Calcium Phosphate Market Size, Share & Industry Analysis, By Form (Powder, Granules, Crystals, and Liquid/Suspension), By End Use Industry (Agriculture & Animal Nutrition, Healthcare & Pharmaceuticals, Food Processing, Chemicals, Cosmetics & Personal Care, and Others), and Regional Forecast, 2026-2034

Calcium Phosphate Market Size and Future Outlook

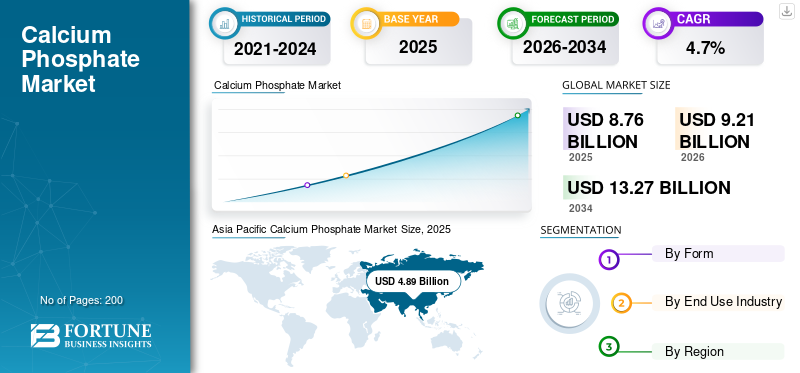

The global calcium phosphate market size was valued at USD 8.76 billion in 2025. The market is projected to grow from USD 9.21 billion in 2026 to USD 13.27 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period. Asia Pacific dominated the calcium phosphate market with a market share of 55.82% in 2025.

Calcium phosphate refers to a family of calcium salts of phosphoric acid that are widely used across feed-grade mineral nutrition, food additives, pharmaceutical excipients, nutraceutical formulations, fertilizer inputs, and selected industrial and personal care applications. Commercial demand centers on tricalcium phosphate, dicalcium phosphate, monocalcium phosphate, hydroxyapatite, and related grades, supplied as powder, granules, crystals, or liquid or suspension forms, depending on performance, purity, and processing requirements.

The market growth is driven by its broad applications in mineral fortification, livestock nutrition, controlled phosphorus delivery, and pharmaceutical and nutraceutical formulations. The product consumption is further supported by the demand for feed phosphates in compound feed, anti-caking and fortification uses in food processing, expanding use of bioceramic and exacipient-grade materials in healthcare, and the steady requirement for technical phosphates in chemicals and specialty manufacturing.

Furthermore, the market comprises several major players, including ICL Group Ltd., Innophos, Budenheim, Phosphea, and OCP Group, as well as other regional phosphate and specialty-ingredient suppliers. Product purity, source integration, regulatory approvals, feed and food registration capabilities, technical application support, and distribution reach continue to influence the competitive positioning in the global market.

Download Free sample to learn more about this report.

CALCIUM PHOSPHATE MARKET TRENDS

Feed Mineral Optimization, Clean-Label Fortification, and Higher-Purity Healthcare Grades

The product demand is increasingly shaped by the optimization of mineral nutrition in livestock and poultry, a growing preference for stable, multifunctional food ingredients, and stricter quality requirements in pharmaceutical and nutraceutical formulations. Feed-grade dicalcium phosphate and monocalcium phosphate continue to benefit from large-scale compound feed production, while food-grade tricalcium phosphate remains relevant in anti-caking, fortification, and texture-management applications. This supports a balanced demand profile across high-volume agricultural channels and higher-value regulated end uses.

At the same time, manufacturers are giving greater attention to specialty hydroxyapatite, purified calcium phosphate excipients, and differentiated particle-engineering solutions for tablets, dietary supplements, and biomedical applications. Portfolio strategies increasingly emphasize purity control, contaminant management, traceability, and formulation support as customers seek performance consistency in regulated applications. As a result, suppliers are positioning the compound as a commodity phosphate input and a value-added ingredient serving feed, food, healthcare, and industrial customers.

