Biological Buffers Market Size, Share & Industry Analysis, By Type (Phosphate, TRIS, Acetate, and Others), By Formulation (Solid and Liquid), By Grade (Research Grade and GMP Grade), By Application (Molecular Biology, Clinical Diagnostics, Drug Manufacturing, and Others), By End User (Pharmaceutical and Biotechnology Companies, Research & Academic Institutes, and Others), and Regional Forecasts, 2026-2034

Biological Buffers Market Size and Future Outlook

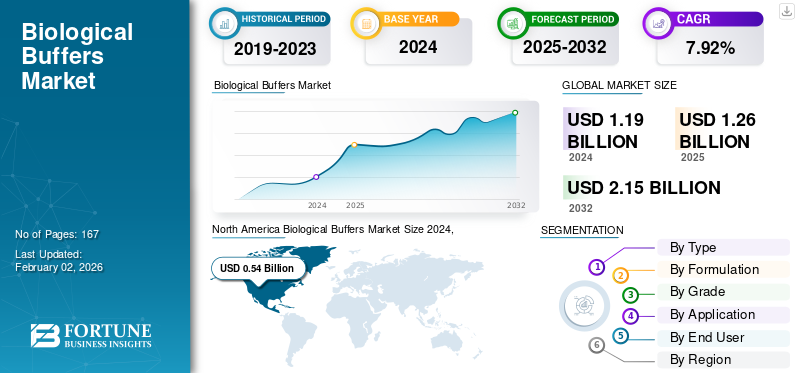

The global biological buffers market size was valued at USD 1.26 billion in 2025. The market is projected to grow from USD 1.35 billion in 2026 to USD 2.60 billion by 2034, exhibiting a CAGR of 8.55% during the forecast period. North America dominated the global biological buffers market with a market share of 45.56% in 2025.

Biological buffers play a vital role in various biopharmaceutical processes, which are integral to drug development and diagnostic assays. These high quality buffers are primarily used to control pH and maintain stability in drugs and various upstream processes. In addition, various key players are capitalizing by focusing on optimizing buffer manufacturing.

- For instance, in September 2023, Advancion Corporation launched a commercial HEPES sodium salt buffer produced at its Sterlington, Louisiana, facility. HEPES sodium salt is a zwitterionic biological buffer, often combined with HEPES free acid, and is widely used in bioprocessing, diagnostics, and molecular biology applications.

Key industry players, such as Merck KGaA, Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., Boston BioProducts, and Avantor, Inc., are investing profoundly in expanding their manufacturing capacity.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rise in Drug Discovery Consuming Standardized Buffers Drive Market Growth

With the increasing burden of various chronic as well as acute diseases across the world, the demand for precise diagnostics and innovative treatments is growing. The market’s growth is driven by rapid advancements in drug development workflows and the use of various key buffers for maintaining pH levels. Furthermore, to capture the growing market demands, various key players are directing their resources toward strategic collaborations.

- In October 2025, Merck KGaA partnered with Promega Corporation to co-develop novel technologies that advance drug screening and discovery.

MARKET RESTRAINTS

Temperature Sensitivity of Certain Buffers to Restrict Market Growth

The major factor restraining the biological buffers market growth is the risk associated with the temperature sensitivity of certain buffers. They are used in various applications that require higher sensitivity, such as drug development or diagnostic assays. Degradation due to temperature sensitivity can result in incorrect readings, hampering product adoption to certain extent.

- For instance, in March 2024, Wuhan Desheng Biochemical Technology Co., Ltd published an article titled ‘Deep analysis of temperature sensitivity and its impact on biological buffer HEPES’, reporting the influence of temperature on the buffering capacity of HEPES, a biological buffer.

MARKET OPPORTUNITIES

Shift toward an Inline Buffer Dilution Offer Significant Growth Opportunities

A shift toward inline buffer dilution, reducing the need for human interventions, offers growth opportunities. Automated, on-demand dilution reduces inaccuracies caused by manual errors, ensuring precise buffer concentrations essential for downstream processes. This shift also addresses the challenges of overcoming bottlenecks associated with large buffer volume storage and preparation time. Additionally, due to such advantages, various contract manufacturers, among other key operational entities, are focused on advancing their in-line buffer dilution.

- In April 2023, Asahi Kasei Bioprocess America partnered with GeminiBio to advance the application of inline buffer formulation and streamline biopharmaceutical manufacturing processes.

MARKET CHALLENGES

Stringent Regulatory Standards and Validation Requirements for Buffers Used in Clinical and GMP Settings

Stringent regulatory standards for buffers used in clinical and GMP settings pose a significant market challenge due to the high levels of quality, safety, and consistency regulations. Diverse regulations across different regions pose challenges for global manufacturers to adhere to multiple requirements, thereby complicating supply chains and standardizing processes. These stringent standards can limit agility and increase barriers to market entry, affecting overall market growth.

BIOLOGICAL BUFFERS MARKET TRENDS

Increasing Focus on Development of Manufacturing Capabilities is a Prominent Market Trend

One of the significant global trends in the biological buffers market is the increasing focus of key companies on developing their buffer manufacturing capabilities. To meet the growing demand for biological buffers, many key players are expanding their manufacturing capacities.

