Bus Dispatch Management System Market Size, Share & Industry Analysis, By Deployment Model (Cloud and On-Premises), By Component (Software and Hardware), By Application (Fleet Management, Route Optimization, Passenger Information Systems, and Others), By Propulsion Type (ICE and Electric), and Regional Forecast, 2026–2034

Bus Dispatch Management System Market Size and Future Outlook

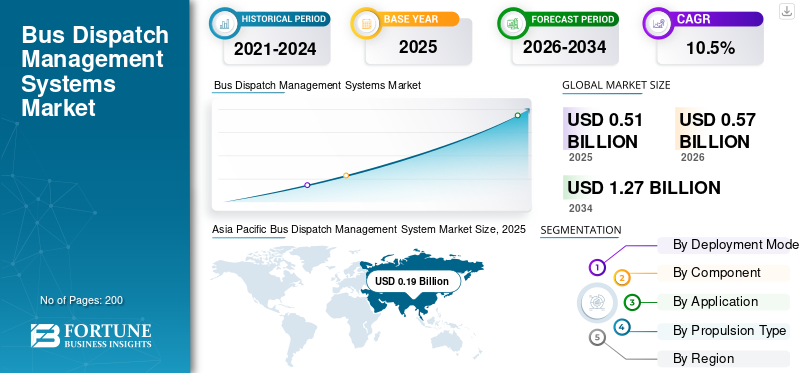

The global bus dispatch management system market size was valued at USD 0.51 billion in 2025. The market is projected to grow from USD 0.57 billion in 2026 to USD 1.27 billion by 2034, exhibiting a CAGR of 10.5% during the forecast period. Asia Pacific dominated the bus dispatch management system market with a market share of 37.25% in 2025.

A global bus dispatch management system is a centralized digital platform that enables real-time planning, scheduling, tracking, and coordination of bus fleets across multiple regions or countries. It integrates GPS, communication tools, and data analytics to optimize routes, improve operations efficiency, ensure timely dispatch, and enhance passenger service. The system supports fleet monitoring, driver management, and incident response while enabling seamless coordination between depots, control centers, and transit authorities globally.

Key factors that stimulate growth and demand within a market include technological advancements, rising consumer demand, government regulations, urbanization, and increased investment. They influence adoption rates, innovation, and expansion by creating favorable conditions for businesses to develop solutions and meet evolving customer and management systems software industry needs.

Major players in the market include Trapeze Group, GIRO Inc., Clever Devices, INIT GmbH, Optibus, and IVU Traffic Technologies, competing through advanced scheduling algorithms, real time tracking, AI driven optimization, cloud based platforms, and integrated communication systems to enhance operational efficiency, passenger experience, and data-driven decision-making.

Download Free sample to learn more about this report.

BUS DISPATCH MANAGEMENT SYSTEM MARKET TRENDS

Shift Toward Cloud-Based and Mobility-as-a-Service (MaaS) Platforms as a Key Trend

A key trend shaping the market is the increasing integration of digital technologies and smart systems. Advanced fleet management software, IoT-enabled monitoring systems, and predictive maintenance tools are transforming how yachts are managed. These technologies enable real time fleet tracking of vessel performance, fuel consumption, maintenance schedules, and compliance requirements, enhancing operational efficiency and reducing downtime. Additionally, digital platforms improve transparency for yacht owners by providing remote access to operational data and financial management reports. Automation in administrative tasks, such as crew payroll and regulatory documentation, further streamlines management processes. As yacht owners demand greater control and visibility, service providers are investing in digital capabilities to differentiate their offerings and deliver more efficient and data-driven services.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Urban Transit Demand and Smart City Initiatives to Drive System Adoption

Increasing urbanization and the expansion of public transportation networks are major drivers for the global bus dispatch management system market growth. Governments globally are investing in smart city initiatives that emphasize efficient, technology-enabled mobility solutions. As bus fleets grow in size and complexity, there is a rising need for centralized systems that can manage scheduling, routing, and real-time tracking. These platforms help reduce operational inefficiencies, minimize delays, and improve passenger satisfaction. Additionally, integration with Intelligent Transportation Systems (ITS) allows transit authorities to enhance service reliability and optimize resource allocation. The push for sustainable mobility and reduced traffic congestion further accelerates the adoption of advanced dispatch management solutions across urban and intercity transit systems.

