Marine Propeller Market Size, Share & Industry Analysis, By Type (Propellers, Thrusters, and Others) By Application (Merchant Ships, Naval Ships, Recreational Boats, and Others), By Number of Blades (3-blade, 4-blade, and 5-blade), By Propulsion (Inboard, Outboard, Sterndrive, and Others), By Material (Stainless Steel, Aluminum, Bronze, Nickel-Aluminum Bronze, and Others), By End-User (OEM and Aftermarket), and Regional Forecast, 2026-2034

Marine Propeller Market Size & Trends

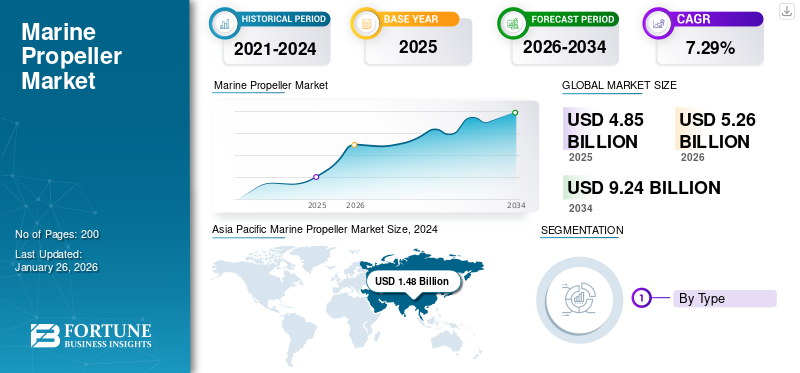

The global marine propeller market size was valued at USD 4.85 billion in 2025. The market is projected to grow from USD 5.26 billion in 2026 to USD 9.24 billion by 2034, exhibiting a CAGR of 7.29% during the forecast period. Asia Pacific dominated the marine propeller market with a market share of 33.08% in 2025.

A maritime propeller comprises a complex design containing radiating blades and a propeller shaft. The power-generated by the revolving blades moves a naval ship through the water, employing the central hub construction. Depending on the speed and maneuverability needs of the navy ship, a maximum of five to six radiating blades can be installed.

The maritime sector's growing demand for fuel-efficient and environmentally sustainable propulsion systems is driving advancements in marine propellers. This shift includes the implementation of hybrid and electric propulsion technologies, which improve fuel efficiency and lower emissions. The expansion of global trade and shipping operations, along with the growth of maritime tourism and recreational boating, is driving the demand for advanced marine propellers. This development highlights the need for effective and dependable propulsion systems for various ranges of vessels. In April 2021, Rolls-Royce reached an agreement with Fincantieri Marinette Marine to design and produce up to 40 fixed-pitch propellers for the U.S. Navy's Constellation-class (FFG-62) guided missile frigate program.

Ukraine and Russian ports on the Black Sea are major export hubs for corn, crude oil, and wheat. The war has led to the shutdown of cargo operations and export through the sea, slowing the growth of the marine sector.

On the other hand, European countries have increased their defense spending due to Russia’s invasion. Germany increased its defense spending above 2% of GDP and allocated USD 109 billion, which is more than the total defense bill for 2021.

Furthermore, Poland and Denmark also declared an increase in the defense budget for security purposes. On 16th March 2022, the Polish National Defense Minister announced that Warsaw would procure three new Mine Countermeasure Vessels (MCVs) to boost its naval capacities in the Baltic Sea.

On 22nd January 2022, Russia reportedly deployed 140 combat and supply ships, 1,000 military vehicles, and more than 50 aircraft for military exercises. In response, NATO deployed over 100 jets and 120 allied ships to the Mediterranean region.

With rising expenditure on the procurement of new warships and increased spending on the modernization of naval vessels, the market will witness significant growth during the forecast period.

Download Free sample to learn more about this report.

Marine Propeller Market Key Takeaways

- 2025 Market Size: USD 4.85 billion

- 2026 Market Size: USD 5.26 billion

- 2034 Forecast Market Size: USD 9.24 billion

- CAGR: 7.29% from 2026–2034

- Asia Pacific dominated the marine propeller market with a market share of 33.08% in 2025.

