Chiplets Market Size, Share & Industry Analysis, By Packing Technology (2.5D/3D, Flip Chip Chip Scale Package (FCCSP), Flip Chip Ball Grid Array (FCBGA), Fan-Out (FO), System-in-Package (SiP), and Wafer-Level Chip Scale Package WLCSP)), By Processor (Central Processing Unit (CPU), Graphics Processing Unit (GPU), Application Processing Unit (APU), Artificial Intelligence Processor-specific Integrated Circuit (AI ASIC) Coprocessor, and Field Programmable Gate Array (FPGA)), By Application (Enterprise Electronics, Consumer Electronics, Automotive, & Others), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

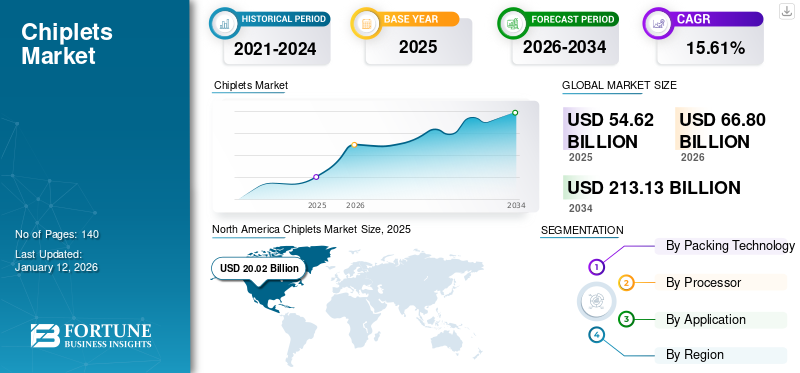

Chiplets Market Size and Future Outlook

The global chiplets market size was valued at USD 54.49 billion in 2025. The market is projected to grow from USD 66.61 billion in 2026 to USD 350.79 billion by 2034, exhibiting a CAGR of 23.1% during the forecast period. North America dominated the chiplets market with a market share of 36.70% in 2025.

The chiplets market is transitioning from monolithic system-on-chip design toward a modular semiconductor architecture built on interoperable silicon blocks that can be combined within a single package to deliver higher performance, flexibility, and faster product development cycles. The market growth is supported by increasing demand for high-performance computing, artificial intelligence, data centers, 5G infrastructure, and advanced automotive electronics, along with physical and economic limitations of traditional node scaling.

Customers are placing strong emphasis on bandwidth density, power efficiency, and seamless interoperability between heterogeneous dies manufactured on different process nodes. There is significant interest in advanced packaging approaches such as 2.5D and 3D integration, and open ecosystem frameworks that enable multi-vendor compatibility.

Major semiconductor and packaging providers such as Advanced Micro Devices, Intel, Taiwan Semiconductor Manufacturing Company, Samsung Electronics, NVIDIA, and Broadcom are strengthening their competitive position by investing in advanced packaging platforms, high-speed interconnect technologies, and open chiplet ecosystems.

Download Free sample to learn more about this report.

Chiplets Market Key Takeaways

- 2025 Market Size: USD 54.49 billion

- 2026 Market Size: USD 66.61 billion

- 2034 Forecast Market Size: USD 350.79 billion

- CAGR: 23.1% from 2026–2034

- North America dominated the chiplets market with a 36.70% share in 2025.

- The 2.5D/3D segment is expected to hold a 33.00% market share in 2026.

- The CPU segment is projected to account for 30.02% market share in 2026.

North America

North America held a 36.66% share in 2025, valued at USD 20.02 billion.

Asia Pacific

Asia Pacific accounted for 31.82% share in 2025, valued at USD 17.38 billion.

Europe

Europe contributed 20.70% share in 2025, valued at USD 11.31 billion.

U.S.

The U.S. market reached USD 14.33 billion in 2025, driven by strong AI chip and hyperscale data center demand.

Japan

The Japan market accounted for USD 3.99 billion in 2025, supported by advanced semiconductor packaging and automotive processor development.

Read More

Generative-AI Impact

Advanced Capabilities and Accelerated Development of AI Applications for Chiplets Fueled Market Growth

Generative AI is significantly influencing the development and application of chiplet technology, reshaping how semiconductor designs are approached. Chiplets allow for the creation of more powerful AI chips by breaking down complex functionalities into smaller, specialized modules. This modular approach enables manufacturers to optimize performance by selecting the best chiplets for specific tasks, thereby enhancing design flexibility and reducing costs associated with traditional monolithic designs.

