Black Mass Recycling Market Size, Share & Industry Analysis, By Feedstock Type (Production & Process Scrap and End of Life Material), By Chemistry (Nickel-based (NMC & NCA), Lithium Iron Phosphate (LFP), and Others), By Recovered Materials (Lithium (Li), Nickel (Ni), Cobalt (Co), Copper (Cu), Manganese (Mn), Graphite, and Others) and Regional Forecast, 2026-2034

Black Mass Recycling Market Size and Future Outlook

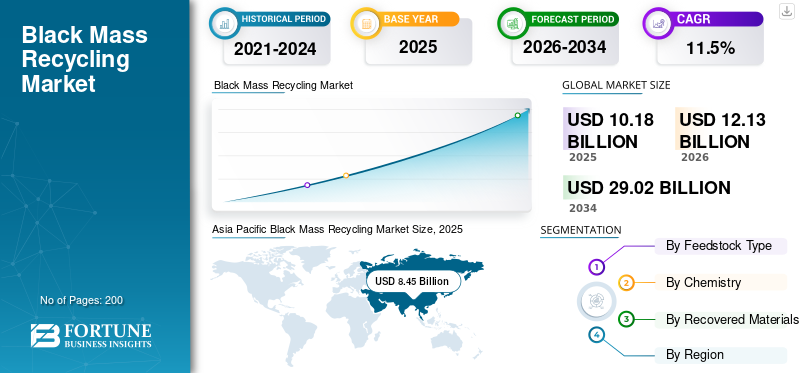

The global black mass recycling market size was valued at USD 10.18 billion in 2025. The market is projected to grow from USD 12.13 billion in 2026 to USD 29.02 billion by 2034, exhibiting a CAGR of 11.5% during the forecast period. Asia Pacific dominated the black mass recycling market with a market share of 83.01% in 2025.

Black mass recycling is the process of recovering valuable materials from end-of-life and manufacturing scrap lithium-ion batteries. Batteries are collected, safely discharged, dismantled, and processed to produce black mass, a powder containing battery materials such as lithium, nickel, cobalt, and manganese, along with minor binder and electrolyte residues. The black mass is then refined using hydrometallurgical processing to produce battery-grade products, such as lithium carbonate, lithium hydroxide, and nickel-cobalt-manganese salts, which can be supplied back into the battery materials chain. Market demand is driven by rising demand for lithium-ion batteries, increasing volumes of battery scrap from gigafactories, and a stronger focus on critical mineral security and circular supply chains. Growth is supported by long-term interest from automakers and battery manufacturers in closed-loop sourcing, as well as by recycling mandates and sustainability targets in key regions.

The market is led by specialized battery recyclers and large integrated players that can secure steady feedstock and deliver battery-grade quality at scale. Key companies such as American Battery Technology Co. (ABTC), Atom Trace, BASF SE, Cirba Solutions, and Cylib linked recycling platforms compete by leveraging strong refining capabilities, regional plants near battery manufacturing hubs, and partnerships with automakers and cell producers. Key differentiators include reliable feedstock access, high recovery rates, consistent purity, regulatory compliance, and long-term supply and offtake contracts.

Download Free sample to learn more about this report.

BLACK MASS RECYCLING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 10.18 billion

- 2026 Market Size: USD 12.13 billion

- 2034 Forecast Market Size: USD 29.02 billion

- CAGR: 11.50% from 2026–2034

- Asia Pacific dominated the market with a 83.01% share in 2025.

- The Production & Process Scrap segment is expected to dominate the market in 2026.

- The Nickel (Ni) segment is expected to dominate the market in 2026.

Asia Pacific

The market reached USD 8.45 billion in 2025 and is projected to grow to USD 10.04 billion in 2026.

Europe

The market reached USD 1.04 billion in 2025 and is projected to witness strong growth by 2026.

North America

The market reached USD 0.59 billion in 2025.

U.S.

The market is projected to reach USD 0.67 billion by 2026.

