Chickpea Snacks Market Size, Share & Industry Analysis, By Product Type (Roasted Chickpeas, Puffed Chickpea Snacks, Chickpea Chips & Crisps, Chickpea-Based Crackers, Chickpea Snack Bars, and Others), By Form (Whole Chickpea Snacks and Flour-based Snacks), By Flavor (Spicy, Sweet, Salty, and Others), By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

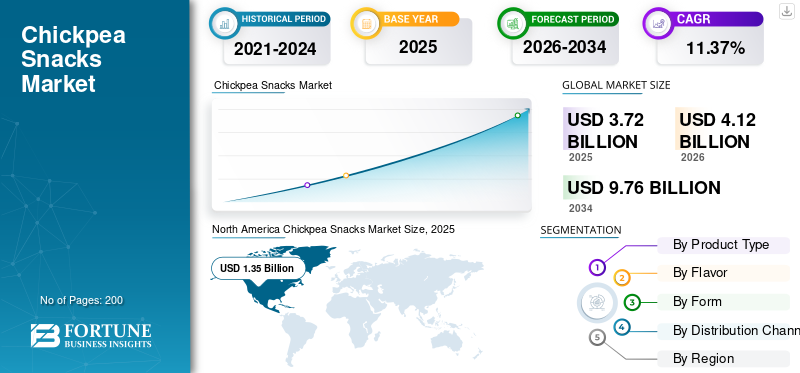

The global chickpea snacks market size was valued at USD 3.72 billion in 2025. The market is projected to grow from USD 4.12 billion in 2026 to USD 9.76 billion by 2034, exhibiting a CAGR of 11.37% during the forecast period. North America dominated the global chickpea snacks market with a market share of 36.3% in 2025.

Chickpea snacks, including roasted chickpeas, puffed or extruded formats, and chips, are gaining traction as a healthy snack category because chickpea-based products naturally align with health consciousness, gluten-free positioning, and “better-for-you” snack options built around plant-based protein and high protein and fiber claims. Demand acceleration is most visible in North America and the U.S., where mainstream snack aisles are expanding beyond corn and potato into legume-forward formats, while online retail continues to scale discovery and repeat purchase across niche flavors and functional variants.

The global chickpea snacks industry is dominated by major players, including Pepsico Inc., Nestle SA, General Mills, Kraft Heinz, and Kellogg's Company. These players focus on renovating core brands with legume-based line extensions, investing heavily in R&D for healthier formulations, and leveraging mass retail and convenience channels to achieve scale and trial.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Health Consciousness and “Better-for-You” Snacking to Drive Market Growth

The rising global emphasis on wellness and preventive nutrition is one of the primary forces driving the global chickpea snacks market growth. Consumers are increasingly substituting conventional salty snacks, typically high in saturated fats, sodium, and refined carbohydrates, with “better-for-you” alternatives that provide tangible functional and nutritional benefits. This shift has been particularly evident in North America and Western Europe, where clean-label, high-protein, and gluten-free snack formats have transitioned from niche health segments to mainstream retail categories.

- According to the National Institutes of Health (NIH), chickpeas, being naturally rich in plant-based protein (19–21%) and dietary fiber (17–18%), have become a preferred base ingredient for health-conscious consumers seeking satiety-enhancing, low-glycemic, and nutrient-dense snack options.

Market Restraints

Raw Material Volatility and Processing Costs to Impede Market Expansion

Taste, texture, and “beany” off-notes are among the primary sensory barriers limiting broader consumer acceptance and repeat purchase of chickpea snacks, especially in more mainstream snacking occasions. “Beany” off-notes in chickpea snacks typically present as earthy, grassy, green, bitter, or lingering legume-like flavors driven largely by oxidation of unsaturated fatty acids and associated volatile compounds. These notes become more pronounced as pulse content and protein concentration increase. They can clash with familiar snack flavor profiles, such as those of cheese, barbecue, or sweet coatings. Chickpea flours and proteins have high water absorption and different pasting and structural properties than cereal flours. This can lead to dense, hard, dry, or overly brittle textures in extruded or baked snacks. Mass-market consumers are accustomed to neutral-tasting, crisp, and starch-based snacks. If not carefully formulated it can lead to unexpected beany flavors, bitterness, aftertastes, or chalky/dry mouthfeel. This may trigger trial rejection and negative word-of-mouth, thereby constraining chickpea snacks largely to health- or protein-focused niches.