MARKET RESTRAINTS

High Initial Investment and Integration Complexity to Restrain Market Growth

Despite the clear benefits, the adoption of bus dispatch management systems is often limited by high initial implementation costs and integration challenges. Deploying such systems requires significant investment in hardware, software, and supporting infrastructure, including GPS devices, communication networks, and cloud platforms. Additionally, integrating new dispatch systems with legacy transit management systems can be technically complex and time-consuming. Many transit agencies, especially in developing regions, face budget constraints that hinder large-scale digital transformation. The need for skilled personnel to operate and maintain these systems further adds to operational costs. These financial and technical barriers can slow down adoption rates, particularly among smaller fleet operators and public transport agencies with limited funding.

MARKET OPPORTUNITIES

Integration of AI and Predictive Analytics to Unlock Growth Opportunities

The incorporation of Artificial Intelligence (AI) and predictive analytics presents significant growth opportunities in the market. Advanced analytics can enable demand forecasting, dynamic route optimization, and predictive maintenance of fleet vehicles. By analyzing historical and real-time data, operators can make proactive decisions to improve service efficiency and reduce downtime. AI-powered systems can also enhance passenger experience through accurate arrival predictions and personalized travel information. Furthermore, the integration of these technologies with cloud-based platforms allows scalability and remote access, making them attractive for both large and mid-sized transit agencies. As digital transformation accelerates, vendors offering intelligent, data-driven dispatch solutions are well-positioned to capitalize on emerging market demand.

MARKET CHALLENGES

Data Security and Privacy Concerns as a Key Market Challenge

As bus dispatch management systems rely heavily on real-time data collection and communication, ensuring data security and privacy remains a significant challenge. These systems handle sensitive information, including vehicle locations, passenger data, and operational details, making them potential targets for cyberattacks. Any breach or system failure can disrupt transit operations and compromise passenger safety. Additionally, varying data protection regulations across regions create complexities for global deployments. Transit agencies must invest in robust cybersecurity measures, including encryption, secure communication protocols, and regular system audits. However, maintaining high levels of security while ensuring system performance and accessibility can be challenging. Addressing these concerns is essential to build trust and ensure long-term adoption of digital dispatch solutions.

Segmentation Analysis

By Deployment Model

Scalability, Real-Time Accessibility, and Lower Upfront Costs to Drive Cloud Segment Dominance

Based on deployment model, the market is categorized into cloud and on-premises.

The cloud segment dominates the market due to its scalability, cost efficiency, and ability to provide real-time data access across geographically dispersed transit networks. Cloud-based systems enable seamless updates, remote monitoring, and integration with advanced analytics and AI tools, enhancing operational agility. Transit agencies increasingly prefer cloud deployment to reduce infrastructure costs and improve system flexibility. The growing need for centralized control, multi-location coordination, and data-driven decision-making further strengthens cloud adoption, especially among large urban transit authorities and smart city projects.

The on-premises segment is projected to grow at a CAGR of 9.7% over the forecast period. Demand is driven by agencies prioritizing data security, regulatory compliance, and full system control. Legacy infrastructure compatibility and limited cloud readiness in certain regions also support continued adoption.

By Component

High Ownership Volume and Versatile Usage to Propel Motor Yachts Segment Dominance

Based on component, the market is categorized into hardware and software.

The software segment dominates the market due to its critical role in enabling real-time fleet management, route optimization, and data-driven decision-making. Advanced software platforms integrate AI, analytics, and communication tools to improve operational efficiency and service reliability. Transit agencies increasingly invest in scalable, upgradeable software solutions that support automation and seamless integration with existing systems. The shift toward digital transformation and smart mobility further strengthens demand for intelligent dispatch software across global transit networks.

The hardware segment is projected to grow at a CAGR of 8.1% over the forecast period. Growth is supported by increasing deployment of GPS devices, onboard units, and communication infrastructure required to support real-time tracking and system connectivity across expanding bus fleets.

To know how our report can help streamline your business, Speak to Analyst

By Application

Centralized Control and Real-Time Fleet Visibility to Drive Fleet Management Segment Dominance

Based on application, the market is categorized into fleet management, route optimization, passenger information systems, and others.

