Carrier Screening Market Size, Share & Industry Analysis By Type (Targeted Disease Carrier Screening, Expanded Carrier Screening (ECS), and Custom Panel Screening), By Technology (DNA Sequencing, Polymerase Chain Reaction (PCR), Microarray-based Screening, and Others), By Indication (Hemoglobinopathies, Cystic Fibrosis, Spinal Muscular Atrophy (SMA), Fragile X, and Others), By Sample Type (Blood, Saliva, and Others), By Service Provider (Clinical Laboratories, Hospital Laboratories, Direct-to-Consumer (DTC) Testing Companies, and Others), and Regional Forecast, 2026-2034

Carrier Screening Market Size and Future Outlook

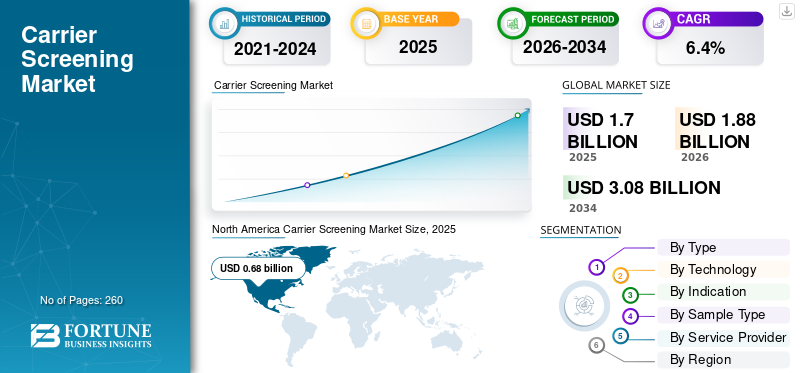

The global carrier screening market size was valued at USD 1.70 billion in 2025 and is projected to grow from USD 1.88 billion in 2026 to USD 3.08 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period. North America dominated the global carrier screening market with a market share of 40.% in 2025.

Carrier screening is a genetic test that identifies whether a person carries a gene for a specific inherited condition, even if they do not exhibit symptoms themselves. It is recommended before or during pregnancy to understand the risk of passing a recessive genetic disorder to a child. The rising number of genetic disorders is further supporting the demand for carrier screening, thereby driving the adoption rate of products and services in the market.

- For instance, according to data published by the World Health Organization (WHO) in 2025, globally, it is estimated that approximately 7.9 million births, or 6% of total births annually, occur with a genetic or partially genetic defect.

Moreover, the increasing strategic initiatives by key players operating in the market to improve their market share and raise awareness about personalized medicine and companion diagnostics are likely to boost test volumes among the patient population in the market. This, coupled with a growing focus on research and development activities to develop and introduce novel screening tests among key players, including Natera, Inc., Labcorp, Quest Diagnostics Incorporated, Myriad Genetics, Inc., and others, is expected to drive the global carrier screening market growth.

Download Free sample to learn more about this report.

Carrier Screening MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.70 billion

- 2026 Market Size: USD 1.88 billion

- 2034 Forecast Market Size: USD 3.08 billion

- CAGR: 6.4% from 2026–2034

- North America dominated the carrier screening market with a 40% share in 2025.

- NGS segment led the market with a 73.3% share in 2025.

- Clinical laboratories segment dominated with a 57.0% share in 2026.

North American

North America led with USD 0.68 billion in 2025 and is projected to reach USD 0.72 billion in 2026, driven by strong genetic testing adoption and healthcare infrastructure.

Europe

Europe is expected to reach USD 0.50 billion in 2026, supported by NHS and Genomics England initiatives and rising test volumes.

Asia Pacific

Asia Pacific is projected to reach USD 0.34 billion in 2026, emerging as the second-largest regional market.

U.S.

Estimated to reach USD 0.72 billion in 2026, supported by high adoption of advanced genetic screening and strong reimbursement coverage

Japan

Growing demand driven by increasing awareness of genetic disorders and expanding adoption of precision medicine-based screening programs.