Market Opportunities

Expansion Through Online Retail and D2C Models to Unlock New Growth Opportunities

Online retail and direct-to-consumer (D2C) models drive significant growth in the global market by enhancing accessibility, enabling niche branding, and supporting personalized sales amid rising e-commerce adoption. D2C strategies enable brands to bypass intermediaries, establish direct customer relationships, and collect data for targeted marketing through social media and influencer partnerships. Smaller producers leverage DTC websites and subscriptions to reach global audiences with unique flavors, clean labels, and sustainable packaging, democratizing competition against larger players. Examples include brands such as Hippeas and Biena expanding via online-exclusive launches and DTC expansions into new regions.

- For instance, in March 2021, HIPPEAS, a plant-based snacks manufacturer made from chickpeas and yellow peas, launched its direct-to-consumer e-commerce site at HIPPEAS.com, to capitalize on surging online snack demand amid pandemic-driven shifts in retail.

Chickpea Snacks Market Trends

Growing Penetration in the Plant-Based and Vegan Food Space to Shape Market

The growing penetration of plant-based and vegan diets is driving significant expansion in the global market, fueled by the high protein and fiber content of chickpeas, which serve as a healthy, gluten-free alternative to traditional snacks. The demand for plant-based proteins is propelling chickpea snacks, with consumers favoring nutrient-dense, gluten-free, and non-GMO options. Health consciousness boosts adoption among vegetarians and those reducing meat intake, while innovations such as flavored roasted chickpeas expand appeal.

- According to the Good Food Institute, in 2022, the U.S. plant-based food retail market reached USD 8 billion in sales, representing a 6.6% year-over-year growth.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Wide Acceptance, Minimal Processing, and Lower Production Cost Make Roasted Chickpeas Dominant Snack

By product type, the market segments include roasted chickpeas, puffed chickpea snacks, chickpea chips & crisps, chickpea-based crackers, chickpea snack bars, and others.

Roasted chickpeas held the dominant chickpea snacks market share in 2025 at USD 0.45 billion. It is the most established and widely accepted format of chickpea-based snacks across global markets. They require minimal processing, which keeps production costs lower and enables competitive pricing compared to other types. Since the product offering includes whole, natural, high-protein, and high-fiber snacks with fewer additives, it is emerging strongly among health-conscious consumers. Additionally, they offer high flavor versatility, such as spicy, salty, sweet, and other regional seasonings, while maintaining a familiar “snackable” texture, supporting broad adoption across all retail channels.

The chickpea snack bars segment is expected to grow significantly during the forecast period, with a CAGR of 13.12% from 2026 to 2034.

To know how our report can help streamline your business, Speak to Analyst

By Flavor

Wide Acceptability of Salt Flavored Snacks Drives its Top Position

On the basis of flavor, the market is segmented into spicy, sweet, salty, and others.

The salty segment dominated the market with USD 1.78 billion in 2025, driven by the familiar and universally accepted taste in savory snacking. The salty formulations are cost-effective, easy to scale, and carry minimal flavor risk. In addition, salted variants serve as a base for flavor innovations, enabling brands to expand their portfolios. Thus, the segment is anticipated to grow at a CAGR of 11.33% during the forecast period.

The spicy segment is expected to grow significantly at a CAGR of 12.90% during the forecast period.

By Form

Less-Processed and Clean-Label Trend Drive the Whole Chickpea Snacks Segment Growth

On the basis of form, the market is segmented into whole chickpea snacks and flour-based snacks.

