Charging as a Service Market Size, Share & Industry Analysis, By Service (Usage-Based, Subscription, and Others), By Application (Commercial and Residential), By Charging point (Fast and slow), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

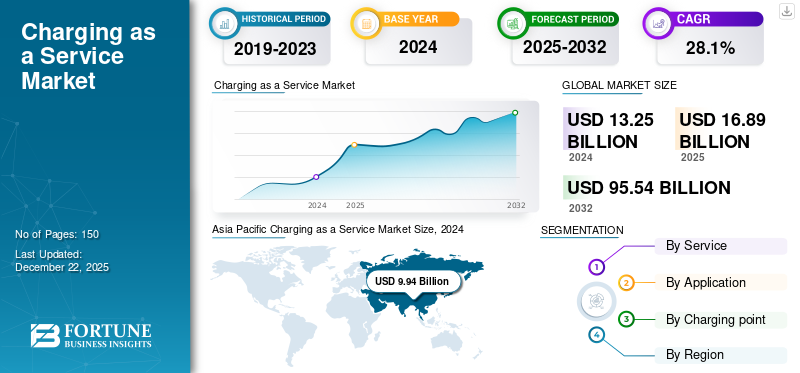

The global charging as a service market size was valued at USD 16.89 billion in 2025. The market is projected to grow from USD 21.87 billion in 2026 to USD 130.18 billion by 2034, exhibiting a CAGR of 24.98% during the forecast period.

Charging-as-a-Service (CaaS) refers to the business model in which providers offer electric vehicle (EV) charging infrastructure, software, and operational services on a subscription, pay-per-use, or contract basis. It enables fleets, businesses, municipalities, and individual EV owners to access and use charging facilities without bearing the upfront capital expenditure (CAPEX) of setting up chargers, grid integration, maintenance, and software management.

Furthermore, the market encompasses several major players with ChargePoint, EVgo, Shell Recharge Solutions, and BP Pulse at the forefront. A broad service portfolio, continuous innovation in subscription and fleet-based models, and strong geographic expansion have supported the dominance of these companies.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Electric Vehicle (EV) Adoption to Propel Market Growth

Rapid adoption of electric vehicles (EVs) worldwide drives the charging as a service market. Falling battery costs, stricter emission regulations, government incentives, and rising consumer awareness of sustainability are pushing EV sales upward across passenger cars, commercial vehicles, and public transport fleets. This development increases the demand for charging as a service.

Global EV sales have grown from about 10 million units in 2022 to an expected 17 million in 2024, with China and Europe leading in adoption.

MARKET RESTRAINTS

High Infrastructure and Maintenance Costs May Limit Market Growth

Installing and maintaining EV charging infrastructure requires significant capital expenditure, making it one of the restraints. The cost of a standard Level 2 charger ranges between USD 2,000–5,000, while a single DC fast charger can cost USD 40,000–100,000 or more, excluding grid upgrades and land acquisition. This results in long payback periods, especially in regions with limited EV adoption.

MARKET OPPORTUNITIES

Fleet Electrification and Logistics Demand Create Lucrative Opportunities

Rapid electrification of commercial fleets create lucrative opportunities for charging as a service market. The rapid electrification includes last-mile delivery, ride-hailing services, and public transport buses in urban areas. Amazon, FedEx, and UPS are transitioning thousands of vehicles to EVs to meet sustainability targets and reduce operating costs.

- For instance, Amazon has committed to deploying 100,000 electric delivery vans by 2030, while FedEx aims for a fully electric fleet by 2040. The requirement for depot charging, route optimization, and cost management creates an opportunity for charging as a service market growth.

MARKET CHALLENGES

Limited Grid Capacity and Power Supply is a Challenging Factor

The effectiveness of charging as models depends heavily on a reliable electricity supply, yet many regions face challenges with grid infrastructure. High-capacity charging hubs require strong grid connections, which may not be available in developing economies. Grid instability, frequent outages, and limited capacity can lead to inconsistent service, making it difficult for charging as a service provider to ensure customer satisfaction.

CHARGING AS A SERVICE MARKET TRENDS

Subscription-Based Charging Models is One of the Significant Market Trends

A major trend in the charging-as-a-service market is the rise of subscription-based charging, where users pay a fixed monthly fee for unlimited or discounted charging access. This model provides predictable revenue for operators and is cost effective for consumers, especially frequent EV users and fleets. Manufacturers such as Tesla and Hyundai are also partnering with networks to bundle charging subscriptions with EV purchases.

- For instance, Ionity in Europe offers a subscription package that reduces charging costs by nearly 50% per kWh compared to ad-hoc usage.

Download Free sample to learn more about this report.

Segmentation Analysis

By Service

Cost Transparency & Flexibility of Usage-Based Service Drive Market Growth

On the basis of service, the market is classified into usage-based, subscription, and others.

The usage-based segment is expected to hold the maximum charging-as-a-service market share of 49.93% in 2026. The pay-per-use (per kWh) model allows electric vehicle users to pay only for the exact amount of electricity they consume, making it highly transparent and economical. However, compared to other plans that may include unused credits or fixed monthly upfront costs, this model eliminates unnecessary expenses.

- For instance, Tesla offers pay-per-use charging where costs vary regionally but are billed per kWh (e.g., USD 0.25–0.50/kWh in the U.S.). Drivers pay only for what they consume, making it attractive for both regular commuters and occasional long-distance travelers.

