Bioprocess Validation Market Size, Share & Industry Analysis, By Test Type (Extractables and Leachables Testing, Microbiological Testing, Compatibility Testing, Integrity Testing, Physiochemical Testing, & Others), By Mode (In-house and Outsourced), By Validation Area (Process Validation, Cleaning Validation, Analytical Method Validation, Equipment Qualification, & Others), By Pharmaceutical (Monoclonal Antibodies, Recombinant Proteins, Vaccines, Cell & Gene Therapies, Biosimilars, & Others), By End User (Pharmaceutical & Biotechnology Companies, & Others), and Regional Forecast, 2026-2034

Bioprocess Validation Market Overview

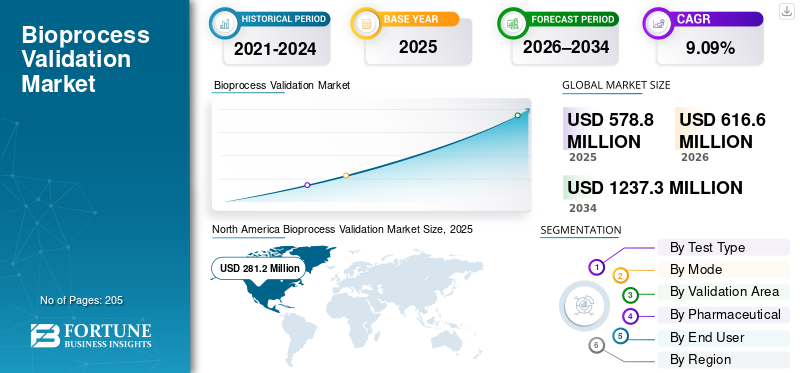

The global bioprocess validation market size was valued at USD 578.8 million in 2025. The market is projected to grow from USD 616.6 million in 2026 to USD 1,237.3 million by 2034, exhibiting a CAGR of 9.09% during the forecast period. North America dominated the bioprocess validation market with a market share of 48.58% in 2025.

Bioprocess validation ensures biopharmaceutical manufacturing processes consistently produce safe, effective biologics. It is the documented proof that a biomanufacturing process, such as the production of a monoclonal antibody, vaccine, cell/gene therapy, or recombinant protein, will consistently produce a product that meets pre-defined product quality attributes and regulatory requirements at the intended commercial scale. This market is growing significantly due to increased focus on developing innovative biologics products.

The key players in the market include Merck KGaA, Eurofins Scientific, SGS Société Générale de Surveillance SA, Sartorius AG, and others. These companies are focused on technological advancements in their service offerings.

Download Free sample to learn more about this report.

BIOPROCESS VALIDATION MARKET TRENDS

Outsourcing to CDMOs is a Prominent Market Trend

In recent years, the market is shifting from in-house validation to outsourced validation services. Bioprocess validation work is becoming more specialized, while companies seek faster timelines and variable capacity rather than permanently expanding internal QA/validation teams. As biomanufacturing footprints globalize, companies also outsource to ensure consistent GMP documentation, standardized execution, and audit-ready data across sites. The trend is especially strong during technology transfers, capacity expansions, remediation projects, and when internal teams face bandwidth constraints. Additionally, outsourcing also reduces fixed-cost burden and provides access to niche expertise and high-end instrumentation that is costly to maintain in-house. These factors are supporting the overall global bioprocess validation market growth.

- For instance, in October 2024, SGS announced an expansion of biopharmaceutical testing capabilities at its Lincolnshire, U.S. site, explicitly noting that the facility currently provides outsourcing services to developers and manufacturers in the pharmaceutical, biopharmaceutical, and medical device

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Biologics & Biosimilars Pipeline Increasing Validation Demand is Propelling Market Growth

The market is primarily being driven by the rapid expansion of the biologics and biosimilars pipeline. This is due to each new molecule moving from development to commercial scale, triggering fresh process validation (PPQ/CPV), analytical method validation/transfer, cleaning validation, and extensive documentation for GMP readiness. As sponsors add more biosimilar assets, they also increase comparability work, change controls, and tech transfers across sites/CDMOs, each step requiring validation support to prove consistency and control. Additionally, increasing collaborations between operating companies also support the market expansion.

