Carbon Accounting & Emissions Management Consulting Market Size, Share & Industry Analysis, By Service Type (Carbon Accounting, Scope 3 Assessment, Decarbonization Strategy, Climate Risk & Scenario Analysis, Carbon Disclosure & Compliance, Carbon Markets & Offsets Advisory, Emissions Reduction Implementation, & Others), By Organization Size (Large Enterprises and Small & Medium Enterprises), By End-Use Industry (Energy & Utilities, Oil & Gas, Manufacturing, Transportation & Logistics, Financial Services, Retail & Consumer Goods, & Others), and Regional Forecast, 2026-2034

Carbon Accounting & Emissions Management Consulting Market Size and Future Outlook

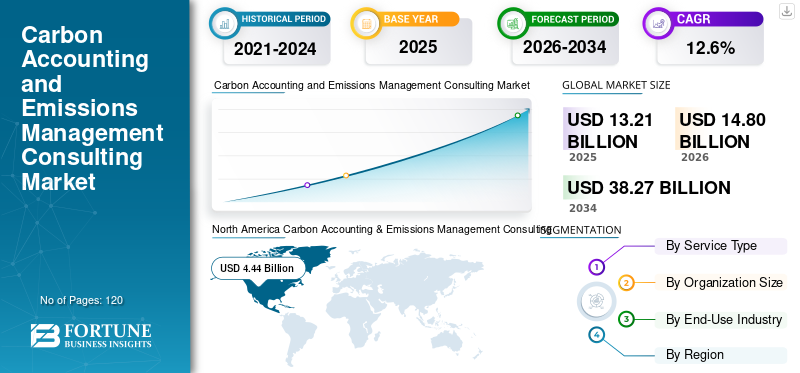

The global carbon accounting & emissions management consulting market size was valued at USD 13.21 billion in 2025. The market is projected to grow from USD 14.80 billion in 2026 to USD 38.27 billion by 2034, exhibiting a CAGR of 12.6% during the forecast period. North America dominated the carbon accounting & emissions management consulting market with a market share of 33.38% in 2025.

Carbon accounting & emissions management consulting services help organizations measure, report, and reduce Greenhouse Gas (GHG) emissions across operations and supply chains. These consulting solutions combine carbon accounting frameworks, emissions data management platforms, lifecycle assessment tools, and regulatory advisory to support accurate Scope 1, Scope 2, and Scope 3 reporting while helping organizations evaluate their carbon footprints and track emissions across complex operational networks.

The industry is witnessing strong growth in the market as companies strengthen data-driven climate strategies, supported by evolving sustainability regulations, increasing ESG disclosure requirements, and rising corporate commitments to net-zero targets and broader sustainability goals. Growing adoption of digital carbon management platforms is accelerating demand for integrated consulting services across North America, Europe, and Asia Pacific, where organizations are focusing on improving climate governance, regulatory compliance, and long-term operational sustainability.

- For instance, in February 2025, Deloitte expanded its climate and sustainability advisory services to support corporate carbon accounting and net-zero transition planning for global enterprises.

Deloitte, Accenture, PwC, ERM, and Anthesis Group are among the key players holding a significant share of the market. Their competitive positioning is supported by advanced carbon accounting methodologies, digital emissions management platforms, climate risk modeling capabilities, and the ability to deliver end-to-end decarbonization consulting solutions for enterprises, financial institutions, and government organizations pursuing long-term climate transition strategies.

Download Free sample to learn more about this report.

Carbon Accounting and Emissions Management Consulting Market Key Takeaways

- 2025 Market Size: USD 13.21 billion

- 2026 Market Size: USD 14.80 billion

- 2034 Forecast Market Size: USD 38.27 billion

- CAGR: 12.6% from 2026-2034

- North America dominated the carbon accounting & emissions management consulting market with a 33.38% share in 2025.

- Carbon data & management systems consulting is projected to grow at the highest CAGR of 15.6% during the forecast period.

