92% in 2025.

The global biofortification market is expected to grow steadily, driven by rising micronutrient deficiencies, increasing focus on food systems security, and strong government and institutional support for nutrient-enriched crops. Biofortification, enhancing the micronutrient content of crops through breeding, agronomic practices, or genetic engineering, plays a vital role in addressing “hidden hunger.” Growing consumer interest in functional nutrition, government-backed nutrition interventions, and the increasing burden of anaemia, zinc deficiency, and immune-related disorders further support the global market. The private sector in the global market is increasingly investing in research collaborations and seed development to expand the commercial adoption of nutrient-enriched crops.

Major players in the global market include Bayer AG, Syngenta Group, Corteva Agriscience, DuPont, and BASF SE. These organisations collectively drive the development and distribution of biofortified seeds, conduct crop trials, enhance nutrients, develop global distribution models, and implement commercialisation strategies across cereals, pulses, and tubers.

Download Free sample to learn more about this report.

Biofortification Market Takeaways

- 2025 Market Size: USD 142.70 million

- 2026 Market Size: USD 157.85 million

- 2034 Forecast Market Size: USD 368.79 million

- CAGR: 11.19% from 2026–2034

- Asia Pacific dominated the biofortification market with a 42.92% share in 2025.

- Cereals & grains remained the leading segment and are projected to grow at a CAGR of 11.48%.

- Conventional breeding remains the dominant technology segment, expanding at a CAGR of 11.23%.

North America

North America is projected to grow at a CAGR of 10.92%, driven by rising demand for functional and fortified food products.

Europe

Europe is expected to expand at a CAGR of 10.46%, supported by demand for nutrient-rich grains and favorable regulations.

Asia Pacific

Asia Pacific led the global market in 2025 and is projected to grow at a strong CAGR of 11.87% through 2034.

U.S.

Growth is supported by increasing adoption of vitamin A-enriched sweet potatoes and iron-fortified beans in food programs and commercial products.

Japan

Demand is expected to benefit from increasing consumer focus on nutrition-rich foods and preventive healthcare initiatives.

Read More

MARKET DYNAMICS

Market Drivers

Rising Global Burden of Micronutrient Deficiencies Accelerates to Support Market Growth

Biofortified crops are gaining momentum as a key strategy to address the rising global burden of micronutrient deficiencies, which affect more than 2 billion people globally, as reported by the Food and Agriculture Organization (FAO) and the World Health Organization (WHO). Micronutrient deficiencies, commonly known as "hidden hunger", can lead to severe health consequences, including impaired cognitive development, weakened immune systems, and increased risk of mortality, especially among children and women in developing regions. The most prevalent deficiencies include iron (leading to anaemia), zinc (impairing growth and immunity), and vitamin A (causing blindness and increased susceptibility to infections).

- According to the National Institutes of Health (NIH), a study in rural Madagascar found high prevalences of nutrient deficiencies, particularly zinc, with 66.5% of the population estimated to be deficient. Other concerns included vitamin B12 deficiency at 15.6% (3.6% without inflammation), vitamin A (retinol) deficiency at 11.6%, and iron deficiency at 11.7% (ferritin) and 2.3% (soluble transferrin receptors).

Market Restraints

Regulatory Constraints and Long Variety Approval Cycles to Restrain Growth

Regulatory constraints and long approval cycles for new crop varieties are considerable barriers hindering the global biofortification market growth. These regulatory challenges introduce delays in launching biofortified seeds and restrict access for farmers and consumers, especially where differing standards, certification requirements, and trade policies occur between countries. A lack of harmonized standards and regulations for biofortified seeds and end-products often means longer assessment and implementation timelines, especially when exporting or distributing crops internationally. Addressing these regulatory and approval obstacles is essential for scaling the market and maximising its contribution to global nutritional security.

Market Opportunities

Integration of Biofortified Crops Into Functional Foods and Nutraceuticals to Unlock New Growth Opportunities

Integrating biofortified crops into functional foods and nutraceuticals offers significant new growth opportunities by enhancing the nutritional profile of these products to address micronutrient deficiencies and improve health outcomes. Biofortified crops, which are conventionally bred or genetically enhanced to have higher levels of essential micronutrients such as iron, zinc, and vitamin A, can be used as ingredients in functional foods and nutraceutical formulations targeting specific health concerns. Advanced breeding techniques and gene editing technologies are improving the efficiency of producing biofortified crops, making them more accessible for food industry applications. Programs such as HarvestPlus have facilitated the commercial availability and adoption of these crops, aligning breeding goals with the nutritional needs and preferences of consumers and farmers.