- For instance, in July 2024, Evotec expanded its strategic partnership with Sandoz for the development and commercial manufacturing of biosimilars.

MARKET RESTRAINTS

High Analytical Complexity and Need for Specialized Technical Expertise to Hamper Market Growth

High analytical complexity is a market restraint as biologics, vaccines, and CGT products often require a wide panel of sensitive assays, and each method must be validated, transferred, and kept in a controlled state across sites. This raises the cost and time of validation projects and makes execution dependent on scarce specialists. When there is a lack of deep expertise, method robustness issues, and documentation gaps can trigger deviations, repeat studies, and delayed batch release or tech transfer timelines, directly slowing program ramp-up. The same complexity also increases dependence on high-end instrumentation and sophisticated data handling, which smaller players may struggle to maintain in-house. As a result, projects can bottleneck around specialist capacity, inflating service pricing and extending lead times. This results in limiting the market growth to a certain extent.

- For instance, in March 2025, the U.S. FDA issued a Warning Letter to Aspen Biopharma Labs Private Limited for deficiencies, including inadequate analytical method validation practices, noting that such failures increase the risk of drug quality defects.

MARKET OPPORTUNITIES

Adoption of Single-use Technologies to Offer Lucrative Opportunities for Market Expansion

Adoption of Single-Use Technologies (SUTs) is a strong market opportunity for validation service providers. Every new disposable flow path increases the need for Extractables & Leachables (E&L), integrity, and compatibility evidence to satisfy GMP expectations. As manufacturers scale SUT use from PD into commercial suites, they increasingly need repeatable, standardized validation packages rather than one-off studies. The opportunity is especially attractive in CDMO-led multiproduct facilities, where frequent changeovers and supplier changes create recurring validation workloads. Overall, the SUT wave expands the addressable base for validation-as-a-service beyond lab testing, as customers seek audit-ready documentation and interpretation. For instance, in April 2024, Cytiva unveiled the Xcellerex compact single-use magnetic mixing system for large-scale mAb, vaccine, and advanced therapy manufacturing.

MARKET CHALLENGES

Supply Chain and Capacity Constraints for Specialized Testing Labs Pose a Prominent Challenge to Market Growth

Supply chain disruptions and limited specialized testing capacity are a persistent market challenge. Validation timelines often depend on scarce lab slots, long lead times for consumables/reagents, and the availability of trained analysts. When labs face sudden demand spikes, backlogs extend turnaround times, delaying batch release, PPQ schedules, and filing packages. Moreover, supply chain volatility also forces labs to qualify alternate reagents/materials, adding rework and slowing throughput. This is especially painful for high-value biologics and short-shelf-life modalities where waiting for testing can block shipment. As a result, biomanufacturers increasingly need multi-lab contingency plans and are pushed toward premium/expedited services, raising cost and planning complexity. All the factors cumulatively affect the market growth.

Segmentation Analysis

By Test Type

Increasing Demand Due to Rising Adoption of SUTs to Propel Extractables And Leachables Testing Segment Growth

Based on test type, the market is divided into extractables and leachables testing, microbiological testing, and compatibility testing, integrity testing, physiochemical testing, and others.

The extractables and leachables testing segment captured the largest global bioprocess validation market share. Biomanufacturing has shifted heavily toward single use systems, and every polymer contact surface creates a direct patient-safety and compliance risk that must be characterized and documented. As SUS adoption scales from process development to commercial production, companies need repeatable E&L packages that are typically more specialized and higher-value than routine physchem or compatibility checks. Owing to this, operating players are also focusing on expanding their service offerings with regulatory approvals.

- For instance, in May 2025, SGS announced it received ISO 17025 accreditation for its Canadian pharmaceutical lab to offer Extractables and Leachables testing.

The integrity testing segment is anticipated to rise with a CAGR of 10.56% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Mode

High Investment in Internal Manufacturing to Boost In-House Segmental Growth

On the basis of mode, the market is divided into in-house and outsourced.

The in-house segment dominated the global market in 2025. Large biopharmaceutical manufacturers prefer to keep core validation activities embedded within their quality system. This reduces regulatory risk by ensuring consistent SOPs, faster internal approvals, and tighter control over GMP documentation and batch-impact decisions. In-house teams also protect process know-how/IP, which is especially important for biologics, where minor changes can affect CQAs. This is why companies investing in new biologics facilities often build strong internal lab/manufacturing infrastructures that inherently require sizeable in-house validation organizations. Furthermore, the segment is set to hold a 59.6% share in 2026.