Read More

Market Dynamics:

Market Drivers

Technological Advancements and Rising Awareness to Augment Market Growth

The global carrier screening market is experiencing strong growth as technology, policy, and clinical practice come together to shape demand. One of the most significant influences has been the widespread adoption of next-generation sequencing (NGS). This technology has made testing more affordable, reducing the cost per test and enabling the simultaneous screening of multiple conditions through expanded carrier screening (ECS) panels. Between 2018 and 2023, sequencing costs are estimated to have fallen by over 40 percent. As a result, laboratories worldwide have been transitioning from traditional, single-gene PCR tests to broader, panel-based approaches that enhance accuracy and increase overall testing volumes.

Additionally, regulatory changes have also had a major impact on the overall market. In 2021, the American College of Medical Genetics (ACMG) updated its guidelines to recommend ECS for anyone planning a pregnancy, regardless of ethnic background. This inclusive approach led to a sharp rise in testing across the U.S. and spurred adoption in other regions such as Europe, Australia, and parts of Asia. Additionally, the increasing number of in vitro fertilization (IVF) procedures and integration of carrier screening into standard preconception and IVF processes have further driven demand. Fertility clinics now frequently include ECS to help lower the risk of inherited diseases.

- For instance, according to the American Society for Reproductive Medicine (ASRM), the total number of IVF cycles performed at the 371 reporting SART member clinics increased from 389,993 in 2022 to 432,641 in 2023.

Furthermore, awareness campaigns focused on conditions such as thalassemia, spinal muscular atrophy (SMA), and cystic fibrosis have also promoted broader acceptance of genetic screening. Identifying carrier status early can help prevent severe genetic disorders, which in turn motivates healthcare providers, governments, and insurers to expand access to testing. Together, these factors are driving faster adoption and deeper market penetration across both developed and emerging healthcare systems, thereby contributing to the global carrier screening market growth.

Market Restraints

High Cost Associated with Tests to Limit the Product Adoption

While the global carrier screening market continues to grow, several challenges still limit its complete adoption. The most significant hurdle remains the cost of testing, particularly in developing countries. Even though next-generation sequencing (NGS) has become more affordable, expanded carrier screening (ECS) panels still range between USD 250 to 600 in many regions. Without widespread insurance coverage, these costs remain prohibitive for large portions of the population. Reimbursement policies also vary widely. Some countries, such as the U.S., Australia, and a few European nations, subsidize testing; however, many health systems in Asia, Latin America, and Africa provide little to no support for testing.

Furthermore, the uneven adoption of screening guidelines, as many health authorities continue to rely on ancestry-based or disease-specific approaches, prevents large-scale rollout. The lack of standardized national or international frameworks delays integration into public health programs. For instance, while the U.S. and Australia now recommend universal ECS, the U.K. NHS still limits testing to high-risk groups, slowing broader access.

Additionally, the shortage of trained professionals also constrains growth. Carrier screening typically requires genetic counseling both before and after testing; however, many regions lack sufficient qualified professionals to meet the rising demand. This shortfall is particularly evident in rapidly growing fertility markets, such as India and Southeast Asia.

Therefore, all the above-mentioned factors, coupled with a stringent regulatory scenario for approving related products, are responsible for the reduced demand and adoption rate of these tests, which is further expected to hinder market growth.

Market Opportunities

Penetration of Carrier Screening into Emerging Markets to Create Market Opportunities

The global carrier screening market is set for strong growth as new opportunities emerge across regions and technologies. One of the largest opportunities lies in the penetration of ECS into emerging markets. Countries such as India, Brazil, Indonesia, and the GCC states are seeing steady growth in fertility treatments along with rising awareness of genetic disorders. With more than 140 million births recorded each year across the Asia-Pacific and Africa regions, even partial carrier screening adoption could translate into billions of dollars in additional market value.

Furthermore, government-backed genetic health programs are also helping shape this opportunity. Nations such as the UAE, Saudi Arabia, and Qatar already operate nationwide premarital screening initiatives focused on hemoglobinopathies, and several are now considering the inclusion of broader expanded carrier screening (ECS) panels. In parallel, China’s large-scale investments in genomics and population health infrastructure are opening another major frontier for market expansion.

