Cholangiocarcinoma Drugs Market Size, Share & Industry Analysis, By Therapy (Chemotherapy, Immunotherapy, Targeted Therapy, & Others), By Drug Class (Antimetabolites, Platinum Compounds, PD-L1 Inhibitors, FGFR Inhibitors, IDH1 Inhibitors, PD-1 Inhibitors, & Others), By Disease Indication (Intrahepatic Cholangiocarcinoma, Perihilar Cholangiocarcinoma, Distal Cholangiocarcinoma, Advanced/Recurrent Cholangiocarcinoma, & Others), By Age Group (Pediatric & Adult), By Type (Branded & Generic), By Route of Administration (Oral & Parenteral), By Distribution Channel, and Regional Forecast, 2026-2034

Cholangiocarcinoma Drugs Market Size and Future Outlook

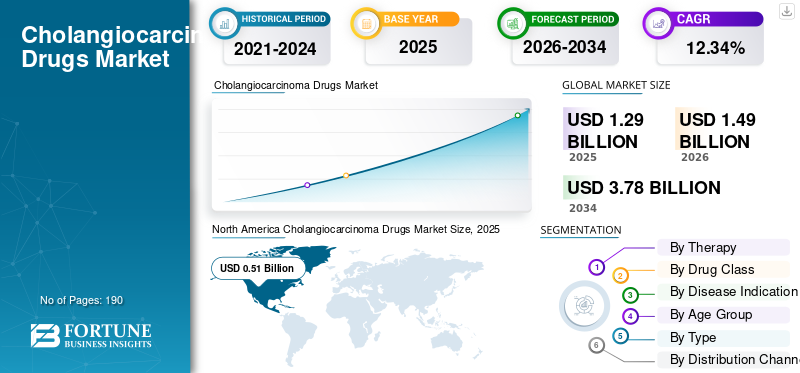

The global cholangiocarcinoma drugs market size was valued at USD 1.29 billion in 2025. The market is projected to grow from USD 1.49 billion in 2026 to USD 3.78 billion by 2034, exhibiting a CAGR of 12.34% during the forecast period. North America dominated the cholangiocarcinoma drugs market with a market share of 39.53% in 2025.

The global cholangiocarcinoma drugs market is anticipated to grow steadily over the forthcoming years. The rising clinical focus on rare and aggressive biliary tract cancers drives the market growth. Also, the growing use of biomarker-based treatment approaches supports the market's overall expansion. As more patients undergo genomic profiling, the demand for targeted therapies that address specific alterations such as FGFR2 fusions, IDH1 mutations, and HER2 expression is also increasing. These factors are improving treatment personalization and expanding the commercial opportunity beyond traditional chemotherapy. Additionally, updated clinical guidance for biliary tract cancers continues to support the use of newer systemic and precision-led treatment options, which are helping strengthen market expansion.

Key companies operating in the market are increasingly focusing on improving access to these drugs and on regulatory approvals and reimbursements.

- For instance, in February 2026, Partner Therapeutics, Inc. (PTx) received Orphan Drug Designation (ODD) from the U.S. FDA for zenocutuzumab‑zbco for the treatment of adults with advanced unresectable or metastatic cholangiocarcinoma. Zenocutuzumab-zbco is being developed in a subset of patients with cholangiocarcinoma harboring a neuregulin 1 (NRG1) gene fusion.

Furthermore, leading players in the industry, such as Incyte, Innovent Biologics, Servier, and Taiho Pharmaceutical, are focusing on research and development and expanding their offerings to strengthen their market positions.

Download Free sample to learn more about this report.

Cholangiocarcinoma Drugs Market Key Takeaways

- 2025 Market Size: USD 1.29 billion

- 2026 Market Size: USD 1.49 billion

- 2034 Forecast Market Size: USD 3.78 billion

- CAGR: 12.34% from 2026–2034

- North America dominated the cholangiocarcinoma drugs market with a 39.53% share in 2025.

- The immunotherapy segment is projected to grow at a 26.01% CAGR during the forecast period.

- The PD-L1 inhibitors segment is expected to expand at a 41.88% CAGR over the forecast period.

North America

North America led the market with USD 0.51 billion in 2025.

