Bus Axle Market Size, Share & Industry Analysis, By Axle Position (Front Axle and Rear Axle), By Axle Configuration (2-Axle Buses, 3-Axle Buses, and Articulated/Multi-axle Buses), By Bus Type (City/Transit Buses, Intercity Buses, School Buses, and Others), By Technology (Conventional Axles and Electric Drive Axles (E-Axles)), and Regional Forecast, 2026-2034

Bus Axle Market Size and Future Outlook

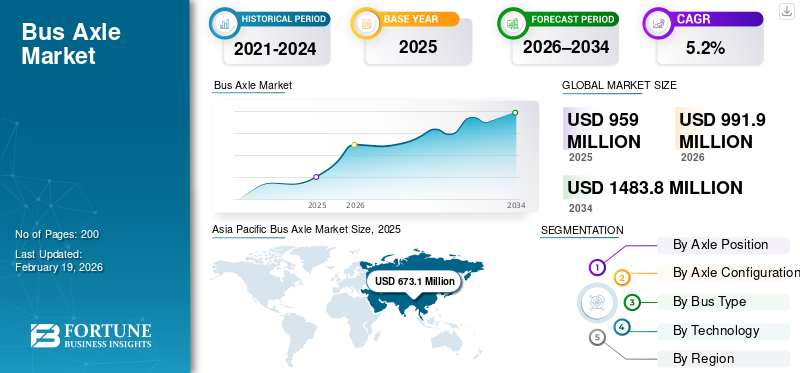

The global bus axle market size was valued at USD 959.0 million in 2025. The market is projected to grow from USD 991.9 million in 2026 to USD 1,483.8 million by 2034, exhibiting a CAGR of 5.2% during the forecast period. Asia Pacific dominated the bus axle market with a market share of 70.19% in 2025.

The market refers to the global industry involved in the design, manufacturing, and sale of axle systems used in buses. It includes the front and rear axles for city, intercity, and electric buses, supporting load-bearing, stability, power transmission, and overall vehicle performance.

Key drivers of the bus axle market include rising public transportation demand, urbanization, and government investment in mass transit. Growth in electric and low-emission buses, stricter safety and load regulations, fleet modernization, and increasing bus production in emerging economies, further boosting the demand for advanced, durable axle systems.

The market analysis highlights moderate consolidation, strong OEM partnerships, and focus on lightweight and electric-compatible axles. Key players include ZF Friedrichshafen, Dana Incorporated, Meritor, AAM, SAF-HOLLAND, and Hyundai Transys, competing on technology, durability, and global presence.

Download Free sample to learn more about this report.

Bus Axle Market Key Takeaways

- 2025 Market Size: USD 959.0 million

- 2026 Market Size: USD 991.9 million

- 2034 Forecast Market Size: USD 1,483.8 million

- CAGR: 5.2% from 2026–2034

- Asia Pacific dominated the bus axle market with a 70.19% share in 2025.

- Electric drive axle (e-axle) segment is projected to grow at the fastest CAGR of 6.9% during the forecast period.

- 2-axle buses segment accounted for the largest market share in 2025.

North America

North America represented the third-largest market in 2025.

Asia Pacific

Asia Pacific dominated the market in 2025, valued at USD 673.1 million.

Europe

Europe held the second-largest market share and is projected to grow at a CAGR of 5.0% during the forecast period.

U.S.

U.S. market projected to reach USD 15.8 million by 2026.

Japan

Japan market projected to reach USD 65.02 million by 2026.

Read More

BUS AXLE MARKET TRENDS

Lightweight and Integrated Axle Designs to Propel the Market Growth

A key trend in the market is the growing focus on lightweight and integrated axle designs. OEMs are increasingly adopting advanced materials and optimized structures to reduce vehicle weight without compromising load capacity or durability. Integrated axles that combine braking, suspension, and drive components are gaining traction as they improved energy efficiency, reduce assembly complexity, and lower maintenance requirements. This trend aligns with the broader industry focus on improving fuel efficiency and extending vehicle range, particularly for electric buses. As bus manufacturers seek compact and efficient vehicle architectures, axle suppliers are prioritizing modular and multifunctional axle solutions.

- In October 2025, ZF presented a new generation of bus/coach axle systems emphasizing light weighting and efficiency, including designs aimed at reducing energy consumption and improving recuperation clear momentum toward integrated, efficiency-led axle architectures.

