Cancer Vaccines Market Size, Share & Industry Analysis, By Type (Preventive and Therapeutic), By Technology (Molecular-based, Vector-based, and Cell-based), By Indication (Cervical Cancer, Bladder Cancer, Prostate Cancer, Lung Cancer, and Others), By Distribution Channel (Hospitals, Government & Organization Supply, and Others), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

Cancer Vaccines Market Size and Future Outlook

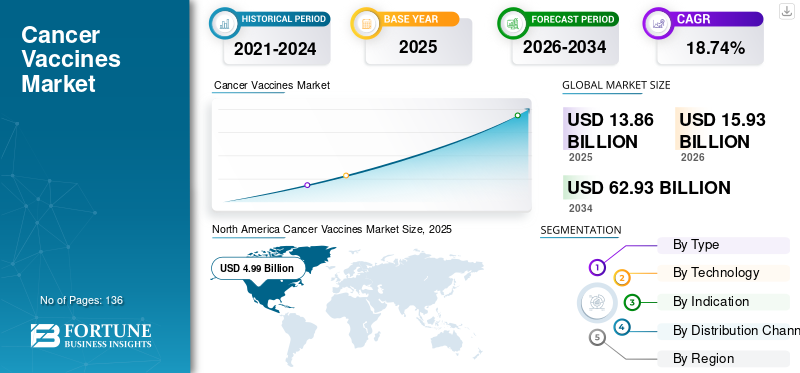

The cancer vaccines market size was valued at USD 11.62 billion in 2025. The market is projected to grow from USD 12.71 billion in 2026 to USD 45.37 billion by 2034, exhibiting a CAGR of 17.25% during the forecast period. North America dominated the cancer vaccines market with a market share of 38.3% in 2025.

The global cancer vaccines market includes preventive vaccines that reduce the risk of virus-related cancers and therapeutic vaccines that help the immune system identify and attack cancer cells. The market is gaining significant momentum as cancer care is gradually moving toward earlier prevention, immune-based treatment, and more personalized therapy. As cancer incidence continues to rise, healthcare providers and drug developers are focusing on vaccine approaches that can either prevent cancer-causing infections or reduce the risk of recurrence after treatment. As a result, cancer vaccines are becoming an important area of innovation within oncology, supported by advances in mRNA technology, tumor sequencing, neoantigen discovery, and combination immunotherapy.

- For instance, in January 2026, Moderna and Merck announced five-year data for intismeran autogene, their individualized mRNA cancer vaccine candidate, in combination with KEYTRUDA for patients with high-risk stage III/IV melanoma after complete resection.

Key players in the market include Dendreon Pharmaceuticals LLC., Serum Institute of India Pvt. Ltd, Merck & Co., Inc., and GSK plc. They expand research and development activities for innovative therapeutic and preventive cancer vaccines, along with an increasing pipeline of candidates, which are major factors supporting the market growth.

Download Free sample to learn more about this report.

VACCINES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 11.62 Billion

- 2026 Market Size: USD 12.71 Billion

- 2034 Forecast Market Size: USD 45.37 Billion

- CAGR: 17.25% from 2026–2034

- North America dominated the cancer vaccines market with a 38.3% share in 2025.

- The therapeutic segment is expected to register the fastest growth at a CAGR of 24.34% during the forecast period.

- The cell-based segment is projected to grow at a CAGR of 16.08% during the forecast period.

North America

North America generated USD 4.45 billion in 2025, driven by strong immuno-oncology research and rapid adoption of personalized cancer vaccines.

Europe

Europe is projected to reach USD 3.98 billion in 2026, supported by government-backed cancer prevention programs and active clinical research.

Asia Pacific

Asia Pacific is expected to reach USD 3.22 billion in 2026, fueled by rising cancer incidence and expanding healthcare access.

U.S.

The market is estimated at USD 4.33 billion in 2026, accounting for approximately 34.07% of global revenue.

Japan

The market is projected to reach USD 0.33 billion in 2026, representing about 2.60% of global revenue.

