Chronic Pain Drugs Market Size, Share & Industry Analysis, By Drug Class (NSAIDs, Opioids, Antidepressants, Anticonvulsants / Gabapentinoids, Topical Analgesics, Local Anesthetics, & Others), By Disease Indication (Musculoskeletal Pain, Neuropathic Pain, Cancer-related Pain, Postsurgical / Post-traumatic Pain, Visceral Pain, & Others), By Age Group (Pediatric & Adult), By Type (Branded & Generic), By Route of Administration (Oral & Parenteral), By Distribution Channel (Hospital Pharmacies, Specialty pharmacies, Drug Stores & Retail Pharmacies, & Others), and Regional Forecast, 2026-2034

Chronic Pain Drugs Market Size and Future Outlook

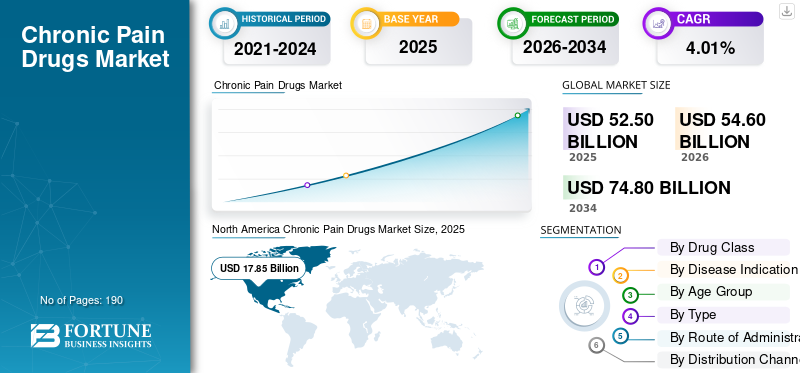

The chronic pain drugs market size was valued at USD 52.50 billion in 2025. The market is projected to grow from USD 54.60 billion in 2026 to USD 74.80 billion by 2034, exhibiting a CAGR of 4.01% during the forecast period. North America dominated the chronic pain drugs market with a market share of 34% in 2025.

The market is poised to grow steadily over the forecast period, driven by the wide prevalence of chronic pain and sustained demand for pharmacological treatment for neuropathic pain, musculoskeletal pain, migraine, cancer-related pain, and other persistent pain conditions. The market growth is also reassured by the increasing need for safer and more targeted therapies to reduce dependence on traditional opioid-based treatment approaches. Furthermore, the growing burden of chronic pain in geriatric population and rising focus on improving quality of life are supporting continued product development, lifecycle expansion, and pipeline investment in this market.

Key companies operating in the market are increasingly focusing on expanding their product offerings and commercializing them.

- For instance, in May 2025, Eli Lilly and Company acquired SiteOne Therapeutics to expand its pain pipeline. The development strengthened the company’s effort to develop novel non-opioid therapies, including STC-004, a Phase 2 sodium channel inhibitor being developed for pain. Such pipeline-focused acquisitions show that companies are increasing investment in next-generation therapies, which is expected to support future growth of the market.

Furthermore, leading players in the chronic pain drugs industry, such as Viatris Inc., Eli Lilly and Company, AbbVie Inc., and Teva Pharmaceutical Industries Ltd, are focusing on research and development and strategic partnerships, expanding their offerings to strengthen their market positions.

Download Free sample to learn more about this report.

Chronic Pain Drugs Market Key Takeaways

- 2025 Market Size: USD 52.50 billion

- 2026 Market Size: USD 54.60 billion

- 2034 Forecast Market Size: USD 74.80 billion

- CAGR: 4.01% from 2026–2034

- North America dominated the market with a 34.0% share in 2025.

- NSAIDs segment dominated the market.

- Musculoskeletal pain segment accounted for the largest market share in 2025.

North America

Valued at USD 17.85 billion in 2025 and maintained market leadership.

Asia Pacific

Projected to reach USD 14.14 billion in 2026, supported by rising aging population and chronic pain prevalence.

Europe

Expected to reach USD 14.09 billion in 2026, driven by an aging population and chronic disease burden.

U.S.

The U.S. market is projected to reach USD 17.26 billion in 2026.

Japan

The Japan market is estimated at USD 3.20 billion in 2026.