The growing connection between carrier screening, IVF, and preconception care is further reshaping global carrier screening market demand, and leading fertility centers are increasingly offering bundled genetic testing packages that pair carrier screening with aneuploidy testing and polygenic risk scoring. Additionally, integration of artificial intelligence tools that assist in variant interpretation, along with automated lab workflows, is helping laboratories cut turnaround times and lower operating costs. Strategic partnerships between sequencing providers and fertility clinics are also creating new business models, thereby generating a significant market opportunity.

Market Challenges

Limited and Resistant Diagnosis in Developing Countries to Hinder the Market Growth

There is an increasing focus on strategic initiatives among governmental and non-governmental organizations to raise awareness about the early detection and monitoring of genetic diseases among the patient population. However, an increasing prevalence of delayed diagnosis of genetic conditions owing to distinct factors, such as late referrals of patients with genetic conditions, along with limited expertise among genetic counseling to identify diseases, especially in emerging countries.

Furthermore, ethical, legal, and cultural considerations pose challenges. Concerns around reproductive decision-making, carrier disclosure, and genetic privacy create resistance in certain populations. These challenges collectively limit the global uniformity and scalability of carrier screening programs in developing countries.

Carrier Screening Market Trends

Preferential Shift from Targeted Tests to Expanded Multi-Gene Panels to Fuel Test Demand

Several major trends are reshaping the carrier screening market. First, the rapid migration from targeted tests to expanded multi-gene panels continues globally. In 2023, more than 70% of tests in North America are already panel-based, and Europe and the APAC region are following a similar trajectory. Panel standardization across labs is increasing clinical confidence and simplifying payer policies.

Additionally, another major trend is the normalization of at-home sample collection and saliva kits, driven by DTC genomics players and IVF centers catering to convenience-focused patients. This has lowered access barriers and expanded testing to rural and remote populations. These trends shorten turnaround time, enabling scale-up of testing volume. Collectively, these trends indicate a clear shift toward high-throughput, AI-enabled, patient-centric carrier screening ecosystems.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Increasing Number of Expanded Carrier Screening (ECS) Tests to Lead Segment Dominance

Based on type, the market is bifurcated into Targeted disease carrier screening, expanded carrier screening (ECS), and custom panel screening.

To know how our report can help streamline your business, Speak to Analyst

The expanded carrier screening (ECS) segment held the largest global carrier screening market share in 2025. The growth is primarily driven by the increasing number of expanded carrier screening (ECS) tests, which cover hundreds of genes simultaneously, regardless of ethnicity or family history. This, coupled with the growing focus of healthcare organisations on published guidelines to incorporate carrier screening. For instance, the American College of Medical Genetics and Genomics (ACMG) provides guidelines on preconception and prenatal carrier screening.

The custom panel screening segment is expected to grow at a CAGR of 5.9% over the forecast period.

By Technology

Increasing Prevalence of Genetic Disorders Fuels Next-Generation Sequencing (NGS) Segmental Growth

Based on technology, the market is segmented into next-generation sequencing (NGS), polymerase chain reaction (PCR), microarray-based screening, and other technologies.

The next-generation sequencing (NGS) segment dominated the global market in 2025. By technology, the next-generation sequencing (NGS) segment accounted for a 73.3% share in 2025. The growth is attributed to the increasing prevalence of genetic disorders, such as hemoglobinopathies, cystic fibrosis, spinal muscular atrophy (SMA), fragile X syndrome, and others, resulting in high utilization of next-generation sequencing (NGS), thereby contributing to the segment's growth. Additionally, a decrease in sequencing costs per gene, expansion of ECS panels, and a rise in reimbursement for tests contribute to the segmental growth.

The polymerase chain reaction (PCR) segment is poised for growth, with a forecasted rate of 6.0% over the forecast period.

By Indication

Growing Prevalence of Hemoglobinopathies Led to the Dominance of the Segment

Based on the indication, the market is segmented into hemoglobinopathies, cystic fibrosis, spinal muscular atrophy (SMA), fragile X syndrome, and others.

The hemoglobinopathies segment dominated the market in 2025. In 2026, the segment is anticipated to dominate with a 28.9% share. The dominant share is attributed to the growing prevalence of hemoglobinopathies, such as thalassemia and sickle cell, which in turn leads to an increasing number of carrier screening tests globally.

