Biomass Fuel (Wood Pellets and Palm Kernel Shell (PKS)) Market Size, Share & Industry Analysis by Feedstock (Wood Pellets, Palm Kernel Shell (PKS), and Others), By Combustion Method (Direct Combustion, Gasification, Pyrolysis, and Others), By Application (Industrial, Transportation, Commercial, Residential, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

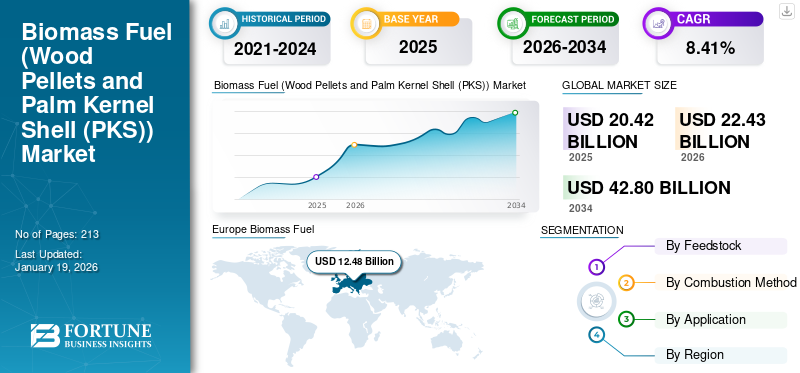

The global biomass fuel (wood pellets and palm kernel shell (PKS)) market size was valued at USD 20.42 billion in 2025. The market is projected to grow from USD 22.43 billion in 2026 to reach USD 42.80 billion by 2034, exhibiting a CAGR of 8.41% during the forecast period.

Over decades, discoveries in biomass fuel (wood pellets and palm kernel shell (PKS)) and technological innovations for harnessing energy have witnessed the evolution of bioenergy through three generations, from non-food biomass to algal biomass, known as third-generation biomass, and edible crops to feedstock. The International Energy Agency records the conventional use of biogas, which requires mainly cooking and heating in households and within small industries, prominently in developing countries, to be replaced by solid biomass, bioethanol, and biogas digesters. Biomass fuel with carbon capture and storage (BECCS) is increasing as it offers renewable energy and also permits negative emissions by capturing and keeping the CO₂ released during biomass combustion. The demand for biomass feedstocks to produce biomass fuel with carbon capture and storage (BECCS) has been increasing since these materials are plentiful and include residues from agriculture, byproducts from forestry, and organic waste.

While bioenergy can make remarkable contributions to lowering carbon emissions, most biomass energy is derived from purpose-grown trees and plants, needing land, which is a scarce commodity. With low energy yields for every unit of land and competition from other land usage and residues, some scientists see land-intensive biomass increasing in the next decade and the possibility of scaling down to a legacy fuel by 2050. The biomass fuel cell market is growing due to the rising demand for clean and decentralized energy solutions. Iwatani Corporation and Enviva Inc. lead the market through large-scale manufacturing, strategic partnerships, and a commitment to renewable energy goals.

Download Free sample to learn more about this report.

Biomass Fuel Market Key Takeaways

- 2025 Market Size: USD 20.42 billion

- 2026 Market Size: USD 22.43 billion

- 2034 Forecast Market Size: USD 42.80 billion

- CAGR: 8.41% from 2026–2034

- Europe dominated the biomass fuel (wood pellets and palm kernel shell (PKS)) market with a 60.41% share.

- The wood pellets segment is projected to account for 86.37% of the market share in 2026.

- The direct combustion segment is expected to hold 56.29% of the global market share in 2026.

Asia Pacific

Asia Pacific accounted for 19.95% of the global market in 2025 and is expected to reach USD 4.39 billion in 2026.

North America

North America captured 14.10% of global revenue in 2025 and is projected to reach USD 3.13 billion in 2026.

Europe

Europe generated USD 12.48 billion in revenue in 2025 and is projected to reach USD 13.87 billion in 2026.

U.S.

The U.S. biomass fuel (wood pellets and palm kernel shell (PKS)) market was valued at approximately USD 2.78 billion in 2025.