Japan

The market is projected to reach USD 0.19 billion by 2026.

Read More

BLACK MASS RECYCLING MARKET TRENDS

Rising Shift Toward Closed-Loop Battery Material Supply to Shape Market Dynamics

Automakers and battery manufacturers are increasingly prioritizing black mass recycling to secure a stable supply of critical battery materials and reduce reliance on imported minerals. The concept of the circular economy is gaining traction in regions that are pushing local battery ecosystems, where recycled, valuable metals such as lithium, nickel, cobalt, and manganese can support domestic cathode supply chains. At the same time, demand for traceable, lower-carbon raw materials are increasing, making recycled content a procurement advantage for OEMs and cell makers. As battery production expands, manufacturing scrap volumes are surging, strengthening the need for high-throughput recycling and consistent refining capability. Hence, the rising shift toward closed-loop battery material supply will favor product adoption.

- The U.S. government is heavily investing in black mass recycling to build a domestic supply chain for critical minerals such as lithium, cobalt, and nickel. Key initiatives include USD 3 billion in grants awarded by the U.S. Department of Energy (DOE) in September 2024, as well as tax credits for recycling facilities.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Volumes of End of Life Batteries and Manufacturing Scrap of Lithium-Ion Batteries to Drive Market Growth

Black mass recycling demand is directly supported by rising battery availability from two sources: end-of-life batteries and manufacturing scrap from lithium-ion battery production. Scrap generation increases as new gigafactories scale up, while end-of-life volumes rise as early electric vehicle fleets age. These feedstocks contain valuable lithium, nickel, cobalt, and manganese, providing strong economic motivation to recover and refine them into battery-grade products. Governments and OEMs also push recycling to reduce waste risks and strengthen critical mineral security. Hence, higher battery volumes throughout the battery lifecycle will create a high-value chain for manufacturers to leverage, thereby driving the global black mass recycling market growth during the forecast period.

- According to the U.S. Environmental Protection Agency (EPA), many battery recyclers also accept battery materials as manufacturing scrap for processing, creating a favorable environment for market growth.

MARKET RESTRAINTS

Feedstock Variability and High Refining Costs May Limit Market Expansion

Black mass quality varies by battery chemistry, supplier, and pre-processing method, making refining more complex and raising operating costs. Recyclers must manage impurities, including aluminum, copper, fluorine compounds, and binder residues, to meet battery-grade purity requirements. In addition, black mass logistics and handling require strict safety controls and permits, increasing compliance cost and time. Profitability also fluctuates with lithium, nickel, and cobalt prices, which directly affect recycling spreads and contract terms. Along with these factors, energy-intensive recycling technologies can slow market expansion even when demand remains structurally positive.

MARKET OPPORTUNITIES

Battery Grade Refining and Long-Term Offtake Partnerships to Create Lucrative Opportunities

A major opportunity lies in scaling battery-grade refining of lithium carbonate, lithium hydroxide, and nickel-cobalt-manganese salts, which can be directly supplied to cathode producers. Automakers and battery makers are increasingly willing to sign long-term offtake agreements to secure recycled-material supply and meet recycled-content targets. Regions building local battery supply chains also create opportunities for new recycling hubs near gigafactories to reduce logistics risk and improve access to feedstock. Players that can consistently deliver high-purity outputs, strong recovery rates, and low-carbon, traceable materials are positioned to capture higher-value growth.

Segmentation Analysis

By Feedstock Type

Production and Process Scrap Segment Dominates Due to Steady Gigafactory Output

Based on feedstock type, the market is segmented into production & process scrap and end-of-life material.

Production & process scrap segment accounted for the largest global black mass recycling market share in 2025, supported by the rapid scale-up of lithium-ion battery manufacturing and by high scrap generation during electrode coating, cell assembly, and formation stages. This feedstock is relevant as it is easier to secure, coming from organized factory channels with clearer traceability, lower safety risks than used packs, and more consistent chemistry and impurity profiles. As a result, recyclers typically achieve better processing stability and higher recovery efficiency. The segment also benefits from proximity to gigafactories, which reduces logistics costs and improves feedstock continuity for refiners.