- Small & Medium Enterprises (SMEs) are expected to register the fastest growth at a CAGR of 14.3% during the forecast period.

North America

North America accounted for USD 4.44 billion in revenue in 2025.

Asia Pacific

Asia Pacific generated USD 3.34 billion in revenue in 2025 and remains the fastest-growing regional market.

Europe

Europe is supported by a structured regulatory environment and strong corporate sustainability commitments.

U.S.

The market is estimated to reach USD 4.09 billion in 2026, accounting for the largest share in North America.

Japan

The market is estimated to reach USD 0.51 billion in 2026, accounting for approximately 3.5% of global sales.

Read More

CARBON ACCOUNTING & EMISSIONS MANAGEMENT CONSULTING MARKET TRENDS

Growing Adoption of Supplier Decarbonization Programs is Reshaping the Market Demand

Demand for these services is increasingly influenced by corporate requirements to track emissions and manage carbon emissions across extended supplier networks and procurement systems. Companies are expanding carbon management initiatives beyond internal operations and towards supplier engagement programs, value-chain emissions mapping, and structured decarbonization planning to improve transparency in Scope 3 reporting and better understand organizational carbon footprints. These evolving priorities are influencing market dynamics as organizations adopt data-driven emissions monitoring frameworks, supplier reporting tools, and sector-specific decarbonization roadmaps to strengthen sustainability governance. Consulting providers are responding by developing integrated advisory services focused on supplier emissions assessment, carbon reduction target setting, and supply-chain decarbonization strategies aligned with corporate sustainability goals. These capabilities support improved emissions visibility across global procurement networks while helping organizations align with international reporting frameworks and long-term climate transition objectives.

- For instance, in March 2025, PwC expanded its supply-chain decarbonization advisory services to help global manufacturers implement supplier carbon reporting frameworks.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Mandatory Climate Disclosure Frameworks to Drive Market Growth

The market is experiencing accelerated growth as governments and regulatory bodies introduce mandatory climate disclosure frameworks requiring organizations to measure and report greenhouse gas emissions with greater transparency. New regulations and reporting standards are pushing companies to establish structured carbon accounting systems, develop decarbonization roadmaps, and strengthen sustainability governance practices. As regulatory expectations expand across multiple industries, organizations are increasingly seeking specialized consulting services to support emissions inventory development, climate risk assessment, and compliance with evolving reporting frameworks. In response, consulting providers are expanding capabilities in emissions data management, regulatory advisory, and climate strategy development to help enterprises improve carbon transparency and align with international sustainability standards.

- For instance, in April 2025, Accenture expanded its sustainability consulting services to help enterprises integrate advanced carbon accounting systems and climate reporting capabilities across global operations.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Inconsistent Emissions Data Availability to Constrain Market Expansion

Unlike traditional environmental reporting processes, these services require access to detailed emissions data across multiple operational units, suppliers, and logistics networks. Variability in data availability, inconsistent reporting methodologies, and limited digital infrastructure across organizations often complicate the development of accurate greenhouse gas inventories. Many companies still rely on fragmented data sources and manual reporting systems, which can reduce the reliability and comparability of emissions calculations. Differences in organizational reporting standards, supplier transparency levels, and regional regulatory interpretations further increase complexity in carbon accounting projects. For consulting providers supporting multinational corporations, these data inconsistencies can extend project timelines, increase verification requirements, and limit the rapid deployment of standardized carbon management frameworks across global operations.

MARKET OPPORTUNITIES

Expansion of Carbon Pricing Mechanisms is Creating New Demand Opportunities for Consulting Services

An emerging opportunity in the market is being created by the expansion of carbon pricing mechanisms and emissions trading systems across multiple regions. Governments are increasingly introducing carbon taxes, emissions trading schemes, and border carbon adjustment policies that require organizations to quantify and manage their carbon liabilities more effectively. As these regulatory instruments expand, companies are seeking specialized consulting services to assess carbon exposure, develop emissions reduction strategies, and optimize participation in carbon markets. Consulting providers are therefore expanding their capabilities in carbon pricing analytics, emissions forecasting, and regulatory strategy advisory to support organizations navigating through evolving carbon policy environments.

