Carbon-Neutral Materials Market Size, Share & Industry Analysis, By Material Type (Carbon-Neutral Cement and Concrete, Carbon-Neutral Metals, Carbon-Neutral Polymers, Carbon-Neutral Glass and Ceramics, Carbon-Neutral Composites, and Others), By End-Use Industry (Building and Construction, Automotive and Transportation, Packaging, Electrical and Electronics, Consumer Goods, Industrial Manufacturing, and Others), and Regional Forecast, 2026-2034

Carbon-Neutral Materials Market Size and Future Outlook

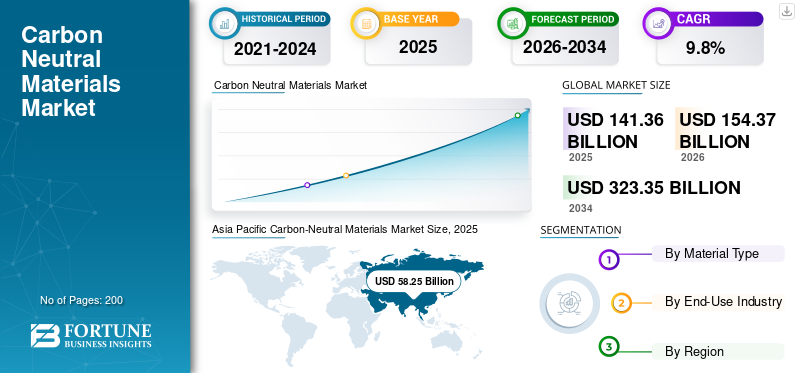

The carbon-neutral materials market size was valued at USD 141.36 billion in 2025. The market is projected to grow from USD 154.37 billion in 2026 to USD 323.35 billion by 2034, exhibiting a CAGR of 9.8% during the forecast period. Asia Pacific dominated the carbon neutral materials market with a market share of 41.21% in 2025. This growth trajectory reflects the increasing focus on reducing greenhouse gas emissions and minimizing the overall carbon footprint across industrial value chains.

Carbon-neutral materials refer to material classes or commercially supplied material grades whose lifecycle-related carbon dioxide emissions are significantly reduced and balanced. This is done through advanced reduction and renewable energy integration, low-emission production pathways, recycled or bio-based feedstock, carbon capture, circular processing, and verified decarbonization measures. Commercial demand spans carbon-neutral polymers, metals, cement and concrete, glass and ceramics, composites, and selected specialty materials supplied into construction, transportation, packaging, electronics, consumer products, and industrial manufacturing sectors.

The market growth is driven by companies, project developers, and public buyers placing greater emphasis on embodied carbon reduction, circularity, and low-emissions procurement across industrial value chains, including manufacturing, shipping, logistics, and energy utilities. Growth is further supported by evolving definitions for near-zero and low-emissions industrial materials, the expansion of buy-clean style frameworks, and the increasing availability of lower-carbon product grades from leading materials producers.

Furthermore, the market comprises several major players, including Holcim, Heidelberg Materials AG, Saint-Gobain, ArcelorMittal, and Nucor Corporation, along with regional producers of low-carbon cement, glass, steel, aluminum, polymers, and engineered materials. Renewable-energy access, recycled-feedstock availability, process innovation, certifications, industrial integration, and downstream customer relationships support these companies’ competitive positioning in the global market.

Download Free sample to learn more about this report.

Carbon Neutral Materials Market Takeaways

- 2025 Market Size: USD 141.36 billion

- 2026 Market Size: USD 154.37 billion

- 2034 Forecast Market Size: USD 323.35 billion

- CAGR: 9.8% from 2026–2034

- Asia Pacific dominated the carbon-neutral materials market with a 41.21% share in 2025.

- The carbon-neutral cement and concrete segment led the market with a 24.2% share in 2025.

- The building and construction segment accounted for the largest end-use share at 27.7% in 2025.

North America

North America remained a significant regional market, reaching USD 26.95 billion in 2025.

Europe

Europe reached a valuation of USD 34.06 billion in 2025 and is projected to grow at a 9.5% CAGR during the forecast period.

Asia Pacific

Asia Pacific maintained its leadership, with the market growing from USD 53.35 billion in 2024 to USD 58.25 billion in 2025.

U.S.

The market is estimated to reach USD 24.27 billion by 2026, supported by increasing investments in sustainable construction materials.

Japan

The market is projected to reach approximately USD 6.32 billion by 2026, accounting for around 4.1% of global sales.