- For instance, calcium phosphate grades remain widely used in feed mineral supplementation, food fortification, and anti-caking, and selected pharmaceutical and bioceramic formulations where phosphorus-calcium balance, purity, and processing functionality are important.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Feed-Grade Mineral Demand, Nutrition Fortification, and Healthcare Functional Use to Support Product Consumption

Animal nutrition remains the dominant demand center, supported by the need to deliver bioavailable phosphorus and calcium in poultry, swine, ruminant, and aquaculture diets. Dicalcium phosphate and monocalcium phosphate are widely used as they combine mineral density, compatibility with compound feed systems, and a well-established role in supporting skeletal development and productivity. This creates a large and relatively resilient demand base across major livestock-producing regions.

Beyond feed, food processing and healthcare applications are supporting calcium phosphate market growth. The compound continues to be used in food fortification, anti-caking systems, tablet formulations, and nutraceutical products where mineral content, flow properties, and formulation stability matter. Producers that can serve both volume-driven feed channels and specification-driven food and healthcare uses are, therefore, better positioned to capture broad-based growth.

MARKET RESTRAINTS

Raw-Material Cost Exposure, Regulatory Stringency, and Application-Specific Substitution May Restrict Market Expansion

While calcium phosphate remains an essential material across several sectors, the market is exposed to volatility in phosphoric acid, phosphate rock, purification chemistry, and energy-linked processing costs. Production economics can tighten when feedstock pricing rises or environmental compliance costs increase, especially for food-grade and pharmaceutical-grade materials, where purity control adds cost and complexity.

The market also faces substitution risk in selected applications. Alternative mineral sources, chelated nutrition products, other phosphate salts, carbonate-based fillers, and crop- or species-specific formulation changes may reduce the intensity of direct calcium phosphate use depending on performance targets and cost relationships. These factors can pressure margins and make adoption more sensitive to customer qualification cycles and regulatory requirements.

MARKET OPPORTUNITIES

Premium Excipients, Functional Nutrition, and Specialty Bioceramic Applications to Create Lucrative Growth Opportunities

Hydroxyapatite and highly controlled tricalcium phosphate grades are gaining interest in specialty medical, dental, and bone-regeneration applications, while tablet and supplement manufacturers continue to seek excipients with reliable compression and mineral-delivery performance.

Additional opportunities exist in clean-label food systems, advanced premix solutions, and differentiated feed phosphates that improve formulation efficiency or traceability. Suppliers that combine process integration with strong technical support, regulatory documentation, and customer-specific grade development are better positioned to capture incremental value outside purely volume-driven channels.

MARKET CHALLENGES

Qualification Timelines, Purity Expectations, and Multi-Industry Compliance Requirements May Hamper Market Growth

Manufacturers and distributors must navigate feed registration, food additive rules, pharmacopoeial compliance, impurity thresholds, and customer-specific validation requirements across multiple end-use industries. This increases complexity in product qualification, production planning, and documentation management, especially for suppliers serving both bulk and specialty channels.

In addition, end users are increasingly focused on bioavailability, contaminant control, formulation consistency, and total system cost rather than only purchase price. Suppliers, therefore, need dependable quality systems, flexible production capabilities, and strong application support to sustain long-term growth while maintaining customer confidence across regulated and performance-sensitive markets.

Segmentation Analysis

By Form

Powder Segment Led the Market Owing to Wide Usage in Feed Premixes

Based on form, the market is segmented into powder, granules, crystals, and liquid/suspension.

The powder segment accounted for the largest calcium phosphate market share in 2025. The segment growth is driven by its broad use in feed premixes, mineral blends, food additive systems, pharmaceutical excipients, and technical formulations where dry handling, blend uniformity, and ease of dosing are important. Furthermore, the segment held a 51.7% share in 2025.

The granules segment is expected to grow significantly, driven by the rising use in fertilizer blends, feed applications requiring improved handling characteristics, and specialty formulations where reduced dusting and better flow properties support processing efficiency. The calcium segment is projected to grow at a CAGR of 4.5% during the analysis period.

