Bus Interior Components Market Size, Share & Industry Analysis, By Material Type (Plastics & Polymers, Metals/Composites, and Fabrics & Foams), By Application (OEM and Aftermarket/Replacement), By Bus Type (City/Transit Buses, Intercity Buses, Coach/Luxury Buses, and School Buses), By Component Type (Seating Systems, Flooring Systems, Interior Panels & Trims, Handrails & Safety Fittings, and Interior Systems & Modules), and Regional Forecast, 2026-2034

Bus Interior Components Market Size and Future Outlook

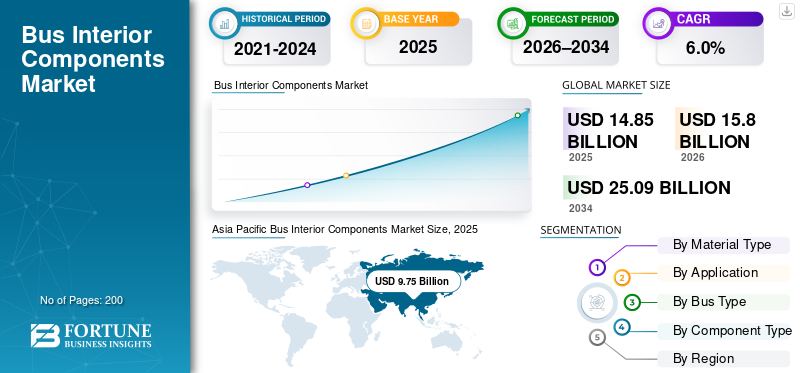

The global bus interior components market size was valued at USD 14.85 billion in 2025. The market is projected to grow from USD 15.8 billion in 2026 to USD 25.09 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period. Asia Pacific dominated the bus interior components market with a market share of 65.66% in 2025

Bus interior components comprise passenger-facing and functional systems installed inside buses, including seating, flooring, interior panels, handrails, safety fittings, and integrated modules that enhance comfort, safety, durability, accessibility, and operational efficiency. Rising public transport investments, urbanization, fleet replacement cycles, and growing adoption of electric buses drive the global market. Stricter safety and accessibility regulations, demand for lightweight, durable materials, and the increasing refurbishment of aging bus fleets further support sustained market growth. Major players include Adient, Grammer, Faurecia (FORVIA), Toyota Boshoku, Freedman Seating, and Yanfeng Automotive Interiors. These companies focus on lightweight materials, modular interiors, fire-safe designs, and partnerships with bus OEMs to support electrification-led interior innovation.

Download Free sample to learn more about this report.

Bus Interior Components Market Key Takeaways

- 2025 Market Size: USD 14.85 billion

- 2026 Market Size: USD 15.8 billion

- 2034 Forecast Market Size: USD 25.09 billion

- CAGR: 6.0% from 2026–2034

- Asia Pacific dominated the bus interior components market with a 65.66% share in 2025.

- The OEM segment held the leading market share driven by rising electric and transit bus production.

- The Flooring Systems segment dominated due to high durability and replacement frequency.

North America

North America is the fastest-growing regional market, driven by fleet modernization and electric bus adoption.

Asia Pacific

Asia Pacific dominated the global market in 2025 due to large-scale bus production and electrification programs.

Europe

Europe showed stable technology-driven growth supported by electric and hydrogen bus adoption.

U.S.

U.S. market reached USD 0.60 billion, supported by transit fleet modernization and electric bus adoption.

Japan

Japan market was valued at USD 1.42 billion in 2025.

Read More

BUS INTERIOR COMPONENTS MARKET TRENDS

Electrification and Advanced Interior Integration Enhance Component Demand

The global market trends are increasingly shaped by the electrification of buses and the integration of advanced interior systems. As bus OEMs transition from traditional diesel fleets to battery-electric and zero-emission platforms, demand for updated bus seating systems, lightweight flooring, digital displays, HVAC modules, and integrated safety features is gaining traction. Electrified buses require more sophisticated interior assemblies for thermal management, battery isolation, and passenger comfort, increasing per-vehicle interior content value. OEMs and suppliers are innovating to design modular interiors that support both electric powertrain packaging and next-generation passenger interfaces. The trend reflects a holistic shift in bus design strategies toward zero-emission, infotainment-ready interiors, driven by sustainability and passenger experience priorities.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Government Electrification Policies Accelerate Interior Component Adoption

Supportive government policies and infrastructure investments to electrify heavy-duty public transport are key drivers of the bus interior components market growth. Regulatory mandates to reduce carbon emissions and improve urban air quality are accelerating the replacement of diesel buses with electric models, raising demand for interior components tailored to these modern fleets. Electrification programs stimulate procurement of new buses with advanced interior systems that improve accessibility, safety standards, and passenger comfort. This trend bolsters both OEM production and aftermarket retrofit demand for seating, flooring, and integrated control modules. The policy impetus harmonizes with broader public transport modernization drives, ensuring long-term demand continuity for components aligned with zero-emission technologies.

