Chronic Kidney Disease Drugs Market Size, Share & Industry Analysis, By Drug Class (SGLT2 Inhibitors, ACE Inhibitors, Angiotensin II Receptor Blockers, Direct Renin Inhibitors, Mineralocorticoid Receptor Antagonists, Endothelin Receptor Antagonists, & Others), By Stage (Stage 1, Stage 2, Stage 3a, Stage 3b, Stage 4, & Others), By Disease Indication (Diabetic Kidney Disease, Hypertensive Nephropathy / Nephrosclerosis, Polycystic Kidney Disease, Chronic Tubulointerstitial Nephritis, & Others), By Route of Administration, By Distribution Channel, and Regional Forecast, 2026-2034

Chronic Kidney Disease Drugs Market Size and Future Outlook

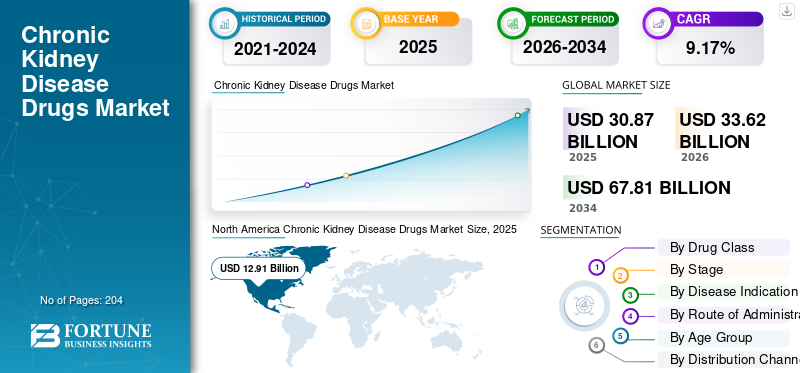

The global chronic kidney disease drugs market size was valued at USD 30.87 billion in 2025. The market is projected to grow from USD 33.62 billion in 2026 to USD 67.81 billion by 2034, exhibiting a CAGR of 9.17% during the forecast period. North America dominated the chronic kidney disease drugs market with a market share of 41.82% in 2025.

Chronic kidney disease (CKD) drugs involve the use of pharmacotherapies that slow kidney function decline, reduce albuminuria/proteinuria, and lower the risk of kidney failure and cardio-renal events across routine clinical practice. These drugs are prescribed across CKD stages (1–5 non-dialysis) and can extend into late-stage care where treatment intensity and add-on medications typically increase. Factors shaping this market include rising CKD burden, driven by diabetes, hypertension, obesity, and aging populations, and earlier identification through broader screening and routine eGFR/albuminuria testing. The market is also influenced by payer pressure to delay dialysis initiation and reduce hospitalization costs, which supports the adoption of therapies with demonstrable kidney and cardiovascular benefits.

Major companies such as AstraZeneca, Boehringer Ingelheim, and Eli Lilly are expanding renal-protection portfolios around SGLT2 inhibitors.

Download Free sample to learn more about this report.

CHRONIC KIDNEY DISEASE DRUGS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 30.87 Billion

- 2026 Market Size: USD 33.62 Billion

- 2034 Forecast Market Size: USD 67.81 Billion

- CAGR: 9.17% from 2026–2034

- North America dominated the chronic kidney disease drugs market with a 41.82% share in 2025.

- The endothelin receptor antagonists (ERAs) segment is projected to grow at a CAGR of 11.82% during the forecast period.

- The stage 5 (non-dialysis) segment is expected to expand at a CAGR of 10.59% over the forecast period.

North America

North America reached USD 12.91 billion in 2025 and maintained market leadership, supported by broad adoption of advanced renal-protective therapies, favorable reimbursement policies, and strong patient access programs.

Europe

Europe is projected to reach USD 8.81 billion in 2026 and grow at a CAGR of 8.09%, driven by standardized treatment pathways, rising hypertension prevalence, and increasing uptake of novel kidney disease therapies.

Asia Pacific

Asia Pacific is expected to attain USD 7.98 billion in 2026, supported by a growing diabetic and hypertensive patient population, expanding healthcare access, and rising chronic-care initiatives.

U.S.

The market is estimated to reach approximately USD 13.29 billion in 2026, accounting for around 39.5% of global revenue, driven by strong adoption of innovative CKD therapies and advanced healthcare infrastructure.

Japan

The market is projected to reach around USD 1.00 billion in 2026, supported by an aging population, increasing CKD prevalence, and growing demand for effective renal disease management solutions.