Read More

CANCER VACCINES MARKET TRENDS

Growing Use of AI and Bioinformatics in Identifying Cancer Vaccine Targets for Vaccine Development

A significant global trend in the market is the integration of AI and bioinformatics tools to accelerate and improve the identification of tumor-specific targets. Traditional target discovery can take significant time and may miss complex tumor antigens, whereas AI-based platforms can analyze genomic, proteomic, and immune response data at scale. These factors help companies identify neoantigens and other cancer-associated targets that are more likely to trigger a strong immune response. As a result, AI and bioinformatics are improving the design of personalized and precision cancer vaccines, reducing early research uncertainty, and supporting the development of vaccines for cancers where standard immunotherapy options remain limited.

- For instance, in November 2025, Evaxion expanded its R&D pipeline with EVX-04, an AI-designed precision cancer vaccine candidate for acute myeloid leukemia. The study noted that EVX-04 was developed using its AI-Immunology platform and targets multiple non-conventional ERV tumor antigens, demonstrating how AI can identify new vaccine targets and support precision cancer vaccine development.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expanding Use of Immunotherapy Combinations for Therapeutic Cancer Vaccine Development Fuels Market Growth

The key driver of the cancer vaccines market growth is the rising use of therapeutic cancer vaccines in combination with established immunotherapies, particularly checkpoint inhibitors. Cancer vaccines are designed to train the immune system to recognize tumor-specific antigens. At the same time, checkpoint inhibitors help remove signals that suppress immune responses and prevent T cells from attacking cancer cells. When both approaches are used together, the vaccine can help generate a targeted immune response, and the checkpoint inhibitor can help sustain that response inside the tumor environment. As a result, combination strategies are becoming an important driver of therapeutic cancer vaccine development, as they may improve response durability, reduce recurrence risk, and expand the use of cancer vaccines across melanoma, lung cancer, and other solid tumors.

- For instance, in October 2024, Merck and Moderna announced the initiation of a Phase 3 trial evaluating V940 (mRNA-4157), an individualized neoantigen therapy, in combination with KEYTRUDA (pembrolizumab) after neoadjuvant KEYTRUDA and chemotherapy in patients with certain non-small cell lung cancer subtypes. The companies stated that this trial expanded the INTerpath clinical program and showed continued development of V940 in combination with anti-PD-1 therapy across earlier-stage cancers.

MARKET RESTRAINTS

Limited Clinical Success of Therapeutic Cancer Vaccines May Slow Market Growth

A key factor restraining market growth is the limited clinical success of cancer vaccines. Many candidates have shown immune activation in studies but have not consistently delivered strong clinical benefits, such as tumor reduction, improved survival, or durable disease control. These factors create uncertainty for investors, regulators, and healthcare providers, as a vaccine must demonstrate measurable patient benefit rather than just immune response. As a result, repeated clinical setbacks can slow approvals, increase development costs, erode confidence in late-stage programs, and delay the faster adoption of therapeutic cancer vaccines in oncology care.

- For instance, a 2025 systematic review published in eClinicalMedicine reported that therapeutic anticancer vaccines in common hematological malignancies generally demonstrated immunogenicity but mostly failed to show consistent anticancer activity. The review also highlighted challenges such as small study sizes, heterogeneous interventions, and unclear endpoint definitions, underscoring why limited clinical success remains a major restraint to therapeutic cancer vaccine development.

MARKET OPPORTUNITIES

Rising Development of Personalized Neoantigen Vaccines Creates Strong Growth Opportunities

The global market is moving toward more personalized treatment approaches as companies aim to design vaccines tailored to each patient’s tumor mutation profile. Such a shift creates a significant growth opportunity as neoantigen vaccines can train the immune system to recognize cancer-specific targets. As tumor sequencing, AI-based antigen prediction, and mRNA delivery platforms continue to improve, vaccine developers can identify stronger targets and produce patient-specific vaccines more efficiently. As a result, personalized neoantigen vaccines are expected to expand the role of cancer vaccines in recurrence prevention, adjuvant therapy, and combination treatment with checkpoint inhibitors.