End-of-life material is anticipated to expand rapidly, with a CAGR of 19.4% over the forecast period, driven by the aging of electric vehicle fleets and the increasing number of consumer and industrial batteries entering retirement. This feedstock is structurally large and long-term; it requires stricter handling as packs must be safely collected, transported, discharged, and dismantled before processing. Compared to manufacturing scrap, end-of-life batteries exhibit greater variability in chemistry, state of health, and contamination, which increases sorting and pretreatment requirements. Moreover, policy support and producer responsibility programs are improving collection networks and formalizing flows. Automakers also push end-of-life recycling to meet recycled-content goals and strengthen circular supply chains.

By Chemistry

Nickel-Based Segment Dominates Due to Higher Recovery Economics

Based on chemistry, the market is segmented into nickel-based (NCM & NCA), lithium iron phosphate (LFP), and others.

Nickel-based segment dominated the global market in 2025 due to high recovery rates from NMC and NCA batteries. These chemistries typically offer stronger recycling economics due to higher nickel and cobalt content, which improves the value per ton of black mass and supports stronger demand for refined nickel, cobalt, and manganese salts. Recyclers also prioritize these streams when available, as the revenue from nickel and cobalt can better cover refining costs and impurity management. Long-term supply agreements between recyclers, automakers, and cathode producers further support a stable offtake for nickel-based recovery routes.

Lithium iron phosphate is growing rapidly as LFP adoption rises across mass-market electric vehicles, two-wheelers, and stationary storage. While LFP black mass is generally lower in value than nickel- and cobalt-rich streams, it is becoming increasingly important due to the sheer volume growth and the improvement in lithium-focused recovery strategies. Recyclers are investing in better process control to manage LFP-specific impurities and improve lithium extraction yields, so that economics remain attractive. This shift is pushing the industry to develop scalable refining solutions for LFP-heavy feedstock, which will drive the segment at a 13.8% CAGR over the forecast period.

Other chemistries make up a smaller but steady share of the market, mainly from mixed feedstock streams such as LMO, blended cathodes, and unknown batches collected from consumer electronics and diversified recycling channels. These streams are more difficult to optimize as composition can vary widely, increasing the need for sorting and raising the effort required for impurity removal. Yields and product consistency can also be less predictable, affecting pricing and off-take confidence. Despite these challenges, the segment remains relevant for recyclers that operate broad collection networks and handle mixed inflows. Improving pre-processing and better classification practices will gradually support more stable recovery outcomes, helping the segment grow at a CAGR of 11.7% during the forecast period.

By Recovered Materials

Nickel (Ni) Segment Dominates the Market as It is a Core Ingredient in Batteries

Based on recovered materials, the market is segmented into Lithium (Li), Nickel (Ni), Cobalt (Co), Copper (Cu), Manganese (Mn), graphite, and others.

To know how our report can help streamline your business, Speak to Analyst

Nickel (Ni) segment remains a major value pool as nickel-rich cathodes are widely used in long-range electric vehicles and premium battery platforms. Recovered nickel is typically converted into nickel intermediates that can be supplied to precursor producers, supporting closed-loop sourcing models. This segment benefits when feedstock contains higher shares of NMC and NCA, where nickel concentration supports stronger recovery economics. Recyclers with stable feedstock access and strong refining capability are better positioned to deliver consistent nickel quality at scale, which is important for qualification and long-term offtake. Continued investment in domestic battery supply chains also supports demand for nickel recovery in key regions.

The lithium segment is the fastest-growing in recovered materials, expanding at a CAGR of around 13.8% over the forecast period. It becomes a central focus as lithium carbonate and lithium hydroxide are essential for cathode production, and many regions are trying to localize critical mineral supply. This becomes even more critical as LFP adoption increases, since LFP contains no nickel or cobalt and shifts the revenue focus toward lithium. As recycling volumes rise from manufacturing scrap and end-of-life batteries, refiners are scaling lithium extraction and purification to meet battery-grade specifications. Strong offtake interest, recycled-content targets, and low-carbon sourcing requirements further support lithium-focused capacity additions.