MARKET DYNAMICS

MARKET DRIVERS

Rising Public Transport Investments to Drive the Market Growth

Increasing government investment in public transportation infrastructure is a key driver of the bus axle market growth. Urban congestion, pollution concerns, and the need for affordable mobility are encouraging cities to expand and modernize bus fleets. The large-scale procurement of city, intercity, and electric buses directly increases the demand for reliable front and rear axles. Additionally, public transport projects often prioritize long vehicle life and high load-bearing capacity, pushing OEMs to adopt advanced axle systems. The replacement demand from expanding fleets further supports aftermarket sales. Emerging economies in Asia, Latin America, and the Middle East are particularly active, where bus rapid transit systems and intercity connectivity projects are driving sustained axle demand.

MARKET RESTRAINTS

Limited Standardization across Bus Platforms to Restrain Market Expansion

The lack of standardization in bus designs across regions and applications acts as a key restraint for the bus axle market. Axle requirements vary significantly based on bus type, load capacity, road conditions, and regulatory norms, forcing manufacturers to develop multiple customized solutions. This increases engineering complexity, extends development timelines, and limits economies of scale. OEMs often demand application-specific axles, reducing interchangeability and slowing faster market penetration of new designs. For axle suppliers, managing diverse product portfolios raises production costs and inventory challenges, ultimately restraining margin expansion and limiting rapid scalability across global bus platforms.

MARKET OPPORTUNITIES

Electrification of Bus Fleets to Create Growth Opportunities

The rapid adoption of electric buses presents a significant opportunity for the bus axle market. Electric buses require specially designed axles that can accommodate higher vehicle weights due to batteries while supporting electric drive components and regenerative braking systems. This shift is driving the demand for lightweight yet high-strength axles and integrated e-axle solutions. Manufacturers that invest in electrification-ready designs can secure long-term OEM contracts and differentiate themselves technologically. Additionally, government incentives for zero-emission buses are accelerating fleet electrification across Europe, China, and North America, expanding the addressable market for innovative axle solutions tailored to battery electric vehicle electric and plug in hybrid electric vehicle (PHEV) buses.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Dependence to Create Challenges for Market Growth

Supply chain disruptions and fluctuating raw material prices represent a major challenge for the bus axle market. Axle manufacturing relies heavily on steel and alloy components, making costs sensitive to commodity price volatility. Global supply chain issues, including logistics delays and geopolitical uncertainties, can impact production schedules and delivery timelines. These challenges strain relationships with OEMs that operate on tight production plans and long-term contracts. Smaller manufacturers are particularly vulnerable due to limited sourcing flexibility. Managing supply risks while maintaining consistent quality and cost competitiveness remains a critical challenge for axle suppliers operating in the global market.

Segmentation Analysis

By Axle Position

High Load-Bearing Role and Power Transmission Requirements to Drive Rear Axle Dominance

Based on segmentation by axle position, the market is classified into front axle and rear axle.

The rear axle segment dominates the bus axle market due to its critical role in load bearing, power transmission, and vehicle stability. Most buses, including city, intercity, and electric models, rely on robust rear axles to support high passenger loads and drivetrain integration. Increasing adoption of heavy-duty and electric buses further strengthens rear axle demand as these vehicles require reinforced designs to handle higher weights, torque, and regenerative braking stresses, sustaining OEM and replacement demand.

The front axle segment, the second-largest, is projected to grow at a CAGR of 4.7% over the forecast period. The segment growth is supported by rising safety regulations, steering performance requirements, and fleet modernization, driving the demand for advanced front axles with improved durability, suspension integration, and load-handling capabilities.

By Axle Configuration

Operational Simplicity and High Deployment in Urban Transit to Support 2-Axle Buses Segmental Dominance

In terms of axle configuration, the market is categorized into 2-axle buses, 3-axle buses, and articulated / multi-axle buses.

The 2-axle bus segment dominates the bus axle market due to its widespread use in city and intercity public transport systems. These buses offer optimal balance between passenger capacity, maneuverability, and operating cost, making them the preferred choice for urban transit authorities and private operators. High production volumes, standardized designs, and frequent deployment in dense routes drive consistent OEM and aftermarket axle demand. Their suitability for diesel, CNG, and electric configurations further reinforces sustained adoption across developed and emerging markets.

The articulated and multi-axle buses segment is the fastest growing, registering a CAGR of 6.5% over the forecast period. The segment growth is driven by the rising demand for high-capacity buses in megacities, bus rapid transit corridors, and airport shuttle services, increasing the need for multi-axle load distribution and advanced axle systems.

To know how our report can help streamline your business, Speak to Analyst

By Bus Type

Dense Urban Deployment and High Fleet Turnover to Sustain City/Transit Bus Segment Dominance

Based on bus type, the market is segmented into city/transit buses, intercity buses, school buses, and others.