- For instance, in December 2025, NEC Bio Therapeutics announced Phase I results for NECVAX-NEO1, its personalized AI-powered oral cancer vaccine, at the ESMO Immuno-Oncology Congress 2025. The trial data confirmed safety and immunogenicity and provided clinical proof-of-concept for the investigational oral bacteria-based DNA vaccine in patients with solid tumors, underscoring the market growth opportunity for personalized neoantigen vaccine platforms.

MARKET CHALLENGES

Complex Manufacturing and Regulatory Requirements May Challenge Commercial Scale-Up of Cancer Vaccines

The global market is expected to face challenges as many next-generation cancer vaccines, especially personalized neoantigen vaccines, require tumor sequencing, antigen prediction, customized manufacturing, rigorous quality testing, and timely patient delivery. This creates a longer, more complex production pathway than for conventional oncology drugs. As a result, companies may face higher manufacturing costs, batch-to-batch standardization issues, regulatory uncertainty, and slower clinical-to-commercial scale-up, which can limit broader access and delay market expansion.

- For instance, a 2025 review published in Oncology Reviews highlighted that personalized neoantigen-based cancer vaccines face several challenges in development and clinical deployment, including tumor heterogeneity, immune evasion, manufacturing complexity, safety concerns, and limited response rates in some patient populations. Such development highlights how operational barriers remain major challenges to wider global market growth.

Segmentation Analysis

By Type

Preventive Segment Dominated as It Reduces Risk of Virus-related Cancers

By type, the global market is segmented into preventive and therapeutic.

The preventive segment dominated the cancer vaccines market share in 2025, as HPV and hepatitis B vaccines are already widely used in public health programs to reduce the risk of virus-related cancers. Preventive vaccines have received regulatory approval, broader population-level use, and stronger government procurement support. HPV vaccination is especially important as it directly helps prevent cervical cancer and other HPV-related cancers, creating great demand through national immunization programs, school-based vaccination, and global health initiatives. As a result, preventive cancer vaccines generate stronger current market adoption and revenue compared with therapeutic vaccines, while therapeutic vaccines continue to build future growth potential through clinical pipelines.

- For instance, in March 2026, Merck & Co., Inc. announced new data reinforcing the long-term efficacy of GARDASIL9 and GARDASIL at the EUROGIN International Multidisciplinary HPV Congress. The company highlighted data supporting protection against certain HPV-related cancers and diseases, demonstrating that established preventive cancer vaccines continue to strengthen market demand and reinforce the dominance of the preventive segment.

The therapeutic segment is expected to grow at a CAGR of 24.34% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Molecular-based Segment Dominates Market as It Helps Immune System Recognize Cancer Cells More Precisely

Based on technology, the market is segmented into molecular-based, vector-based, and cell-based.

The molecular-based segment dominates the market as it includes DNA, RNA, peptide, and protein-based vaccine approaches suitable for personalized and targeted cancer vaccine development. These platforms encode or deliver tumor-specific antigens, helping the immune system recognize cancer cells more precisely. The segment is further supported by advances in mRNA technology, genomic sequencing, and AI-based antigen selection, enabling companies to design vaccines more quickly and tailor them to each patient’s tumor profile. As a result, molecular-based cancer vaccines are becoming the preferred technology platform for next-generation therapeutic cancer vaccine pipelines.

- For instance, in January 2026, in 2026, Merck and Moderna announced five-year data for intismeran autogene, also known as mRNA-4157/V940, in combination with KEYTRUDA. The companies stated that the investigational therapy is an mRNA-based, individualized neoantigen therapy encoding up to 34 neoantigens based on a patient’s tumor's unique mutational signature, highlighting why molecular-based platforms are driving cancer vaccine innovation.

The cell-based segment is expected to grow at a CAGR of 16.08% over the forecast period.

By Indication

Cervical Cancer Segment Dominated as It is One of the Most Vaccine-Preventable Cancers

By indication, the market is segmented into cervical cancer, bladder cancer, prostate cancer, lung cancer, and others.