Europe

Europe is projected to reach USD 0.37 billion in 2026 at a 10.78% CAGR.

Asia Pacific

Asia Pacific is estimated to reach USD 0.40 billion in 2026.

U.S

The market is estimated at USD 0.54 billion in 2026, accounting for 36.12% of global revenue.

Japan

The market is projected to reach USD 0.08 billion in 2026, representing 5.46% of global revenue.

Read More

CHOLANGIOCARCINOMA DRUGS MARKET TRENDS

Increasing Adoption of Biomarker-Driven Targeted Therapies is a Prominent Market Trend Observed

A significant global trend in the cholangiocarcinoma drugs market is the increasing adoption of biomarker-driven targeted therapies. This cancer includes patient subsets with distinct genomic alterations, such as FGFR2 fusions, IDH1 mutations, and HER2 expression. As molecular profiling becomes more widely used, physicians can identify eligible patients more accurately and match them with targeted treatments, rather than relying solely on broad chemotherapy-based approaches. This improves treatment personalization, encourages pharmaceutical companies to invest in niche-targeted assets, and strengthens the commercial potential of precision oncology in cholangiocarcinoma.

- For instance, in January 2026, Elevar Therapeutics announced the submission of a New Drug Application to the U.S. FDA for lirafugratinib as a second-line treatment for cholangiocarcinoma. This highlights how companies are advancing highly selective, targeted therapies for biomarker-defined patient populations, which is expected to further strengthen the market's shift toward personalized treatment strategies.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Adoption of Precision Medicine in Cholangiocarcinoma Treatment to Drive Growth

The rising adoption of precision medicine is driving the cholangiocarcinoma drugs market growth since this disease has a meaningful subset of patients with targetable molecular alterations, especially FGFR2-driven disease. As genomic profiling becomes more integrated into clinical decision-making, physicians can identify suitable patients more accurately and use targeted therapies better aligned with tumor biology. This increases the clinical value of biomarker-led treatment, supports demand for specialized oncology drugs, and encourages companies to invest further in cholangiocarcinoma-focused pipelines. Because of this cause-and-effect shift, precision medicine is strengthening both treatment innovation and market growth in cholangiocarcinoma drugs.

- For instance, in December 2024, Relay Therapeutics, Inc., a precision medicine company, partnered with Elevar Therapeutics, Inc., for lirafugratinib (RLY-4008). Lirafugratinib is a selective, oral small-molecule inhibitor of fibroblast growth factor receptor 2 (FGFR2) being developed for patients with FGFR2-driven cholangiocarcinoma (CCA) and other FGFR2-altered solid tumors.

- Similarly, in February 2025, Gilead Sciences, Inc. received conditional marketing authorization from EMA for seladelpar for the treatment of primary biliary cholangitis (PBC) in combination with ursodeoxycholic acid (UDCA) in adults who have an inadequate response to UDCA alone, or as monotherapy in those unable to tolerate UDCA.

MARKET RESTRAINTS

Small Patient Population Limits Commercial Potential, Hampering Market Growth.

The small patient population limits the market growth potential of the market because cholangiocarcinoma is a rare cancer, and, within that already limited population, only a subset of patients qualify for specific targeted treatments. This factor creates a challenge for the market, as fewer patients reduce the revenue potential of each therapy, and the narrow pool also slows clinical trial recruitment. As a result, companies may face longer development timelines, weaker commercial returns, and a limited incentive to expand aggressively in this indication compared with larger oncology markets. That is why the small patient population remains an important restraint on the growth of the market.

- For instance, in May 2024, the U.S. FDA issued a withdrawal notice for Truseltiq (infigratinib) stating that the sponsor requested withdrawal partly because of difficulties in recruiting and enrolling subjects for the required confirmatory trial in first-line cholangiocarcinoma, and because continued distribution in the second-line setting was not commercially reasonable. This highlights how the small and hard-to-enroll patient population can directly affect both clinical development and commercial viability in this market.