Moreover, the integration of chiplet technology is crucial for accelerating generative AI applications, particularly in edge computing. By facilitating faster data processing and reducing latency, chiplets enable more efficient deployment of AI models in various sectors. This is particularly relevant as the demand for real-time data processing grows. Due to the rising demand for AI chips, experts in the industry are predicting substantial growth in the High-Bandwidth Memory (HBM) sector, with an estimated increase of 331% this year and 124% in 2025, according to an industry analyst.

Chiplets Market Trends

Growing High-Bandwidth Memory Integrations to Fuel the Market Expansion

The growing integration of high-bandwidth memory is becoming a major trend for chiplets market growth as compute-intensive workloads increasingly demand faster and more energy-efficient data movement. Chiplet architectures enable memory to be placed closer to compute dies using advanced packaging, significantly reducing latency and power consumption associated with off-chip memory access.

As compute scales across multiple chiplets, shared high-bandwidth memory pools enable better workload balancing and utilization. This design flexibility allows vendors to tailor memory capacity and bandwidth independently from compute logic, accelerating product customization. For Instance,

- Nvidia’s Rubin platform development blog talks about six new chips and a coordinated multi-chiplet design to power next-generation AI infrastructure, reflecting the industry shift toward modular compute and memory architectures that enable better utilization and workload distribution.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Innovation of Thermal and Power Management Fuels the Market Growth

Increasing innovation in thermal and power management is becoming a critical enabler for chiplet market development as multi-die architectures push power density far beyond traditional packaging limits. Advanced thermal interface materials, integrated heat spreaders, and localized cooling solutions are allowing densely packed chiplets to operate at higher sustained performance without throttling. Power delivery innovations such as distributed voltage regulation and optimized power routing across chiplets are reducing IR drop and improving energy efficiency at the system level. For instance,

- In May 2025, Marvell launched a multi-die packaging platform for custom AI accelerators that explicitly addresses power consumption and thermal handling, emphasizing improved die-to-die interconnect efficiency and system power performance.

These improvements make it feasible to scale compute-intensive workloads while maintaining reliability and long-term performance stability.

MARKET RESTRAINTS

Dependence on Advanced Manufacturing Infrastructure Hampers the Market Expansion

Dependence on advanced manufacturing infrastructure significantly hampers the expansion of the chiplets market by concentrating critical capabilities within a limited set of global players.

Chiplet architectures rely heavily on cutting-edge foundries, advanced packaging lines, and specialized OSAT facilities that support 2.5D and 3D integration. Limited availability of these facilities creates capacity bottlenecks, delaying production timelines and increasing costs. The need for highly specialized equipment and process expertise raises entry barriers for smaller semiconductor firms and new market entrants.

In addition, tight coupling between wafer fabrication and back-end packaging requires close coordination across the supply chain, increasing operational complexity and execution risk. Geopolitical factors and regional manufacturing imbalances further amplify vulnerability to disruptions. As a result, market expansion remains constrained by infrastructure readiness rather than end-market demand, slowing broader adoption of chiplet-based architectures.

MARKET OPPORTUNITIES

Increasing Ecosystem Expansion and Partnership Models Create Significant Opportunities for the Market

The increasing expansion of the chiplet ecosystem and the rise of partnership-driven models are creating significant growth opportunities by lowering adoption barriers and accelerating innovation. Collaboration among fabless companies, foundries, OSATs, EDA vendors, and IP providers is enabling more integrated and efficient design-to-manufacturing workflows. These partnerships reduce integration complexity by aligning chiplet design rules, packaging requirements, and validation processes early in the development cycle.

As ecosystems mature, reusable chiplet IP and reference platforms are emerging, allowing companies to shorten development timelines and reduce engineering risk. Cross-industry collaboration also encourages interoperability, supporting multi-vendor sourcing strategies and improving supply chain resilience. For instance,

- In January 2026, Cadence announced a chiplet ecosystem with IP partners including Arm, Arteris, and others to provide pre-validated chiplet solutions and simplify design workflows. This will directly address engineering risk and interoperability barriers.

Segmentation Analysis

By Packaging Technology

Rising Deployment of 2.5D/3D Packing Technology to Propel Segmental Growth

Based on the packaging technology, the market is divided into 2.5D/3D, Flip Chip Chip Scale Package (FCCSP), Flip Chip Ball Grid Array (FCBGA), Fan-Out (FO), System-in-Package (SiP), and Wafer-Level Chip Scale Package (WLCSP).

2.5D/3D accounted for the largest market share as it enables direct integration of compute chiplets with high bandwidth memory, which is essential for AI training and hyperscale data center processors. Technologies such as CoWoS and Foveros support high density and are already used in commercial products from NVIDIA and Intel. These approaches also improve yield economics by allowing smaller dies to be combined instead of producing large monolithic chips at advanced nodes. The 2.5D/3D segment is expected to lead the market, contributing 33.00% globally in 2026.