- In November 2025, India’s e-bus penetration was forecast to rise significantly, driven by supportive government schemes such as PM E-DRIVE and government investments in public transportation However, delivery bottlenecks and supply constraints slowed adoption.

MARKET RESTRAINTS

Supply Chain Bottlenecks and Component Delays Limit Market Expansion

The market faces restraints from supply chain bottlenecks affecting deliveries of critical sub-assemblies and complete buses. Component suppliers, especially for electric buses, contend with shortages of batteries, specialized electronics, and imported powertrain parts, delaying new bus deliveries and interior installations. Delays in fulfilling bus orders constrain OEM production planning and slow the ramp-up of interior components, particularly in regions expanding e-bus adoption. Extended lead times for interior components reduce flexibility for fleet upgrades and aftermarket retrofits. These supply limitations also constrain smaller regional players and delay deployment of advanced interior technologies, potentially slowing near-term growth against rising electrification expectations.

MARKET OPPORTUNITIES

Urbanization and Fleet Modernization Open Growth for Modular Interiors

Rapid urbanization and the associated expansion of public transport present significant opportunities for suppliers of bus interior components. As cities in emerging and developed economies invest in modern transit fleets to reduce congestion and emissions, the need for updated interiors increases, creating demand for modular, durable seating, advanced flooring, and integrated safety and infotainment systems. Fleet modernization programs encourage upgrading older buses with newer interior modules to extend service life and enhance passenger comfort. There is further opportunity in designing interiors for accessibility compliance, such as wheelchair securement systems and priority seating solutions. Suppliers that align offerings with urban mobility plans stand to capture incremental growth as urban passenger volumes and comfort expectations rise.

MARKET CHALLENGE

Operational Reliability and Technical Failures Affect Adoption Rates

Operational reliability challenges and technical failure rates in advanced buses pose a significant challenge for the market. New electric buses and their complex electrical systems sometimes experience frequent breakdowns, which can diminish confidence among fleet operators and delay interior system upgrades or replacements. High maintenance demands and technical disruptions can shift fleet investment priorities away from interior enhancements to core operational stability. These challenges complicate lifecycle cost planning and delay the deployment of next-generation interior modules, thereby restricting market growth. The industry must address these performance issues through enhanced testing, quality assurance, and improvements in component durability to sustain long-term expansion of the interior market.

- In October 2025, Bengaluru reported over 13,000 breakdowns in its electric bus fleet over 2.5 years, highlighting operational reliability concerns that affect confidence in fleet and interior component investments.

Segmentation Analysis

By Material Type

Plastic & Polymers Segment Dominate Due to Lightweight Properties and Design Flexibility

Based on material type, the market is segmented into plastics & polymers, metals & composites, and fabrics & foams.

Among these, plastics & polymers dominate due to their lightweight properties, design flexibility in seat designers, corrosion resistance, and compliance with fire-retardant standards. These materials are extensively used in seat type, interior panels, seat shells, flooring layers, HVAC ducts, and lighting housings. Rising adoption of electric buses further strengthens demand, as OEMs focus on reducing vehicle weight to improve range and energy efficiency. Ease of mass production and lower lifecycle costs also make plastics and polymers the preferred choice for high-volume city and transit bus interiors in the global market.

- In July 2023, the European Commission reinforced fire safety and material compliance standards for vehicle interiors, encouraging wider use of certified polymer-based interior materials.

The fabrics & foams segment is projected to grow at a 10.0% CAGR over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Bus Type

High Passenger Density and Frequent Utilization Drive City/Transit Bus Segment Dominance

Based on bus type, the market is segmented into city/transit buses, intercity buses, coach/luxury buses, and school buses.

City/transit buses dominate interior component demand due to their high production volumes, dense interior layouts, and intensive daily usage. These buses require extensive seating, flooring, handrails, and safety fittings to support standing passengers and frequent boarding cycles. Urban electrification initiatives further increase the value of interior spaces as new layouts and modular systems are adopted. High wear rates also lead to frequent interior upgrades, reinforcing demand across both OEM and replacement channels for this segment.