MARKET OPPORTUNITIES

New Regulatory Approvals Are Opening Treatment Segments, Offering Significant Market Growth Opportunities

New regulatory approvals are creating a major growth opportunity in the global market by expanding the number of patients who can be treated with newer branded therapies beyond traditional chemotherapy alone. As regulators approve more targeted, biomarker-defined treatments, physicians gain additional options for patients with specific molecular characteristics, thereby increasing treatment adoption and enhancing the market potential of precision oncology in this indication. These factors collectively encourage more companies to invest in rare biliary tract cancers, support follow-on clinical development, and strengthen the market's long-term commercial outlook. As a result, regulatory approval is becoming an important opportunity area for future market expansion.

- For instance, in November 2024, Jazz Pharmaceuticals received accelerated approval from the U.S. FDA for Ziihera (zanidatamab-hrii) for adults with previously treated, unresectable, or metastatic HER2-positive biliary tract cancer. This is important for the market because it shows that new approvals are opening additional biomarker-defined treatment segments within biliary tract cancers, thereby improving access to precision therapies and expanding revenue opportunities for companies operating in this space. Source: Jazz Pharmaceuticals / FDA.

MARKET CHALLENGES

High Treatment Costs Pose a Challenge for Market Growth

The global cholangiocarcinoma drugs market is advancing with the entry of targeted therapies and precision-led treatment options, but high treatment costs remain a major challenge for wider adoption. Because many newer therapies are developed for small biomarker-defined patient groups, their pricing is often high, which can create affordability and reimbursement pressure for healthcare systems. This can slow patient access, limit uptake in cost-sensitive markets, and make it harder for companies to achieve broad commercial expansion. As a result, treatment cost continues to be an important factor challenging the growth of the market.

- For instance, in February 2026, Springer Nature Link published an article titled 'Battle against time for innovative cancer treatment: an updated cost-effectiveness analysis of pemigatinib in intrahepatic cholangiocarcinoma' highlighted that pemigatinib was not cost-effective at its listing price for advanced intrahepatic cholangiocarcinoma, underscoring the pricing pressure surrounding targeted therapy adoption in this market. This shows how high therapy costs can become a direct barrier to reimbursement acceptance and wider patient access, especially in rare cancers where budget impact is closely scrutinized.

Segmentation Analysis

By Therapy

Wide Clinical Use of Chemotherapy for Cholangiocarcinoma to Lead the Segmental Growth

Based on the therapy, the market is categorized into chemotherapy, immunotherapy, targeted therapy, and others.

Among these, chemotherapy is estimated to dominate the market. Chemotherapy dominated the market as it is the foundational treatment approach for cholangiocarcinoma, especially in first-line and advanced disease settings. Since many patients are diagnosed when surgery is no longer possible, systemic therapy becomes the main treatment route, and chemotherapy has historically been the most broadly used option across the eligible patient pool. This wide clinical use has resulted in higher treatment volume and stronger revenue contribution than newer modalities, which are still limited to selected patient subgroups. Forgoing research and development in the region and an innovative pipeline further reinforces the segment's dominance.

- For instance, in July 2024, Lisata Therapeutics, Inc. announced promising preclinical results for its investigational candidate, certepetide (formerly LSTA1). The data presented showed that certepetide combined with standard-of-care chemotherapy and immunotherapy improved survival in mice with intrahepatic cholangiocarcinoma. These findings suggest potential benefits for human patients with this aggressive cancer and support advancing clinical development efforts for certepetide in intrahepatic cholangiocarcinoma.

The immunotherapy segment is expected to grow at a CAGR of 26.01% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Drug Class

Establishment of Antimetabolites in Standard Cancer Care to Drive Segmental Growth

Based on drug class, the market is segmented into antimetabolites, platinum compounds, PD-L1 inhibitors, FGFR inhibitors, IDH1 inhibitors, HER2-directed therapies, PD-1 inhibitors, and others.

In 2025, the antimetabolites segment dominated the market based on drug class. Antimetabolites, such as gemcitabine, remain among the most established and widely used components of cholangiocarcinoma therapy. As gemcitabine is used across standard chemotherapy regimens and in combination with newer agents, it continues to reach a larger patient population than many biomarker-specific drug classes. This has created a direct cause-and-effect advantage for antimetabolites; broader clinical applicability leads to greater utilization, supporting its larger share.