Read More

CARBON-NEUTRAL MATERIALS MARKET TRENDS

Embodied Carbon Reduction in Industrial Materials is a Significant Market Trend

Product demand is increasingly shaped by crop-intensity requirements and nutrient-use-efficiency priorities. Additionally, the need to lower embodied carbon in buildings, vehicles, packaging systems, and industrial products without compromising performance, processability, or supply reliability are few major market trends. Large buyers are giving weight to environmental product declarations, recycled-content claims, renewable-power-backed production, and low-emissions material labels when selecting suppliers. This is strengthening the commercial role of lower-carbon cement and concrete, recycled and renewable-power-based metals, bio-attributed and circular polymers, and advanced materials with reduced lifecycle intensity.

Alongside policy support, portfolio strategies are increasingly centered on product differentiation, decarbonized production pathways, and application-specific premium capture. Manufacturers are investing in clinker reduction, scrap- and renewable-energy-backed metals, circular polymers, and traceability systems that can translate sustainability claims into procurement-ready offers. As embodied-carbon reporting becomes more formal across construction and manufacturing value chains, suppliers are highlighting verified emissions data, certifications, and commercialization pathways to strengthen customer retention and pricing power.

- For instance, lower-emission cement and steel definitions, buy-clean procurement frameworks, and expanding bioplastics and circular-material offerings are strengthening commercial demand signals for decarbonized materials.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Embodied Carbon Procurement and Industrial Decarbonization Are Driving Market Growth

Buildings, infrastructure, transport equipment, and consumer products are under increasing pressure to reduce lifecycle emissions, which is making low-emissions material sourcing more important across procurement decisions. Carbon-neutral cement and concrete, recycled and renewable-power-backed metals, low-carbon glass, and circular polymers are benefiting as they can reduce emissions at the material-selection stage while fitting into existing applications and manufacturing systems. This creates a large and relatively durable demand base across regions where policy frameworks, corporate climate targets, and green-building standards are influencing purchasing behavior.

Beyond direct procurement policies, producers are expanding low-carbon portfolios, industrial partnerships, and traceability systems to improve market access and premium realization. Product demand is reinforced by growing use of environmental product declarations, low-embodied-carbon specifications, and decarbonization targets in construction, automotive, packaging, and industrial manufacturing. As buyers seek scalable ways to cut scope 3 emissions, carbon-neutral materials are becoming a practical commercialization route within broader net-zero strategies. These factors boost the overall carbon-neutral materials market growth.

- For instance, lower-embodied-carbon concrete, steel, aluminum, and polymers are increasingly prioritized in public procurement programs and corporate decarbonization roadmaps as they reduce emissions without requiring a complete redesign of end-use systems.

MARKET RESTRAINTS

Premium Pricing, Certification Complexity, and Limited Scaled Supply Restricts Market Expansion

While carbon-neutral materials are gaining commercial relevance, the market remains sensitive to price premiums and limited supply at an industrial scale. Production costs can remain high where low-carbon pathways depend on renewable electricity, green hydrogen, carbon capture, advanced recycling, or specialty feedstocks, reducing pricing flexibility as compared to conventional materials. In addition, fragmented standards and differing disclosure methodologies can complicate customer comparisons and slow procurement decisions.

Supply-side constraints can also restrict growth in some applications. Many producers are still in the early stages of scaling low-carbon cementitious systems, renewable-power-based metals, circular polymers, and traceable decarbonized materials. These factors can lengthen qualification cycles, increase supply risk, and limit the pace at which demand moves from pilot projects to recurring high-volume contracts.

MARKET OPPORTUNITIES

Demand for Low-Embodied-Carbon Construction Inputs and Circular Materials is Creating Lucrative Growth Opportunities

Market opportunities are emerging from construction decarbonization, circular-economy targets, and premium product positioning in metals, polymers, and specialty materials. Building and infrastructure programs can support larger-scale commercialization as construction remains the earliest and most visible demand center for lower-carbon cement, concrete, steel, glass, and insulation materials. At the same time, packaging, consumer products, and transportation applications are supporting higher-value adoption of bio-attributed polymers, recycled-content materials, and advanced lightweight composites.

Additional suppliers combining process innovation with traceability, regulatory alignment, and application support is also a beneficial market opportunity. Companies that can offer verifiable carbon reductions, reliable delivery, and product performance comparable to conventional materials are better positioned to capture premium demand. These capabilities can improve conversion rates, customer stickiness, and geographic expansion, especially in regions where public procurement and corporate climate commitments are becoming more formalized.

MARKET CHALLENGES

Definition Uncertainty, Infrastructure Gaps, and Qualification Requirements Can Hamper Market Growth

Producers and downstream buyers must navigate evolving definitions for carbon-neutral, near-zero, and low-emissions materials while also responding to changing reporting rules, certification requirements, and customer-specific procurement criteria. This increases uncertainty around contract structures, acceptable premium levels, and comparability across suppliers, particularly in markets where standards are still developing.