Read More

CHRONIC PAIN DRUGS MARKET TRENDS

Shift Toward Non-Opioid Pain Management is an Emerging Market Trend

A key market trend emerging is the shift toward non-opioid pain management practices. As healthcare systems, physicians, and drug developers are focusing on safer long-term treatment approaches, the adoption of non-opioid and addiction-free pain management is crucial. Concerns related to opioid dependence, misuse risk, and long-term safety have increased the demand for alternatives that can deliver pain relief with lower addiction potential. As a result, companies are investing more in novel mechanisms such as sodium channel inhibitors and other targeted non-opioid therapies. This shift is expected to transform the market by encouraging innovation, expanding treatment options, and supporting the commercial growth of safer pain drugs across chronic pain management pathways.

- For instance, in January 2025, Vertex Pharmaceuticals received FDA approval for JOURNAVX (suzetrigine), a non-opioid treatment for adults with moderate-to-severe acute pain. Such developments strengthen confidence that the future pain treatment landscape will increasingly move beyond traditional opioid-based therapies.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Aging Population and Higher Pain Burden Supports Market Expansion

The crucial factor driving the chronic pain drugs market growth is surging aging population. Since older adults are more likely to develop long-term pain conditions such as osteoarthritis, neuropathic pain, lower back pain, and other degenerative disorders, they are anticipated to elevate product demand. As the number of older population increases, the patient pool requiring continuous pain relief and long-term symptom management also expands. This creates higher demand for both established pain medicines and newer therapies that can offer better safety and sustained relief. Additionally, older patients often live with multiple chronic conditions, which increases the need for more consistent pharmacological pain management and supports long-term growth of this market.

- For instance, in February 2025, the WHO reported that globally, the number of people aged 60 and older is projected to rise from 1.1 billion in 2023 to 1.4 billion by 2030, and chronic pain prevalence also rises with age. In the U.S., 36.0% of adults aged 65 and older had chronic pain in 2023.

MARKET RESTRAINTS

Safety Risks and Regulatory Caution Around Long-Term Opioid Use Restricts Market Growth

A significant factor restricting the growth of the market is the safety concerns revolving around long-term opioid use for pain management. These therapies continue to be associated with misuse, addiction, overdose, and other serious adverse outcomes. As these risks have become more visible, regulators and healthcare providers have adopted a more cautious approach toward prolonged opioid prescribing in chronic pain management. This reduces prescribing confidence, limits treatment duration, and pushes both physicians and payers to favor more closely monitored or alternative pain treatment strategies.

- For instance, in July 2025, the U.S. FDA announced major class-wide prescribing information updates for opioid pain medicines to emphasize further and characterize the risks associated with long-term use. The updates followed a review of data showing serious long-term safety risks, including misuse, addiction, opioid use disorder, and overdose. Such oversight of opioid-based pain treatment can further limit prescribing growth in the market.

MARKET OPPORTUNITIES

Expanding Focus on Personalized and Indication-Specific Pain Management Offers New Market Growth Avenues

The market is poised to benefit from the broader shift toward multimodal and personalized pain management. Chronic pain is not a single-condition disease, and patients often respond differently depending on the underlying cause of pain. Physicians are moving away from one-size-fits-all treatment and increasingly prefer therapies matched to specific pain mechanisms. These factors create room for newer therapies that can be positioned for clearly defined patient groups rather than broad, undifferentiated pain use. Similarly, multimodal care models are encouraging the use of safer, mechanism-based medicines alongside other treatment approaches, which is improving the commercial potential of differentiated pain drugs.

- For instance, in May 2025, TRemedical dosed the first patient in the Phase II trial of TRD205 for chronic post-surgical neuropathic pain. The TRD205 is a first-in-class AT2R antagonist being developed specifically for this chronic pain subtype, highlighting the move toward more targeted and indication-focused pain treatment.

MARKET CHALLENGES

Long-Term Tolerability Issues with NSAIDs Pose a Significant Challenge for Market Growth

A significant challenge faced by the market is the risk associated with adverse effects linked to widely used non-opioid drugs such as NSAIDs. These medicines are commonly used for long-term pain relief but are not free from clinically significant safety risks. With prolonged or repeated use, NSAIDs have been associated with cardiovascular events such as heart attack and stroke, and regulators have also highlighted the need for caution based on dose and duration of treatment. As a result, although NSAIDs remain important in chronic pain management, their long-term risk profile creates a treatment challenge. It pushes the market toward safer alternatives and more selective prescribing.