Read More

CHRONIC KIDNEY DISEASE DRUGS MARKET TRENDS

Shift toward Advanced Treatments beyond Traditional ACE Inhibitors/ARBs is a Significant Market Trend

The CKD treatment landscape is evolving from solely focusing on blood-pressure management with ACE inhibitors/ARBs to more advanced, outcome-oriented therapies aimed at directly addressing kidney disease progression and cardio-renal risk. Clinicians are progressively adding newer classes to existing RAAS blockade to attain reductions in albuminuria, a slower decline in eGFR, and fewer kidney-failure incidents, rather than merely lowering BP. This trend is influenced by more robust clinical evidence, wider guideline support, and insurance interest in therapies that can postpone dialysis/transplant expenses. Consequently, value share is shifting toward newer renal-protective agents and specialty therapies, whereas ACEi/ARBs continue to be fundamental but contribute less to value due to their generic status. The market is experiencing an increase in combination/stacked treatments among eligible patients, increasing annual spending per patient. These factors are supporting the global chronic kidney disease drugs market growth.

- For instance, in January 2025, Novo Nordisk announced that the U.S. FDA approved Ozempic (semaglutide) for reducing the risk of kidney failure/kidney disease worsening and cardiovascular death in adults with type 2 diabetes and CKD.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising CKD Burden Driven by Diabetes, Hypertension, Obesity, and Aging Population to Propel Market Growth

The growing CKD prevalence is a significant market driver as it directly broadens the population of diagnosed and treated patients, thereby enhancing the long-term need for chronic treatments. The increase is closely associated with a greater occurrence of type 2 diabetes and hypertension, which rank among the most frequent underlying causes of advancing kidney injury and CKD-related issues. Additionally, with the rise in obesity, the length and severity of metabolic stress are heightened, which in turn elevates the risk of CKD and speeds up its progression, leading more patients to require ongoing pharmacological treatment. Furthermore, the aging population intensifies this as the prevalence and progression risk of CKD increase with age, leading to higher treatment intensity in advanced stages. Collectively, these factors boost both the start of therapy and the continuation of therapy, elevating total drug usage. They also enhance payer emphasis on delaying progression to prevent dialysis expenses, promoting wider adoption of kidney-protective treatments in the long run. All these factors cumulatively drive the global market growth.

- For instance, according to data published by the American Society of Nephrology in October 2024, the global CKD prevalence has risen sharply and type 2 diabetes and hypertension were leading causes of CKD-related deaths, with marked increases observed among older adults.

MARKET RESTRAINTS

High Costs of Treatment to Hamper Market Growth

The high expense of treatment serves as a significant barrier in the CKD pharmaceuticals market, as it may restrict the swift adoption of newer renal-protective therapies from guidelines to everyday practice. Numerous CKD patients necessitate prolonged, multi-year treatment. Thus, even moderate monthly expenses can add up and result in postponed start, cessation, or step-therapy limitations. Cost pressure is particularly evident for branded, newer agents, as reimbursement differs by payer and country, leading to inconsistent access across regions and income levels. In settings with lower and middle incomes, financial limitations may restrict usage to low-cost generics, hindering growth in value for advanced therapies. In general, expensive treatment serves as a barrier between clinical necessity and real adoption, limiting market growth.

- For instance, in a CMS fact sheet on negotiated prices for Initial Price Applicability Year 2026 published in February 2026, CMS lists Farxiga with a CY2023 30-day list price (WAC) of USD 556 and Jardiance with a CY2023 30-day list price (WAC) of USD 573.

MARKET OPPORTUNITIES

Focus on Early Diagnosis to Increase Patient Base to Offer Market Growth Opportunities

The emphasis on early detection represents a significant market opportunity, as it transforms a vast number of undiagnosed CKD patients into recognized, risk-stratified, and treated individuals who can begin renal-protective therapy earlier. Expanding the routine testing of eGFR and urine albumin (uACR) in high-risk populations such as diabetes, hypertension, and older adults enhances the identification of early-stage and albuminuric CKD that standard care frequently overlooks. In addition, timely diagnosis broadens the reachable treated demographic, enhances adherence via organized monitoring, and raises the count of patients suitable for contemporary disease-altering therapies. It additionally backs payer objectives by transitioning care from late-stage intervention to progression avoidance, potentially delaying dialysis and expensive hospital stays. As screening is standardized, treatment routes become more systematic, enhancing the adoption of renal-protective medication classes and raising lifetime therapy duration per patient. In general, earlier detection enhances market worth by raising both patient numbers and duration of treatment. All these factors would drive the market growth in the coming years.