- For instance, in April 2025, Merck announced launched a USD 1 billion Biologics Center of Excellence in Wilmington, Delaware, comprising laboratory and manufacturing capabilities to support launch and commercial production.

The outsourced segment is anticipated to rise with a CAGR of 10.61% over the forecast period.

By Validation Area

High Usage in Validation to Boost Equipment Qualification Segment Growth

On the basis of validation area, the market is divided into process validation, cleaning validation, analytical method validation, equipment qualification, and others.

The equipment qualification segment captured the highest share of the global market in 2025. It is a mandatory step for bringing any GMP asset into equipment, and utilities, and often whole cleanroom systems, must be proven to be installed correctly and operating consistently before process work can scale. Unlike process or cleaning validation, qualification is triggered by every new build, capacity expansion, equipment replacement, automation upgrade, and major change control, so it occurs repeatedly across a site’s lifecycle. It is also labor-intensive and touches multiple disciplines, which increases service spending. Furthermore, the segment is set to hold a 27.5% share in 2026.

- For instance, in November 2025, Exyte completed the integration of Pharmaplan to enable end-to-end delivery of GMP facilities from feasibility to qualified handover.

The analytical method validation segment is anticipated to rise with a CAGR of 10.62% over the forecast period.

By Pharmaceutical

Expanding Pipeline of Monoclonal Antibodies Supported the Segmental Dominance

Based on pharmaceutical, the market is divided into monoclonal antibodies, recombinant proteins, vaccines, cell & gene therapies, biosimilars, and others.

The monoclonal antibodies segment is anticipated to capture the largest market share in 2025. These are the largest installed base of commercial biologics manufacturing with several marketed products and a strong clinical pipeline. In addition, mAbs increasingly sit within higher-value modalities such as mAb portfolios and related platforms, driving new facilities, equipment qualification cycles, and qualification/validation packages. Furthermore, the segment is set to hold a 36.5% share in 2026.

- For instance, in September 2025, Eli Lilly announced plans to build a USD 5 billion manufacturing facility in Virginia, described as a dedicated site for Lilly’s emerging bioconjugate platform and monoclonal antibody portfolio.

The cell & gene therapies segment is anticipated to rise with a CAGR of 16.27% over the forecast period.

By End User

Strong Biologics Expansion and GMP Investments Support Pharmaceutical & Biotechnology Companies Segment Growth

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, contract development & manufacturing organizations, and others.

In 2025, the pharmaceutical & biotechnology companies segment held the leading position in the global market. These companies are actively involved in developing biologics portfolios and are the largest operators of GMP manufacturing networks. Additionally, increased investments by biopharmaceutical companies support segment growth. Furthermore, it is set to hold a 68.2% share in 2026.

- For instance, in September 2025, Gilead Sciences launched a new U.S. manufacturing hub to strengthen its biologics capacity and capabilities.

In addition, contract development & manufacturing organizations segment is projected to grow at a CAGR of 12.01% during the forecast period.

Bioprocess Validation Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Bioprocess Validation Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America market size was USD 268.8 million in 2024 and dominated the global market. The region also maintained its dominance in 2025, with USD 281.2 million. The regional dominance is driven by rapidly expanding biologics & biosimilar pipelines, strong regulatory support, and the presence of advanced CDMOs in the region.

U.S. Bioprocess Validation Market

The U.S. market accounted for the leading share of the North American market and can be analytically approximated at around USD 273.8 million in 2026, accounting for roughly 44.4% of global market.

Asia Pacific

Asia Pacific market size is projected to be valued at USD 150.1 million in 2026. The regions are projected to secure the position of the second largest region in the industry. Factors such as the rapid expansion of biologics manufacturing, especially in China, India, and the increasing CDMO investments, are responsible for regional market growth.

Japan Bioprocess Validation Market

The Japanese market in 2026 is estimated at around USD 22.1 million, accounting for roughly 3.6% of global revenues.

China Bioprocess Validation Market

China’s market is projected to reach revenues of around USD 43.0 million in 2026, representing roughly 7.0% of global sales.