Cobalt recovery remains important in black mass recycling as cobalt is a critical material for stabilizing high-energy cathodes and supporting battery safety and durability, especially in nickel-based chemistries used for long-range and premium electric vehicles. Its high unit value also helps recyclers strengthen overall recovery economics when cobalt-bearing feedstock is available. Demand is supported by continued use of NMC and NCA batteries in performance applications and by battery material supply chains seeking secure and traceable sourcing. However, growth is moderated over time by lower cobalt intensity trends in some cathode formulations and the rising share of LFP batteries. The segment is estimated to grow at a CAGR of 7.9% over the forecast period.

Black Mass Recycling Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Black Mass Recycling Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 8.454 billion, and is expected to maintain its leading share in 2026, valued at USD 10.04 billion. The region’s dominance is underpinned by its large lithium-ion battery manufacturing base, high availability of production and process scrap, and strong downstream integration across cathode materials and refining. The region also benefits from established collection and processing infrastructure, which improves recovery economics and supports higher-throughput recycling. Regulatory focus on battery circularity and supply security further strengthens regional demand, while continuous capacity additions in recycling and battery materials support sustained growth.

China Black Mass Recycling Market

China is estimated to reach USD 9.09 billion in 2026, accounting for around 75% of global revenues, supported by the world’s largest battery manufacturing ecosystem, strong scrap generation from gigafactories, and highly integrated recycling and refining supply chains.

Japan Black Mass Recycling Market

Japan is set to reach USD 0.19 billion in 2026, representing around 2% of global revenues, supported by established battery supply chains, high compliance standards, and increasing focus on domestic recovery of critical battery materials.

North America

North America remains a significant regional market, valued at USD 0.59 billion in 2025. Market growth is supported by scaling battery manufacturing capacity, the growing availability of manufacturing scrap, and policy support to build localized critical mineral and battery material supply chains. The region is also strengthening recycling investments to support closed-loop sourcing and to meet sustainability and traceability requirements from automakers and battery makers.

U.S. Black Mass Recycling Market

The U.S. market is expected to reach USD 0.67 billion in 2026, accounting for around 5% of global revenues, driven by battery plant expansions, scrap availability from new capacity ramp-ups, and increasing emphasis on local refining and recycling.

Europe

Europe is projected to grow at 15.7% over the coming years. The region reached a valuation of USD 1.04 billion in 2025. Focus on domestic critical mineral recovery and sustainable battery supply chains continues to support recycling capacity additions and long-term offtake activity. Further growth is supported by rising electric vehicle production, expanding battery investments, and a strong regulatory push for recycling, traceability, and circular material sourcing.

Germany Black Mass Recycling Market

The German market is likely to reach USD 0.32 billion in 2026, equivalent to around 2% of global revenues. Growth is supported by Germany’s large and increasingly electrified vehicle production base, which structurally increases battery manufacturing activity and the availability of production scrap for recyclers. VDA data highlights record electrified-vehicle output milestones in Germany, reinforcing the scale of upstream battery and component throughput that feeds recycling volumes.

Belgium Black Mass Recycling Market

The Belgium market in 2026 is anticipated to reach USD 0.22 billion, accounting for roughly ~2% of global revenues. The country benefits from established industrial capabilities, led by Umicore’s Hoboken complex, which processes large material volumes and has dedicated lithium-ion battery and production scrap treatment capacity, strengthening Belgium’s position in the European market.