- For instance, in May 2025, the National Kidney Foundation (NKF) issued a press release urging a global shift to make urinary albumin testing a standard of care for CKD detection and monitoring in high-risk adults.

MARKET CHALLENGES

Regulatory Hurdles and Reimbursement Variability Present a Major Obstacle to Market Expansion

Regulatory obstacles and inconsistent reimbursement continue to pose significant issues in the CKD medications market due to the lengthy, intricate, and endpoint-focused nature of kidney outcomes trials, as regulators and HTA organizations frequently require substantial proof of clinically relevant outcomes alongside safety in populations with comorbidities. Despite advancements in regulations, reimbursement choices can vary significantly from one country to another, resulting in unequal patient access, postponed launches, or limited eligibility requirements. This unpredictability generates uncertainty for producers regarding peak uptake and necessitates significant investment in real-world evidence, health-economic models, and access initiatives. It also hinders the adoption of newer specialized treatments, resulting in utilization remaining focused on less expensive standards in certain areas. All the factors cumulatively affect the market growth.

Segmentation Analysis

By Drug Class

Higher Usage of the Drug Class to Propel SGLT2 Inhibitors Segment Growth

Based on drug class, the market is divided into SGLT2 inhibitors, ACE inhibitors, angiotensin II receptor blockers (ARBs), direct renin inhibitors, mineralocorticoid receptor antagonists (MRAs), endothelin receptor antagonists (ERAs), immunosuppressants, corticosteroids, complement inhibitors, and others.

The SGLT2 inhibitors segment captured the largest global chronic kidney disease drugs market share in 2025. It is a core therapy for slowing CKD progression and reducing kidney failure risk in routine care. Their clinical use has expanded as physicians increasingly prioritize renal outcomes (eGFR decline, dialysis delay) and cardio–renal risk reduction, leading to higher initiation rates and longer time-on-therapy. In addition, SGLT2 inhibitors are typically used as add-on therapy rather than replacement. Hence, they scale market value without displacing baseline standards. Wider adoption across nephrology, diabetology, and cardiology settings further supports consistent prescribing and strengthens segment leadership.

- For instance, according to a study published by Oxford Population Health in November 2025, SGLT2 inhibitors deliver major kidney and heart benefits for people with CKD regardless of diabetes status or albuminuria level.

The endothelin receptor antagonists (ERAs) segment is anticipated to rise at a CAGR of 11.82% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Stage

Broader Treatable Population Supported the Stage 3b Segmental Dominance

Based on stage, the market is divided into stage 1, stage 2, and stage 3a, stage 3b, stage 4, stage 5 (non-dialysis), and others.

The stage 3b segment captured the largest global chronic kidney disease drugs market share in 2025. Stage 3b typically includes a broader treatable population than Stage 4–5. This combination of high patient volume and higher treatment intensity drives a larger value contribution, especially as payers and clinicians prioritize avoiding progression to dialysis leading to segment dominance. Furthermore, the segment is set to hold 22.2% share in 2026.

- For instance, in August 2024, Novartis announced the U.S. FDA accelerated approval of Fabhalta (iptacopan) for the reduction of proteinuria in adults with primary IgA nephropathy at risk of rapid progression, based on the Phase III APPLAUSE-IgAN interim analysis. The company noted the main study population included patients with baseline eGFR ≥30 mL/min/1.73m², capturing late Stage 3b patients and reinforcing focus on moderate-to-advanced CKD population.

The stage 5 (non-dialysis) segment is anticipated to rise with a CAGR of 10.59% over the forecast period.

By Disease Indication

High Prevalence of Diabetic Kidney Disease (DKD) to Boost Segmental Growth

In terms of disease indication, the market is divided into diabetic kidney disease (DKD), hypertensive nephropathy/nephrosclerosis, glomerular diseases, polycystic kidney disease (PKD), Chronic Tubulointerstitial Nephritis, Obstructive Uropathy–related CKD, systemic autoimmune–associated CKD, infectious/inflammatory–associated CKD, congenital/structural kidney disorders (non-PKD), and others.