The city/transit buses segment dominates the bus axle market due to their extensive deployment in urban public transportation networks and high daily utilization rates. These buses operate on fixed routes with frequent stop-and-go cycles, increasing wear on axles and driving consistent replacement demand. Ongoing investments in urban mobility, bus rapid transit systems, and electric city buses further strengthen axle demand. Large fleet sizes and regular maintenance schedules across municipal operators ensure steady OEM and aftermarket consumption of front and rear axles.

The intercity bus segment, which holds the second-largest bus axle market share, is expected to grow at a CAGR of 4.5% over the forecast period. The segment growth is supported by the rising intercity connectivity, tourism, and long-distance travel demand, driving the need for durable, high-load axles optimized for highway performance and passenger comfort.

By Technology

Proven Reliability and Broad Vehicle Compatibility to Reinforce Conventional Axles Segment’s Dominance

Based on technology, the market is segmented into conventional axles and electric drive axles (e-axles).

The conventional axles segment dominates the bus axle market due to their proven reliability, cost-effectiveness, and compatibility across diesel, CNG, and hybrid bus platforms. Fleet operators and transit authorities continue to prefer conventional axles due to their established performance, ease of maintenance, and wide service network availability. High penetration across existing bus fleets and ongoing replacement demand further support dominance, as operators prioritize durability and lifecycle cost efficiency over rapid technology shifts.

The electric drive axle (e-axle) segment is the fastest growing segment and is projected to expand at a CAGR of 6.9% over the forecast period. The segmental expansion is driven by accelerating electric bus adoption, government emission mandates, and demand for integrated, energy-efficient drivetrain solutions that enhance vehicle range and reduce maintenance complexity.

Bus Axle Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Bus Axle Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the bus axle market and is also the fastest-growing region, driven by massive public transportation expansion, rapid urbanization, and strong domestic bus manufacturing. Countries such as China and India continue to invest heavily in city buses, electric mobility, and intercity connectivity, sustaining high axle demand. Large vehicle production volumes, cost-efficient manufacturing, and government-backed fleet electrification programs further accelerate growth. The region is projected to register the highest CAGR over the forecast period, supported by the rising replacement demand from large, aging bus fleets.

China Bus Axle Market

In 2026, the China market is estimated to expand at a value of around USD 379.61 million, accounting for the largest share of global market revenues. Growth is driven by massive EV parc expansion, dense public fast-charging deployment, strong government mandates, utility-backed smart grid integration, and rapid adoption of AI-enabled, ultra-fast charging infrastructure nationwide.

Japan Bus Axle Market

The Japan market is estimated to grow at a value of around USD 65.02 million in 2026, accounting for a notable share of the global market revenues. The regional growth is supported by urban charging upgrades, OEM-led smart charging platforms, grid optimization initiatives, and the increasing adoption of vehicle-to-grid and energy management systems.

Europe

Europe holds the second-largest share of the bus axle market, supported by stringent emission regulations and rapid adoption of electric and low-emission buses. Transit authorities across Western and Northern Europe are actively modernizing fleets, increasing the demand for advanced axles compatible with electric drivetrains. Strong presence of leading axle manufacturers and technology innovation further supports market stability. The Europe market is expected to grow at a CAGR of 5.0% over the forecast period, driven by replacement demand, electrification incentives, and investments in sustainable urban mobility infrastructure.

Germany Bus Axle Market

In 2026, the Germany market is estimated to expand at a value of around USD 37.20 million, accounting for a significant share of the global market revenues. The market expansion is fueled by stringent emission norms, high EV penetration, extensive public charging rollout, renewable energy integration, and strong investments by utilities and automotive OEMs.

North America

North America represents the third-largest market for bus axles, supported by steady investments in public transportation and school bus fleets. The region benefits from structured maintenance cycles and high replacement demand from aging buses. The gradual adoption of electric buses, supported by federal and state funding programs, is creating incremental opportunities for advanced axle solutions. While growth is moderate compared to Asia Pacific, demand remains stable due to long vehicle lifecycles, regulatory safety requirements, and ongoing upgrades to urban and regional transit systems.

U.S. Bus Axle Market

The U.S. market is estimated at a valuation of around USD 15.8 million in 2026, accounting for a notable share of the global market revenues. The regional market growth is driven by federal incentives, rapid DC fast-charger installations, fleet electrification, smart home charging adoption, and expanding interoperability across charging networks.