The fleet management segment dominates the market as it forms the core function of bus dispatch management systems, enabling real-time tracking, scheduling, and coordination of vehicles. Transit agencies rely on fleet management solutions to enhance operational efficiency, reduce delays, and ensure optimal resource utilization. These systems support driver monitoring, maintenance scheduling, and incident management, making them essential for daily operations. Increasing fleet sizes and the need for centralized command centers further reinforce demand for advanced fleet management capabilities across public and private transit operators.

The route optimization segment is projected to grow at a CAGR of 8.7% over the forecast period. Growth is driven by rising demand for fuel efficiency, reduced travel time, and dynamic routing using AI and real-time traffic data, particularly in congested urban environments.

By Propulsion Type

Widespread Fleet Base and Established Infrastructure to Drive ICE Segment Dominance

Based on propulsion type, the market is categorized into ICE and Electric.

The ICE segment dominates the market due to the extensive global presence of conventional diesel and gasoline-powered bus fleets. Most transit agencies continue to rely on ICE buses owing to established fueling infrastructure, lower upfront costs, and operational familiarity. Dispatch management systems are widely integrated with these fleets to enhance scheduling, tracking, and efficiency. Additionally, slower fleet electrification in several regions ensures continued reliance on ICE-based systems, sustaining demand for compatible dispatch solutions across both public and private transportation networks.

The electric segment is projected to grow at a CAGR of 11% over the forecast period. Growth is driven by increasing electrification of bus fleets, government incentives, and the need for advanced dispatch systems to manage charging schedules, range optimization, and energy-efficient operations.

Bus Dispatch Management System Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Bus Dispatch Management System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the bus dispatch management system market due to rapid urbanization, expanding public transportation networks, and strong government investments in smart city initiatives. China, India, and Japan are increasingly deploying digital transit solutions to manage large and complex bus fleets efficiently. The growing need for real-time tracking, route optimization, and improved passenger services further drives adoption. Additionally, rising fleet electrification and infrastructure modernization accelerate demand for advanced dispatch systems across metropolitan and intercity transport networks.

China Bus Dispatch Management System Market

The Chinese market is estimated at around USD 0.12 billion in 2026, supported by rapid urbanization, expansion of public transit fleets, and government initiatives promoting smart mobility and digital infrastructure development.

Japan Bus Dispatch Management System Market

The Japanese market is estimated at around USD 0.01 billion in 2026, driven by smart city initiatives, advanced public transit digitization, and increasing adoption of AI-based scheduling and real-time fleet monitoring solutions.

North America

North America holds the second-largest market share, supported by advanced transportation infrastructure and early adoption of intelligent transit systems. The region is projected to grow at a CAGR of 10.2% over the forecast period, driven by increasing investments in smart mobility and digital fleet management solutions. Transit agencies in the U.S. and Canada are focusing on improving operational efficiency, reducing costs, and enhancing passenger experience through AI-driven dispatch systems. Strong presence of key market players and continuous technological innovation further contribute to regional market growth.

U.S. Bus Dispatch Management System Market

The U.S. market is estimated at around USD 0.14 billion in 2026, driven by large transit networks, high investment in smart transportation, and rapid adoption of AI-powered dispatch and analytics platforms.

Europe

Europe represents the third-largest market, driven by stringent regulations promoting sustainable mobility and efficient public transportation systems. Germany, the U.K., and France are adopting advanced dispatch solutions to optimize transit operations and reduce emissions. Integration of Mobility-as-a-Service (MaaS) platforms and increasing investments in digital infrastructure further support market growth. Additionally, the region’s focus on electrification of bus fleets is creating demand for dispatch systems capable of managing energy-efficient routing and charging schedules.

U.K. Bus Dispatch Management System Market

The U.K. market is estimated at around USD 0.02 billion in 2026, supported by strong public transportation infrastructure, government-backed digital mobility programs, and growing demand for cloud-based fleet management systems.

Germany Bus Dispatch Management System Market

The German market is estimated at around USD 0.03 billion in 2026, fueled by technological advancements, integration of intelligent transport systems, and increasing focus on operational efficiency and sustainable urban mobility solutions.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth due to increasing investments in urban infrastructure and smart transportation projects. Governments in the UAE and Saudi Arabia are focusing on modernizing public transit systems, creating demand for advanced dispatch management solutions. Growing urban populations and the need for efficient mobility solutions are driving adoption. However, budget constraints and limited digital infrastructure in some areas may moderate growth, although ongoing development initiatives are expected to create new opportunities.