- For instance, in March 2025, South Pole expanded its carbon market advisory services to help multinational corporations evaluate carbon pricing exposure and develop strategies for participation in voluntary and compliance carbon markets.

MARKET CHALLENGES

Lack of Standardized Carbon Reporting Methodologies Across Regions to Increase Implementation Complexity

Carbon accounting & emissions management consulting market growth face significant challenges due to fragmented regulatory requirements and varying emissions reporting standards across different countries and industries. Organizations must often comply with multiple frameworks such as the GHG Protocol, TCFD recommendations, regional sustainability disclosure regulations, and country-specific reporting guidelines, requiring customized carbon accounting methodologies and verification procedures. Differences in sector-specific emissions calculation approaches, supply chain reporting practices, and regulatory interpretations can complicate the development of unified carbon management systems. For consulting providers supporting multinational corporations, aligning emissions data across diverse regulatory environments often requires extensive data validation, framework mapping, and compliance verification processes. This lack of global standardization increases project complexity, extends implementation timelines, and raises operational costs, creating challenges for scaling carbon management advisory services across multiple regions while maintaining consistency in emissions reporting and climate governance practices.

Segmentation Analysis

By Service Type

Carbon Accounting Segment Led as It Forms the Foundational Layer for Corporate Emissions Measurement and Climate Reporting

By service type, the market is segmented into carbon accounting, scope 3 assessment, decarbonization strategy, climate risk & scenario analysis, carbon disclosure & compliance, carbon markets & offsets advisory, emissions reduction implementation, and carbon data & management systems consulting.

Carbon accounting held the largest carbon accounting & emissions management consulting market share as it represents the foundational process through which organizations quantify greenhouse gas emissions across operations and value chains. Companies increasingly prioritize accurate Scope 1 and Scope 2 emissions inventories to establish regulatory compliance, sustainability reporting frameworks, and baseline data for long-term decarbonization planning. As climate disclosure regulations and investor scrutiny continue to intensify, enterprises are investing in structured carbon accounting frameworks, emissions data validation systems, and third-party advisory services to improve transparency and credibility in sustainability reporting. These capabilities support organizations in aligning with global reporting frameworks while enabling better climate governance and performance monitoring across multiple industries.

- For instance, in March 2025, KPMG introduced enhanced emissions measurement advisory programs to assist multinational corporations in strengthening Scope 1 and Scope 2 carbon accounting processes across global operations.

Carbon data & management systems consulting is emerging as the fastest-growing segment and is projected to expand at a CAGR of 15.6% during the forecast period. As organizations increasingly adopt digital sustainability platforms and automated emissions monitoring tools, demand for consulting services supporting carbon data architecture, emissions analytics integration, and enterprise sustainability software deployment is rising rapidly. These digital capabilities enable companies to improve emissions data accuracy, streamline reporting workflows, and support real-time carbon performance monitoring across complex global operations.

To know how our report can help streamline your business, Speak to Analyst

By Organization Size

Large Enterprises Govern Due to Complex Supply Chains, Requiring Extensive Regulatory Compliance Programs

By organization size, the market is segmented into large enterprises and small & medium enterprises (SMEs).

Large enterprises held the largest share driven by their extensive operational footprints, complex supply chains, and increasing regulatory obligations related to climate disclosure and sustainability reporting. Multinational corporations across manufacturing, energy, technology, and financial services sectors are prioritizing enterprise-wide carbon accounting frameworks, emissions data management systems, and decarbonization strategy development to meet investor expectations and regulatory compliance requirements. These organizations typically require comprehensive consulting support for Scope 1, Scope 2, and Scope 3 emissions measurement, climate risk analysis, and sustainability governance integration across global operations. As a result, large enterprises continue to represent the primary demand base for advanced carbon management advisory services.