Japan

Japan’s biomass fuel market is projected to reach USD 0.65 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Renewable Energy and Increasing Focus on Utilizing Waste Energy to Drive the Market Growth

While there is a rising focus on decarbonization and reducing reliance on fossil fuels, there is a growing global shift toward renewable energy sources. Governments, industries, and energy providers increasingly adopt clean energy solutions to meet net-zero targets and carbon reduction goals. Biomass fuel (wood pellets and palm kernel shell (PKS)) plays a crucial role in this transition as it is considered a carbon-neutral energy source when sustainably produced.

By 2030, renewable fuels are anticipated to represent 5.5% of the energy consumption across the industry, building, and transportation sectors. The demand is expected to grow in all regions, particularly in China, Brazil, Europe, India, and the U.S., which account for more than two-thirds of the projected increase. All five regions and nations have established supportive policies for various renewable fuels, and in some instances, for all types. These policies differ by fuel type, sector, and country. Still, they generally consist of a mix of mandates, greenhouse gas performance standards, and incentives for investment in direct production and related infrastructure.

Emerging Demand from the Transportation and Industrial Sectors to Boost the Market Growth

There has been a growing adoption of bioethanol, biodiesel, and sustainable aviation fuel to reduce greenhouse gas emissions in the transportation sector. Many countries have blending mandates for biofuels in conventional fuels, increasing biomass fuel (wood pellets and palm kernel shell (PKS)) consumption.

Following the Green Deal, the EU is leading the way in modifying its transport sector toward climate impartiality. The current transport regulations offer a distinctive long-term horizon for sustainable carbon-based fuels in aviation and shipping through the defined quotas, specifically for biomass covered by Annex IX, and synthetic CO2-based fuels. Industries such as cement, steel, paper, and chemicals use biomass fuel to lower their carbon footprint for heat and power generation.

Thus, the emerging demand from the transportation and industrial sectors is expected to significantly boost the biomass fuel (wood pellets and palm kernel shell (PKS)) market growth, driven by increasing biofuel adoption, stricter emissions regulations, and strong government support.

MARKET RESTRAINTS

High Upfront and Operating Costs to Restrain Market Growth

Setting up biomass fuel (wood pellets and palm kernel shell (PKS)) plants, such as biogas units, biomass power plants, and biofuel production facilities, requires significant capital expenditure (CAPEX). Costs for equipment such as boilers, gasifiers, and feedstock preparation units are higher than conventional energy plants. Biomass systems often require continuous feedstock handling, processing, and specialized maintenance, increasing operating expenses (OPEX).

Feedstock costs (collection, drying, storage, transport) are also high due to low energy density and the bulky nature of biomass materials. The return on investment is often slower due to high upfront and operational costs, making investors hesitant. Biomass plants usually take several years to become profitable, especially without strong government incentives.

Other renewable sources such as solar and wind have lower operation costs and faster scalability, making biomass comparatively expensive in some regions. Due to the high upfront and operational costs, it takes longer for biomass projects to recover their investment. This makes it less attractive for investors, especially in regions without strong subsidies or incentives.

MARKET OPPORTUNITIES

Waste-to-Energy Initiatives to Offer Growth Opportunities

Municipal solid waste and agricultural residues are increasingly used for energy conversion via incineration, gasification, and anaerobic digestion, supporting waste management and renewable energy generation. These technologies are gaining traction in Asia, Europe, and North America, creating strong growth momentum.

As stated by the U.S. Energy Information Administration in October 2024, waste-to-energy plants burn MSW (municipal solid waste), which is often known as trash or garbage, for the production of steam in a boiler and the steam is utilized for powering an electric generator turbine. MSW is a mixture of energy-rich materials such as yard waste, paper, plastics, and products made from wood. For every 100 pounds of MSW in the U.S., nearly 85 pounds can be burned as fuel for the generation of electricity. Waste-to-energy plants turn garbage weighing 2,000 pounds into ash weighing between 300 pounds and 600 pounds and they reduce the waste volume by about 87%.

MARKET CHALLENGES

Limited Feedstock Availability and Inconsistent Supply Chains to Restrain the Market Growth

Biomass fuel depends on agricultural waste, wood chips, and organic residues, which are seasonal and region-specific. This leads to irregular supply and higher procurement costs in certain areas or seasons. Many developing regions have no organized system for collecting, storing, and transporting biomass. This causes delays, degradation of material quality, and high transportation costs.

Download Free sample to learn more about this report.