By End Use Industry

To know how our report can help streamline your business, Speak to Analyst

Agriculture & Animal Nutrition Segment Dominated the Market Due to the Extensive Use of the Product

By end-use industry, the market is categorized into agriculture & animal nutrition, healthcare & pharmaceuticals, food processing, chemicals, cosmetics & personal care, and others.

The agriculture & animal nutrition segment accounted for the largest share in 2025. The segment growth is driven by the widespread use of calcium phosphate as a mineral source in livestock feed, premixes, and nutrient systems, as well as by its role in selected fertilizer and soil nutrition applications. Furthermore, the segment held a 42.5% share in 2025.

The healthcare & pharmaceuticals segment is expected to grow favorably over the forecast period. The segment growth is driven by the continued product use in pharmaceutical excipients, nutraceutical formulations, bone-health products, and bioceramic applications, where controlled purity and mineral-delivery performance are critical. The segment is expected to grow at a CAGR of 4.4% over the forecast period.

Calcium Phosphate Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Calcium Phosphate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 4.89 billion, and is expected to maintain its leading share in 2026 with a value of USD 5.17 billion. The region benefits from large-scale feed production, strong demand for food processing, broad healthcare manufacturing activity, and the central role of China and India in global phosphate consumption. The regional growth is also rising with the demand for mineral ingredients. China remains the largest market, while India, Japan, South Korea, and the broader Asia Pacific region continue to support demand, driven by feed mineral requirements, fortification uses, pharmaceutical production, and diverse industrial processing needs.

China Calcium Phosphate Market

In 2025, the China market touched USD 1.95 billion. The product demand is supported by its large feed and food-processing base, extensive phosphate-chemistry ecosystem, and substantial pharmaceutical-manufacturing footprint. The market growth in the country is also impelled by the continued product use across mineral nutrition, excipients, and technical applications.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, with the market estimated to reach USD 0.84 billion by 2026. The market’s growth is driven by strong adoption in food ingredients, nutraceuticals, and pharmaceutical excipients, alongside established use in animal nutrition and selected industrial applications. Application intensity remains strong in the U.S., supported by its large healthcare and dietary supplement markets, developed feed sector, and robust regulatory and formulation infrastructure.

U.S. Calcium Phosphate Market

In 2025, the U.S. market reached USD 0.65 billion. The U.S. market dominates regional consumption due to its large food, nutraceutical, and pharmaceutical base, significant demand for feed phosphates, and established product use in excipients, fortification systems, and specialty formulations.

Europe

The Europe market is expected to experience significant growth in the coming years. The market is estimated to touch a value of USD 1.30 billion in 2026 and is projected to grow at a CAGR of 3.1% over the forecast period. The market’s growth is supported by the demand for efficient mineral nutrition, continued use of food-grade anti-caking and fortification ingredients, and strong adoption of regulated excipient-grade materials. The region benefits from mature feed and food systems, high formulation standards, and an emphasis on quality, compliance, and supply security.

U.K. Calcium Phosphate Market

The U.K. market reached a valuation of around USD 0.20 billion in 2025, representing approximately 2.5% of the global market revenue.

Germany Calcium Phosphate Market

The Germany market touched a value of approximately USD 0.27 billion in 2025, accounting for about 3.4% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market is expected to reach a valuation of USD 0.42 billion in 2026. The product demand is concentrated in livestock nutrition, food processing, and selected industrial uses, supported by large-scale animal production systems, regional feed manufacturing, and growing demand for processed foods. Strong agricultural economics and rising premix consumption continue to support the regional product demand.

Brazil Calcium Phosphate Market

The Brazil market reached a value of approximately USD 0.15 billion in 2025, equivalent to around 4.6% of global sales.

Middle East & Africa

The Middle East & Africa region is gradually expanding, driven by food-security priorities, rising feed demand, selected food and pharmaceutical applications, and the strategic role of regional phosphate and mineral ingredient suppliers. Agriculture & animal nutrition remains the region’s most important application, while regulated food and healthcare uses continue to contribute incremental demand growth.