Small & Medium Enterprises (SMEs) are expected to register the highest growth rate in the market during the study period, expanding at a CAGR of 14.3%. Increasing awareness of climate reporting requirements, growing participation in global supply chains, and pressure from large corporate buyers to disclose emissions data are encouraging SMEs to adopt structured carbon management practices.

By End-Use Industry

Prioritization of Enterprise-Wide Carbon Measurement and Decarbonization Programs by Industrial Producers is Boosting the Dominance of Manufacturing Segment

Based on end-use industry, the market is segmented into energy & utilities, oil & gas, manufacturing, transportation & logistics, financial services, retail & consumer goods, technology & telecommunications, government & public sector, and others (agriculture, construction, etc.).

Manufacturing accounts for the highest share of the market, driven by extensive emissions monitoring requirements due to energy-intensive production environments such as metals, chemicals, cement, electronics, and automotive manufacturing. Industrial producers operate on complex global supply chains and high-energy processes that generate significant greenhouse gas emissions, making carbon accounting and decarbonization planning a strategic priority. Companies in this sector increasingly deploy consulting services to establish emissions inventories, develop science-based reduction targets, and implement operational decarbonization strategies across manufacturing facilities and supplier networks. As sustainability regulations expand and customers demand low-carbon products, manufacturing continues to represent the largest demand base in the market.

The energy & utilities segment is expected to register the highest growth rate, expanding at a CAGR of 13.9% from 2026 to 2034, supported by accelerating investments in energy transition programs, renewable power development, and emissions reduction initiatives across power generation and utility infrastructure. Utilities are increasingly adopting carbon accounting systems and climate strategy advisory services to manage emissions reporting obligations and align with national decarbonization targets.

Carbon Accounting & Emissions Management Consulting Market Regional Outlook

By geography, the market is studied across Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Carbon Accounting & Emissions Management Consulting Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for over USD 4.44 billion in revenue in 2025, supported by strong regulatory enforcement, large concentration of multinational corporations, and growing adoption of enterprise-wide sustainability reporting programs across the U.S., Canada, and Mexico. Regional demand is closely linked to expanding climate disclosure requirements, increasing investor scrutiny on environmental performance, and the rapid adoption of net-zero transition strategies among large corporations. Companies across manufacturing, energy, financial services, and technology sectors are increasingly investing in structured carbon accounting frameworks, emissions monitoring systems, and decarbonization advisory services to strengthen regulatory compliance and climate governance. The region also exhibits a strong presence of global consulting firms and sustainability advisory providers offering advanced climate analytics, supply-chain emissions assessment, and enterprise decarbonization strategy development. As corporate climate commitments expand and regulatory reporting frameworks continue to evolve, North America remains a major center for carbon management consulting services.

U.S. Carbon Accounting & Emissions Management Consulting Market

The U.S. is expected to dominate the regional market with an estimated revenue of about USD 4.09 billion in 2026, driven by the country’s large corporate base, expanding sustainability disclosure regulations, and strong demand for climate risk advisory services across multiple industries. Unlike many emerging markets, U.S. organizations are rapidly integrating carbon accounting systems within enterprise governance frameworks to support investor transparency, regulatory compliance, and long-term decarbonization planning. Large corporations across manufacturing, technology, energy, and financial sectors are adopting digital carbon management platforms, supply-chain emissions tracking systems, and advanced climate analytics to improve emissions transparency and operational sustainability. Continuous investments in climate strategy advisory, emissions data management infrastructure, and enterprise sustainability transformation programs are strengthening the country’s position as the leading contributor to the regional market.