- For instance, in 2024, HarvestPlus launched a major biofortification project to address hidden hunger in Bangladesh and Uganda, targeting high rates of micronutrient deficiencies in rural and poverty-affected regions in both countries. The initiative leverages biofortified staple crops, such as zinc-enriched rice in Bangladesh and vitamin A maize, vitamin A sweet potato, and iron beans in Uganda, to improve nutrition security and address the lack of essential vitamins and minerals in daily diets, which leads to health issues such as stunting and weakened immunity.

Biofortification Market Trends

Expansion of High-Zinc and High-Iron Food Staples to Shape Industry

The expansion of high-zinc and high-iron food staples is indeed a recent and significant trend in the global market. Biofortification enhances the micronutrient content of staple foods, such as rice, wheat, and maize, with a focus on increasing zinc and iron levels to address widespread deficiencies and improve health outcomes. This approach is gaining traction as a sustainable and cost-effective solution to combat malnutrition, especially in developing countries.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Crop Type

Cereals & Grains Maintain Leading Share Driven by High Global Consumption

By crop type, the market is segmented into cereals & grains, roots & tubers, pulses & legumes, and oilseeds.

Cereals & grains represented the dominant category, rising from USD 113.08 million in 2025 to USD 299.09 million by 2034, at a CAGR of 11.48%. The cereal segment, which also includes rice, wheat, corn, millets, and other grains, holds a significant global biofortification market share due to its staple role in diets, particularly in developing regions. Biofortified cereals such as iron-fortified millet, vitamin A maize, and zinc-enriched rice have seen increased adoption supported by health programs and government initiatives globally. This institutional and consumer demand contributes to the robust market expansion at the noted CAGR.

The pulses & legumes segment is expected to grow at a relatively higher CAGR over the forecast period, with a CAGR of 10.83%.

To know how our report can help streamline your business, Speak to Analyst

By Target Nutrient

Zinc Dominates Market Due to Widespread Global Zinc Deficiency

On the basis of target nutrient, the market is segmented into zinc, iron, vitamins, amino acids, and others.

Zinc is described as a rapidly expanding targeted nutrient segment in the global market, with its value rising from about USD 76.50 million in 2026 to roughly USD 180.58 million by 2034 at an implied CAGR of around 11.33%. This positions zinc among the higher‑growth nutrient categories within biofortification, reflecting sustained emphasis on addressing zinc deficiency through staple crops. Zinc-biofortified crops are gaining traction as zinc deficiency is linked to immune dysfunction, impaired growth, and cognitive issues in large populations, especially in low- and middle-income countries.

- The vitamins segment is expected to grow significantly at a CAGR of 12.18% during the forecast period.

By Technology

Conventional Breeding Leads Due to Policy Push & Wide Acceptance

By technology, the market is divided into conventional breeding, agronomic practices, and genetic engineering.

Conventional breeding is projected to grow from approximately USD 116.60 million in 2026 to roughly USD 273.14 million by 2034, implying a CAGR of nearly 11.23%, and remains the leading technology in the global market. Regulators and consumers widely accept this approach as a non-GMO method that relies on selecting and crossing nutrient-dense varieties naturally, making approvals and deployment faster across regions.

- The genetic engineering segment is anticipated to grow at a CAGR of 12.16% during the forecast period.

Biofortification Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Biofortification Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific leads the global market, with a market size projected to grow from about USD 61.24 million in 2025 to USD 167.17 million by 2034, reflecting a compound annual growth rate (CAGR) of approximately 11.87%. The strong adoption of biofortified staples, such as rice, wheat, and maize, in populous countries, including India, China, Bangladesh, Indonesia, and Vietnam, drives this leading position. Biofortification initiatives aim to enhance crop nutritional quality, driving growth and innovation in the global market.

South America

South America is one of the fastest-growing regions in the market, with a projected CAGR of approximately 11.43%. This growth is driven by increasing adoption of biofortification programs focused on staple crops such as maize, beans, and cassava in countries such as Brazil, Colombia, and Peru. Brazil is a key market, exhibiting rapid growth in biofortification, driven by strong development and deployment of biofortified crops.

North America

North America is the third-largest region in the global market, with a projected compound annual growth rate (CAGR) of about 10.92%. This rapid growth is primarily driven by increasing consumer preference in North America for functional foods, fortified staples, and clean-label products that provide added nutritional benefits. The U.S. market notably benefits from innovation in biofortified crops such as vitamin A-enriched sweet potatoes and iron-fortified beans, which are increasingly integrated into food assistance programs, commercial food products, and institutional meal initiatives.

Europe

Europe is expected to rise at a projected CAGR of approximately 10.46%, driven by increasing demand for nutrient-rich grains and strong regulatory backing for health-enhancing foods. The demand for fortified cereals such as wheat, maize, and rice is especially significant, supported by rising consumer health consciousness about malnutrition and nutrient deficiencies. Key drivers include government and regulatory initiatives promoting biofortified crops as part of public health strategies and sustainable agriculture practices.