BIOMASS FUEL (WOOD PELLETS AND PALM KERNEL SHELL (PKS)) MARKET TRENDS

Shift toward Advanced Biomass Fuel to Lead the Market Growth

Advanced biomass fuels have higher calorific value and burn more efficiently, making them more suitable for industrial-scale power generation. Fuels such as torrefied pellets are water resistant, less bulky, and easier to handle, reducing logistical costs and improving supply chain reliability. Advanced fuels can be co-fired with coal in existing power plants without major retrofitting, easing the transition to cleaner energy.

IMPACT OF TARIFF ON THE BIOMASS FUEL (WOOD PELLETS AND PALM KERNEL SHELL (PKS)) MARKET

In 2025, biomass fuel (wood pellets and palm kernel shell (PKS)) prices show a possibility of being affected by tariffs, although specific impacts depend on the region and the type of biomass fuel. Tariffs influence fuel costs, certainly impacting the economics of biomass power generation. For example, the tariffs on wood pellets, if implemented, impact the spot market for biomass fuel (wood pellets and palm kernel shell (PKS)). Conversely, government subsidies and policies also support biomass energy projects, potentially offsetting the impact of tariffs.

Tariffs on biomass fuel, especially between major trade partners (such as the U.S. and Europe or China) can cause supply chain disruptions. Exporting nations such as Canada, the U.S., or Southeast Asian Countries may face reduced demand. Importers may seek alternative suppliers or shift to other renewable sources.

SEGMENTATION ANALYSIS

By Feedstock

Widespread Usage in Power Generation to Drive Wood Pellets Demand

Based on feedstock, the market is segmented into wood pellets, palm kernel shell (PKS), and others.

The wood pellets segment held the largest biomass fuel (wood pellets and palm kernel shell (PKS)) market share of 86.37% in 2026 and is expected to continue its dominance over the forecast period. Wood pellets are widely used for residential heating, industrial heating, and power generation. Many countries are promoting biomass-based heating systems to reduce fossil fuel usage. Supportive regulations such as subsidies, tax credits, and renewable energy targets boost wood pellet demand. Europe, Japan, and South Korea offer incentives to increase biomass use in energy production. Industries such as cement, chemicals, and food processing are adopting wood pellets for heating. They offer a cleaner and more cost-effective option than oil and gas.

The palm kernel shell (PMS) segment is projected to grow at a considerable CAGR of 8.59% over the forecast period. It is a by-product of palm oil production, widely available in Malaysia, Indonesia, Thailand, and other oil-producing nations. Low production cost makes it an attractive biomass fuel.

By Combustion Method

Benefit of High Energy Efficiency and Supportive Government Policies to Drive the Dominance of Direct Combustion Segment

The market is segmented as direct combustion, gasification, pyrolysis, and others based on the combustion method.

The direct combustion segment is expected to be the dominating segment, accounting for a market share of 56.29% in 2026. Direct combustion is the oldest and most widely used biomass conversion method. It is easy to implement with well-established technologies such as stoker boilers, fluidized bed boilers, and furnaces. Rising need for renewable energy in industrial heating, direct heating, and electricity generation drives segment growth. Direct combustion is ideal for combined heat and power systems, offering higher energy efficiency. Many governments provide subsidies, renewable energy incentives, and carbon credit programs for biomass projects. Such policies favor biomass combustion for carbon reduction and coal replacement.

The biomass pyrolysis segment is growing and is anticipated to depict a remarkable CAGR of 9.33% over the forecast period. Biomass pyrolysis produces bio-oil, biochar, and syngas. Bio-oil is gaining attention to fossil fuels for heating, power generation, and even for refining into transportation fuels. The growing need for liquid biofuels in industries and transport boosts pyrolysis adoption.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rising Clean Energy Demand to Fuel Industrial Segment Growth

Based on application, the market is segmented into industrial, transportation, commercial, residential, and others.

The industrial segment is expected to be the dominating segment, accounting for 42.87% market share in 2026. The industrial sector is under increasing pressure to reduce carbon emissions and shows a shift toward renewable energy sources. Biomass fuel (wood pellets and palm kernel shell (PKS)) offers a carbon-neutral alternative for industrial heat and power generation. Many industries are switching from coal, oil, and natural gas to biomass fuel as wood pellets, palm kernel shells, and agricultural residues. The global push to decarbonize the transport sector is driving biomass-based fuel adoption. Biofuels such as bioethanol, biodiesel, and renewable diesel from biomass replace conventional fossil fuels in vehicles.