India Bioprocess Validation Market

India’s market in 2026 is estimated at around USD 26.2 million, accounting for roughly 4.3% of global revenues.

Europe

Europe market is anticipated to grow at a CAGR of 7.70% during the forecast period. The region is anticipated to become the third highest among all regions. The regional market is majorly driven by the presence of strong biotech clusters, supportive EMA regulations, and expanding CDMO ecosystems across European countries.

U.K. Bioprocess Validation Market

The U.K. market in 2026 is estimated at around USD 24.8 million, representing roughly 4.0% of global revenues.

Germany Bioprocess Validation Market

Germany market size is projected to reach approximately USD 29.2 million in 2026, equivalent to around 4.7% of global sales.

Latin America and Middle East & Africa

The Latin America and the Middle East and Africa regions would grow at a relatively slower over the study period. The Latin America market size is set to reach a valuation of USD 28.4 million in 2026. These regional growth is majorly driven by emerging biomanufacturing and increasing selective outsourcing in these regions.

Among the Middle East & Africa region, the GCC market in 2026 is estimated at around USD 9.5 million, accounting for roughly 1.5% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Expansions in Specialized Testing Capacity and Digital Validation Offerings Are Reshaping Competitive Positioning

The global bioprocess validation market is moderately fragmented. Key players include Eurofins Scientific, SGS, Nelson Labs (Sotera Health), Charles River Laboratories, Thermo Fisher Scientific Inc., MerckKGaA, and Sartorius. These players are focusing on capacity expansions, capability build-outs in extractables & leachables, and sterility assurance, M&A to expand microbiology footprints, and partnerships to accelerate digital/AI-enabled validation workflows.

- For instance, in June 2025, Nelson Labs announced the expansion project to double ISO-classified cleanroom capacity at its Salt Lake City headquarters to meet growing demand for sterility assurance services and stringent EU GMP Annex 1 requirements.

Other key players in the market include Laboratory Corporation of America Holdings, DOC S.r.l., Hangzhou Cobetter Filtration Equipments Co., Ltd, Meissner Filtration Products, Inc. and others. These companies are actively offering innovative services across various applications.

LIST OF KEY BIOPROCESS VALIDATION COMPANIES PROFILED

- Merck KGaA (Germany)

- Eurofins Scientific (Luxembourg)

- SGS Société Générale de Surveillance SA (Switzerland)

- Sartorius AG (Germany)

- Cytiva (Danaher) (U.S.)

- Laboratory Corporation of America Holdings (U.S.)

- DOC S.r.l. (Italy)

- Hangzhou Cobetter Filtration Equipments Co., Ltd (China)

- Meissner Filtration Products, Inc. (U.S.)

- Charles River Laboratories. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Sikich announced a strategic partnership with ValGenesis to offer ValGenesis’ AI-powered digital validation platform to life sciences clients, modernizing validation processes.

- October 2025: Intertek Pharmaceutical Services launched Extractables & Leachables (E&L) testing services to support compliance with new Korean Pharmacopeia requirements.

- October 2025: Alcami announced a 20,000 sq ft lab services expansion in Durham, NC, to strengthen analytical capabilities for biologics/CGT (method establishment, release/stability, and characterization).

- July 2025: ValGenesis announced up to USD 16 million in strategic financing to accelerate global expansion and AI-driven innovation in validation lifecycle management (digital validation).

- September 2024: Pace Life Sciences announced the acquisition of Catalent’s analytical services lab in RTP, North Carolina, expanding capacity/capabilities in analytical services that support validation programs.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.09% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Test Type, Mode, validation Area, Pharmaceutical, End User, and Region |

| By Test Type |

|

| By Mode |

|

| By Application |

|

| By Pharmaceutical |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 578.8 million in 2025 and is projected to reach USD 1,237.3 million by 2034.

In 2025, the North American market value stood at USD 281.2 million.

The market is expected to exhibit a CAGR of 9.09% during the forecast period.

By test type, the extractables and leachables testing segment led the market.

The rising global biologics & biosimilars pipeline, in turn, increasing validation demand, are the key factors driving the market.

Merck KGaA, Eurofins Scientific, SGS Société Générale de Surveillance SA, and Sartorius AG, are some of the prominent players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us