- For instance, in March 2025, Avantor, Inc. expanded its European manufacturing site. The new production facility's advanced technologies expand the site's capacity for manufacturing, formulating, and filling United States Pharmacopoeia (USP) purified water and Water for Injection (WFI)-based hydration solutions, which are essential for buffer preparation.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Phosphate’s Multiple Benefits Over its Counterparts Leads its Dominance

Based on type, the market is divided into phosphate, TRIS, acetate, and others.

Global Biological Buffers Market Share, By Type, 2024 Phosphate’s Multiple Benefits Over its Counterparts Leads its Dominance

Based on type, the market is divided into phosphate, TRIS, acetate, and others.

To know how our report can help streamline your business, Speak to Analyst

The phosphate segment is projecteed to dominate the market with a share of 40.54% in 2026 as phosphate buffers offer longer stability, non-toxicity, and higher buffer capacity. These benefits enable key companies to launch new products under this segment.

- In April 2025, Biologix Group Limited launched a series of reagents and consumables, including PBS buffer and DPBS buffer, for cell culture.

The acetate segment is anticipated to grow at a CAGR of 9.82% in the forecast period.

By Formulation

Convenience of Liquid Formulations in Various Applications Assists its Dominance

Based on formulation, the market is segmented into solid and liquid.

liquid-based segment is projecteed to dominate the market with a share of 51.99% in 2026. These buffers are easier to use and sterile, reducing the time required for weighing, dissolving, pH tuning, filtration, and extra quality control. The segment is expected to grow with a dominant share as key players are directing their resources towards the production of liquid buffers.

- In October 2025, Advancion Corporation expanded its U.S.-based manufacturing capabilities with the commercial launch of the MOPS buffer produced at its Sterlington, Louisiana, facility.

Solid buffers are projected to grow at a CAGR of 6.61% during the study period.

By Grade

Wide Application of Research Grade Buffer in Downstream and Upstream Bioprocesses to Lead the Segmental Growth

Based on grade, the market is segmented into research grade and GMP grade.

In 2024, the global market was dominated by research grade biological buffers owing to its wide applications in drug discovery, cellular biology, and synthetic biology. Research grade buffers are used for various upstream and downstream processes, driving demand for high quality buffers. The segment is anticipated to hold a 54.01% biological buffers market share in 2026.

- In January 2025, Bio-Rad Laboratories, Inc. launched Nuvia wPrime 2A Media, a chromatography resin for biomolecule purification. The charge state of the resin’s functional ligand can be modulated by the pH of the buffer, enabling the purification of otherwise difficult-to-separate biomolecules from other impurities. The wide range of applications for research-grade buffers in downstream bioprocesses is expected to drive segment growth.

The GMP-grade buffers are projected to grow at a CAGR of 9.67% during the study period.

By Application

Wide Applications in Molecular Biology to Drive Growth of the Segment

Based on application, the market is segmented into molecular biology, clinical diagnostics, drug manufacturing, and others.

The molecular biology segment is projecteed to dominate the market with a share of 34.03% in 2026 as biological buffers are extensively used in molecular biology, particularly for clinical applications such as cell and gene therapies, vaccines, and other biologics. Additionally, compliance with regulations and investments in managing the quality of these buffers supports its growth.

- In May 2023, Alpha Teknova, Inc. launched the company's proprietary product line, AAV-Tek Solutions, to address critical pain points in the AAV gene therapy development workflow. The first product released in this line, the AAV-Tek AEX Buffer Screening Kit, can save gene therapy developers months of process development time.

In addition, drug manufacturing is projected to grow at a CAGR of 11.01% during the study period.

By End User

High Usage by Pharmaceutical and Biotechnology Companies to Lead the Segmental Growth

Based on end user, the market is segmented into pharmaceutical and biotechnology companies, research & academic institutes, and others.

In 2024, the global market was driven by pharmaceutical and biotechnology companies, serving as primary end-users. Pharmaceutical and biotechnology companies utilize buffers in bulk for every step, ranging from early research to large-scale production of biologics and vaccines. Due to widespread adoption, they are investing heavily in establishing new standards of safety and compliance. The segment is estimated to hold a 51.2% market share in 2025.

- In October 2024, Nirrin Technologies partnered with Boston BioProducts to establish a new standard of QC excellence in buffer manufacturing, utilizing Nirrin’s Atlas system as a central analytical testing tool.

The research & academic institutes segment is projected to grow at a CAGR of 6.32% during the study period.

Biological Buffers Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

The North America market was valued at USD 0.57 Billion in 2025, capturing 45.56% of global revenue, and is estimated to reach USD 0.61 Billion in 2026. The regional market is poised for robust growth due to the rising prevalence of key diseases, resulting in increasing research and diagnostic activities and new product launches. In 2025, the U.S. market is valued at USD 0.55 billion by 2026.

North America Biological Buffers Market Size 2025,(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

- In July 2024, Bio-Rad Laboratories, Inc. launched four new Droplet Digital PCR (ddPCR) platforms.