Fan-out (FO) is anticipated to rise with a CAGR of 26.2% over the forecast period, owing to its ability to provide lower-cost heterogeneous integration for chiplets that do not require silicon interposers. It is increasingly used for integrating I O dies, edge AI processors, and automotive chiplets where cost and volume are key factors. Panel-level fan-out manufacturing also enables higher production efficiency and better scalability.

By Processor

Early and Large-Scale Adoption of Chiplet Architecture in Server to Propel Central Processing Unit Segment’s Growth

Based on the processor, the market is divided into Central Processing Unit (CPU), Graphics Processing Unit (GPU), Application Processing Unit (APU), Artificial Intelligence Processor-specific Integrated Circuit (AI ASIC) Coprocessor, Field Programmable Gate Array (FPGA).

Central Processing Unit (CPU) accounted for the largest market share, mainly due to early and large-scale adoption of chiplet architecture in server and data center processors to improve core scalability and manufacturing efficiency. Leading vendors such as Advanced Micro Devices and Intel have widely implemented chiplet-based CPUs to increase core counts while maintaining acceptable yield at advanced nodes. This approach allows separation of compute and I/O dies, enabling optimization across different process technologies. The central processing unit (CPU) segment will account for 30.02% market share in 2026.

Artificial Intelligence Processor-specific Integrated Circuit (AI ASIC) Coprocessor is anticipated to rise with a CAGR of 27.7% over the forecast period, driven by increasing deployment of custom AI accelerators designed using chiplet-based architectures for training and inference workloads. Companies such as NVIDIA and Broadcom are developing modular AI processors to improve performance scalability and integrate high-bandwidth memory efficiently.

By Application

To know how our report can help streamline your business, Speak to Analyst

Large-Scale Deployment of Chiplets across Enterprise Electronics to Propel Segmental Growth

Based on the application, the market is divided into enterprise electronics, consumer electronics, automotive, industrial automation, military & aerospace, and others (healthcare, etc.).

Enterprise electronics accounted for the largest market share, mainly due to the extensive adoption of chiplet-based processors in data centers, cloud infrastructure, and networking equipment to achieve higher compute density and scalability. Major cloud and processor providers, including Intel and Advanced Micro Devices, have already deployed chiplet-based server CPUs and accelerators. This architecture also allows faster product upgrades by reusing existing chiplets across multiple platforms. Growing hyperscale data center expansion continues to drive strong demand from this segment. The enterprise electronics segment is expected to account for 27.42% of the market in 2026.

The automotive segment is anticipated to rise with a CAGR of 26.3% over the forecast period, driven by increasing semiconductor requirements for autonomous driving, advanced driver assistance systems, and software-defined vehicle platforms. Chiplets enable integration of AI accelerators, sensor processors, and connectivity components within a single package, improving performance and reducing system complexity

Chiplets Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Chiplets Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 20.02 billion in 2025, representing 36.66% of the global market share, and is projected to reach USD 24.35 billion in 2026. The market growth in North America is driven by the strong presence of major processor and AI chip developers such as Intel, Advanced Micro Devices, and NVIDIA. The region benefits from high demand for chiplet-based processors across hyperscale data centers, artificial intelligence infrastructure, and cloud computing. In addition, significant investments in advanced packaging, heterogeneous integration, and domestic semiconductor manufacturing are accelerating innovation

U.S Chiplets Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market led the revenue of USD 14.33 billion in 2025, accounting for roughly 26.0% of global sales.

Asia Pacific

In 2025, Asia Pacific held 31.82% of the global market, reaching a valuation of USD 17.38 billion, and is projected to grow to USD 21.42 billion in 2026. The region serves as a global hub for advanced packaging technologies, including 2.5D, 3D, and fan-out integration, which are essential for chiplet adoption. Increasing demand for AI processors, high-performance computing, and 5G infrastructure across China, Taiwan, South Korea, and Japan is further accelerating growth. In addition, a strong manufacturing ecosystem, skilled workforce, and continuous investments in semiconductor capacity expansion are supporting regional market expansion.

Japan Chiplets Market

The Japanese market in 2025 accounted for USD 3.99 billion, accounting for roughly 7.0% of global revenues. Japan’s market growth is attributed to a strong focus on advanced semiconductor packaging and next-generation processor development for automotive and industrial applications. Domestic companies such as Renesas Electronics and Sony Semiconductor Solutions are investing in heterogeneous integration to support AI, imaging, and automotive compute platforms.

China Chiplets Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at USD 6.13 billion, representing roughly 11% of global sales.

India Chiplets Market

India’s market in 2025 was valued at USD 2.33 billion, accounting for roughly 4% of global revenues.