Europe

The European market is supported by a structured regulatory environment and strong corporate sustainability commitments, particularly across major economies such as Germany, U.K., France, Italy, and the Netherlands. These countries continue to lead regional adoption, supported by mature sustainability ecosystems, strong ESG investment activity, and large industrial sectors implementing long-term decarbonization strategies. Demand for these services is closely tied to expanding climate disclosure regulations, emissions trading systems, and corporate net-zero transition programs across industrial and financial sectors. Companies across manufacturing, energy, transportation, and technology industries are increasingly adopting enterprise carbon accounting frameworks to improve emissions transparency and regulatory compliance. Unlike regions with fragmented climate policies, Europe benefits from coordinated sustainability regulations that encourage standardized emissions reporting and climate risk disclosure across multiple industries. Growing regulatory oversight, supply-chain decarbonization requirements, and investor-driven ESG expectations are accelerating investments in digital carbon management platforms, emissions analytics systems, and integrated climate strategy advisory services.

U.K. Carbon Accounting & Emissions Management Consulting Market

The U.K. market in 2026 is estimated at around USD 0.82 billion, representing roughly 5.5% of global sales.

Germany Carbon Accounting & Emissions Management Consulting Market

Germany’s market is projected to reach approximately USD 0.90 billion in 2026, equivalent to around 6.1% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing region in the market, generating revenue of USD 3.34 billion in 2025 globally. Regional market expansion is primarily driven by increasing aerospace manufacturing localization, expansion of commercial aircraft structural assembly capacity, and rising defense platform industrialization across major economies. China’s growth is closely linked to domestic narrow body aircraft production and aerostructure manufacturing investments, while Japan’s demand is supported by high-precision wing and composite component assembly programs integrated into global aerospace supply chains. South Korea, India, and ASEAN countries are emerging contributors as regional governments encourage aerospace capability development and Tier-1 supplier expansion.

China Carbon Accounting & Emissions Management Consulting Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 1.33 billion, representing roughly 9.0% of global sales.

Japan Carbon Accounting & Emissions Management Consulting Market

The Japan market in 2026 is estimated at around USD 0.51 billion, accounting for roughly 3.5% of the global sales.

India Carbon Accounting & Emissions Management Consulting Market

The India market in 2026 is estimated at around USD 0.60 billion, accounting for roughly 4.0% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by defense localization initiatives, aerospace industrial development programs, and expanding advanced manufacturing activity, particularly across the GCC and some North African economies. Government-backed investments in domestic aircraft assembly, military platform integration, and aerospace capability development are supporting the regional market used in structural assembly and fastening operations. The GCC benefits from high-capex, specification-driven defense and aerospace projects requiring ITAR-compliant, digitally integrated drilling and fastening platforms, while North Africa is witnessing gradual expansion of aerostructure manufacturing aligned with European aerospace supply chains. Across parts of Sub-Saharan Africa, limited but growing industrial capability is encouraging incremental adoption of semi-automated drilling and fastening solutions in defense and heavy equipment assembly.

GCC Carbon Accounting & Emissions Management Consulting Market

The GCC market is projected to reach around USD 0.36 billion in 2026, representing roughly 2.4% of the global sales.

South America

The South America market is supported by the region’s developing aerospace and industrial manufacturing footprint, particularly in Brazil and Argentina, which serve as key hubs for aircraft assembly, aerostructure production, and defense-related manufacturing. Brazil’s commercial and defense aircraft programs represent the primary driver of demand in the market, supported by structural assembly operations requiring precision hole-making and fastening automation. While overall production volumes remain lower compared to North America and Europe, export-oriented aerospace manufacturing and participation in global supply chains are encouraging investment in digitally integrated drilling and fastening platforms. Argentina and select regional facilities are gradually modernizing assembly infrastructure to improve structural repeatability, reduce manual dependency, and align with international aerospace quality standards.