The diabetic kidney disease (DKD) segment dominated the global market in 2025. It represents the largest and fastest-expanding CKD patient pool, driven by the global rise in type 2 diabetes. In addition, DKD patients are more likely to be diagnosed and followed longitudinally, which increases treatment initiation, regimen intensification, and persistence over multiple years. It represents the largest and fastest-expanding CKD patient pool, driven by the global rise in type 2 diabetes. DKD patients are more likely to be diagnosed and followed longitudinally, which increases treatment initiation, regimen intensification, and persistence over multiple years, in turn supporting segment growth. Furthermore, the segment is set to hold 46.5% share in 2026.

- For instance, in April 2025, the International Diabetes Federation (IDF) released new Diabetes Atlas estimates noting that nearly one in nine adults is living with diabetes and that over 250 million people are unaware they have the condition.

The congenital/structural kidney disorders (non-PKD) segment is anticipated to rise with a CAGR of 10.19% over the forecast period.

By Route of Administration

High Patient Adherence to Oral Medications to Boost Oral Segmental Growth

In terms of route of administration, the market is divided into oral and parenteral.

The oral segment captured the highest share of the global market in 2025. Most CKD therapies are designed for long-term, outpatient management, where daily tablets are the most practical and scalable option, driving industry expansion. Oral drugs fit routine prescribing workflows in primary care and nephrology, supporting earlier initiation, easier refills, and better persistence versus clinic-dependent administration. Oral dosing also enables combination without creating infusion burden. Additionally, new product launches by operating players also supported the segment growth. Furthermore, the segment is set to hold 86.9% share in 2026.

- For instance, in January 2023, the U.S. FDA accepted a supplemental New Drug Application (sNDA) for Jardiance (empagliflozin) tablets for CKD treatment.

The parenteral segment is anticipated to rise with a CAGR of 7.86% over the forecast period.

By Age Group

High Usage in Adults to Boost Adults Segmental Growth

On the basis of age group, the market is divided into pediatrics and adults.

The adults segment captured the highest share of the global market in 2025. Adult patients represent the largest share of diagnosed and treated CKD, leading to higher prescription volumes and longer time-on-therapy than pediatrics. As kidney function declines with age, adults are more likely to require intensified, multi-drug regimens to slow progression and manage complications, increasing per-patient spend. Adults also have broader access to reimbursed therapies across primary care and specialty pathways, further reinforcing share dominance. Furthermore, the segment is set to hold 97.3% share in 2026.

- For instance, in November 2025, the Institute for Health Metrics and Evaluation (IHME) reported that the number of adults living with CKD has more than doubled since 1990. The figures reached nearly 800 million worldwide, based on the Global Burden of Disease 2023 findings.

The pediatrics segment is anticipated to rise with a CAGR of 12.22% over the forecast period.

By Distribution Channel

High Distribution Volume by Drug Stores & Retail Pharmacies Supported Segment’s Leading Position

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

In 2025, the drug stores & retail pharmacies segment held the leading position in the global market. Most CKD therapies are long-term, refill-driven outpatient medicines, making community dispensing the most frequent and accessible touchpoint for patients. Retail chains and neighborhood drugstores also provide broad geographical coverage, faster fulfillment, and stronger payer-network integration. Moreover, retail pharmacies also support chronic disease programs, which improves persistence and keeps dispensing volumes high. Furthermore, the segment is set to hold 50.4% share in 2026.

In addition, the online pharmacies segment is projected to witness a CAGR of 13.81% during the forecast period.

Chronic Kidney Disease Drugs Market Regional Outlook

By geography, the market is divided into Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

North America

North America Chronic Kidney Disease Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America established itself as the market leader, holding a valuation of USD 11.83 billion in 2024 and reaching USD 12.91 billion in 2025. This ongoing superiority is fueled by the widespread use of innovative renal-protective treatments, robust reimbursement strategies, and increasing patient support/access initiatives.

U.S. Chronic Kidney Disease Drugs Market

The U.S. is poised to dominate the North American market in 2026. The market value for 2026 can be analytically approximated at around USD 13.29 billion, accounting for roughly 39.5% of the global market.

Europe

Europe is anticipated to maintain a consistent growth path, depicting a CAGR of 8.09% over the analysis period. The region is anticipated to record a market size of USD 8.81 billion in 2026. Widespread implementation of standard-of-care pathways and alignment with guidelines in significant markets, combined with shifting demographics, high prevalence of hypertension, and a growing adoption of new renal-protective agents, are crucial elements driving market growth in the region.

U.K. Chronic Kidney Disease Drugs Market

The U.K. market is estimated to touch around USD 1.83 billion in 2026, representing roughly 5.4% of global revenues.