- For instance, in December 2022, AstraZeneca announced that Imfinzi plus chemotherapy was approved in the EU for first-line treatment of adult patients with unresectable or metastatic biliary tract cancer, with the chemotherapy regimen specifically including gemcitabine plus cisplatin. This shows that antimetabolite-based therapy remains deeply embedded in new treatment approvals, supporting continued segment dominance.

The PD-L1 inhibitors segment is projected to grow at a CAGR of 41.88% during the forecast period.

By Disease Indication

Increasing Disease Burden of Advanced/Recurrent Cholangiocarcinoma to Lead Growth in the Segment

Based on disease indication, the market is segmented into intrahepatic cholangiocarcinoma, perihilar cholangiocarcinoma, distal cholangiocarcinoma, advanced/recurrent cholangiocarcinoma, and others.

In 2025, the advanced/recurrent cholangiocarcinoma dominated the market share because a large share of patients is identified only after the disease has progressed beyond the point of curative surgery. When diagnosis happens late, or recurrence develops after initial treatment, patients move into systemic therapy pathways that drive most drug spending in the market. This late-stage presentation increases demand for drug-based management, and that higher treatment intensity translates into greater market value for the advanced/recurrent segment. As a result, advanced and recurrent disease continues to account for the largest share of cholangiocarcinoma drug demand. Recent regulatory approvals for the indication highlight the growing demand.

- For instance, in November 2024, Jazz Pharmaceuticals received accelerated approval from the U.S. FDA for Ziihera for adults with previously treated, unresectable, or metastatic HER2-positive biliary tract cancer. This directly reflects the market's strong concentration in advanced and previously treated diseases, where systemic drug therapy is most actively used.

In addition, the intrahepatic cholangiocarcinoma segment is projected to grow at a CAGR of 14.21% during the study period.

By Age Group

Large Adult Patient Pool Drives Higher Treatment Demand to Drive Segmental Growth

Based on age group, the market is segmented into pediatric and adult.

Based on the age group, the adult segment accounted for the largest cholangiocarcinoma drugs market share. Adult cases occur predominantly in older populations, while pediatric cases remain very rare. Since most diagnosed patients are adults, nearly all approved therapies, clinical studies, and treatment pathways are designed for adults. This larger patient pool drives higher treatment demand, leading to a much greater share of overall market revenue. Key companies also strategize to launch innovative products and their consecutive approvals from the respective regulatory bodies to monetize their growth potential.

- For instance, in September 2022, Taiho Oncology announced the U.S. FDA approval of LYTGOBI for adult patients with previously treated, unresectable, locally advanced, or metastatic intrahepatic cholangiocarcinoma with FGFR2 fusions or rearrangements. This shows how product approvals in this market are primarily focused on adult patients, reinforcing the dominance of the adult age segment.

In addition, the pediatric segment is projected to grow at a CAGR of 15.09% during the study period.

By Type

Higher Revenue Generation Potential of Branded to Boost the Segment Growth

Based on type, the market is segmented into branded and generic products.

Based on type, branded drugs dominated the market. The cholangiocarcinoma treatment market is increasingly driven by newer targeted therapies, immunotherapies, and specialty oncology products marketed under proprietary brands. Since this is a rare and biomarker-driven cancer setting, many of the most important therapies are still under exclusivity and do not yet face broad generic competition. These factors result in innovation remaining concentrated in branded products and capturing a larger share of market revenue.

- For instance, in August 2022, Incyte announced FDA approval of Pemazyre, which the company described as the targeted treatment for adults with previously treated, unresectable, locally advanced, or metastatic cholangiocarcinoma with an FGFR2 fusion or rearrangement. Such approvals strengthen the branded drug segment by introducing differentiated products with limited direct generic substitution in a rare oncology market.

In addition, the generic segment is projected to grow at a CAGR of 6.55% during the study period.

By Route of Administration

Higher Revenue Generation Potential of Branded to Boost the Segment Growth

Based on route of administration, the market is segmented into oral and parenteral.

Based on route of administration, the parenteral segment dominated the market. Cholangiocarcinoma treatment has relied on intravenous chemotherapy-based regimens for a long time, and newer immunotherapy and antibody-based treatments are also largely delivered through infusion. This creates a market pattern: when the standard of care centers on hospital-administered IV therapy, a larger share of patients receive treatment via parenteral routes, leading to higher utilization and revenue for this segment. In addition, patients with advanced biliary tract cancer often require closely monitored treatment in specialist oncology settings, further reinforcing the dominance of parenteral administration over oral alternatives.

