Cargo Vessel Market Size, Share & Industry Analysis, By Ship Type (Tanker, Bulk Carriers, Container Ships, General Cargo Vessel, Roll on/Roll off Ships, and Others), By Fuel Type (Diesel and Gasoline, Hybrid, LNG, and Others), By Gross Tonnage (Below 50000 GT, 50000 - 120000 GT, and Above 120000 GT), By Deadweight (Below 75000 DWT, 75000 - 200000 DWT, and Above 200000 DWT), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

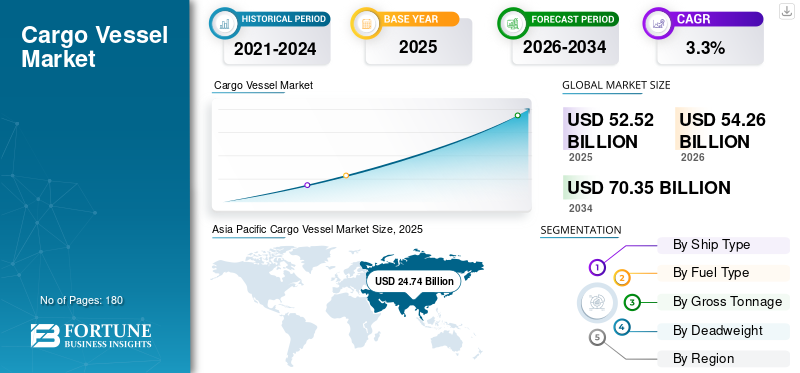

The global cargo vessel market size was estimated at USD 52.52 billion in 2025 and is projected to reach USD 54.26 billion in 2026 to USD 70.35 billion by 2034, growing at a CAGR of 3.30% from 2026 to 2034. Asia Pacific dominated the cargo vessel market with a market share of 47.10% in 2025.

Cargo vessels are carried out from one port to another to transport goods and materials. Cargo vessels come in several different sizes based on the cargo quantity needed and the size of the port where they are picked up. Cargo vessels are divided in size depending on transporting cargo, such as capsize, panamax, handymax, and handysize. Capesize bulk carrier vessels are the largest type of cargo vessel. The primary responsibility and concern for safely transporting crew, passengers, and cargo lies with all ships designed and built.

Cargo transport is the cost-effective mode of transport, and cargo transport through seaways is preferred by industry types, such as automotive, oil & gas, food & beverages, and others. Rising maritime trade activities propels the market, globally.

Download Free sample to learn more about this report.

Global Cargo Vessel Market Overview

Market Size & Forecast

- 2025 Market Size: USD 52.52 billion

- 2026 Market Size: USD 54.26 billion

- 2034 Forecast Market Size: USD 70.35 billion

- CAGR: 3.3% during 2026–2034

Market Share

- Asia Pacific dominated the cargo vessel market with a 47.10% share in 2025, supported by China, Japan, and South Korea’s shipbuilding strength and high maritime trade volumes.

- Tanker segment held the largest ship type share in 2022, driven by demand for oil and chemical transport.

- Diesel & gasoline fuel type remains dominant, while LNG-powered ships are emerging fastest due to emission-reduction initiatives.

Key Country Highlights

- China: World’s largest shipbuilding hub (41% global share), major investments in LNG-fueled bulk carriers and container vessels.

- Japan: Strong presence in shipbuilding innovation, focusing on hybrid and LNG-powered vessels (e.g., MOL Group’s decarbonization targets for 2050).

- South Korea: Home to Hyundai Heavy Industries, Samsung Heavy Industries, and KSOE—leading in bulk carrier and tanker production.

- Europe: Increasing investments in advanced cargo ships, with Damen Shipyards and Mitsubishi Heavy Industries adopting air lubrication systems for fuel efficiency.

- United States: Demand for general cargo and container vessels driven by modernization of maritime transport and NASSCO’s fleet upgrades.

Cargo Vessel Market Latest Trends

Modern Air Lubrication Systems Used in Shipbuilding to Boost Global Cargo Vessel Market Growth

The International Maritime Organization recognizes air lubrication technologies as an innovative energy efficiency technology for reducing carbon emissions. The method is used for reducing resistance between the hull and seawater by using air bubbles is the Air Lubrication System. Distributing the air bubbles on the surface of the hull causes a decrease in resistance to be exerted upon the ship's hull and thus produces energy savings.

For instance, in 2023, Alfa Laval completed its acquisition of Marine Performance Systems B.V. This maritime technology company has developed the first fluidic air lubrication system on the market-based in Rotterdam, the Netherlands.