- For instance, according to data published in the 2023 Global State of Thalassemia Awareness Report by BGI Genomics, 5.2% of the global population carries hemoglobin abnormalities, resulting in approximately 300,000 to 400,000 children born with severe hemoglobinopathies each year. Thalassemia, a hereditary hemoglobinopathy, occurs in approximately 4.4 out of every 10,000 live births and is more prevalent in Mediterranean coastal areas, Africa, the Middle East, Southeast Asia, and southern China.

The spinal muscular atrophy (SMA) segment is expected to grow at a CAGR of 7.1% over the forecast period.

By Sample Type

Preferred Blood Sample for Accurate Diagnosis Led to the Segmental Dominance

Based on sample type, the market is divided into blood, saliva, and others.

The blood segment dominated the market in 2025. The high preference for blood samples by clinical laboratories is due to their high efficiency and accuracy in disease diagnosis and monitoring. Furthermore, the segment is set to hold a 73.7% share in 2026.

- For instance, according to statistics published by the Royal College of Pathologists, 500 million bio-chemistry and 130 million haematology tests are carried out annually, resulting in 14 tests for each person in England and Wales being performed.

In addition, the saliva segment is projected to grow at a CAGR of 6.8% during the study period.

By Service Provider

Increasing Number Test Volume in Clinical Laboratories Led to the Segmental Dominance

Based on the service provider, the market is divided into clinical laboratories, hospital laboratories, direct-to-consumer (DTC) testing companies, and others.

The clinical laboratories segment dominated the market in 2025. The increasing prevalence of genetic diseases, a rising patient pool, a growing number of test volumes, and an increase in the number of clinical laboratories are key factors driving segmental growth in the market. Furthermore, the segment is set to hold a 57.0% share in 2026.

- For instance, according to statistics published by the American Clinical Laboratory Association, approximately 322,488 clinical laboratories are operating in the U.S.

In addition, the direct-to-consumer (DTC) testing companies segment is projected to grow at a CAGR of 7.0% during the study period.

Carrier Screening Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America:

North America held the dominant share in 2024, valued at USD 0.62 billion, and also took the leading share in 2025 with USD 0.68 billion. The dominance of the region is attributed to several factors, including the growing prevalence of genetic disorders, the development of healthcare infrastructure, adequate reimbursement policies, the growing adoption of technologically advanced technologies, and others. In 2026, the U.S. market is estimated to reach USD 0.72 billion.

- For instance, according to data published by the Centers for Disease Control & Prevention (CDC) in 2024, approximately 350 million tests are performed annually in the U.S.

North America Carrier Screening Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe and Asia Pacific:

Other regions, such as Europe and the Asia Pacific, are expected to witness considerable growth in the forecast period. During the study period, the European region is projected to record a growth rate of 6.0% and reach the valuation of USD 0.50 billion in 2026. The wide adoption of NGS by the NHS and Genomics England, a growing number of test volumes, stringent regulatory standards, the widespread implementation of digital pathology systems, increasing demand for these carrier screening services, improved healthcare access, strategic government initiatives, and others are some of the factors supporting the growth of the market in the region. Backed by these factors, countries such as the U.K. are expected to record the valuation of USD 0.07 billion, Germany to record USD 0.11 billion, and France to record USD 0.08 billion in 2026. After Europe, the market in the Asia Pacific is estimated to reach USD 0.34 billion in 2026 and secure the position of the second-largest region in the market. In the region, India is projected to reach USD 0.07 billion, while China is expected to reach USD 0.08 billion by 2026.

Latin America and Middle East & Africa

Over the study period, the Latin America and Middle East & Africa regions are expected to witness considerable growth in this market. The Latin America market in 2026 is expected to reach a valuation of USD 0.16 billion. The growing prevalence of genetic diseases, rising awareness about early disease diagnosis, increasing healthcare modernization projects, and improvement in healthcare systems drive product adoption in these regions. In the Middle East & Africa, GCC is set to attain the value of USD 0.06 billion in 2026.