- The propellers segment led the market accounting for 49.56% market share in 2026.

- The merchant ships segment will grow with the highest CAGR during the forecast period.

Asia Pacific

The market reached USD 1.61 billion in 2025 and is projected to grow to USD 1.75 billion in 2026, supported by rising naval vessel procurement, ship modernization, and expanding maritime tourism.

Europe

Europe reached USD 1.22 billion in 2025 and is expected to reach USD 1.34 billion in 2026, supported by demand for cruise ships and yachts and advancements in propulsion technologies.

North America

North America generated USD 0.94 billion in 2025 and is projected to reach USD 1.01 billion in 2026, driven by investments in the marine industry and increasing adoption of advanced marine propulsion systems.

U.S.

The marine propeller market is projected to reach USD 0.79 billion by 2026, driven by marine fleet modernization, digitalization, and continued investment in the maritime sector.

Japan

The marine propeller market is projected to reach USD 0.19 billion by 2026, supported by the country's established shipbuilding industry and ongoing demand for advanced marine propulsion technologies.

Read More

Market Dynamics

Market Drivers

Increase in Demand for Electric Propulsion Technology in Shipbuilding Industry to Drive Market Growth

The Electric Propulsion System (EPS) includes hybrid diesel and gas turbine engines to power marine vessels. It uses diesel generator-powered energy to drive propeller blades, eliminating the need for clutches and gearing systems.

Compared to the traditional system, this technology has a number of advantages. It offers great redundancy, improved mobility, and increased payload due to the variable arrangement of mechanical components, decreased pollutants, and lower fuel consumption. In May 2020, Daewoo Shipbuilding & Marine Engineering, a South Korean shipbuilder, created an electric propulsion system for the Republic of Korea Navy's KDDX destroyer and LPX-II LHD projects.

Growth in International Seaborne Trade to Propel Market Growth owing to Post-Pandemic Trade Resumption

The United Nations Conference on Trade and Development (UNCTAD) reports that global maritime trade and transportation have been greatly affected by the healthcare and economic crises triggered by the pandemic, along with supply chain challenges. The marine propeller market is expected to witness substantial growth, driven by international seaborne trade, especially in the post-pandemic period. Following a significant downturn in 2020, global trade rebounded swiftly in 2021 and 2022, returning to pre-pandemic levels by early 2021. The recent increase in trade volumes has heightened demand for maritime transport services, particularly for dependable and efficient propulsion systems. In 2023, maritime trade volumes grew by 2.4% to reach 12,292 million tons, recovering from a decline in 2022.

This marine propeller market growth was fueled by the global economy's resilience and changes in trade dynamics influenced by geopolitical tensions and logistical hurdles. UNCTAD anticipates a 2% increase in maritime trade for 2024, with an average annual growth rate of 2.4% projected from 2025 to 2029. Containerized trade is forecast to expand by 3.5% in 2024 and by 2.7% each year from 2025 to 2029. Additionally, in 2023, ton-miles growth- measuring trade volumes adjusted for distance- surpassed the growth in total tons, rising by 4.2%, attributed to longer shipping routes caused by factors such as the conflict in Ukraine and lower water levels in the Panama Canal.

Market Restraints

Implementation of Stringent Environmental Regulations to Hamper Market Growth

Under the new IMO2020 requirements, sulfur content in fuel oil must be reduced from 3.50 percent m/m to 0.50 percent m/m (mass by mass). These new regulations aim to reduce health problems in coastal areas and port cities, while mitigating environmental impacts such as acid rain and lightning storms along trade routes. These severe environmental laws will considerably influence seaborne commercial activities, stifling business expansion.

The International Maritime Organization (IMO) implemented stringent sulfur regulations known as IMO2020. The new environmental rules would affect international shipping costs. These regulations are directly related to the level of Sulfur Oxide (SOx) emissions produced by shipping vessels sailing around the globe. Modern commercial ships and container ships run their engines on traditional fossil fuels, commonly referred to as ‘bunker fuels.’ These Include Marine Gas Oil (MGO), Marine Diesel Oil (MDO), Marine Fuel Oil (MFO), Heavy Fuel Oil (HFO), and Intermediate Fuel Oil (IFO).