Germany Chronic Kidney Disease Drugs Market

Germany market size is projected to reach approximately USD 1.99 billion in 2026, equivalent to around 5.9% of global sales.

Asia Pacific

The Asia Pacific region is expected to reach USD 7.98 billion by 2026, cementing its status as the third-largest regional market. A growing patient population from the increasing prevalence of diabetes and hypertension, enhanced access to diagnostics, and the expansion of private hospital networks and chronic-care initiatives are anticipated to drive significant growth throughout the region.

Japan Chronic Kidney Disease Drugs Market

The Japan market is estimated to touch around USD 1.00 billion in 2026, accounting for roughly 3.0% of global revenues.

China Chronic Kidney Disease Drugs Market

The China market is projected to reach revenues of around USD 3.17 billion in 2026, representing roughly 9.4% of global sales.

India Chronic Kidney Disease Drugs Market

The India market is estimated to touch around USD 1.25 billion in 2026, accounting for roughly 3.7% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to depict moderate growth rates over the analysis period. The Latin American market is expected to reach USD 1.59 billion by 2026, while the GCC in the Middle East & Africa is expected to touch a valuation of USD 0.56 billion in 2026.

South Africa Chronic Kidney Disease Drugs Market

The South Africa market is projected to reach around USD 0.14 billion in 2026, representing roughly 0.4% of the global market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Held the Highest Market Share due to Diversified and Robust Product Portfolios

Bayer AG, AstraZeneca, and Boehringer Ingelheim Pharmaceuticals, Inc. are some of the key players in the global market. Robust efforts in research and development, regulatory clearances, and the introduction of new products are helping maintain their market position. Additionally, strategic efforts to broaden their market presence are further strengthening their standing in the sector.

- For instance, in September 2025, AstraZeneca launched AstraZeneca Direct, an online platform, for the expansion of access to medications for U.S. patients living with chronic kidney disease and other chronic conditions.

Eli Lilly and Company, Novartis AG, GSK plc, and Sanofi are notable participants in the market. Concentrating on product releases and strategic efforts such as partnerships and research projects helps enhance their market share.

LIST OF KEY CHRONIC KIDNEY DISEASE DRUGS COMPANIES PROFILED

- AstraZeneca (U.K.)

- Bayer AG (Germany)

- Boehringer Ingelheim Pharmaceuticals, Inc. (Germany)

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Calliditas Therapeutics AB (Sweden)

- Otsuka Pharmaceuticals Inc. (Japan)

- GSK plc (U.K.)

- Amgen Inc. (U.S.)

- Sanofi (France)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Novartis shared that the final Phase III ALIGN results indicating Vanrafia (atrasentan) supported slowing kidney function decline in adults with IgA nephropathy, with plans toward traditional approval.

- February 2026: Roche announced positive Phase III MAJESTY results for Gazyva/Gazyvaro (obinutuzumab) in primary membranous nephropathy, meeting the primary endpoint.

- January 2026: Variant Bio announced a multi-year research collaboration and license agreement with Boehringer Ingelheim focused on discovering and validating novel targets for kidney disease/cardiorenal disease.

- December 2025: Rectify and Boehringer Ingelheim announced a collaboration to advance first-in-class CKD treatments, aiming to accelerate development around a CKD-relevant mechanism.

- November 2025: Otsuka Pharmaceuticals announced that the U.S. FDA provided accelerated approval for VOYXACT (sibeprenlimab-szsi) to reduce proteinuria in adults with primary IgA nephropathy at risk for progression.

REPORT COVERAGE

The global chronic kidney disease drugs market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, and the introduction of new products, and pipeline analysis. Furthermore, it outlines collaborations, mergers & acquisitions, along with the prevalence of key diseases across key countries and regions. The global market forecast report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.17% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Stage, Disease Indication, Route of Administration, Age Group, Distribution Channel, and Region |

| By Drug Class |

|

| By Stage |

|

| By Disease Indication |

|

| By Route of Administration |

|

| By Age Group |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 30.87 billion in 2025 and is projected to reach USD 67.81 billion by 2034.

In 2025, North Americas market value stood at USD 12.91 billion.

The market is expected to exhibit a CAGR of 9.17% during the forecast period of 2026-2034.

By drug class, the SGLT2 Inhibitors segment is expected to lead the market.

Rising prevalence of chronic kidney diseases and increasing regulatory approvals are key factors primarily driving market expansion.

Bayer AG, Amgen Inc., AstraZeneca, and Eli Lilly and Company are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 204

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us