The cervical cancer segment dominated the market in 2025, as it is one of the most vaccine-preventable cancers, given its strong association with human papillomavirus infection. HPV vaccines have a clear preventive role in reducing cervical cancer risk, which makes this indication more commercially established than many therapeutic cancer vaccine indications that are still in clinical development. Governments, public health agencies, and manufacturers are also expanding HPV vaccination access to improve prevention among girls, women, and eligible male populations. As a result, cervical cancer holds a leading position as it combines high disease burden, clear vaccine-prevention evidence, and broad public health implementation.

- For instance, the American Cancer Society estimated that 13,490 new cervical cancer cases would be diagnosed in 2026 in the U.S.

The lung cancer segment is expected to grow at a CAGR of 36.00% over the forecast period.

By Distribution Channel

Hospitals Segment Dominated Owing to a Substantial Number of Outpatient Visits & Easy Availability of Vaccines

Based on the distribution channel, the market is segmented into hospitals, government & organization supply, and others.

The hospitals segment held the dominant share in 2025. The dominance was attributed to increasing cancer prevalence and high outpatient visits by individuals to hospitals for primary screening and consultations regarding cancer. Moreover, the high availability and supply of products such as vaccines in hospital settings, along with patients' preference for vaccination at nearby, well-equipped healthcare centers, further boosted the segment's share. This segment held 55.2% of the market share in 2025.

- For instance, in April 2025, NHS England expanded its Cancer Vaccine Launch Pad to fast-track eligible melanoma patients into personalized cancer vaccine trials at participating hospitals. The development supported the hospital channel by showing that hospitals remain the key setting for screening, trial enrollment, vaccine delivery, and patient monitoring.

The government & organization supply segment is expected to grow at a CAGR of 16.74% over the forecast period.

Cancer Vaccines Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cancer Vaccines Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 4.38 billion and maintained its leading position in 2025 at USD 4.45 billion. The North America market is growing due to strong immuno-oncology research, high cancer burden, advanced clinical trial infrastructure, and faster adoption of mRNA and personalized cancer vaccine platforms.

U.S. Cancer Vaccines Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 4.33 billion in 2026, accounting for roughly 34.07% of the global revenues.

Europe

Europe is projected to grow at 15.98% in the coming years, the second-highest among all regions, and reach a valuation of USD 3.98 billion by 2026. Strong public health vaccination programs, government-backed cancer-prevention initiatives, and active clinical research on therapeutic and personalized cancer vaccines support regional growth.

U.K. Cancer Vaccines Market

The U.K. market is estimated at around USD 0.95 billion in 2026, representing roughly 7.49% of the global revenues.

Germany Cancer Vaccines Market

Germany's market is projected to reach approximately USD 1.10 billion in 2026, equivalent to around 8.69% of the global revenues.

Asia Pacific

Asia Pacific is estimated to reach USD 3.22 billion in 2026 and secure the position of the third-largest region in the market. The market in Asia Pacific is growing due to rising cancer incidence, a large patient population, improved healthcare access, and increased HPV vaccination and oncology research activity.

Japan Cancer Vaccines Market

The Japanese market in 2026 is estimated at around USD 0.33 billion, accounting for approximately 2.60% of the global revenues.

China Cancer Vaccines Market

China's market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 1.05 billion, representing approximately 4.59% of global sales.

India Cancer Vaccines Market

The Indian market in 2026 is estimated at around USD 0.47 billion, accounting for roughly 8.29% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The market in Latin America is estimated to reach a valuation of USD 0.44 billion in 2026. The region's growth is driven by expanding cancer screening and prevention programs, improved vaccine access, and a rising government focus on reducing the cervical cancer burden. In the Middle East & Africa, the GCC is set to reach USD 0.12 billion in 2026.

South Africa Cancer Vaccines Market

The South African market is projected to reach approximately USD 0.10 billion in 2026, accounting for roughly 0.82% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations and Significant Investments for Increased Vaccine Production to Propel Market Growth

The global market is primarily dominated by a handful of key manufacturers, including Merck & Co., Inc., GSK plc, and Dendreon Pharmaceuticals LLC. The dominance of these companies is due to their increased focus on launching clinical trials for cancer vaccine products. This, along with a growing focus on acquisitions and collaborations among the major players to strengthen their global presence, is also supporting the rising market share of these companies.