To know how our report can help streamline your business, Speak to Analyst

By Application

Corporate Adoption of Electric Vehicle Drive Commercial Application Segment Growth

In terms of application, the market is categorized into commercial and residential

The commercial segment is expected to capture the largest share of 83.31% of the market in 2026. The segment’s growth is attributed to rapid electrification of fleets for logistics vans, last-mile delivery vehicles, taxis, ride-hailing services, and municipal/public buses. Logistics firms, ride-hailing operators, delivery companies, and public transport agencies are rapidly shifting to EV fleets to cut fuel costs and meet carbon targets.

- In December 2024, Amazon India announced the company deployed EVs across 500 cities, helping Amazon's 2040 net-zero carbon goal. The initiative reduces emissions and supports India's sustainability efforts.

By Charging point

Higher Revenue Potential for Operators Drive Growth for Fast Charging Points

Based on charging point, the market is segmented into fast and slow.

The Fast segment is expected to lead the market, contributing 78.70% globally in 2026. Fast public and private charging stations (DC fast chargers) generate more revenue per unit of time compared to slow AC chargers, this is the preferred choice for charging as a service providers and investors. This development increases the demand for fast charging points during the forecast period.

- For instance, General Motors forecasts a rapid expansion of public DC fast-charging infrastructure—from around 60,000 stalls currently to a staggering 100,000 by the end of 2027

Charging as a Service Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and rest of the world

Asia Pacific Charging as a Service Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific dominated the market with a valuation of USD 12.72 billion in 2025 and is projected to reach USD 16.51 billion in 2026. Asia Pacific (APAC) is the dominating region in the Charging-as-a-Service (CaaS) market, mainly driven by China’s extensive electric vehicle adoption, strong government policies, and rapid infrastructure investment. China accounts for more than half of the world’s public EV chargers, with over 1.8 million public charging points installed by 2023, far ahead of other regions. Japan and South Korea are also investing heavily in fast-charging corridors and smart-grid integration, while India is emerging with government-backed incentives and private investments in solar-powered charging hubs. The combination of scale, policy support, and consumer demand drive market growth The Japan market is projected to reach USD 0.49 billion by 2026, the China market is projected to reach USD 13.32 billion by 2026, and the India market is projected to reach USD 1.15 billion by 2026.

North America

The North America market accounted for USD 0.7 billion in 2025, representing 4.17% of the global industry, and is expected to reach USD 0.9 billion in 2026. North America, Europe, and the rest of the world, are expanding steadily. In North America, U.S. initiatives such as the NEVI program are funding nationwide fast-charging networks, with major players such as Tesla, ChargePoint, and Electrify America leading. Europe remains in a strong position, supported by the EU’s regulation mandating charging stations along highways and Norway achieving EV penetration above 80% of new car sales. However, Latin America, the Middle East, and Africa are still in the early stages of adoption due to lower EV penetration and weaker grid infrastructure. The U.S. market is projected to reach USD 0.75 billion by 2026.

Europe

Europe recorded a market size of USD 3.08 billion in 2025, capturing 18.22% of the global market share, and is projected to reach USD 3.96 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings coupled with Strong Distribution Network of Key Companies Support their Leading Position

The global Charging as a Service (CaaS) market shows a semi-concentrated structure, with numerous small-to-mid-size companies actively operating across different regions. These players are focused on charging technological innovation, infrastructure partnerships, and international expansion to strengthen their foothold.

Tesla Inc., BP Pulse, and Shell Recharge Solutions are some of the market's dominant players. Their broad portfolio of fast-charging networks, global presence supported by extensive retail and service station networks, and strategic collaborations with manufacturers and governments are a few characteristics that underpin their dominance.

Other prominent players in the market include Electrify America, EVgo, ChargePoint, Ionity, Tata Power, Fastned, and Blink Charging.

LIST OF KEY CHARGING AS A SERVICE COMPANIES PROFILED

- Tesla Inc. (U.S.)

- BP Pulse (U.K.)

- Shell Recharge Solutions (Netherlands)

- Electrify America (U.S.)

- EVgo (U.S.)

- ChargePoint (U.S.)

- Ionity (Germany)

- Tata Power EV Charging (India)

- Fastned (Netherlands)

- Blink Charging (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2025: China’s CATL announced plans to expand its EV battery-swapping business, aiming to build 1,000 swap stations in the near term and 10,000 long term, initially focusing on fleets.

- December 2024: Brooklyn-based startup It’s Electric began deploying curbside chargers across New York City, with a goal of scaling from 1,400 to 10,000 units by 2030.

- October 2024: EDF confirmed its acquisition of UK-listed Pod Point for over USD 12 million, with plans to shift it from hardware-focused business to a subscription-based charging service model.

- September 2024: ChargePoint expanded its fleet solutions by acquiring ViriCiti, a company specializing in fleet monitoring and energy management software.

- July 2023: Engie acquired EVBox to scale its global EV charging services, reinforcing its role as a major market player in Europe and beyond

REPORT COVERAGE

The global charging as a service market analysis provides an in-depth study of market size & forecast by all market segments included in the report. It includes details on market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The report also encompasses detailed competitive landscape with information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 24.98% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service

|

|

By Application

|

|

|

By Charging Point

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 16.89 billion in 2025 and is projected to reach USD 130.18 billion by 2034.

In 2025, the market value stood at USD 12.72 billion.

The market is expected to exhibit a CAGR of 24.98% during the forecast period of 2026-2034.

The usage-based segment led the market by service.

The key factors driving the market are rising electric vehicle (EV) adoption to propel the market growth.

Tesla Inc., BP Pulse, and Shell Recharge Solutions are some of the prominent players in the market.

Asia Pacific dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us