Brain Computer Interface (BCI) Market Size, Share & Industry Analysis, By Product Type (Invasive BCI, Partially Invasive BCI, and Non-Invasive BCI), By Component (Hardware and Software), By Application (Assistive Technology, Disability and Rehabilitation, and Others), By End-user (Hospitals & Specialty Clinics, Rehabilitation Centers, Homecare Settings, and Others), and Regional Forecast, 2026-2034

Brain Computer Interface (BCI) Market Size and Future Outlook

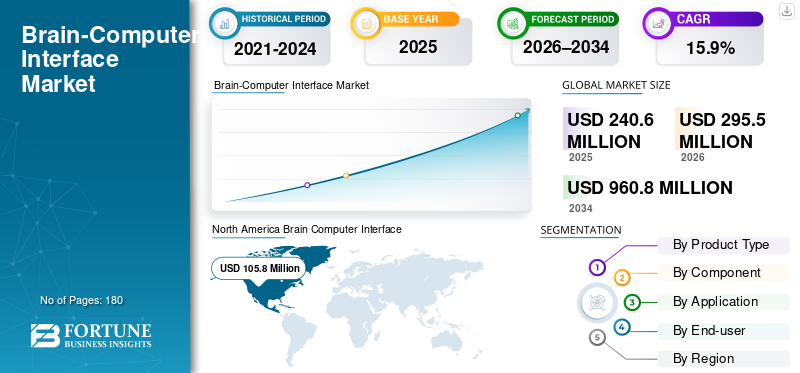

The global Brain Computer Interface (BCI) market size was valued at USD 240.6 million in 2025. The market is projected to grow from USD 295.5 million in 2026 to USD 960.8 million by 2034, exhibiting a CAGR of 15.9% during the forecast period. North America dominated the global brain computer interface (BCI) market with a market share of 43.97% in 2025.

Brain Computer Interfaces (BCIs) translate brain signals into digital commands to communicate, move a cursor, or trigger rehabilitation actions without relying on weakened muscles. In healthcare, momentum occurs via two factors: disability-focused assistive control, such as helping people with paralysis interact with devices, and neurorehabilitation, such as using brain intent to retrain movement after neurological injury. Simultaneously, technology is shifting from lab prototypes to regulated, clinically deployed systems. On the implant side, companies are steadily expanding human studies.

Blackrock Neurotech, g.tec medical engineering GmbH, Neuralink Corp., and Synchron Inc. held the largest market share, driven by increasing investments and strategic initiatives, such as new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

Brain Computer Interface Market Takeaways

- 2025 Market Size: USD 240.6 million

- 2026 Market Size: USD 295.5 million

- 2034 Forecast Market Size: USD 960.8 million

- CAGR: 15.9% from 2026–2034

- North America dominated the BCI market with a 43.97% share in 2025.

- The disability and rehabilitation segment is projected to hold 51.2% of the market share in 2026.

- Hospitals and specialty clinics are expected to account for 44.5% of the market share in 2026.

North America

North America held the leading position in the market, reaching USD 105.8 million in 2025.

Europe

Europe is expected to record robust growth, reaching USD 107.4 million by 2026.

Asia Pacific

Asia Pacific is projected to reach USD 48.9 million by 2026.

U.S.

The market is forecast to reach USD 112.3 million by 2026, accounting for 38.0% of global revenue.

Japan

The market is projected to generate USD 8.6 million by 2026

Read More

BRAIN COMPUTER INTERFACE (BCI) MARKET TRENDS

Minimally Invasive Interfaces and Faster Translation from Trials to Practice Likely to Boost Overall Market

A clear trend is the push toward interfaces that are either non-invasive (EEG-based) or less invasive than traditional open-brain approaches, as scaling in healthcare depends on safety, repeatability, and patient acceptability. Synchron’s endovascular approach exemplifies this direction: the company received FDA IDE approval in July 2021. Furthermore, it announced the first U.S. implant in July 2022, positioning blood-vessel implantation as a potentially more scalable alternative to craniotomy-dependent systems.