In 2025, the whole chickpea snacks segment dominated USD 2.03 billion. These snacks are less processed, more natural, and nutritionally intact, aligning strongly with clean-label and health-driven purchasing behavior. Whole formats also preserve the chickpea’s inherent protein, fiber, and texture, delivering a more authentic and satisfying snack experience. The segment is anticipated to grow with a stable CAGR of 11.72% during the forecast period.

The flour-based snacks segment is expected to grow at a CAGR of 10.94% during the forecast period for the global chickpea snacks market.

By Distribution Channel

High Footfall and Brand Visibility Drive the Supermarkets & Hypermarkets Channel Growth

On the basis of distribution channel, the market is segmented into supermarkets & hypermarkets, convenience stores, specialty stores, online retail and others.

The supermarkets & hypermarkets distribution channel remains dominant with USD 1.99 billion in 2025. This channel benefits from high foot traffic, strong product visibility, and ample shelf space, which support impulse purchases and brand discovery. Consumers also prefer supermarkets for one-stop shopping, where chickpea snacks are placed alongside regular salty snacks, increasing trial and repeat buying.

The online segment is anticipated to grow at a CAGR of 15.57% during the forecast period.

Chickpea Snacks Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Chickpea Snacks Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America led the market with USD 1.35 billion in 2025 and is anticipated to grow at a 10.94% CAGR during the forecast period. The rising popularity for healthier, plant-based snack alternatives primarily drives the growth of chickpea snacks in North America. Consumers are increasingly seeking products that are high in protein and fiber, gluten-free, and made from recognizable ingredients, positioning chickpea snacks as a strong substitute for traditional fried snacks. The increasing demand for clean-label and vegan snacks is significantly influencing the growth of the North American market.

Europe

Europe is estimated to expand from an anticipated USD 1.21 billion in 2026 to USD 2.88 billion in 2034 at a CAGR of 11.49%. The emerging vegan population in Germany, France, Spain, and the U.K., is positively driving the demand for chickpea snacks in the region. Additionally, key brands are focusing on launching new products to capitalize on an emerging snack trend in the region. For instance, in May 2025, Gosh, a U.K.-based vegan snacks manufacturing company, launched Veg Bites snack packs to capitalize on the growing market for healthier snacking options. The newly launched snacks are made from a blend of baked sweet potato, chickpeas, black beans, chipotle, harissa, and various herbs and spices.

Asia Pacific

Asia Pacific records the highest regional CAGR at 12.15%, growing from USD 0.96 billion in 2026 to USD 2.67 billion in 2034. Rapid urban growth and rising disposable incomes are increasing demand for on-the-go, packaged snacks with perceived health benefits. Consumers, particularly younger demographics, are showcasing strong interest in plant-based, protein-rich, and better-for-you snacks. Increasing chickpea production and the availability of raw materials are positively influencing market growth. Additionally, the expansion of modern retail and e-commerce platforms has significantly improved product accessibility across both developed and emerging markets in Asia Pacific.

South America

South America is projected to grow at a 11.37% CAGR, expanding from USD 0.20 billion in 2026 to USD 0.49 billion by 2034. The chickpea snack market in South America is primarily driven by growing health awareness and a gradual shift in dietary preferences away from traditional, carb-heavy snacks. Consumers are increasingly seeking affordable sources of plant protein and fiber, positioning chickpeas as a practical and nutritious option. In addition, the local availability of pulses and improvements in food processing capabilities are helping manufacturers introduce chickpea-based snacks at competitive price points.

Middle East & Africa

The Middle East & Africa market size is projected to increase from USD 0.12 billion in 2026 to USD 0.29 billion in 2034 at a 10.08% CAGR. In MEA, demand is strongly supported by deep cultural familiarity with chickpeas through traditional foods such as hummus and falafel, which encourages acceptance of snack formats. Rapid urbanization, a young population, and increasing preference for convenient yet healthy packaged foods are key growth drivers in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing New Product Launches by Major Companies Strengthen Market Presence

The global market is fragmented, comprising the presence of multiple players, including both local and international companies. Pepsico Inc., Nestle SA, General Mills, Kraft Heinz, and Kellogg's Company are key players that hold a strong presence in the global market. These players are focusing on new chickpea-based products, expanding their geographical presence, and engaging in mergers and acquisitions to enhance their presence in the competitive landscape.