In addition, many low-carbon production routes depend on infrastructure that remains unevenly available, such as renewable power, recycled-feedstock collection systems, carbon-capture networks, or hydrogen supply. End users also require technical validation, supply assurance, and requalification before shifting large volumes away from conventional materials. These factors can slow adoption even when long term demand fundamentals remain favorable.

Segmentation Analysis

By Material Type

Carbon-Neutral Cement and Concrete Segment Dominates Due to Growing Construction Activities

Based on material type, the market is segmented into carbon-neutral polymers, carbon-neutral metals, carbon-neutral cement and concrete, carbon-neutral glass and ceramics, carbon-neutral composites, and others.

The carbon-neutral cement and concrete segment accounted for the largest carbon-neutral materials market share in 2025. The segment’s growth is driven by the growing scale of global construction activity, the central role of concrete in embodied-carbon reduction strategies, and increasing commercialization of lower-clinker, supplementary-cementitious, carbon-mineralized, and other lower-emission concrete systems. Furthermore, the segment held a 24.2% share in 2025.

The carbon-neutral polymers segment is expected to grow significantly, driven by rising adoption of circular polymers, bio-attributed resins, bio-based plastics, and lower-carbon specialty materials in packaging, consumer goods, and transport applications. The segment is projected to grow at a 9.5% CAGR during the study period.

By End-Use Industry

To know how our report can help streamline your business, Speak to Analyst

Building and Construction Segment Dominates Market Due to Embodied-Carbon Targets

By end-use industry, the market is categorized into building and construction, automotive and transportation, packaging, electrical and electronics, consumer goods, industrial manufacturing, and others.

The building and construction segment accounted for the largest share in 2025. The segment’s growth is driven by embodied-carbon targets in buildings and infrastructure, broader use of lower-emission cement, steel, glass, insulation, and composites, and the growing role of environmental product declarations in material selection. Furthermore, the segment held a 27.7% share in 2025.

The automotive and transportation segment is also expected to grow favorably over the projected period. This is driven by the use of lower-carbon metals, lightweight composites, and decarbonized polymers in electric vehicles, mobility platforms, and transport equipment, where supply-chain emissions performance is becoming more commercially relevant. The segment is expected to grow at a CAGR of 9.8% over the forecast period.

Carbon-Neutral Materials Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Carbon-Neutral Materials Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2024, valued at USD 53.35 billion, and also held leading share in 2025, valued at USD 58.25 billion. The region benefits from its large cement, steel, glass, and industrial manufacturing base, central role of China and India in materials production and consumption, and growing DE carbonization initiatives across construction, metals, and polymers. China remains the largest market, while India, Japan, South Korea, and the broader Asia Pacific region continue to support demand, driven by industrial scale, infrastructure activity, export manufacturing, and increasing interest in lower-embodied-carbon materials.

China Carbon-Neutral Materials Market

In 2026, the China market is estimated to reach USD 35.34 billion. This growth is supported by its large cement and steel base, expanding circular-materials activity, strengthening low-carbon industrial investment, and the gradual commercialization of lower-emission building materials, metals, and polymers across major supply chains.

To know how our report can help streamline your business, Speak to Analyst

India Carbon-Neutral Materials Market

The India market in 2026 is estimated at around USD 10.66 billion, representing approximately 7.5% of global market revenue.

Japan Carbon-Neutral Materials Market

Japan market is projected to reach approximately USD 6.32 billion in 2026, accounting for about 4.1% of global sales.

North America

North America is also a significant contributor to the market and reached USD 26.95 billion in 2025. The market’s growth is driven by buy-clean procurement frameworks, corporate decarbonization commitments, rising demand for lower-embodied-carbon construction materials, and growing commercialization of decarbonized metals, circular polymers, and specialty materials. Application intensity remains strong in the U.S., supported by public procurement initiatives, advanced industrial capacity, and better availability of product disclosures and certification pathways.

U.S. Carbon-Neutral Materials Market

In 2026, the U.S. market is estimated to reach USD 24.27 billion. The U.S. dominates regional consumption due to its large construction and manufacturing base, early adoption of low-embodied-carbon procurement, expanding lower-carbon cement, steel, and glass offerings, as well as continued development of circular and bio-attributed materials.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to grow at a 9.5% rate and reached a valuation of USD 34.06 billion in 2025. The market’s growth is supported by strong regulatory pressure to decarbonize industry, active commercialization of low-carbon metals and building materials, mature sustainability reporting practices, and wider acceptance of recycled and traceable lower-emission material grades. The region benefits from policy support, technical know-how, and greater willingness among industrial buyers to pay for verified emissions reductions.

U.K. Carbon-Neutral Materials Market

The U.K. market in 2026 is estimated at around USD 3.96 billion, representing approximately 2.8% of global market revenue.