Another trend is the “shorter path” from research to commercialization for certain components. Even where implants remain early, the ecosystem is maturing, with more human data, clearer regulatory touchpoints, and more realistic deployment workflows.

In parallel, non-invasive BCI rehabilitation is steadily becoming more structured, which signals that regulators will evaluate BCI rehab as a product with defined indications and controls. Expected continued convergence between therapy content (rehab protocols) and decoding software (signal processing and intent classification), shifts value toward integrated platforms rather than standalone devices.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Neurological Disease Burden and Unmet Functional Needs Fuel Market Growth

A significant market driver is the rising number of people living with neurological impairment and the availability of modern age assistive and rehabilitation tools which still leave a large gap. Stroke remains a core demand pool as motor deficits can persist long after acute care, keeping rehabilitation volumes high year after year. Global stroke burden has continued to increase over time, reinforcing the need for scalable recovery solutions rather than purely therapist-intensive models. BCIs fill this gap by connecting “intent” with feedback or assisted movement, which is especially relevant during weak or inconsistent muscle activation.

Commercial and regulatory progress is also accelerating clinical confidence. In parallel, implantable BCIs are moving from feasibility toward broader clinical evidence generation. Neuralink reported its first human implant in January 2024, illustrating how quickly high-profile programs are pushing into human use. Collectively, expanding patient need and clearer clinical pathways are bringing BCIs into hospitals, specialty clinics, and research programs, thereby increasing global Brain Computer Interface (BCI) market growth.

MARKET RESTRAINTS

Clinical Proof, Reimbursement Clarity, and Lag of Workflow Fit Limit Market Growth

BCIs can be compelling in demos, however healthcare buying decisions depend on evidence, economics, and implementation friction. In neurorehabilitation, outcomes must be durable and measurable against standard therapy, which is hard to prove across varied stroke severity, comorbidities, and therapy adherence. Even when a device clears regulation, hospitals and rehab networks still need reimbursement pathways or budget justification, without exponentially increasing staff time.

On the implant side, adoption is naturally slower as implants introduce surgical considerations, long-term safety monitoring, and device management obligations. While progress is real, large-scale uptake depends on longer follow-up, consistent performance, and clearer patient selection. For newer interfaces, regulatory milestones may enable wider clinical use, however they do not automatically translate into broad procurement. However, commercialization still requires scaled training, supply, and service support. Finally, data governance and cybersecurity expectations in hospitals are tightening; BCIs generate sensitive neural data, and many health systems will move cautiously until privacy, consent, and ownership policies are operationalized.

MARKET OPPORTUNITIES

Rehab Networks, Home-Based Recovery, and Scalable Decoding to Create Significant Growth Opportunities

The strongest near-term opportunity is to turn BCIs into repeatable care pathways rather than one-off pilots. Neurorehabilitation is a prime example: once a rehab network standardizes protocols such as patient selection, session design, and outcomes tracking, utilization can scale without reinventing the program at each site. Vendors are positioning themselves to increase repeatability.

A second opportunity is homecare. Many patients plateau after discharge because the intensity drops; portable, non-invasive BCIs paired with remote monitoring can help to continue training in important matters while feeding objective progress data back to clinicians. Regulation is gradually making this attainable, which supports future reimbursement discussions and home deployment models.

Finally, healthcare research is an underappreciated growth engine. As BCI platforms become easier to deploy and analyze, more clinical studies can shift from “signal collection” to “actionable decoding,” reallocating budgets toward software, analytics, and validated models, especially as the prevalence of neurological diseases continues to rise.

MARKET CHALLENGES

Training Burden, Heterogeneous Signals, and Clinical Adoption to Challenge Market Growth

BCIs have a unique clinical challenge: people’s brain signals are variable, and the clinical environment is messy. Signal quality can change with fatigue, medication, electrode placement, and disease progression, so a strong performance in a controlled study may degrade in day-to-day use. That variability makes hospitals cautious, especially when outcomes must be consistent across diverse patient populations.

Operationally, BCIs also carry a training burden. Rehab staff need confidence in setup and troubleshooting; neurology teams need clear protocols for patient selection and follow-up; and researchers need tools that reduce time spent cleaning data. Although technology is becoming more advanced, scaling can be slow. This also highlights that early programs are still building evidence, clinician experience, and long-term safety datasets.