UAE Bus Dispatch Management System Market

The UAE market in 2026 is estimated at around USD 0.02 billion, driven by smart city developments, modernization of urban transportation infrastructure, and increasing investments in intelligent mobility and connected transit systems.

Latin America

Latin America is emerging as a developing market, supported by gradual improvements in public transportation infrastructure and increasing urbanization. Brazil and Mexico are adopting digital dispatch systems to enhance fleet efficiency and reduce operational challenges. Growing demand for real-time tracking and better passenger services is encouraging transit authorities to invest in advanced solutions. While economic constraints and infrastructure gaps persist, rising focus on smart mobility and modernization is expected to drive steady market growth in the region.

Brazil Bus Dispatch Management System Market

The Brazil market in 2026 is estimated at around USD 0.01 billion, supported by urban transit modernization efforts, increasing demand for efficient fleet management, and gradual adoption of digital public transportation solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation-Driven Competition and Strategic Partnerships Shaping Market Dynamics

The global bus dispatch management system market is characterized by the presence of established technology providers and emerging digital mobility firms competing on innovation, scalability, and integration capabilities. Key players such as Trapeze Group, GIRO Inc., INIT GmbH, and Clever Devices focus on enhancing software-driven solutions with real-time tracking, AI-based scheduling, and cloud deployment. Companies are increasingly investing in R&D to strengthen predictive analytics and automation features. Strategic collaborations with transit authorities and smart city projects further enable vendors to expand their global footprint and improve solution customization across diverse operational environments.

In addition to established players, new entrants and niche technology firms are intensifying competition by offering cost-effective, cloud-native platforms with faster deployment capabilities. Market participants are differentiating through user-friendly interfaces, interoperability with existing transport systems, and cybersecurity enhancements. Mergers, acquisitions, and partnerships remain key strategies to gain technological expertise and regional access. Furthermore, vendors are focusing on Mobility-as-a-Service (MaaS) integration to align with evolving transportation ecosystems. As demand for intelligent transit solutions grows, competition is expected to center on data-driven innovation, service reliability, and long-term client engagement strategies.

LIST OF KEY BUS DISPATCH MANAGEMENT SYSTEM COMPANIES PROFILED IN REPORT

- Trapeze Group (Canada)

- Clever Devices (U.S.)

- INIT GmbH (Germany)

- GIRO Inc. (Canada)

- Optibus (Israel)

- IVU Traffic Technologies (Germany)

- Samsara Networks (U.S.)

- Verizon Connect (U.S.)

- Cubic Transportation Systems (U.S.)

- RouteMatch Software (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: INIT GmbH secured a contract in the Middle East to deploy its integrated dispatch and telematics solution for large-scale bus fleet operations.

- February 2026: Trapeze Group partnered with a European transit authority to deploy integrated cloud-based dispatch and passenger information systems, enhancing real-time fleet visibility and service efficiency.

- February 2026: GIRO expanded deployment of its HASTUS platform across North American transit agencies, improving workforce and fleet scheduling efficiency.

- January 2026: IVU Traffic Technologies secured new contracts in Asia Pacific for its IVU.suite dispatch and scheduling software implementation.

- January 2026: Clever Devices collaborated with the U.S. public transit agency to implement real-time bus tracking and automated dispatch communication systems.

- October 2025: Trapeze launched an upgraded intelligent transportation platform with AI-enabled scheduling and multimodal integration to support smart city transit ecosystems.

- September 2025: Optibus launched a cloud-native planning platform integrating real-time data and predictive analytics for transit agencies.

REPORT COVERAGE

The global bus dispatch management system market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Deployment Model, By Component, By Application, By Propulsion Type, and By Region |

| By Deployment Model |

|

| By Component |

|

| By Application |

|

| By Propulsion Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 0.51 billion in 2025 and is projected to reach USD 1.27 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 0.19 billion.

The market is expected to exhibit a CAGR of 10.5% during the forecast period of 2026-2034

The ICE segment is leading the market by propulsion type.

Rising urban transit demand and smart city initiatives to drive system adoption.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us