Similarly, in October 2022, to substantially reduce fuel intake and CO2 emissions, Carnival Corporation strategies to install air lubrication systems in at least 20% of ships carrying more than half of its cruise brands by 2027. The technology is available from DK Group, Mitsubishi Heavy Industries Limited, Wartsila Oyj Abp, and others. Such developments catalyze the growth of the market by enabling cost-effective solutions to reduce carbon emissions.

- Asia Pacific witnessed cargo vessel market growth from USD 25.85 Billion in 2021 to USD 22.44 Billion in 2022.

Download Free sample to learn more about this report.

DRIVING FACTORS

Increasing Adoption of Green Fuels over Convectional Fuels to Augment Market Growth

The most widely used energy sources globally are gas, oil, and other fuels. These sources are responsible for 80% of the total power consumption. Fossil fuel's use in the maritime sector has several well-known disadvantages and it’s the main reason for greenhouse gas emissions and environmental damage. Studies have identified shipping as a significant source of anthropogenic SOx and NOx emissions, showing they account for 13% of global SOx and 15% of global NOx emissions. Considering the environmental implications, it is worth considering alternative energy sources, such as liquefied petroleum gas (LPG), LNG, methanol, hydrogen, and others, which could replace fossil fuels driving market growth.

For instance, In MOL Group's environmental vision, 2.2.2, the objective of zero greenhouse gas emissions is set for 2050. MOL Group has already ordered built LNG-fueled car carriers, bulk carriers, tankers, ferries, and a tugboat, and this new building bulk carrier will be its 17th LNG-fueled ocean-going vessel. Hence, such developments propel the shipbuilding market, especially across the cargo sector.

Increasing Maritime Trade, Government Support, and Strategy Collaborations to Drive Market Growth

The international shipping industry accounts for around 80% of world trade. The growth of maritime trade continues to provide benefits for global consumers through competition in freight costs. The main factors for further growth of this sector are the increasing effectiveness of shipping as a mode of transport and greater entrepreneurship liberalization. For instance, according to the reports, traffic on the Northern Sea Route is expected to rise to 80 million tons of shipments annually by 2025 across Arctic shipping. This rapid development has raised economic growth, environmental, political, and social challenges that several governments are addressing.

For instance, in 2021, with the completion of 13.0 million CGT of seagoing vessels, China remained the world's largest shipbuilding industry, accounting for 41.1% of the world's total. Further, China would hold an 84.6% share of the world's economies.

Further, free trade and growing demand for consumer goods are being underpinned by increasing industrialization and the liberalization of national economies. The increasing efficiency and speed of shipping have also been made possible by advances in technology.

RESTRAINING FACTORS

The Cyclic Nature of the Market Raises Concern about the Annual Shipbuilding Capacity, Order Backlog and Profitability of Shipbuilders

The cyclic nature of this market puts excess capacity pressure on shipbuilders during the peak, affecting manufacturers' operational activities and profitability. Due to this cyclic nature and inflation in raw materials, especially steel, most manufacturers have suffered losses over the past few years. Along with the minor players, major shipbuilders, such as Korea Shipbuilding & Offshore Engineering Co. (KSOE), Samsung Heavy Industries, and Daewoo Shipbuilding & Marine Engineering Co. are facing losses over the past few years.

For instance, despite many orders, the cumulative loss of Samsung Heavy Industries is estimated to be more than USD 4.5 billion since 2015. There are many more such companies in the market. Hence, government support regarding subsidy, tax, loans, and credit is crucial for reviving the vessel industry in specific countries/regions.

Segmentation Analysis

By Ship Type Analysis

Tanker Segment Held Largest Cargo Vessel Market Share Due to the Increasing Demand for Transporting Oil & Chemicals

Based on the ship type, the market is segmented into tanker, bulk carriers, container ships, general cargo vessel, roll on/roll off ships, and others. In other segments, we have considered the reefer ship, intermodal container, feeder ship, multi-purpose vessels, and others.

The tanker segment accounted for the largest market share in 2022. The growth is due to its increasing applications for carrying loads in large amounts, and it can carry up to 24,000 GT. The increasing demand for container ships globally fuels segmental growth during the forecast period.

For instance, in September 2022, the Greek shipowning company Imperial Petro announced a deal to acquire two vessels to be delivered in January 2024. The two vessels have an overall capacity of about 163,716 deadweight tonnages. The total value of the agreement is around USD 71 million.