Europe

The Europe market was valued at USD 11.31 billion in 2025, capturing 20.70% of global revenue, and is estimated to reach USD 13.95 billion in 2026. Europe is projected to record the highest growth rate of 25.8% in the coming years. This growth is owing to strong demand from electric vehicles, industrial automation, and AI-driven systems, which are accelerating adoption. Government initiatives under regional semiconductor programs and collaborations with global ecosystem partners are further supporting market expansion.

U.K Chiplets Market

The U.K. market in 2025 was valued at USD 2.42 billion, representing roughly 4.0% of global revenues.

Germany Chiplets Market

Germany’s market is projected to reach approximately USD 2.20 billion in 2025, equivalent to around 4.0% of global sales.

Rest of The World

The South America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The South America market reached a valuation of USD 1.95 billion in 2025. The South America and Middle East & Africa market growth is owing to the expansion of 5G networks, which is creating demand for advanced networking and edge processors, where chiplets help improve performance and reduce power consumption. Middle East & Africa contributed approximately USD 3.94 billion to the global market in 2025, accounting for 7.22% share, and is expected to reach USD 4.74 billion in 2026. In the Middle East & Africa, the GCC accounted for a value of USD 1.49 billion in 2025. The Latin America region captured 3.59% of the global market in 2025, generating USD 1.96 billion in revenue, and is projected to reach USD 2.34 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Companies Expanding Advanced Packaging Capacity and Forming Strategic Ecosystem Alliances to Reinforce Competitive Advantage

Chiplet industry participants are prioritizing the expansion of advanced packaging and heterogeneous integration capabilities to support increasing demand from AI, data center, and high-performance computing applications. Major manufacturers are scaling technologies such as 2.5D interposer and 3D stacking by setting up new packaging lines and enhancing backend integration facilities. For instance, Taiwan Semiconductor Manufacturing Company and Samsung Electronics are increasing their advanced integration capacity to support next-generation processors. This approach helps reduce supply constraints and ensures timely delivery for large-volume computing programs.

Companies are also entering long-duration ecosystem partnerships with processor vendors, cloud providers, and packaging specialists to ensure stable business flow and technology alignment.

LIST OF KEY CHIPLETS COMPANIES PROFILED

- Intel Corporation (U.S.)

- Advanced Micro Devices, Inc. (AMD) (U.S.)

- NVIDIA Corporation (U.S.)

- Taiwan Semiconductor (Taiwan)

- ASE Group (Taiwan)

- GlobalFoundries (U.S.)

- Synopsys, Inc. (U.S.)

- Broadcom, Inc. (U.S.)

- Marvell (U.S.)

- Samsung (South Korea)

- IBM Corporation (U.S.)

- Amkor Technology (U.S.)

- Arm (U.S.)

- ASMPT (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Cadence partnered with Arm, Samsung Foundry, Arteris, eMemory, M31, Silicon Creations, Trilinear, and ProteanTecs to launch a Chiplet Spec-to-Packaged Parts ecosystem, aiming to simplify chiplet development and speed time to market for physical AI, data center, and HPC applications.

- December 2025: Intel showcased a conceptual extreme multi-chiplet processor package that could scale to 12× the size of today’s largest AI chips, integrating up to 16 compute chiplets, 24 HBM5 stacks, and multiple base dies using advanced 2.5D and 3D packaging.

- October 2025: GlobalFoundries joined imec’s Automotive Chiplet Program as a key foundry partner, alongside companies including Infineon and STATS ChipPAC. The program aims to accelerate chiplet-based architectures for next-generation, software-defined vehicles, addressing the limits of traditional monolithic chips.

- October 2025: Marvell acquired Celestial AI to accelerate its chiplet-based connectivity strategy for next-generation AI data centers. The deal adds Celestial AI’s Photonic Fabric optical chiplet technology, enabling high-bandwidth, low-latency optical I/O that can be co-packaged with XPUs and switches.

- April 2025: TSMC revealed plans to support extreme multi-chiplet processors using next-generation CoWoS and 3DFabric packaging, enabling assemblies up to 9.5× reticle size on very large substrates. These chiplet-based designs could deliver up to 40× the performance of standard processors while consuming around 1,000W, integrating multiple logic dies.

REPORT COVERAGE

The global chiplets market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 23.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Packing Technology, By Processor, By Application, and Region |

| By Packing Technology |

|

| By Processor |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 54.49 billion in 2025 and is projected to reach USD 350.79 billion by 2034.

In 2025, the market value stood at USD 20.00 billion.

The device market is expected to exhibit a CAGR of 23.1% during the forecast period.

By application, the enterprise electronics is expected to lead the market.

Increasing Innovation of Thermal and Power Management Fuels the Market Growth

Intel, AMD, Taiwan Semiconductor, and IBM Corporation are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us