Europe

In 2025, Europe held 26.08% of the global market, reaching a valuation of USD 0.33 Billion, and is projected to grow to USD 0.35 Billion in 2026. Market growth is supported by ongoing capacity expansions undertaken by leading manufacturers to address rising demand across pharmaceutical, biotechnology, and life sciences applications. The region benefits from a well-established regulatory framework that emphasizes product quality, safety, and compliance, encouraging the adoption of high-performance biological buffers. Strong research infrastructure and continuous investments in bioprocessing activities further support market development. The U.K., Germany, and France are expected to remain major contributors, reaching USD 0.07 billion, USD 0.08 billion by 2026 and USD 0.06 billion, respectively, in 2025.

Asia Pacific

The market in Asia Pacific reached USD 0.25 Billion in 2025, representing 20.19% of total market revenue, and is projected to reach USD 0.28 Billion in 2026, positioning the region as the third-largest market globally. Growth is driven by increasing healthcare expenditure, expanding pharmaceutical manufacturing capabilities, and rising investments in biotechnology research across emerging economies. Favorable government initiatives supporting healthcare modernization and domestic biopharmaceutical production are creating a conducive market environment. The growing focus on clinical research, biologics development, and laboratory infrastructure expansion continues to strengthen demand for biological buffers. The Japan market is valued at USD 0.08 billion by 2026, the China market is valued at USD 0.10 billion by 2026, and the India market is valued at USD 0.03 billion by 2026.

Latin America and the Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 0.05 Billion, representing 3.86% of global demand, and is projected to grow to USD 0.06 Billion in 2026, Latin America maintained a strong presence in the global market, reaching USD 0.05 Billion in 2025, accounting for 3.86% share, and is expected to reach USD 0.05 Billion in 2026 as there is increasing collaboration among academics and key operational entities for diagnostic assays. In the Middle East & Africa, the GCC’s market size is expected to capture USD 0.02 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players:

Market Participants Focus on Strategic Acquisitions to Capitalize Market Share

The global biological buffers market has a semi-consolidated structure, comprising prominent players such as Merck KGaA, Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., and Avantor, Inc., among others. The significant market share of these companies is due to numerous strategic activities, including new product launches, collaborations, and strategic acquisitions, as well as a focus on capacity expansion by key countries.

- In July 2024, Amano Enzyme USA Co., Ltd. inaugurated its manufacturing facility in Illinois, U.S. to enhance the company's production capacity.

Other notable players in the global market include Corning Incorporated, Arlington Scientific, Inc., and Biologix Group Limited. They are expected to prioritize capacity expansion, new product launches, and collaborations to increase their market share in biological buffers.

LIST OF KEY BIOLOGICAL BUFFERS COMPANIES PROFILED:

- Merck KGaA (Germany)

- Thermo Fisher Scientific Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Boston BioProducts (U.S.)

- HOPAX (Taiwan)

- Avantor, Inc. (U.S.)

- Corning Incorporated (U.S.)

- Arlington Scientific, Inc. (U.S.)

- Biologix Group Limited (China)

- Advancion Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Merck KGaA acquired the chromatography business of JSR Life Sciences, a leader in contract development and manufacturing bioprocessing solutions. The acquisition expanded the company’s downstream processing portfolio with advanced Protein A chromatography capabilities.

- September 2024: Bioz, Inc., partnered with Boston BioProducts, a leading provider of high-quality biological buffers and reagent solutions. This partnership aims to redefine how researchers engage with and discover Boston BioProducts' extensive product range through Bioz's advanced technology.

- August 2024: Merck KGaA acquired Mirus Bio for approximately USD 600.0 million to offer solutions in viral vector manufacturing. It also reinforces the company’s commitment to supporting customers in advancing cell and gene therapies from preclinical through commercial production.

- November 2023: Boston BioProducts expanded its leadership team with the addition of Kammie McHugh as Director of Quality & Regulatory and Matt Smart as Director of Process Excellence.

- October 2021: Aceto acquired A&C Bio Buffer, a Good Manufacturing Practices (GMP) manufacturer of custom buffer and chemical blend products.

REPORT COVERAGE

The global biological buffers market analysis provides a detailed study of the market size & forecast by all the market segments included in the report. The report also provides insights into market dynamics and trends expected to drive the market during the forecast period. The report also comprises key aspects, such as an overview of technological advancements, product launches, insights on strategic partnerships, mergers & acquisitions, and key industry developments by key regions. The market forecast also provides a detailed competitive landscape, including market share and profiles of major industry players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attribute | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.55% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Formulation, Grade, Application, End User, and Region |

| By Type |

|

| By Formulation |

|

| By Grade |

|

| By Application |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights states that the global market value stood at USD 1.26 billion in 2025 and is projected to reach USD 2.60 billion by 2034.

In 2025, the market value stood at USD 0.57 billion.

The market is expected to exhibit a CAGR of 8.55% during the forecast period.

The phosphate segment led the market in terms of type.

The increasing prevalence of diseases and rising drug development efforts are driving market growth.

Thermo Fisher Scientific Inc., Merck KGaA, Bio-Rad Laboratories, Inc., and Boston BioProducts are among the major players in the global market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us