The bulk carriers segment is the fastest-growing segment during the forecast period. The increasing demand for bulk carriers for transporting large amounts of goods, such as cereals, coal, grains, ore, cement, and others, is driving segment growth. Further, bulk carriers have a large carrying capacity of up to 300,000 tonnes, and increasing technological aspects in bulk carriers are increasing demand.

For instance, in June 2023, Kansai Electric Power Co (KEPCO) signed a contract with Japanese shipping giant Mitsui O.S.K. Lines (MOL) to manufacture a dual-filled bulk carrier that is capable of burning either conventional marine fuel oil or liquid natural gas LNG. It's going to be built at Oshima Shipbuilding Co.

By Fuel Type Analysis

Diesel and gasoline Segment Dominated due to Growing Decarboniation Efforts by Key Players

Based on fuel type, the segment is classified into diesel and gasoline, hybrid, LNG, and others.

The diesel and gasoline segment accounted for the largest market share in 2022. The increasing efforts toward decarbonizing the environmental situation by various key players using advanced fuels and gases for marine propulsion is significantly growing the segmental growth. For instance, in January 2023, MPC Container Ships and INERATEC signed a contract for supplying synthetic maritime diesel oil (MOD) produced from biogenic carbon dioxide and renewable hydrogen.

The LNG segment is estimated to be the fastest-growing segment during the forecast period of 2023-2030. The increasing demand for LNG fuel over conventional to reduce emissions, helping fleets meet new international environmental regulations requiring cleaner marine fuel. For instance, in February 2023, Hapag-Lloyd signed a contract with Rotterdam to build 12 new 23,500 TEU container ships as LNG powered.

By Gross Tonnage Analysis

50000 GT Segment Dominated the Segment Owing to the Large Fleet

Based on gross tonnage, the segment is classified into below 50000 GT, 50000 – 120000 GT, and above 120000 GT. The below 50000 segment accounted for the largest market share in 2022 owing to higher demand of maritime transport across industries, such as automotive, chemical, and others. For instance, in March 2023, Chengxi Shipyard built a 50000 GT tanker at a contract value of more than USD 54 million. Such developments catalyze the growth of the segment.

The 50000 – 120000 GT segment is estimated to be the fastest-growing segment during the forecast period. The high demand of 50000 to 120000 GT segment ships is for transporting goods across several industries. For instance, in January 2023, Chengxi Shipbuilding, a Chinese company, started building a Cargo Vessel with a contract period of 555 days. Under the contract, the company will build 70000 GT at a contract value of around USD 38.75 million.

By Deadweight Analysis

75000 – 200000 DWT Segment is Dominating due to Significantly Increasing Demand Across Several Industries

To know how our report can help streamline your business, Speak to Analyst

Based on deadweight, the market is segmented into below 75000 DWT, 75000 – 200000 DWT, and above 200000 DWT.

The 75000 – 200000 DWT segment is the fastest-growing segment from 2023-2030 and held the largest market share in 2022. Medium and large-sized container ships, oil tankers, bulk carriers, and others fall under this segment. The growing demand for these ships globally is fueling segmental growth. For instance, in January 2023, the delivery of the tanker was made by Samsung Heavy Industry, Korea. The time taken to build the tanker was 685 days. Under the contract, the company builds 168,000 DWT at a contract value of around USD 119.6 million.

Below 75,000 DWT segment is estimated to be the second fastest-growing segment during the forecast period. The below 75,000 DWT ships are significantly in demand for the transport of cargo. For instance, in July 2022, Seaway 7 took delivery of a new semisubmersible heavy transport ship. The newly built ship, MV Xin Qun 3, entered into a bareboat contract with United Faith. The ship's name is Seaway Swan, and it is a 50,000 DWT LRV with an open stern and big deck, free from obstructions.

- The above 200000 segment is expected to hold a 16.09% share in 2022.

Regional Analysis

The market is studied across regions, including North America, Europe, Asia-Pacific, and Rest of the World.

Asia Pacific Cargo Vessel Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia-Pacific dominated the market with a valuation of USD 24.74 billion in 2025 and USD 25.55 billion in 2026. It is estimated to be the fastest-growing region during the forecast period due to China, Japan, and South Korea's increased marine fleet. In addition, China, Japan, and the Republic of Korea accounted for 94% of the shipbuilding market.

Europe

In Europe, rising investments from private firms to build marine ships are projected to boost the market. Europe is expected to be the second fastest-growing region during the forecast period. The presence of key players and the second-largest fleet in the region has propelled the Europe cargo ship market growth.