Market Opportunities

Advanced, Sustainable, and Digitally Enabled Propulsion Systems Create Robust Market Opportunities

Stricter Environmental Regulations: International Maritime Organization (IMO) emissions standards and global decarburization goals are driving demand for cleaner, more fuel-efficient technologies, including advanced propellers and propulsion systems.

Technological Advancements: Innovations in propeller design (e.g., controllable pitch, hybrid systems), use of high-performance materials, digitalization, and integration of IoT and automation are enhancing efficiency, reliability, and operational control.

Growth in Global Trade and Shipping: Rising international seaborne trade, increased demand for cargo and passenger ships, and expanding marine tourism are boosting the need for efficient marine vessels and propellers.

Shift Toward Sustainability: The industry’s focus on reducing emissions and adopting alternative fuels (LNG and hybrid/electric systems) creates opportunities for propeller solutions that support green shipping initiatives

MARINE PROPELLER MARKET TRENDS

Increasing Adoption of Fixed Propeller in Marine Propulsion Systems Boosts Market Growth

The adoption and implementation of the fixed propeller have increased in recent years. In a fixed pitch marine propeller, the shaft and blades are permanently connected to the hub, with the pitch position of fixed pitch set during manufacturing, typically through casting. Copper alloy is frequently used to make it. Fixed pitch propellers are chosen for their durability and reliability, as they lack mechanical or hydraulic linkages. Compared to Controllable Pitch Propellers (CPP), they offer lower manufacturing, installation, and operational costs, further encouraging their adoption.

Growing Adoption of Rim Thruster in Marine Propulsion Systems to Strengthen Market Growth

The rim thruster has recently grown in popularity among major marine propeller rivals. It is an inexpensive and lightweight propulsion system. SCHOTTEL, a German-based company, has created a cutting-edge rim thruster with an aim to reduce noise and vibration. The Schottel rim thruster improves the effectiveness of the maritime propulsion system while lowering maintenance expenses. Interchangeable blades and slide bearings, water-lubricated bearings, and cost-effective operation are all aspects of the rim thruster. The market is likely to develop due to the rising use of rim thrusters in naval vessels.

Adoption of Environment-friendly Propulsion Systems to Drive Market Growth

Marine propulsion systems propel ships across the water while ensuring minimal environmental impact. The International Maritime Organization (IMO) has set emission reduction targets for the maritime industry, aiming to reduce carbon emissions from international shipping by at least 40% by 2030 and 70% by 2050.

- Asia Pacific witnessed marine propeller market growth from USD 1.30 Billion in 2023 to USD 1.48 Billion in 2023.

Due to rising fuel costs, end customers that use wind power to propel commercial ships have become more interested in wind propulsion systems. It also serves as a substitute for conventional propulsion methods that emit huge amounts of Carbon Dioxide (CO2). The International Windship Association (IWSA) launched a new initiative to accelerate decarburization in the shipping industry in February 2021. The campaign is known as the ‘Decade of Wind Propulsion,’ which aims to promote the adoption of wind-assisted propulsion, hybrid alternative propulsion methods, alternative fuels, and energy efficiency measures to enhance sustainability and reduce emissions.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Propellers Segment Dominated Backed by Increasing Usage of Naval Ships

Based on type, this market is classified into propellers, thrusters, and others.

The propellers segment led the market accounting for 49.56% market share in 2026. The dominance is due to the increased use of naval ships, recreational boats, and merchant ships. Furthermore, the market expansion of key players, the advent of 3D printing in the marine sector, and increased demand for naval vessels are projected to drive segment growth.

- The propellers segment is expected to hold a 49.7% share in 2023.

In April 2021, Nakashima Propeller announced the acquisition of Becker Marine Systems. This acquisition is projected to drive market growth due to a wide range of portfolios that both manufacturers possess such as high-efficiency propellers, rudders, and energy-saving marine devices.