Competitive Landscape

Key Industry Players

Increasing Number of Test Volumes Among the Key Players to Contribute to Their Dominance

A robust and diversified service portfolio, coupled with technologically advanced laboratories and a significant global brand presence, is one of the crucial factors supporting the dominance of these players in the market. Natera, Inc., Labcorp, Quest Diagnostics Incorporated, and Myriad Genetics, Inc. are prominent players in the market in 2025. Moreover, key players offer a wide range of ECS and NIPT tests and have a strong penetration in obstetrics and gynecology tests.

- For instance, Natera, Inc. offers Horizon, which provides comprehensive screening using the latest technology, including next-generation sequencing. Horizon screens for genes associated with specific inherited genetic conditions, including commonly screened conditions such as cystic fibrosis, spinal muscular atrophy, fragile X syndrome, and sickle cell anemia.

Other key players, including Fulgent Genetics, BGI Group, Berry Genomics, Eurofins Scientific, and others, are also expanding their market share through strategic initiatives aimed at increasing their geographical presence in emerging countries to strengthen their services.

List of Key Carrier Screening Companies Profiled:

- Natera, Inc. (U.S.)

- Labcorp (U.S.)

- Quest Diagnostics Incorporated. (U.S.)

- Myriad Genetics, Inc. (U.S.)

- Fulgent Genetics (U.S.)

- BGI Group (China)

- Berry Genomics (China)

- Eurofins Scientific (Luxembourg)

- CENTOGENE GmbH (Germany)

- YOURGENE HEALTH (U.K.)

- MedGenome (India)

KEY INDUSTRY DEVELOPMENTS:

- October 2024 – Yourgene Health (part of the Novacyt group of companies), a leading international molecular diagnostics group, announces that it has received accreditation under the new EU requirements of the in vitro diagnostic regulation (IVDR) for the Yourgene Cystic Fibrosis Base assay.

- January 2024 – Natera, Inc., a global leader in cell-free DNA (cfDNA) testing, announced that it has acquired reproductive health assets from Invitae. These assets relate to Invitae’s non-invasive prenatal screening and carrier screening business.

- October 2022 – Ambry Genetics, a leader in clinical diagnostic testing and a subsidiary of REALM IDx, launched a new reproductive health program driven by its CARE ProgramTM (Comprehensive Assessment, Risk, and Education). This digital platform enhances the patient and provider experience by providing easier access to genetic education, testing, reporting, and counseling.

- February 2020 – Asuragen, Inc., a molecular diagnostics company delivering high-quality, easy-to-use products for complex testing in genetics and oncology, announced that its AmplideX Fragile X Dx and Carrier Screen Kit has been cleared by the U.S. Food and Drug Administration (FDA).

REPORT COVERAGE

The market report provides a detailed analysis of the global carrier screening market, focusing on key aspects such as leading companies, types, applications, techniques, and end-users. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.4% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Technology, Indication, Sample Type, Service Provider, and Region |

|

By Type |

|

|

By Technology |

|

|

By Indication |

|

|

By Sample Type |

|

|

By Service Provider |

|

|

By Region |

North America (By Type, By Technology, By Indication, By Sample Type, By Service Provider, and by Country)

Europe (By Type, By Technology, By Indication, By Sample Type, By Service Provider, and by Country/Sub-region)

Asia Pacific (By Type, By Technology, By Indication, By Sample Type, By Service Provider, and by Country/Sub-region)

Latin America (By Type, By Technology, By Indication, By Sample Type, By Service Provider, and by Country/Sub-region)

Middle East & Africa (By Type, By Technology, By Indication, By Sample Type, By Service Provider, and by Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.70 billion in 2025 and is projected to reach USD 3.08 billion by 2034.

In 2025, the North America regional market value stood at USD 0.68 billion.

Growing at a CAGR of 6.4%, the market will exhibit steady growth over the forecast period (2026-2034).

By type, the expanded carrier screening (ECS) segment is the leading segment in this market.

Technological advancements and rising awareness are among the major factors driving the market's growth.

Natera, Inc., Labcorp, Quest Diagnostics Incorporated, and Myriad Genetics, Inc., are the major players in the global market.

North America dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 260

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us