The residential segment is the second leading segment holding 28.27% share in the market. Residential users increasingly prefer self-sufficient heating systems to reduce reliance on external energy providers and volatile fossil fuel prices. Biomass fuel (wood pellets and palm kernel shell (PKS)) offers local, reliable, and renewable energy.

BIOMASS FUEL (WOOD PELLETS AND PALM KERNEL SHELL (PKS)) MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Europe

Europe Biomass Fuel (Wood Pellets and Palm Kernel Shell (PKS)) Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Europe dominated the market with a valuation of USD 12.48 billion in 2025 and is projected to reach USD 13.87 billion in 2026. Europe dominates the market, with 60.41% share in 2024, and is also the fastest-growing region in the market. The European Union has set ambitious targets for net zero emissions by 2050 and 55% emission reduction by 2030. Biomass is classified as a renewable, low-carbon energy source, making it central to achieving these goals. Many European countries are phasing out coal in the power and heating sectors. Biomass is a direct replacement fuel in district heating and combined heat and power plants. In response to the Russia-Ukraine war, Europe is reducing its dependence on Russian oil and gas. Biomass provides a domestically sourced, renewable alternative to imported fuels. Moreover, markets in the leading countries of Europe such as U.K., Germany, and France have been valued at USD 3.46 billion, USD 1.97 billion, and USD 1.38 billion in 2026.

North America

The North America market was valued at USD 2.88 billion in 2025, capturing 14.10% of global revenue, and is estimated to reach USD 3.13 billion in 2026. The U.S. and Canada focus on reducing carbon emissions and boosting renewable energy. Biomass plays a key role in meeting renewable energy targets. The renewable fuel standard requires blending biofuels into transportation fuel. State-level renewable portfolio standards push for renewable electricity. In September 2024, the U.S. Department of Energy’s Office of Fossil Energy and Carbon Management announced up to USD 15 million in funding to support hydrogen production from biomass, municipal solid waste (MSW), and other feedstock. The funding opportunity will support R&D projects that convert feedstock such as biomass, industrial waste, petcoke, coal, household waste, and waste plastics into synthesis gas, also known as syngas, for enabling the low-cost production of clean hydrogen for use in electricity generation, industrial decarbonization, and transportation. The funding opportunity restricts the use of coal and/or petcoke feedstock to 20%. The estimated value of the U.S. market for biomass fuel in 2025 is around USD 2.78 billion.

Asia Pacific

The market in Asia Pacific reached USD 4.07 billion in 2025, representing 19.95% of total market revenue, and is projected to reach USD 4.39 billion in 2026. Countries such as India, China, Indonesia, Malaysia, Thailand, and Vietnam produce massive crop waste, wood residues, and palm oil waste. The region is home to the world’s fastest-growing economies. Rural and semi-urban industries, such as textiles, food processing, and brick kilns, are adopting biomass as a low-cost, renewable fuel. Governments are promoting biomass heating and power plants for industrial use. In August 2024, in South Korea, Hanwha Energy Corp. shared plans to switch its integrated heat and power plant in Gunsan from coal to biomass. The action aims to lower carbon emissions and satisfy the rising demand for environmentally friendly energy, as per sources in the power and energy sector, which is a subsidiary of the Hanwha Group. The proposal would see biomass powering 55% of the plant's 222-megawatt (MW) capacity, replacing the coal that now supplies the steam turbines that produce 123 MW. The markets for China, Japan, and South Korea depict an estimated valuation of USD 1.4 billion, USD 0.65 billion, and USD 1.17 billion in 2026 respectively.

Rest of the World

The market in the rest of the world has been valued at USD 0.99 billion in 2025. Latin America and African countries are looking to reduce the dependence on imported fossil fuels. Biomass, being locally available, supports energy security and self-sufficiency. Countries in the rest of the world have abundant agricultural residues, forestry byproducts, and organic waste, which are cost-effective feedstocks for biomass fuel. This supports sustainable waste management and circular economy goals. In addition, many governments are adopting renewable energy policies and offering subsidies or tax incentives for biomass projects.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Vendors are Developing Advanced Technologies to Improve Fuel Performance

The global market is mostly fragmented, with key players operating in the industry. The global biomass fuel companies are active in the market through various developments such as product launches, business expansion steps, and others. For instance, in March 2025, Active Energy Group PLC approved an innovative method to purify and enhance biomass materials. Biomass refers to plant materials that can be utilized as fuel. This novel process supports the company’s CoalSwitch technology. CoalSwitch provides a cleaner and more efficient alternative to traditional biomass fuel.