Thruster segment is estimated to be the fastest growing segment during the forecast period of 2025-2032. The segment is witnessing significant growth due to increased demand for advanced propulsion systems in naval, merchant, and recreational vessels. Thrusters, including bow and azimuth thrusters, are increasingly adopted for precise maneuverability in confined spaces, making them integral to modern vessel designs. In addition, increasing maritime tourism activities have fueled demand for smaller vessels requiring efficient thrusters and propellers.

To know how our report can help streamline your business, Speak to Analyst

By Application

Merchant Ships Segment to Showcase Highest CAGR Due to Rising Trade of Imported Goods and Materials

By application, the market is divided into merchant ships, naval ships, recreational boats, and others.

The merchant ships segment will grow with the highest CAGR during the forecast period. The growth is attributed to the growing trade of imported goods and materials worldwide. According to the UNCTAD report (2021), dry bulk carriers have the highest share of 42.5% of dead-weight tonnage.

The naval ship segment will showcase remarkable growth during 2025-2032 due to the rising demand for defense vessels from China, the U.S., Russia, and others.

The recreational boat segment is projected to grow with significant CAGR due to recreational boat-based propellers' technological innovations. For instance, in September 2024, Rolls-Royce signed an agreement to sell its naval propellers and handling business to Fairbanks Morse Defense (FMD). This deal includes multiple units across North America, featuring a marine propeller and waterjet manufacturing facility located in Pascagoula. Rolls-Royce will retain its naval gas turbines and generator sets operations, which offer power-dense solutions for naval propulsion and on-board power requirements.

By Number of Blades

Increased Demand of Merchant Ships and Rising Shipbuilding Activities Lead 5-blade Propellers

By number of blades, the market is classified into 3-blade, 4-blade, 5-blade, and others.

The rising number of merchant, naval and coast guard, and recreational vessels deliveries is leading to the high demand generation for 5-blade marine propellers. The 5-blade segment dominated the market accounting for 45.15% market share in 2026. An increase in shipbuilding activities in China, Japan, South Korea, and Greece and rise in major shipbuilding countries, has led to market consolidation, owing to pandemic-led economic impact and weaker market growth in 2019.

For instance, China, India, and Singapore seek mergers in the shipbuilding industry. The two largest shipbuilders, Marine Engineering and Hyundai Heavy Industries and Daewoo Shipbuilding are waiting for the market competition review from regional governments and the shipbuilding industry.

The 3-blade segment is estimated to depict fastest growth during the forecast period of 2025-2032. 3-blade propellers play a significant role due to their efficiency and cost-effectiveness. These are widely used in smaller vessels, such as recreational boats and passenger ferries, due to their lightweight design, high-speed capabilities, and cost advantages aids the segmental growth.

By Propulsion

Sterndrive Segment dominated due to its Ability to Generate More Horsepower

Based on propulsion, the market is divided into inboard, sterndrive, outboard, and others. The inboard propulsion system will showcase remarkable growth during the forecast period from 2025-2032. Vessels with advanced inboard systems have their engines mounted inside the boat's hull. The inboard system is widely used in watersports boats, with a driveshaft connected to the propeller to power the boat.

The sterndrive segment dominated the market accounting for 33.61% market share in 2026. It is considered as the most powerful propulsion system, capable of generating more horsepower to boost the naval vessel than inboard and outboard.

By Material

Stainless Steel Segment Leads Due to its Growing Usage in Propulsion Systems

By material, the market is segmented into aluminum, stainless steel, aluminum, bronze, nickel-aluminum bronze, and others.

Marine propellers are made up of corrosion-resistant alloys such as aluminum and stainless steel. The stainless steel segment held the largest market share in 2024 due to the growing use of stainless steel material in the propulsion system. It provides higher strength and more reliability than other materials.

Other popular materials used are aluminum alloys, bronze, nickel-aluminum bronze, and others. The increasing adoption of corrosion-resistant alloys material in the propulsion system would drive segment growth.