GCC Calcium Phosphate Market

The GCC market reached a value of USD 0.59 billion in 2025, accounting for approximately 4.6% of global revenues. The product demand in the GCC is supported by investments in feed and food security, integrated phosphate value chains, and the continued product use in controlled agricultural systems, nutrition products, and technical channels.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Application Support and Particle-Engineering Capabilities to Maintain their Market Positions

The market includes a mix of phosphate-integrated producers, feed phosphate manufacturers, specialty ingredient suppliers, and excipient-focused companies that supply calcium phosphate materials across agricultural, food, pharmaceutical, nutraceutical, and selected industrial end uses. The competitive position is defined by access to phosphate intermediates, purification and particle-engineering capabilities, regulatory compliance, application support, and the ability to maintain quality consistency across multiple grades and geographies.

Leading companies differentiate through feedstock integration, formulation support, contaminant control, downstream registrations, and the flexibility to serve both volume-based and specialty end uses. Some key market players include ICL Group Ltd., Innophos, Budenheim, Phosphea, and OCP Group.

LIST OF KEY CALCIUM PHOSPHATE COMPANIES PROFILED

- ICL Group Ltd. (Israel)

- Innophos Holdings, Inc. (U.S.)

- Budenheim (Germany)

- Phosphea (France)

- OCP Group (Morocco)

- Yara International ASA (Norway)

- EuroChem Group (Switzerland)

- Fosfitalia Group (Italy)

- Tokyo Chemical Industry (India) Pvt. Ltd (India)

- J J CHEMICALS (India)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Innophos launched VersaCal Bright, a calcium phosphate-based clean-label whitening alternative to titanium dioxide for selected food uses, following FDA approval of Innophos’ calcium phosphate color-additive petition. This move is aimed at tapping into the stronger growth potential for food-grade calcium phosphate in bakery, confectionery, and processed food reformulation.

- July 2025: Brenntag began offering Budenheim phosphate-based excipients to pharma customers across Germany, France, Benelux, Poland, and the Nordics. The step indicates wider commercial reach for calcium-phosphate-based excipients in oral solid dosage and mini-tablet applications.

- August 2024: Prayon acquired Natural Enrichment Industries (NEI) in the U.S., a producer of calcium phosphate salts (TCP), adding production sites in Herrin and Sesser, Illinois. The move signals stronger North American capacity and broader offerings of food and technical calcium phosphate.

- July 2024: Ventris Medical received a U.S. patent for producing an osteoinductive calcium phosphate for bone grafting, including β-tricalcium phosphate/hydroxyapatite granules. The development depicts continued innovation and higher-value growth opportunities for medical-grade calcium phosphate applications.

- April 2024: Innophos upgraded its Chicago Heights, Illinois, production facility for EC-grade calcium phosphates. The move improved manufacturing flexibility for European food and dietary supplement demand and signals tighter alignment with high-purity, regulation-compliant calcium phosphate requirements.

- April 2023: Innophos added LEVAIR Select, a calcium-based alternative to sodium aluminum phosphate for bakery formulations. The move signals the broader adoption of calcium-based phosphate systems in clean-label and reduced-aluminum food applications.

- September 2022: Innophos launched new LEVAIR baking solutions, expanding its portfolio of ingredient systems for bakery performance and formulation flexibility. This indicates rising supplier focus on specialty phosphate innovation for value-added food applications.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.7% from 2026 to 2034 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Form, End Use Industry, and Region |

| By Form |

|

| By End Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market size stood at USD 8.76 billion in 2025 and is projected to reach USD 13.27 billion by 2034.

The market is slated to exhibit steady growth at a CAGR of 4.7% during the forecast period of 2026-2034.

By end-use industry, the fertilizer segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

ICL Group Ltd., Innophos, Budenheim, Phosphea, and OCP Group are some of the prominent players in the market.

The key factor driving market growth is the rising demand from agriculture and animal nutrition sectors.

The major factors expected to favor product adoption include its widespread use in feed fortification, food processing, pharmaceuticals, and fertilizers, driven by its nutritional value, functional versatility, and broad industrial applicability.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us