- For instance, in April 2024, AstraZeneca announced that Imfinzi plus chemotherapy delivered updated long-term survival benefit in the TOPAZ-1 Phase III trial for patients with advanced biliary tract cancer. The development supports the dominance of the parenteral segment, as both Imfinzi and the backbone chemotherapy used in this setting are administered by infusion, underscoring that major treatment advances in the market continue to be built around parenteral therapy.

In addition, the oral segment is projected to grow at a CAGR of 18.27% during the study period.

By Distribution Channel

Large Patient Volumes to Drive Demand in Hospital Pharmacies, Propelling Growth in the Segment

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

By distribution channel, the hospital pharmacies segment is estimated to dominate the market. Hospital pharmacies dominated the market because cholangiocarcinoma treatment is commonly managed in specialist oncology settings, where patients require multidisciplinary care, biomarker testing, infusion support, and close monitoring for adverse events. Many important therapies in this market are used in advanced cancer care pathways, which are centered in hospitals and large cancer centers rather than in routine retail channels. This specialist-led administration and monitoring increase hospital-based dispensing, which drives a higher share of product flow through this channel.

- For instance, in December 2024, Jazz Pharmaceuticals announced that Ziihera was included in the NCCN Guidelines and was commercially available in the U.S. as an intravenous therapy for eligible patients with biliary tract cancer. This underscores the importance of hospital-centered distribution, as intravenous oncology products for advanced BTC are typically handled through specialist hospital and cancer center channels.

The online pharmacies segment is projected to grow at a CAGR of 19.38% over the study period.

Cholangiocarcinoma Drugs Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cholangiocarcinoma Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.43 billion and maintained its leading position in 2025 at USD 0.51 billion. The market is growing in North America because the region has stronger access to biomarker testing, specialist cancer centers, and recently approved biliary tract cancer therapies. This improves the identification of eligible patients and supports faster uptake of targeted, branded, and immunotherapy-based treatments.

U.S. Cholangiocarcinoma Drugs Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 0.54 billion by 2026, accounting for roughly 36.12% of the global market.

Europe

Europe is projected to grow at a CAGR of 10.78% over the coming years, the second-highest among all regions, and projected to reach a valuation of USD 0.37 billion by 2026. The market is growing in Europe because biliary tract cancers are showing increasing incidence in the region, while precision-medicine networks and clinical trials are improving access to more personalized treatment strategies. This is strengthening demand for newer cholangiocarcinoma therapies beyond standard chemotherapy alone.

U.K. Cholangiocarcinoma Drugs Market

The U.K. market is estimated at around USD 0.05 billion in 2026, representing roughly 3.64% of the global market.

Germany Cholangiocarcinoma Drugs Market

Germany's market is projected to reach approximately USD 0.07 billion in 2026, equivalent to around 4.45% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.40 billion in 2026 and secure the position of the third-largest region in the market. The market is growing fastest in the Asia Pacific because the cholangiocarcinoma burden is higher in many Asian populations, especially in parts of East and Southeast Asia. The large patient pool, together with rising research activity and growing use of molecularly guided treatment, is creating stronger demand for advanced therapies.

Japan Cholangiocarcinoma Drugs Market

The Japanese market in 2026 is estimated at around USD 0.08 billion, accounting for approximately 5.46% of the global market.

China Cholangiocarcinoma Drugs Market

China's market is projected to be one of the largest worldwide, with 2026 revenues expected to hit USD 0.14 billion, representing approximately 9.21% of global sales.

India Cholangiocarcinoma Drugs Market

The Indian market in 2026 is estimated at around USD 0.04 billion, accounting for roughly 2.92% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.08 billion in 2026. The market is growing in Latin America because a meaningful number of patients still present with advanced disease, which increases the need for systemic drug treatment. In the Middle East & Africa, the GCC is set to reach USD 0.02 billion in 2026.