Key Players in the Chickpea Snacks Market

|

Rank |

Company Name |

|

1 |

Pepsico Inc. |

|

2 |

Nestle SA |

|

3 |

General Mills |

|

4 |

Kraft Heinz Company |

|

5 |

Kellogg's Company |

List of Key Chickpea Snacks Companies Profiled

- PepsiCo, Inc. (U.S.)

- Nestle SA (Switzerland)

- The Good Bean (U.S.)

- Biena Snacks LLC (U.S.)

- Saffron Road (U.S.)

- Hippeas, Inc. (U.S.)

- General Mills Inc. (U.S.)

- Calbee Inc. (Japan)

- The Kellogg Company (U.S.)

- The Kraft Heinz Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Festive Chickpea Hearts, one of the chickpea snack brands, launched two new flavors - Nacho Cheese and White Cheddar, with more shareable pack sizes.

- November 2024: Origin Nutrition, an Indian-based company manufacturing high-protein snacks, launched high-protein, compression-popped pea-based chips made from a blend of chickpeas, peas, and pumpkin seeds. The newly launched products are available in Pudina chutney, Sour Cream & Onion, and Tomato flavors.

- July 2024: Nestle SA, one of the leading food and beverage companies, launched a new range of Wotsits and Monster Munch flavors made with chickpea, classifying them as non-high in fat, salt, and sugar (non-HFSS) under its Walkers brand.

- December 2023: PepsiCo Inc. launched new packaging for its chickpea crisp, featuring sea salt and Swiss cheese flavors. The new products are available on Tmall and in major convenience stores.

- October 2023: PepsiCo Inc., one of the leading beverage companies, launched Chickpea Crunch 2.0, featuring butter-fried matsutake flavor and black truffle flavor, under its Sunbites brand.

REPORT COVERAGE

The global chickpea snacks market research report provides in-depth analysis of the market, highlighting key aspects such as global market trends, market dynamics, prominent companies, research and development investments, and end-use applications. Besides this, the report also provides insights into the market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.37% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Flavor · Spicy · Sweet · Salty · Others |

|

|

By Form

|

|

|

By Distribution Channel · Supermarkets & Hypermarkets · Convenience Stores · Specialty Stores · Online Retail · Others |

|

|

By Region · North America (By Product Type, Form, Flavor, Distribution Channel, and Country) • U.S. (By Form) • Canada (By Form) • Mexico (By Form) · Europe (By Product Type, Form, Flavor, Distribution Channel, and Country) • Germany (By Form) • Spain (By Form) • Italy (By Form) • France (By Form) • U.K. (By Form) • Rest of Europe (By Form) · Asia Pacific (By Product Type, Form, Flavor, Distribution Channel, and Country) • China (By Form) • Japan (By Form) • India (By Form) • Australia (By Form) • Rest of Asia Pacific (By Form) · South America (By Product Type, Form, Flavor, Distribution Channel, and Country) • Brazil (By Form) • Argentina (By Form) • Rest of South America (By Form) · Middle East & Africa (By Product Type, Form, Flavor, Distribution Channel, and Country) • South Africa (By Form) • UAE (By Form) • Rest of the MEA (By Form) |

Frequently Asked Questions

Fortune Business Insights says that the global market was at USD 3.72 billion in 2025 and is anticipated to reach USD 9.76 billion by 2034.

The global market will exhibit a steady CAGR of 11.37% over the forecast period.

By product type, the roasted chickpeas segment leads the market.

North America held the largest market share in 2025.

Rising health consciousness and “better-for-you” snacking to drive market growth.

Pepsico Inc., Nestle SA, General Mills, Kraft Heinz, and Kelloggs Company are the leading companies in the market.

Growing penetration in the plant-based and vegan food market to shaping the market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us