Germany Carbon-Neutral Materials Market

Germany’s market is projected to reach approximately USD 9.14 billion in 2026, accounting for about 6.5% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2025 reached a valuation of USD 9.52 billion. The demand is concentrated in construction materials, packaging, and industrial products, with Brazil and Mexico representing the most important country markets. Infrastructure activity, packaging demand, and growing interest in lower-carbon exports and industrial supply chains continue to support regional adoption of carbon-neutral materials.

Brazil Carbon-Neutral Materials Market

Brazil’s market is predicted to reach approximately USD 5.67 billion in 2026, equivalent to around 4.0% of global sales.

The Middle East & Africa

The Middle East & Africa region is gradually expanding, supported by GCC-led low-carbon industrial investments, the rise of renewable energy sources metals and building materials, and growing interest in lower-embodied-carbon inputs for infrastructure and export-oriented value chains.

GCC Carbon-Neutral Materials Market

GCC is expected to reach USD 7.61 billion by 2026, accounting for approximately 5.4% of global revenues. GCC demand is supported by renewable-energy-backed metals, large-scale infrastructure programs, low-carbon industrial investments, and the strategic role of the region in decarbonized materials export potential.

COMPETITIVE LANDSCAPE

Key Industry Players

Expansion of Production Footprints and Specialty Grades Helps Key Players in Maintaining Their Market Positions

The market includes a mix of cement and concrete producers, metals companies, glass manufacturers, polymer suppliers, building-material specialists, and circular-material innovators that supply lower-carbon and carbon-neutral materials into construction, transportation, packaging, industrial, and consumer applications. Competition is shaped by access to renewable energy, recycled or bio-based feedstock, process technology, certification strength, commercial scale, and the ability to provide verifiable product-level emissions data. Leading companies differentiate through product innovation, decarbonized manufacturing routes, integration across value chains, and strong relationships with industrial and institutional buyers. Some key market players include Holcim, Heidelberg Materials AG, Saint-Gobain, ArcelorMittal, and Nucor Corporation.

LIST OF KEY CARBON-NEUTRAL MATERIALS COMPANIES PROFILED

- Holcim (Switzerland)

- Heidelberg Materials AG (Germany)

- Saint-Gobain (France)

- ArcelorMittal (Luxembourg)

- Nucor Corporation (U.S.)

- Novelis Inc. (U.S.)

- Milliken (U.S.)

- Covestro AG (Germany)

- BASF SE (Germany)

- Kingspan Group plc (Ireland)

- Interface, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: BASF announced the first commercial production of biomass balance polyether polyols in North America at Geismar, Louisiana, signaling expansion of lower-carbon polyurethane raw materials into sleep products, automotive, and CASE applications.

- June 2025: Heidelberg Materials officially opened Brevik CCS in Norway, the world’s first industrial-scale carbon capture and storage facility in the cement industry, signaling a major commercial milestone for carbon-captured near-zero cement.

- September 2024: Novelis introduced its 3x30 sustainability initiative, setting new targets to increase recycled content, reduce carbon emissions, and strengthen circular aluminum leadership, signaling a more aggressive decarbonization roadmap for low-carbon metals.

- June 2024: Heidelberg Materials and Linde held the groundbreaking for the world’s first large-scale carbon capture and utilization facility in a cement plant at Lengfurt, Germany, signaling deeper integration of CCU into low-carbon cement production.

- September 2023: BASF launched the industry’s first biomass balance offerings for plastic additives, including Irganox grades certified under ISCC PLUS, signaling broader commercialization of mass-balance-based sustainable plastics solutions.

- May 2022: Novelis announced a USD 2.5 billion low-carbon aluminum recycling and rolling plant in Bay Minette, Alabama, signaling major capacity expansion in recycled, lower-emission aluminum for packaging and automotive applications.

- January 2021: Holcim launched its ECOPlanet global green cement range, with distribution across multiple countries and doubled market presence by the end of 2022, signaling an early large-scale push toward low-carbon cement adoption.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.8% from 2026 to 2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Material Type, End-Use Industry, and Region |

| By Material Type |

|

| By End-Use Industry |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 141.36 billion in 2025 and is projected to reach USD 323.35 billion by 2034.

Recording a CAGR of 9.8%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The building and construction end-use industry segment is leading the market.

Asia Pacific held the highest market share.

Holcim, Heidelberg Materials AG, Saint-Gobain, ArcelorMittal, and Nucor Corporation are some of the prominent players in the market.

The key factor driving market growth is rising demand for decarbonization targets and embodied-carbon reduction commitments.

The major factors expected to favor product adoption include stronger low-carbon procurement policies, growing use of recycled and bio-based feedstock, and expanding availability of premium low-emission material grades.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us