South Africa Cholangiocarcinoma Drugs Market

The South African market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 0.69% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations and Emphasis on Research and Development by Key Players to Propel Market Progress

The global cholangiocarcinoma drugs market is highly consolidated, with companies such as Incyte, Innovent Biologics, Servier, Taiho Pharmaceutical, Jazz Pharmaceuticals, and AstraZeneca holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in October 2025, Incyte announced the first clinical data evaluating its TGFβR2×PD-1 bispecific antibody (INCA33890) for patients with microsatellite stable (MSS) colorectal cancer; and its potent, selective, and orally bioavailable KRAS G12D inhibitor (INCB161734) for patients with KRAS G12D mutations, specifically pancreatic ductal adenocarcinoma (PDAC). Such strategic initiatives aim to elevate adoption and drive growth in the global market.

Other notable players in the global market include Merck & Co., Inc., Relay Therapeutics, and Elevar Therapeutics. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period for the global market.

LIST OF KEY CHOLANGIOCARCINOMA DRUGS COMPANIES PROFILED

- Incyte (U.S.)

- Innovent Biologics (China)

- Servier (France)

- Taiho Pharmaceutical (Japan)

- Jazz Pharmaceuticals (Ireland)

- AstraZeneca (U.K.)

- Merck & Co., Inc., (U.S.)

- Relay Therapeutics (U.S.)

- Elevar Therapeutics (U.S.)

- Eisai Inc. (Japan)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Innovent Biologics, Inc. collaborated with Eli Lilly and Company to advance novel medicines in oncology and immunology. This agreement marked the seventh collaboration between the two companies, deepening a longstanding and productive partnership to deliver new medicines for patients worldwide.

- October 2025: Takeda Pharmaceutical Company Limited collaborated with Innovent Biologics to develop, manufacture, and commercialize two late-stage oncology medicines, IBI363 and IBI343, worldwide outside of Greater China.

- June 2025: Servier India, an affiliate of the France-based Servier Group, launched Ivosidenib (Tibsovo)—a precision, oral therapy, approved for the treatment of patients with IDH1-mutated Acute Myeloid Leukemia (AML) and Cholangiocarcinoma. The milestone marks a critical step in expanding access to targeted cancer therapies in India, particularly for rare and underserved cancer populations.

- September 2024: Lisata Therapeutics, Inc. received Orphan Drug Designation from the U.S. FDA to certepetide for the treatment of cholangiocarcinoma. Lisata is currently evaluating certepetide in its BOLSTER trial, a Phase 2a, randomized study in the U.S. for the treatment of first- and second-line cholangiocarcinoma.

- December 2024: Relay Therapeutics, Inc. collaborated with Elevar Therapeutics, Inc., to elevate treatment outcomes for patients with limited or inadequate therapeutic options using lirafugratinib (RLY-4008). Lirafugratinib is a selective, oral small-molecule inhibitor of fibroblast growth factor receptor 2 (FGFR2) being developed for patients with FGFR2-driven cholangiocarcinoma (CCA) and other FGFR2-altered solid tumors.

REPORT COVERAGE

The global cholangiocarcinoma drugs market analysis provides a detailed analysis of a rare but increasingly important oncology segment. It examines how the treatment landscape is evolving from conventional chemotherapy toward immunotherapy and biomarker-driven targeted therapies as clinical understanding of cholangiocarcinoma improves. The study covers key growth drivers, restraints, challenges, and emerging opportunities influencing market expansion across major regions. It also evaluates market size outlook, competitive positioning, regulatory developments, and recent company activities shaping the industry. In addition, the report offers segment-wise analysis by therapy, drug class, disease indication, age group, type, and distribution channel, helping identify the areas expected to generate the strongest commercial demand.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.34% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Therapy, Drug Class, Disease Indication, Type, Age Group, Route of Administration, Distribution Channel, and Region |

| By Therapy |

|

| By Drug Class |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.29 billion in 2025 and is projected to reach USD 3.78 billion by 2034.

In 2025, the market value stood at USD 0.51 billion.

The market is expected to grow at a CAGR of 12.34% over the forecast period.

By therapy, the chemotherapy segment is expected to lead the market.

Rising generic drug production is driving the need for efficient excipients and market growth.

Incyte, Innovent Biologics, Servier, Taiho Pharmaceutical, and Jazz Pharmaceuticals are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us