- In June 2024, the International Energy Agency reported that city buses accounted for the majority of global electric bus deployments, driven by urban decarbonization policies.

The intercity buses segment is projected to grow at a CAGR of 8.3% over the forecast period.

By Application

Rising Bus Production Volumes Sustain OEM Segment Leadership

Based on application, the market is segmented into OEM and aftermarket/replacement.

The OEM segment dominates the market, driven by the continuous production of new buses for urban transit, school transportation, and intercity mobility. Government-funded fleet expansion and electrification programs are increasing new bus procurement, directly boosting demand for factory-installed interior components. OEM installations ensure standardized quality, regulatory compliance, and integration with vehicle architecture. As electric and low-floor buses require redesigned interior layouts, OEMs increasingly source advanced seating, flooring, and integrated interior modules, strengthening this segment’s share in overall market revenue.

- In March 2024, the U.S. Federal Transit Administration announced additional funding allocations for zero-emission bus procurement under public transit programs.

The aftermarket/replacement segment is projected to grow at a CAGR of 8.7% over the forecast period.

By Component Type

Durability and Replacement Cycles Strengthen Flooring Systems Segment Leadership

Based on component type, the market is segmented into seating systems, flooring systems, interior panels & trims, handrails & safety fittings, and interior systems & modules.

Flooring systems dominate the component landscape due to their universal presence across all bus types and high replacement frequency. Bus flooring must withstand heavy foot traffic, moisture, and harsh operating conditions, particularly in city and school buses. Materials such as PVC, rubber, and composite laminates are widely used for their durability and anti-slip properties. Hygiene requirements and refurbishment programs further drive recurring demand, making flooring systems a consistent revenue contributor across OEM and aftermarket applications.

- In September 2023, Transport for London updated its bus refurbishment guidelines, emphasizing anti-slip and easy-to-clean flooring standards and standard seats.

The interior systems & modules segment is projected to grow at a 7.7% CAGR over the forecast period.

BUS INTERIOR COMPONENTS MARKET REGIONAL OUTLOOK

By region, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Bus Interior Components Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global bus interior components market share due to its massive bus production base, extensive electrification programs, and expanding urban transit networks. High OEM demand is driven by city and transit buses, while cost effective materials dominate interiors. The region benefits from scale-driven manufacturing and strong government-led public transport investments.

China Bus Interior Components Market

China leads globally with a share of 54.9%, supported by large-scale electric bus production and deployment. Interior component demand emphasizes lightweight plastics, integrated interior modules, and standardized seating systems to support high-volume manufacturing.

India Bus Interior Components Market

India’s market is expanding rapidly with a CAGR of 9.6%, due to growing urban transit projects and rising demand for school buses. OEM-driven interiors dominate, with rising demand for durable seating, flooring, and safety fittings across city and intercity buses.

Japan Bus Interior Components Market

Japan focuses on high-quality, durable bus interiors with a strong emphasis on passenger comfort and reliability. Demand is driven by technologically advanced seating systems, premium materials, and precision-engineered interior modules. Japan was valued at USD 1.42 billion in 2025.

North America

North America is the fastest-growing regional market for bus interior components, driven by accelerated fleet replacement cycles, rising adoption of electric buses, and strong public funding support for urban transit modernization. The region shows increasing demand for compliant seating systems, anti-slip flooring, modular interiors, and accessibility-focused safety fittings. Growing refurbishment of aging fleets further strengthens aftermarket demand, particularly in city and school bus segments.

U.S. Bus Interior Components Market

The U.S. market leads with value of USD 0.60 billion, North America due to large-scale transit fleet upgrades and rapid adoption of electric buses. Demand is concentrated on OEM-installed seating, flooring, and integrated interior modules, supported by federal zero-emission transit programs and strict accessibility regulations. The aftermarket is expanding as transit agencies extend fleet life through interior refurbishment.

Europe

Europe shows stable, technology-driven growth in the market, supported by fleet renewal mandates, safety regulations, and the increasing penetration of electric and hydrogen buses. Interior component demand emphasizes fire-resistant materials, lightweight composites, and high-quality passenger comfort features. OEM-led demand dominates, with selective aftermarket growth tied to refurbishment programs.

Germany Bus Interior Components Market

Germany is a key contributor, driven with a CAGR of 6.5%, by advanced bus manufacturing and early adoption of next-generation electric and hydrogen buses. Interior demand focuses on premium seating, advanced flooring, and integrated driver cockpit modules aligned with high technical standards.