Rest of the World

The rest of the world region, including Latin America, the Middle East, and Africa, is witnessing gradual growth in the bus axle market. Rising urbanization, government-backed public transport initiatives, and increasing intercity connectivity are driving new bus procurement. Countries investing in bus rapid transit systems and airport shuttle services are creating the demand for durable axle systems. Although market size remains smaller, improving infrastructure, expanding city fleets, and increasing focus on mass transit are expected to support steady long-term growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies to Leverage Enhanced Engineering Capabilities to Roll out Advanced Products

The bus axle market is dominated by established Tier-1 axle manufacturers and global drivetrain leaders such as ZF Friedrichshafen, Dana Incorporated, Meritor, American Axle & Manufacturing (AAM), SAF-HOLLAND, Hyundai Transys, and Carraro. These players leverage deep OEM relationships, advanced engineering capabilities, and global manufacturing networks to supply front, rear, and drive axles for city, intercity, and electric buses. Their portfolios span conventional heavy-duty axles, lightweight solutions, and integrated electric drive axles, enabling broad application coverage across diesel, CNG, hybrid, and electric bus platforms.

Key market participants are increasingly focusing on technology differentiation through lightweight materials, modular axle architectures, and electrification-ready designs that support higher loads, regenerative braking, and improved efficiency. Strategic collaborations with bus OEMs, electric drivetrain developers, and component suppliers enable integrated solutions and faster time-to-market. Additionally, companies are pursuing capacity expansions, regional localization, aftermarket service strengthening, and targeted acquisitions to enhance competitiveness amid rising global investments in public transportation and bus electrification.

LIST OF KEY BUS AXLE COMPANIES PROFILED

- ZF Friedrichshafen AG (Germany)

- Dana Incorporated (U.S.)

- Meritor, Inc. (U.S.)

- American Axle & Manufacturing (AAM) (U.S.)

- Hyundai Transys (South Korea)

- PRESS KOGYO Co., Ltd. (Japan)

- HANDE Axle (Shaanxi Hande) (China)

- Benteler International AG (Germany)

- KOFCO (Korea Forging Co.) (South Korea)

- GKN Automotive (U.K.)

- JTEKT Corporation (Japan)

- Schaeffler Group (Germany)

- Eaton Corporation (U.S.)

- Scania AB (Sweden)

- Volvo Group (Sweden)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: ZF premiered its next-generation bus and coach axle systems including the A134 and AV134 at Busworld Europe 2025, improving torque and energy efficiency for future platforms.

- October 2025: TECO Electric & Machinery partnered with Italy’s BRIST to debut integrated e-axle solutions for electric buses at Busworld Brussels, unveiling parallel-shaft and wheel-side e-axle modules for diverse bus chassis configuration.

- September 2025: Schaeffler showcased its EMR4 electric axle drive at IAA MOBILITY 2025 in Munich, highlighting its electrified powertrain portfolio including modular e-axle systems for commercial vehicles.

- September 2025: ZF showcased integrated driveline and axle technologies at Busworld Europe 2025 to improve efficiency, safety, and digital intelligence for buses and coaches

- March 2025: Cummins announced that Meritor’s new independent front suspension and advanced eULFA axle technologies will debut at Busworld 2025 to support global bus and coach powertrain solutions

- October 2024: Bharat Forge announced that the company agreed to acquire AAM’s commercial vehicle axle business in India, including facilities in Pune and Chennai, aiming to expand its axle production footprint.

- May 2024: ZF premiered its electric AxTrax 2 LF portal axle at Busworld Türkiye as part of its e-mobility push for low-floor city buses and advanced ADAS solutions for decarbonized bus transport.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.2% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Axle Position, By Axle Configuration, By Bus Type, By Technology, and By Region |

|

By Axle Position |

· Front Axle · Rear Axle |

|

By Axle Configuration |

· 2-Axle buses · 3-Axle buses · Articulated / Multi-axle buses |

|

By Bus Type |

· City / Transit buses · Intercity buses · School buses · Others |

|

By Technology |

· Conventional Axles · Electric Drive Axles (E-Axles) |

|

By Geography |

· North America (By Axle Position, By Axle Configuration, By Bus Type, By Technology, and by Country) o U.S. (By Technology) o Canada (By Technology) o Mexico (By Technology) · Europe (By Axle Position, By Axle Configuration, By Bus Type, By Technology, and by Country) o Germany (By Technology) o U.K. (By Technology) o France (By Technology) o Rest of Europe (By Technology) · Asia Pacific (By Axle Position, By Axle Configuration, By Bus Type, By Technology, and by Country) o China (By Technology) o Japan (By Technology) o India (By Technology) o Rest of Asia Pacific (By Technology) · Rest of the World ( By Axle Position, By Axle Configuration, By Bus Type, By Technology, and by Country ) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 959.0 million in 2025 and is projected to reach USD 1,483.8 million by 2034.

In 2025, the market value stood at USD 673.1 million.

The market is expected to exhibit a CAGR of 5.2% during the forecast period of 2026-2034.

The city/transit buses segment leads the market by bus type.

The rising public transport investments are key factors anticipated to drive the market growth.

Asia Pacific dominates the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us