- For instance, in January 2025, GSK plc collaborated with the University of Oxford (Oxford) to focus on the potential of cancer prevention through vaccination. The GSK-Oxford Cancer Immuno-Prevention Program will conduct translational research, exploring precancer biology to generate key insights on how cancer develops in humans that could inform new approaches to cancer vaccination.

Similarly, other prominent players in the market, including Walvax Biotechnology Co., Ltd., and Synthaverse S.A., are continuously producing these vaccines and focusing on expanding their global distribution channels. Through strategic partnerships and R&D investments, they aim to establish a foothold in emerging markets. Such initiatives are projected to propel the number of emerging players and are expected to register growth by 2034.

LIST OF KEY CANCER VACCINE COMPANIES PROFILED

- Dendreon Pharmaceuticals LLC. (U.S.)

- Serum Institute of India Pvt. Ltd. (India)

- Merck & Co., Inc. (U.S.)

- GSK plc (U.K.)

- Walvax Biotechnology Co., Ltd. (China)

- Synthaverse S.A. (Poland)

- Center of Molecular Immunology (Cuba)

- Moderna, Inc. (U.S.)

- Wantai BioPharm (China)

- BioNTech SE (Germany)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Anixa Biosciences, Inc. collaborated with Cytovance Biologics to produce cGMP clinical materials for its planned Phase 2 clinical trial of its breast cancer vaccine.

- October 2025: TransCode Therapeutics, Inc acquired Polynoma LLC, a privately held biotechnology immuno-oncology company. Polynoma is developing a late-stage candidate, seviprotimut-L, a novel polyvalent shed antigen vaccine for the adjuvant treatment of stage IIB and IIC melanoma.

- September 2025: Serum Institute of India Pvt. Ltd. collaborated with Vidal Health to support national efforts to prevent and raise awareness about cervical cancer. Through the collaboration, a digital health program will be launched on Vidal Health’s platform, offering a convenient, cashless experience and making the HPV vaccine more accessible.

- September 2025: Xiamen Innovax Biotech Co., Ltd. administered the first dose of its Cecolin 9 at the Shitang Community Health Service Center, China. The development marked the official launch of the HPV 9-valent vaccine for females aged 9 to 45 against cervical cancer.

- August 2025: Beijing Wantai Biological Pharmacy Enterprise Co., Ltd. received the Biological Products Batch Release Certificate from China’s National Institutes for Food and Drug Control (NIFDC) for its HPV 9-valent vaccine, Cecolin9

REPORT COVERAGE

The report provides a detailed analysis of the global cancer vaccines market by type, technology, indication, distribution channel, and region. The report also includes market drivers, restraints, opportunities, and challenges affecting the adoption of cancer vaccines. It highlights the impact of rising cancer burden, growing preventive vaccination coverage, and expanding development of personalized neoantigen vaccines. At the same time, it evaluates factors such as limited clinical success of some therapeutic vaccines, manufacturing complexity, safety concerns, high development cost, and regulatory uncertainty.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 17.25% from 2026 to 2034 |

| Unit | Value (USD billion) |

| Segmentation | By Type, Technology, Indication, Distribution Channel, and Region |

| By Type |

|

| By Technology |

|

|

By Indication |

|

|

By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 11.62 billion in 2025 and is projected to reach USD 45.37 billion by 2034.

Registering a CAGR of 17.25%, the market will exhibit steady growth in the forecast period.

By type, the preventive segment dominated the market in 2025.

Expanding use of immunotherapy combinations for therapeutic cancer vaccine development is driving market growth.

Merck & Co., Inc., GSK plc, Serum Institute of India Pvt. Ltd., and Dendreon Pharmaceuticals LLC. are the major players in the global market.

The high demand for mass immunization and product approvals globally is expected to drive adoption of these products.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 136

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us