Aluminum is estimated to be the fastest growing segment during the forecast period. Aluminum plays a key role due to their lightweight, cost-effectiveness, and performance advantages. Aluminum materials are significantly lighter than stainless steel or bronze alternatives, improving vessel acceleration and fuel efficiency. Their lightweight nature makes them ideal for recreational boats and smaller commercial vessels where speed and maneuverability are critical. They are also easier to repair, reducing maintenance costs for operators anticipating the segmental growth.

By End-User

OEM Segment to Depict Fastest Growth due to Increased Maritime Trade

Based on end-user, the market is classified into OEM and aftermarket.

The OEM segment is predicted to register the fastest growth during the forecast period attributed to the increasing demand for maritime trade for merchant vessels from China, India, and Australia. These merchant vessels are equipped with an advanced marine propeller to propel a vessel.

The aftermarket segment is estimated to show significant growth during the forecast period from 2025 to 2032 attributed to the increased upgrades of merchant vessels for enhanced maritime trade across the globe. The aftermarket segment includes the maintenance of propeller components.

MARINE PROPELLER MARKET REGIONAL OUTLOOK

By region, this market is studied across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

Asia Pacific Marine Propeller Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The Asia Pacific dominated the market with a valuation of USD 1.61 billion in 2025 and USD 1.75 billion in 2026, driven by the growing demand for frigates and corvettes from emerging economies, such as India and China, to improve naval fleet coordination. Several procurement initiatives and growing demand for modern amenities in the cruise ship further contribute to market growth. South Korea is the largest supplier of merchant ships in the region. Additionally, the upgrading of marine propeller design systems for older vessels is propelling market growth. The growing popularity of maritime travel tourism activities is also a key growth driver in this region.

The Japan market is projected to reach USD 0.19 billion by 2026, the China market is projected to reach USD 0.49 billion by 2026, and the India market is projected to reach USD 0.32 billion by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 1.22 billion in 2025, accounting for 25.09% share, and is expected to reach USD 1.34 billion in 2026. The market in Europe is estimated to be the fastest growing segment during the forecast period, supported by the presence of leading marine interior manufacturers in France, Germany, the U.K., and Russia. The increasing demand for cruise ships and yachts is driving market expansion. Firms such as SCHOTTEL, Volvo Group, and Wärtsilä play significant roles in the European market, providing various propulsion systems designed for multiple types of vessels. Partnering with top manufacturers and research organizations are propelling technological advancements. The incorporation of intelligent technologies and automation into marine operations is improving the performance of propellers and enhancing fuel efficiency. These innovations present operational benefits by enabling immediate adjustments to maximize vessel performance.

The UK market is projected to reach USD 0.39 billion by 2026, while the Germany market is projected to reach USD 0.25 billion by 2026.

North America

The North America region captured 19.30% of the global market in 2025, generating USD 0.94 billion in revenue, and is projected to reach USD 1.01 billion in 2026. This growth is attributed to the upgrade of dry cargos for real-time data exchange in the U.S. due to the region's flourishing marine industry, presence of the largest marine lines, rise in investment in the marine sector, and increase in the number of marine propeller manufacturers. Furthermore, the high demand for specialized vessels in maritime tourism in Canada is expected to further boost market expansion. The U.S. market is projected to reach USD 0.79 billion by 2026.

Middle East & Africa

Middle East & Africa recorded a market size of USD 0.65 billion in 2025, capturing 13.40% of the global market share, and is projected to reach USD 0.69 billion in 2026. Market development in these regions is fueled by high-net-worth individuals, rise in travel and business opportunities, changing passenger preferences, growing demand for modern ship amenities, and the increasing number of shipbuilding industries.

Latin America

The Latin America market generated USD 0.44 billion in 2025, representing 9.13% of the global market landscape, and is expected to reach USD 0.47 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Technological Trends Implemented by Key Players to Propel Market Growth

The market's forthcoming trends include fuel-efficient propulsion systems, improved materials, rim thrusters, and anti-fouling coatings. Leading players, such as Hyundai Heavy Industries and MAN SE, drive innovation through diverse product portfolios and research & development efforts. Brunswick Corporation introduced the MerCruiser Bravo Four S front-facing drive with Smart Tow technology in August 2020, which grips the water for enhanced maneuverability.