Brazil Carbon Accounting & Emissions Management Consulting Market

The Brazil market is projected to reach around USD 0.38 billion in 2026, representing roughly 2.6% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Climate Advisory Capabilities, Digital Carbon Platforms, and Global Sustainability Expertise are Driving Competition Dynamics

The carbon accounting & emissions management consulting market is moderately consolidated, with competitive positioning shaped less by the range of sustainability service portfolios and more by depth of climate advisory expertise, regulatory compliance capabilities, and long-term relationships with multinational corporations. Leading players such as Deloitte, Accenture, PwC, ERM, and Anthesis Group maintain strong market positions by delivering integrated carbon accounting frameworks, enterprise decarbonization strategies, and climate risk advisory solutions tailored for complex global operations. Their competitive strength is reinforced by advanced emissions analytics platforms, supply-chain carbon assessment capabilities, and the ability to support organizations in aligning with international climate reporting frameworks and sustainability standards.

Competitive differentiation is increasingly driven by a consulting provider’s ability to integrate digital carbon management platforms, support large-scale Scope 3 emissions assessments, and deliver sector-specific decarbonization roadmaps rather than by consulting portfolio size alone. As organizations prioritize transparent emissions reporting, regulatory readiness, and long-term climate transition strategies, market leaders are strengthening investments in sustainability data analytics, AI-enabled carbon modeling tools, and enterprise climate strategy advisory services to reinforce competitive positioning and expand global client relationships.

- For instance, in April 2025, ERM introduced enhanced digital emissions analytics solutions designed to support multinational companies in managing large-scale Scope 3 emissions reporting and regulatory compliances.

LIST OF KEY CARBON ACCOUNTING & EMISSIONS MANAGEMENT CONSULTING COMPANIES PROFILED IN REPORT

- Accenture plc (Ireland)

- Deloitte Global (U.K.)

- PwC (PricewaterhouseCoopers) LLP (U.K.)

- Ernst & Young (EY) Global Limited (U.K.)

- KPMG International Limited (Netherlands)

- The ERM International Group Limited (U.K.)

- The Anthesis Group (U.K.)

- SLR Consulting Limited (U.K.)

- Boston Consulting Group, Inc. (BCG) (U.S.)

- McKinsey & Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: BCG expanded its climate and sustainability consulting practice by introducing advanced decarbonization strategy frameworks designed to support multinational corporations in aligning long-term emissions reduction plans with science-based targets and regulatory disclosure requirements.

- June 2025: Accenture plc expanded its sustainability services by integrating AI-enabled carbon intelligence tools within enterprise consulting programs to support organizations in improving emissions data visibility and accelerating net-zero transition strategies.

- March 2025: IBM Sustainability launched enhanced consulting services integrating AI-driven carbon data analytics with enterprise sustainability platforms to help organizations improve emissions monitoring and automate sustainability reporting processes.

- January 2025: ERM International Group launched enhanced decarbonization strategy advisory programs focused on helping global manufacturers develop operational emissions reduction plans and implement enterprise carbon management frameworks.

- January 2025: Capgemini strengthened its sustainability advisory portfolio by introducing an integrated carbon accounting and digital emissions management services aimed at supporting large enterprises implementing enterprise-wide climate governance frameworks.

REPORT COVERAGE

The global carbon accounting & emissions management consulting market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service Type, Organization Size, End-Use Industry, and Region |

| By Service Type |

|

| By Organization Size |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 13.21 billion in 2025 and is projected to reach USD 38.27 billion by 2034.

In 2025, the North Americas market value stood at USD 4.44 billion.

The market is expected to exhibit a CAGR of 12.6% during the forecast period.

By end-use industry, the manufacturing segment leads the market.

Increasing climate disclosure regulations, rising corporate net-zero commitments, and growing demand for enterprise carbon accounting and decarbonization strategies are key factors driving the market.

Accenture plc, Deloitte Global, PwC (PricewaterhouseCoopers) LLP, and Ernst & Young (EY) Global Limited are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us