Rest of World

The rest of the world is expected to witness moderate growth during the forecast period, with the market valued at USD 0.10 billion in 2025. In Latin America, recycling activity is increasingly linked to import-heavy EV fleets and consumer electronics waste streams, where organized take-back and producer-led collection programs are improving feedstock availability over time. In the Middle East and Africa, demand is still developing. Momentum is supported by large-scale renewable and grid projects that increase stationary storage deployments, which will translate into future end-of-life battery flows. Overall, the region remains early-stage, with growth tied to regulation, expanded formal collection, and partnerships that enable stable black mass supply to global refiners.

COMPETITIVE LANDSCAPE

Key Industry Players

Feedstock Access and Battery Grade Refining Capability Define Competitive Strength

The black mass recycling market is shaped by specialized battery recyclers and battery materials companies that can secure consistent feedstock from end-of-life and manufacturing scrap lithium-ion batteries and convert black mass into battery-grade outputs. Key players include American Battery Technology Co. (ABTC), BASF SE, TENOVA, Umicore, and Wistron Corporation, which strengthen their positions through integrated processing capacity, expanding recycling networks, and long-term offtake relationships with battery supply chain partners. Furthermore, competitive positioning is primarily driven by long-term collection and supply agreements with automakers, cell manufacturers, and gigafactories. High recovery rates across lithium, nickel, cobalt, and manganese, and the ability to meet strict purity and traceability requirements for downstream cathode and precursor customers, will give competitors a competitive advantage.

LIST OF KEY BLACK MASS RECYCLING COMPANIES PROFILED

- American Battery Technology Co. (ABTC) (U.S.)

- Atom Trace (Czech Republic)

- BASF SE (Germany)

- Cirba Solutions (U.S.)

- Cylib (Germany)

- Dainen Materials (Japan)

- RecycLiCo (Canada)

- TENOVA (Italy)

- Umicore (Belgium)

- WISTRON Corporation (Taiwan)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Ascend Elements successfully produced 99% pure recycled lithium carbonate from black mass at its Covington, Georgia, site, demonstrating battery-grade lithium recovery capability and supporting localized critical mineral supply for the U.S. and Europe.

- September 2025: Blue Whale Materials commissioned its baseline black mass line in Bartlesville, Oklahoma, targeting 14 kilotons per year of black mass production and advancing expansion plans supported by over USD 55 million in U.S. Department of Energy funding to scale processing capacity.

- August 2025: Princeton NuEnergy opened a commercial-scale facility in Chester, South Carolina, to produce advanced black mass and battery-grade cathode materials, highlighting the shift toward domestic recycling infrastructure capable of handling both NCM- and LFP-linked streams.

- June 2025: BASF began commercial operations of its black mass plant in Schwarzheide, Germany, with a processing capacity of 15 kilotons per year of end-of-life lithium-ion batteries and production scrap. The start-up strengthens Europe’s black mass supply base and supports local recovery of lithium, nickel, cobalt, and manganese for battery materials.

- April 2025: American Battery Technology Co. (ABTC), a Nevada-based battery materials manufacturer and recycler, doubled its recycled material production capacity at its commercial-scale Lithium-Ion Battery (LIB) recycling facility.

- August 2024: Cirba Solutions officially expanded its black mass-producing facility in Lancaster, Ohio, with support from federal funding from the Bipartisan Infrastructure Law (BIL). Cirba Solutions added two processing lines that are capable of producing 20 kilotons of black mass annually.

REPORT COVERAGE

The global black mass recycling market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.5% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Feedstock Type, Chemistry, Recovered Materials, and Region |

| By Feedstock Type |

|

| By Chemistry |

|

| By Recovered Materials |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 10.18 billion in 2025 and is projected to reach USD 29.02 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 8.45 billion.

Recording a CAGR of 11.5%, the market is slated to exhibit steady growth during the forecast period.

By recovered materials, the Nickel (Ni) segment is leading the market.

Growing volumes of end of life batteries and manufacturing scrap of lithium-ion batteries are the key factors drive market growth.

Entegris, FUJIFILM Corporation, AGC Inc., Resonac Holdings, and 3M are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

The rising shift toward closed-loop battery material supply will favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us