For non-invasive clinical rehab, BCI-driven therapy should meaningfully improve function beyond high-quality conventional therapy, while being cost-effective. For implantable BCIs, hurdles include surgical risk management, device longevity, and post-implant support models. The market’s next phase will be led by companies that showcase BCIs as standard clinical tools, which are easy to deploy, reliably reimbursable, and seamlessly integrated into hospital IT and therapy workflows.

Segmentation Analysis

By Product Type

Wide Adoption of Non-Invasive BCI in Several Healthcare Settings makes it Dominant

Based on product type, the market is segmented into invasive BCI, partially invasive BCI, and non-invasive BCI.

Non-invasive BCI leads with the largest Brain Computer Interface (BCI) market share as they align with healthcare’s risk tolerance and scaling realities. EEG-based systems can be deployed in hospitals, rehab centers, and research programs without surgery, making them easier to approve internally, train staff on, and expand across sites. The regulatory pathway is also clearer for certain use cases, signaling that BCI-guided rehabilitation can be evaluated and commercialized as a device-based intervention. As clinics seek scalable neurorehab solutions, non-invasive BCIs remain the practical starting point.

The invasive BCI segment is projected to grow at a CAGR of 22.8% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Hardware Leads as Early-Stage Clinical BCIs are Still Equipment-Led

By component, the market is classified into hardware and software.

Hardware holds the larger share as early-stage clinical BCIs are still equipment-led: headsets/caps, amplifiers, electrodes, and (for invasive approaches) implantable interfaces and supporting surgical systems. Even in rehab, the purchase decision often begins with physical system deployment in a clinic before software expansion becomes meaningful at scale.

The software segment is estimated to grow at a CAGR of 21.1% during the forecast period.

By Application

Growing Neurological Conditions Propel Disability and Rehabilitation Application

By application, the market is classified into assistive technology, disability and rehabilitation, and others.

Disability and rehabilitation segment leads as clinical need is large and measurable: regaining hand and arm function after stroke, improving independence after spinal cord injury, and restoring control pathways for severe motor impairment. Importantly, rehab BCIs can be integrated into structured therapy, producing repeatable sessions and standardized outcomes. Moreover, the segment is projected to hold a 51.2% share in 2026.

The assistive technology segment is estimated to grow at a CAGR of 21.4% during the forecast period.

By End-user

Hospitals & Specialty Clinics is the Leading End-user Due to its Advanced Healthcare Infrastructure

On the basis of end-user, the market is classified into hospitals & specialty clinics, rehabilitation centers, homecare settings, and others.

Hospitals and specialty clinics lead adoption as they sit at the intersection of diagnosis, surgery, and supervised rehabilitation planning. They also host clinical research that advances BCIs, especially implantable systems that require specialist teams and controlled protocols. Similarly, regulated rehab BCIs such as IpsiHand fit naturally into hospital-led neurorehabilitation pathways before wider diffusion into homecare settings. Furthermore, the segment is set to hold 44.5% market share in 2026.

The homecare settings segment is projected to grow at a CAGR of 23.6% during the forecast period.

Brain Computer Interface (BCI) Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Brain Computer Interface (BCI) Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 85.7 million, and also reached USD 105.8 million in 2025. North America continues to lead the global BCI market due to its strong concentration of advanced healthcare infrastructure, neuroscience research funding, and early adoption of novel neurotechnologies. The U.S. plays a pivotal role, supported by a large base of specialty hospitals, academic medical centers, and rehabilitation institutes actively involved in clinical trials and translational research. The region benefits from a favorable regulatory environment that has enabled multiple BCI systems to progress through clinical evaluation, encouraging hospital-led adoption. In addition, the high prevalence of neurological disorders such as stroke, spinal cord injury, and neurodegenerative diseases sustains demand for assistive and rehabilitation-focused BCIs. Strong collaboration among technology developers, universities, and healthcare providers further accelerates innovation, while greater healthcare spending capacity supports the procurement of advanced BCI hardware and software platforms.