Middle East & Africa

The Middle East & Africa market is projected to grow at a CAGR of about 9.71%, driven by the strong adoption of vitamin A biofortified crops, particularly in Africa. Africa is recognized as a global leader in the adoption of vitamin A-rich crops, such as orange-fleshed sweet potatoes (OFSP) and provitamin A maize, which are widely cultivated to combat vitamin A deficiency and improve nutrition among vulnerable populations. Countries such as Nigeria and Kenya are key markets with active government and NGO-led initiatives promoting biofortified crops through public health programs, farmer training, and seed distribution.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Investment in R&D and Acquisitions to Support Market Growth

The biofortification market's competitive landscape includes a mix of global agricultural research institutions, seed companies, biotechnology firms, and regional crop improvement programs. Leading multinational agricultural companies, such as Bayer AG, Syngenta Group, Corteva Agriscience, DuPont, and BASF SE, dominate the sector through strong investment in R&D, strategic acquisitions, and the expansion of nutrient-focused crop portfolios. Bayer AG holds a market leadership position, focusing on regenerative agriculture and the development of nutrient-dense crops. Syngenta, through acquisitions such as Intrinsyx Bio, enhances its molecular breeding capabilities. Research institutes also play a pivotal role in driving innovation and developing new crop varieties in the global market.

Key Players in the Biofortification Market

|

Rank |

Company Name |

|

1 |

Bayer AG |

|

2 |

Syngenta Group |

|

3 |

Corteva Agriscience |

|

4 |

HarvestPlus |

|

5 |

BASF SE |

List of Key Biofortification Companies Profiled:

- Bayer CropScience (Germany)

- Corteva Agriscience (U.S.)

- Syngenta AG (Switzerland)

- BASF SE (Germany)

- KWS Saat SE & Co. KGaA (Germany)

- Rijk Zwaan (Netherlands)

- East-West Seed (Thailand)

- HarvestPlus (India)

- Seed Co Limited (Zimbabwe)

- NuTech Seed (U.S.)

- Mahyco (Maharashtra Hybrid Seeds Company Ltd.) (India)

KEY INDUSTRY DEVELOPMENTS:

- August 2025: HarvestPlus Solutions (HPS) launched a pioneering Neutral Mark, the first of its kind symbol designed to guide consumers and businesses toward the authenticity and nutritional integrity of biofortified seeds and foods. This Neutral Mark serves as a trustworthy indicator that a food product is genuinely sourced from biofortified grain or contains 100% biofortified seeds, ensuring the product meets rigorous biofortification standards.

- September 2024: HarvestPlus and Cargill launched the NutriHarvest project, a USD 3 million multi-year (36-month) initiative aimed at improving global food security and supporting farmers in India, Kenya, Tanzania, and Guatemala. The project is designed to increase access to nutritious food by delivering over 17 million nutritious meals and impacting more than 119,000 farmers.

- June 2024: Indian badminton star PV Sindhu invested an undisclosed amount in Better Nutrition, a biofortified staples brand from the agritech company Greenday. The brand focuses on biofortified food products enriched with essential micronutrients such as iron, zinc, provitamin A, calcium, and protein.

- April 2024: HarvestPlus launched a new biofortification project in Bangladesh and Uganda to combat hidden hunger, targeting rural and poverty-affected regions with high rates of micronutrient deficiencies. The initiative focuses on distributing zinc rice in Bangladesh and vitamin A maize, vitamin A sweet potato, and iron beans in Uganda, aiming to train 38,000 farmers in Bangladesh and 20,000 in Uganda over 12 months.

- October 2022: India's Arti Roller Flour Industries Pvt. Ltd. launched a branded whole-grain flour product made with zinc-enriched wheat, called City King, initially in Punjab with plans to expand nationwide. This product aims to address zinc deficiency, a major public health issue in India, by providing increased nutritional benefits through naturally biofortified zinc wheat.

REPORT COVERAGE

The global biofortification market industry report provides in-depth analysis of the market, highlighting key aspects such as global market trends, market dynamics, prominent companies, and investment in research and development. Additionally, the report offers insights into global market analysis and highlights key industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.19% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentations |

By Crop Type, Target Nutrient, Technology, and Region |

|

Segmentation |

By Crop Type

|

|

By Target Nutrient

|

|

|

By Technology

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 142.70 million in 2025 and is anticipated to reach USD 368.79 million by 2034.

At a CAGR of 11.19%, the global market will exhibit steady growth over the forecast period.

By crop type, the cereals & grains segment leads the market.

Asia Pacific held the largest market share in 2025.

The rising global burden of micronutrient deficiencies drives the market growth.

Bayer AG, Syngenta Group, Corteva Agriscience, DuPont, and BASF SE are the leading companies in the market.

Expansion of high-zinc and high-iron food staples is shaping the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us