North America

North America is expected to grow significantly during the forecast period. The increased federal funding for procuring marine ships by the U.S. government and growing demand for next-generation and advanced technological ships for maritime transportation are expected to drive the market's growth.

Latin America's market is significantly increasing due to a wide distribution of goods through supply chains, including those considered essential, such as food and medical supplies. Thus, the market is expected to have significant growth in the region.

Middle East & Africa

Middle East & Africa has projected a steady growth owing to the increasing transportation of goods globally.

KEY INDUSTRY PLAYERS

Key Companies to Focus on Business Expansion Through Mergers & Acquisitions

The market is relatively consolidated with the presence of several major players, especially across China and South Korea. Original equipment manufacturers (OEMs) introduced advanced technologies, such as 3D printing, integrated electric propulsion, and robotic systems to design and develop marine ships.

Hyundai Heavy Industries Co. Ltd., General Dynamics Corporation, Thales Group, Mitsubishi Heavy Industries Co. Ltd, and BAE Systems were some of the major players in 2022. Merger & Acquisition is also a prominent strategy of shipbuilders globally. For instance, Hyundai Heavy Industries Co. Ltd. completed the acquisition of Daewoo Shipbuilding & Marine Engineering Co. (DSME) in the first quarter of 2021. Similarly, in 2019, China State Shipbuilding Corporation (CSSC) completed a merger with China Shipbuilding Industry Company (CSIC) to form a new shipbuilding company.

LIST OF KEY COMPANIES PROFILED:

- Hyundai Heavy Industries Co. Ltd (HHI) (South Korea)

- Namura Shipbuilding Co Ltd (Japan)

- Damen Shipyards Group (Netherlands)

- Korea Shipbuilding & Offshore Engineering (South Korea)

- Samsung Heavy Industries (South Korea)

- Daewoo Shipbuilding & Marine Engineering (South Korea)

- General Dynamic NASSCO (U.S.)

- Mitsubishi Heavy Industries (Japan)

- Mazagon Dock Shipbuilders Limited (India)

- China State Shipbuilding Corporation (China)

KEY INDUSTRY DEVELOPMENTS:

- June 2023 – A major contract with Acta Marine for the construction of two further CSOVs, Construction Service Vessels, has recently been concluded between Tersan, one of the main shipyards in the shipping sector. This new contract brings Tersan Shipyards' order book up to four sister projects of Acta Marine, following the two CSOVs currently under construction.

- June 2023 - Udupi Cochin Shipyard Limited (UCSL), the Indian government-run shipbuilder, has bagged an international order to design and construct six new-generation 3800 DWT cargo vessels for a Norwegian firm, Wilson Shipowning AS. A contract of USD 72 million has been concluded with the possibility of buying eight more ships. The first vessel is to be delivered in December 2024, and the rest are due for completion by March 2026.

- April 2023 – Chinese shipyard China Merchants Heavy Industry-Jiangsu awarded a first contract to French LNG containment specialist GTT to design four new LNGCs (Liquified Natural Gas Carriers) on behalf of European ship-owners.

- March 2023 – South Korean shipyard Samsung Heavy Industries (SHI) awarded a contract to French LNG containment specialist GTT to design the new FLNG (Floating Liquified Natural Gas) on behalf of an Asian company.

- December 2022 – GAIL Ltd, a state-owned company in India, has signed a contract with Mitsui O. S. K. Lines Ltd to buy an LNG Carrier. The carrier will be constructed in South Korea,s Daewoo Shipbuilding & Marine Engineerings Co Ltd.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The market research report provides a detailed analysis of the market. It focuses on key aspects such as leading companies, different platforms, systems, and applications of Marine Vessel. Besides this, the report offers insights into the global cargo vessel market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the developed market in recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

CAGR |

Growth Rate of 3.3% (2026-2034) |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Ship Type

|

|

By Fuel Type

|

|

|

By Gross Tonnage

|

|

|

By Deadweight

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 54.26 billion in 2026 and is projected to reach USD 70.35 billion by 2034.

Registering a CAGR of 3.3%, the market will exhibit steady growth during the forecast period (2026-2034).

The bulk carrier in the ship type segment is expected to be the fastest-growing segment of the market during the forecast period due to growing procurement contracts of warships from naval forces.

Hyundai Heavy Industries Co. Ltd. is the leading player in the global market.

Asia Pacific dominated the market in terms of share in 2025.

Modern Air Lubrication Systems Used in Shipbuilding to Enable Market Growth

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us