U.S Brain Computer Interface (BCI) Market

In 2026, the U.S. market is forecast to represent USD 112.3 million, capturing 38.0% of total global revenue.

Europe

Europe is expected to achieve a 16.4% growth rate in the coming years, the second-highest globally, and reach USD 107.4 million by 2026. Europe represents a fast-growing market driven by structured neurorehabilitation programs and a strong emphasis on clinical research collaboration. Several European countries have well-established rehabilitation networks and publicly funded healthcare systems that encourage the integration of innovative therapies into standard care pathways. The presence of specialized BCI developers and neuroscience research institutes across Western and Northern Europe further supports growth. Cross-border research initiatives and EU-backed funding programs have played an important role in expanding clinical evidence for BCI-based rehabilitation and assistive technologies. Additionally, Europe has observed increasing adoption of non-invasive BCIs in rehabilitation centers, particularly for post-stroke motor recovery, as these solutions align well with patient safety expectations and cost-containment priorities within public healthcare systems.

U.K Brain Computer Interface (BCI) Market

The U.K. market is projected to reach USD 17.1 million by 2026, accounting for 5.8% of the global revenue.

Germany Brain Computer Interface (BCI) Market

Germany's market is forecast to reach about USD 19.2 million by 2026, representing roughly 6.5% of global revenue.

Asia Pacific

In 2026, Asia Pacific is predicted to be valued at USD 48.9 million, ranking as the third-largest region globally. Asia Pacific is expected to witness the fastest growth over the forecast period, supported by a rapidly expanding patient base and improving access to advanced neurological care. The rising incidence of stroke and traumatic brain injuries, particularly in aging populations across Japan and China, is driving demand for scalable rehabilitation solutions. Governments in the region are investing heavily in neuroscience research, digital health, and hospital infrastructure, which is creating new opportunities for BCI deployment in both clinical and research settings. In addition, the growing number of tertiary care hospitals and academic institutions is increasing participation in clinical studies involving BCIs. While adoption began from a smaller base than in North America and Europe, improvements in affordability, local manufacturing, and greater awareness among clinicians are accelerating market penetration.

Japan Brain Computer Interface (BCI) Market

Japan is projected to generate approximately USD 8.6 million in revenue by 2026, contributing nearly 2.9% to the global market.

China Brain Computer Interface (BCI) Market

China is forecast to reach approximately USD 12.9 million by 2026, contributing about 4.4% to global revenues.

India Brain Computer Interface (BCI) Market

India is forecast to contribute approximately USD 5.1 million to the market by 2026, corresponding to about 1.7% of global revenues.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa are anticipated to witness moderate Brain Computer Interface (BCI) market growth, with Latin America expected to reach around USD 7.3 million by 2026. Growth in Latin America is supported by gradual improvements in healthcare infrastructure and increasing adoption of advanced medical technologies in urban and private healthcare settings. Brazil and Mexico are witnessing rising demand for rehabilitation services due to higher survival rates from stroke and neurological trauma. The Middle East & Africa is developing steadily, driven mainly by investments in advanced healthcare facilities and centers of excellence, particularly in Gulf countries. Governments in the Middle East are prioritizing the development of specialized hospitals and rehabilitation services as part of broader healthcare modernization initiatives. This has created opportunities for the introduction of BCIs in tertiary care hospitals and academic research settings.

GCC Brain Computer Interface (BCI) Market

By 2026, the GCC is expected to generate approximately USD 1.1 million in the market, accounting for nearly 0.4% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The global market remains moderately fragmented, with a mix of established neurotechnology suppliers and emerging clinical-stage innovators. Competition is shaped less by price and more by clinical validation, regulatory progress, and depth of research deployment. Key players such as Blackrock Neurotech, g.tec medical engineering GmbH, Neuralink Corp., and Synchron Inc. held the largest market share. Non-invasive BCI providers currently hold a stronger commercial footing due to easier integration into hospitals and rehabilitation centers, while invasive and partially invasive players are advancing through clinical trials and early human use.