- For example, the U.S. FDA stated the risk of heart attack or stroke can occur as early as the first weeks of NSAID use and may increase with longer use or higher doses.

Segmentation Analysis

By Drug Class

Wide Adoption of NSAIDs for Long-Term Pain Relief Leads to Segmental Growth

Based on the drug class, the market is categorized into NSAIDs, opioids, antidepressants, anticonvulsants/gabapentinoids, topical analgesics, local anesthetics, cannabinoid-based drugs, and others.

Among these, the NSAIDs segment dominated the market. NSAIDs are widely used as first-line medicines for long-term pain relief in conditions such as osteoarthritis, lower back pain, joint pain, and other inflammatory musculoskeletal disorders. The segment's dominance is supported by broad physician familiarity, relatively lower treatment costs compared to branded alternatives, and the ability to address both pain and inflammation simultaneously, resulting in high prescription and consumption volumes. Due to such broad clinical utility and accessibility, NSAIDs continue to hold a strong position in the market. Additionally, due to the high commercial importance, key companies are increasingly investing in new product launches and their subsequent approvals.

- For instance, in June 2025, Azurity Pharmaceuticals received U.S. FDA approval for XIFYRM (meloxicam injection) for the management of moderate-to-severe pain in adults. Such developments show that NSAID-based pain therapies continue to receive regulatory and commercial support, which strengthens the dominance of this segment in the market.

The cannabinoid-based drugs segment is expected to grow at a CAGR of 6.14% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Increasing Prevalence of Musculoskeletal Pain to Boost Segmental Growth

Based on disease indication, the market is segmented into musculoskeletal pain, neuropathic pain, cancer-related pain, postsurgical/post-traumatic pain, visceral pain, headache/orofacial pain, primary pain syndromes, and others.

In 2025, the musculoskeletal pain segment accounted for the largest share of the market by disease indication. The disease represents one of the most commonly treated chronic pain categories worldwide. Conditions such as osteoarthritis, chronic back pain, neck pain, joint pain, and other mobility-related disorders affect a large adult and aging population, creating sustained demand for pain management drugs. These conditions often demand repeated or continuous pain management, which increases overall drug consumption. As the burden of degenerative and movement-related disorders continues to rise, musculoskeletal pain remains a major contributor to product demand and supports the segment’s leading share. Recent pipeline activity in osteoarthritis pain further confirms that companies see this indication as a major commercial opportunity.

- For instance, in April 2025, Sun Pharma and Moebius Medical announced publications and new data presentations for MM-II in osteoarthritis, highlighting durable pain relief from a single injection and noting that MM-II had recently received FDA Fast Track Designation. Such developments are important as osteoarthritis is one of the largest chronic musculoskeletal pain conditions, and continued innovation in this area supports the dominance of the musculoskeletal pain segment.

The neuropathic pain segment is projected to grow at a CAGR of 4.58% during the forecast period.

By Age Group

Large Share of Adult Patients for Chronic Pain Diagnosis to Drive Segmental Growth

Based on age group, the market is segmented into pediatric and adult.

The adult segment accounted for the largest share of the global market. The adult population accounts for the largest share of chronic pain diagnosis, treatment seeking, and long-term medicine use. Chronic pain is far more common in adults due to higher exposure to occupational strain, sedentary lifestyle risks, obesity, arthritis, nerve disorders, migraine, fibromyalgia, and other age-related or lifestyle-related conditions. Since most chronic pain indications are frequently diagnosed and managed in adult populations, the segment naturally holds the largest market share. Recent approvals specifically for adults show that the market's commercial focus remains strongly centered on adult end users.

- For instance, in August 2025, Tonix Pharmaceuticals received the U.S. FDA approval for Tonmya (cyclobenzaprine HCl sublingual tablets) for the treatment of fibromyalgia in adults. This development supported the dominance of the adult segment, showcasing that companies continue to prioritize adult chronic pain-related conditions where the patient pool and commercial opportunity are larger.

The pediatric segment is projected to grow at a CAGR of 3.11% during the study period.