U.K. Bus Interior Components Market

Large-scale city bus upgrades and zero-emission fleet targets drive the U.K. market. Demand centers on durable seating systems, easy-to-maintain flooring, and modular interior panels, supported by public transport decarbonization initiatives. U.K. valued at USD 0.28 billion in 2025.

Rest of the World

The rest of the world market shows moderate but steady growth, supported by urbanization and gradual public transport upgrades in Latin America and the Middle East & Africa. Demand favors cost-effective, durable interior components, with increasing opportunities in refurbishment and replacement as fleets age. OEM demand remains dominant, while aftermarket growth strengthens in high-utilization urban fleets.

COMPETITIVE LANDSCAPE

Key Industry Players

Lightweight Materials, Modular Designs, and OEM Partnerships Define Bus Interior Components Competitiveness

The global market is shaped by increasing emphasis on lightweight materials, modular interior architectures, and close collaboration between bus OEMs and component suppliers. Leading players such as Adient, Grammer, FORVIA (Faurecia), Toyota Boshoku, Freedman Seating, Yanfeng Automotive Interiors, and Kiel Group compete through durable seating systems, advanced flooring solutions, fire-safe interior panels, and integrated interior modules. Companies focus on improving lifecycle durability, ease of maintenance, and compliance with stringent safety and accessibility regulations. Competitive advantage is strengthened through localized manufacturing, long-term OEM supply contracts, and customization capabilities for city, intercity, and electric buses. Suppliers are also investing in sustainable materials, weight reduction, and modular product platforms to support fleet electrification and the demand for refurbishment. Strategic partnerships with bus manufacturers and transit authorities enable faster adoption of standardized yet flexible interior solutions across global public transport fleets.

LIST OF KEY BUS INTERIOR COMPONENTS COMPANIES PROFILED

- Adient plc (Ireland)

- Grammer AG (Germany)

- Faurecia SE – FORVIA Group (France)

- Toyota Boshoku Corporation (Japan)

- Freedman Seating Company (U.S.)

- Kiel Group (Germany)

- RECARO Automotive Seating (Germany)

- Harita Seating Systems Ltd. (India)

- Lazzerini Srl (Italy)

- USSC Group Inc. (U.S.)

- Continental AG – Interior & HMI Solutions (Germany)

- Bosch Mobility Solutions (Germany)

- Fainsa Group (Spain)

- Trapeze Group (Canada)

- Luminator Technology Group (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: B-Style introduced B-Safe, a head-and-back support system for B-Active wheelchair-accessible vehicles, designed to improve passenger stability and protection during sudden braking or impacts. The launch reflects the growing emphasis on accessibility-focused interior safety fittings and specialized seating components such as recliner seats across par transit and adapted bus fleets.

- November 2025: Prima Industries unveiled INSTATOP, a wireless pushbutton system for urban buses showcased at Busworld Europe 2025. Designed to simplify installation and increase flexibility compared to traditional wired stop buttons, the product targets the demand for interior modules, especially during refurbishments, where rewiring time and downtime strongly affect fleet economics.

- October 2025: Compin Fainsa announced it would showcase a new coach seat at Busworld 2025 (Brussels), highlighting ongoing product refresh cycles in premium bus interiors. The focus on next-generation seating supports higher-value coach and intercity applications where comfort, ergonomics, and weight optimization increasingly influence OEM sourcing decisions.

- October 2025: NFI Group and GILLIG formed a 50/50 joint venture to acquire the assets of American Seating, a key producer of seating for transit buses and motorcoaches. The move aimed to strengthen seat supply continuity, support backlog execution, and invest in operational recovery, directly impacting a core bus interior component category.

- June 2025: Camira launched its SEAQUAL Collection, positioning it as an interior transport fabric made from recycled marine plastic waste, aligned with sustainability goals in bus and coach interiors. The launch supports OEM and retrofit programs seeking lower-impact materials for seating upholstery while meeting durability and safety expectations in public transport.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.0% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material Type, Application, Bus Type, Component Type, and Region |

| By Material Type |

|

| By Application |

|

| By Bus Type |

|

| By Component Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 14.85 billion in 2025 and is projected to reach USD 25.09 billion by 2034.

In 2025, the market value stood at USD 9.75 billion.

The market is expected to grow at a CAGR of 6.0% during the forecast period.

The OEM segment led the market share in the application segment.

The government electrification policies accelerate the adoption of interior components.

Key market players include Adient, Grammer, Faurecia (FORVIA), Toyota Boshoku, and Freedman Seating.

Asia Pacific accounted for the largest share in the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world regions are considered in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us