Large portions of market activity are concentrated around healthcare research platforms and neurorehabilitation systems, where recurring collaborations with academic hospitals and research institutes provide stable revenue streams. Strategic differentiation is increasingly based on signal quality, decoding software, clinical workflow integration, and scalability across care settings, rather than hardware alone. As clinical evidence matures, competition is expected to intensify around regulated rehabilitation use cases and minimally invasive implantable BCIs.

Moreover, other key players, such as Emotiv Inc., BrainGate, Precision Neuroscience, and Neuroelectrics, compete through ongoing technological developments, the growing demand for improved healthcare infrastructure, and efforts to improve procedural outcomes.

LIST OF KEY BRAIN COMPUTER INTERFACE (BCI) COMPANIES PROFILED

- Blackrock Neurotech (U.S.)

- tec medical engineering GmbH (Austria)

- Neuralink Corp. (S.)

- Synchron Inc. (U.S.)

- Emotiv Inc. (U.S.)

- BrainGate (U.S.)

- Precision Neuroscience (U.S.)

- Neuroelectrics (Spain)

- Ripple Neuro (U.S.)

- Compumedics Limited (Australia)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Precision Neuroscience received FDA clearance for its Layer 7 Cortical Interface, an electrode array that can be implanted for up to 30 days to map brain activity.

- November 2024: tec medical engineering’s innovative recoveriX BCI treatment is now available in hospitals and neurorehabilitation centers.

- October 2024: INBRAIN Neuroelectronics, a brain-computer interface therapeutics (BCI-Tx) company developing graphene-based neural technologies, announced the close of a USD 50 million Series B financing round.

- September 2024: The University of San Francisco (USF) Data Institute has announced a pioneering collaboration with EMOTIV, a leading EEG and bioinformatics company, and Quantum Computing Inc. (QCi), an innovative, integrated photonics and quantum optics technology company, to drive groundbreaking innovations in brain health monitoring and analysis.

- September 2024: INBRAIN Neuroelectronics, a brain-computer interface therapeutics (BCI-Tx) company pioneering graphene-based neural technologies, announced the world’s first human procedure of its corticaI interface in a patient undergoing brain tumor resection. INBRAIN’s BCI technology was able to differentiate between healthy and cancerous brain tissue with micrometer-scale precision.

- September 2023: INBRAIN Neuroelectronics S.L., a health-tech company dedicated to developing the world’s first intelligent graphene-neural platform, announced that its Intelligent Network Modulation System has been granted Breakthrough Device Designation (BDD) from the U.S. Food & Drug Administration (FDA) as an adjunctive therapy for treating Parkinson’s disease.

- July 2023: INBRAIN Neuroelectronics S.L. announced a collaboration with Merck KGaA to develop next-generation bioelectronic/neural interface technology.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 15.9% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Product Type, Component, Application, End-user, and Region |

|

By Product Type |

· Invasive BCI · Partially Invasive BCI · Non-Invasive BCI |

|

By Component |

· Hardware · Software |

|

By Application |

· Assistive Technology · Disability and Rehabilitation · Others |

|

By End-user |

· Hospitals & Specialty Clinics · Rehabilitation Centers · Homecare Settings · Others |

|

By Geography |

· North America (By Product Type, Component, Application, End-user, and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Product Type, Component, Application, End-user, and Country/Sub-region) o Germany (By Application) o U.K. (By Application) o France (By Application) o Spain (By Application) o Italy (By Application) o Scandinavia (By Application) o Rest of Europe (By Application) · Asia Pacific (By Product Type, Component, Application, End-user, and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o Australia (By Application) o Southeast Asia (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Product Type, Component, Application, End-user, and Country/Sub-region) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Product Type, Component, Application, End-user, and Country/Sub-region) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 240.6 million in 2025 and is projected to reach USD 960.8 million by 2034.

In 2025, North Americas market value stood at USD 105.8 million.

The market is expected to exhibit a CAGR of 15.9% during the forecast period of 2026-2034.

The non-invasive BCI segment led the market by product type.

The key factors driving the market are rising neurological disease burden and unmet functional needs.

Blackrock Neurotech, g.tec medical engineering GmbH, Neuralink Corp., and Synchron Inc. are some of the major players in the market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us