List of Key Biomass Fuel (Wood Pellets And Palm Kernel Shell (PKS)) Companies Profiled

- Iwatani Corporation (Japan)

- Enviva Inc. (U.S.)

- Drax Global (U.K.)

- CM Biomass (Denmark)

- Hanwa Co., Ltd. (Japan)

- BIO ENECO SDN. BHD. (Malaysia)

- Valfei Products Inc. (Canada)

- Mallard Creek Inc. (U.S.)

- Graanul Invest (Estonia)

- Segezha Group (Russia)

- Energex (Australia)

KEY INDUSTRY DEVELOPMENTS

- In July 2025, Danish biomass leader CM Biomass announced strong financial results for the 2024/25 financial year, continuing stable trading volumes in spite of downward pressure on biomass prices and global economic challenges.

- In April 2025, Utility Global Corporation and the Construction Division of Hanwha Corporation announced a partnership for the production of clean and economical hydrogen from biogas secured from wastewater treatment plants.

- In November 2024, JFE Shoji Group and BIO ENECO inked a Memorandum of Understanding (MoU) for an annual supply of 150,000 tonnes of Green Gold Label-certified palm kernel shells for a period of 15 years. The deal strengthens Bio Eneco’s reliability as a supplier of biomass fuel (wood pellets and palm kernel shell (PKS)) and bolsters Japan’s sustainable energy objectives.

- In August 2024, Hanwha Energy Corp. announced plans to convert its combined heat and power plant in Gunsan, South Korea, from coal to biomass. As per the power and energy industry sources, the Hanwha Group subsidiary currently secured the transition agreement from the Ministry of Trade, Industry, and Energy. Under the plan, 55% of the plant‘s 222-megawatt (MW) capacity will be powered by biomass and will replace the coal currently powering the steam turbines that generate 12.3 MW.

- In September 2022, Enviva Inc. and privately held Alder Fuels collaborated on the long-term supply of biomass byproducts from timber for making a biofuel for aviation, a major part of cutting carbon emissions from air travel. Under the arrangement, Enviva, a U.S. producer of woody biomass, will contribute to 750,000 tonnes per year.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Key market players invest in research and development to create high-performance fuels such as torrefied biomass and bio-oil.

- According to the IEA, as part of a larger expenditure increase on low-emission fuels, worldwide investment in biofuels is predicted to increase by 13% in 2025 to over USD 16 billion.

- According to the International Energy Agency’s World Energy Investment 2025 report, funding for low-emission fuels such as biofuels, biogases, and hydrogen is experiencing strong momentum. The investment is projected to climb by 30% in 2025, reaching nearly USD 25 billion, building on a 20% increase recorded in 2024. This sharp growth reflects accelerating efforts to scale up cleaner alternatives to fossil fuels, driven by policy support, decarbonization goals, and growing demand from industries seeking to cut carbon emissions. It also signals that low-emission fuels are becoming a more central part of the global energy transition strategy.

REPORT COVERAGE

The global biomass fuel market report delivers a detailed insight into the market. It focuses on key aspects such as leading companies and their operations offering biomass fuel. Besides, the report offers insights into market trends and technology and highlights key industry developments. In addition to the factors above, the report encompasses several factors and challenges that contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.41% from 2026 to 2034 |

|

Unit |

Value and Volume (USD Billion, Thousand Tons) |

|

Segmentation |

By Feedstock · Wood Pellets · Palm Kernel Shell (PKS) · Others By Combustion Method · Direct Combustion · Gasification · Pyrolysis · Others By Application · Industrial · Transportation · Commercial · Residential · Others By Region

|

Frequently Asked Questions

As per a study by Fortune Business Insights, the market size stood at USD 20.42 billion in 2025.

The market is likely grow at a CAGR of 8.41% over the forecast period (2026-2034).

By application, the industrial segment is the leading segment in the market.

The Europe market size stood at USD 12.48 billion in 2025.

Emerging demand from the transportation and industrial sector is a key factor anticipated to boost the market growth.

Avtron Power Solutions, BEEHE, Triumph Load, and others are some of the market's top players.

The global market size is expected to reach USD 42.80 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 213

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us