LIST OF KEY MARINE PROPELLER COMPANIES PROFILED

- AB Volvo (Sweden)

- Brunswick Corporation (U.S.)

- Kongsberg Gruppen (Norway)

- Mecklenburger Metallguss GmbH (Germany)

- Bruntons Propellers Ltd. (U.K.)

- Hyundai Heavy Industries Co., Ltd. (South Korea)

- Kawasaki Heavy Industries, Ltd. (Japan)

- MAN SE (Germany)

- NAKASHIMA PROPELLER Co., Ltd. (Japan)

- Rolls-Royce plc (U.K.)

- SCHOTTEL Group (Germany)

- Michigan Wheel Holdings LLC (U.S.)

- Wärtsilä Corporation (Finland)

- VEEM Propellers Ltd. (Australia)

- Andritz AG (Austria)

KEY INDUSTRY DEVELOPMENTS

- January 2025 - Schottel secured a contract to provide propellers and a thruster for a Multi-Purpose Support Ship (MPSS) that Damen is constructing for the Portuguese Navy. For the primary propulsion system, Schottel would supply two EcoPeller type SRE 560 azimuth thrusters, each featuring an electric power input of 2,600 kW.

- January 2025 - Kongsberg Maritime secured a contract to provide sophisticated propulsion and maneuvering systems for the Indonesian Navy’s latest KCR-70 Fast Attack Craft. These vessels, which are developed from the FACM-70 design, are currently being built at Sefine Shipyard in Türkiye. The state-of-the-art propulsion system integrates twin Controllable Pitch Propeller (CPP) Promas systems with a central Kamewa waterjet to provide additional power. This hybrid setup improves speed, maneuverability, and efficiency, allowing the vessels to achieve speeds over 40 knots during high-speed maneuvers.

- December 2024 - Sharrow Marine is set to reveal that its groundbreaking Sharrow Propeller is now offered as an approved supplier choice via ADS, Inc., a leading distributor in defense contracting. This partnership with ADS would facilitate easier access to Sharrow's cutting-edge propellers for multiple defense departments, including the U.S. Navy, Coast Guard, and other governmental organizations.

- November 2024 - In an important move to enhance naval technology, India and the U.K. signed an agreement to work together on designing and developing electric propulsion systems for the Indian Navy. This agreement, which was signed during the third joint working group meeting of the electric propulsion capability partnership in Portsmouth, U.K., represents a notable advancement in promoting indigenous development of state-of-the-art maritime technologies.

- September 2024 - Fairbanks Morse Defense, part of the Arcline Investment Management portfolio, reached an agreement to acquire the naval propulsors and handling division of Rolls-Royce to enhance its capabilities and offerings for clients in the U.S. marine defense industry. The naval marine propellers from Rolls-Royce are utilized in the fleet support vessels, surface combatants, amphibious ships, aircraft carriers of the U.S. Navy, and in the vessels of the U.S. Coast Guard. Additionally, the company's handling systems are employed on the Navy's surface combatants.

REPORT COVERAGE

The research report offers qualitative and quantitative insights into this market. It offers a detailed analysis of the market and segments. It also provides an elaborative analysis of dynamics, the impact of COVID-19, emerging trends, UNCTAD maritime transport report, and the competitive landscape. The report also provides information on recent industry developments such as mergers & acquisitions, partnerships, SWOT analysis, Porter’s Five Forces analysis, business strategies of leading market players, and micro and macroeconomic indicators.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.29% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Application

|

|

|

By Number of Blades

|

|

|

By Propulsion

|

|

|

By Material

|

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 5.26 billion in 2026 and is projected to reach USD 9.24 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.61 billion.

Registering a CAGR of 7.29%, the market will exhibit steady growth in the forecast period (2026-2034).

By type, the propellers segment led the market.

The shipbuilding industrys increased demand for electric propulsion technology is a key factor driving market growth.

AB Volvo (Sweden), Brunswick Corporation (U.S.), Caterpillar (U.S.), and Hyundai Heavy Industries Co., Ltd. (South Korea) are the major players in the market.

Asia Pacific dominated the market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us