By Type

Higher Consumption of Generic Drug Type to Boost Segment Growth

Based on type, the market is segmented into branded and generic products.

The generic drugs dominated the market. This is due to a large proportion of chronic pain treatment still relies on established molecules that are available at lower cost after patent expiry. Chronic pain often requires long-duration therapy, so physicians, payers, and patients tend to prefer lower-cost generic options to reduce the financial burden of treatment. The broad availability of generic products also increases accessibility and prescription volume. As a result, the generic segment continues to dominate overall market value in many countries.

- For instance, in July 2024, ANI Pharmaceuticals received U.S. FDA approval and launched Naproxen Delayed-Release Tablets, USP, the generic version of EC-Naprosyn. Such launches strengthen the generic segment by increasing access to lower-cost pain medicines in a therapy area where long-term affordability is important for sustained treatment use.

In addition, the branded segment is projected to grow at a CAGR of 3.25% during the study period.

By Route of Administration

Higher Convenience and Ease of Administration of Oral Route Leads to Segment’s Expansion

Based on route of administration, the market is segmented into oral and parenteral routes.

In 2025, the oral segment dominated the market. These oral drugs are more convenient, easier to administer, and better suited for long-term outpatient treatment than parenteral options. Chronic pain patients often require repeated or continuous therapy, and oral medicines are generally preferred as they improve treatment adherence and reduce the need for clinical supervision. Oral formulations are also widely distributed through retail and hospital channels and are available across multiple major pain drug classes. These features support the segment's leading position in the market. Recent late-stage development of oral pain candidates further reinforces the commercial importance of this route.

- For instance, in March 2025, Tris Pharma announced positive Phase 3 results from the ALLEVIATE-2 trial for cebranopadol, an investigational first-in-class oral dual-NMR agonist for the treatment of pain. Such developments reinforce the dominance of oral segment, as companies continue to prioritize oral pain medicines for greater patient convenience and market adoption.

In addition, the parenteral segment is projected to grow at a CAGR of 4.89% during the study period.

By Distribution Channel

Large Patient Volumes in Hospital Pharmacies Leads to Segment’s Dominance

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, online pharmacies, and others.

By distribution channel, drug stores & retail pharmacies are estimated to dominate the market. They provide the most accessible and convenient point of purchase for a large number of chronic pain patients, especially those using long-term maintenance medicines or OTC pain relief products. Many chronic pain conditions are managed in outpatient settings, making retail pharmacies an important channel for repeat refills, pharmacist guidance, and broad community-level access. Their strong physical presence, consumer familiarity, and integration with both prescription and self-care pain management help this channel capture high dispensing volumes. Strategic collaborations among key retail providers signify the segment’s growth.

- For instance, in December 2025, Maxwellia launched Naprosyn Pain Relief, announcing its availability via Boots.com, in Boots stores, and in high street pharmacies nationwide. This supports the dominance of drug stores and retail pharmacies as it shows that pain relief products continue to be commercialized through broad retail pharmacy networks, where patient access and repeat purchase are huge.

The online pharmacies segment is projected to grow at a CAGR of 8.69% over the study period.

Chronic Pain Drugs Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Chronic Pain Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 17.13 billion and maintained its leading position in 2025 at USD 17.85 billion. The market is growing as chronic pain prevalence in the region is higher, and the treated patient pool is large. Also the region has robust healthcare infrastructure. These factors support continued demand for long-term pain medicines, including both generic and newer non-opioid therapies.

U.S. Chronic Pain Drugs Market

Given North America's substantial contribution, the U.S. market is estimated at around USD 17.26 billion in 2026, accounting for roughly 31.62% of the global market.

Europe

Europe is projected to grow at 3.34% over the coming years, the second-highest among all regions, and reach a valuation of USD 14.09 billion by 2026. The market is growing in the region as it has an aging population with multiple long-term health needs, increasing the burden of other chronic pain conditions. These factors create sustained demand for chronic pain drugs as health systems manage a larger elderly population requiring ongoing symptom control.

U.K. Chronic Pain Drugs Market

The U.K. market is estimated to reach USD 2.94 billion in 2026, representing roughly 5.39% of the global market.

Germany Chronic Pain Drugs Market

Germany's market is projected to reach approximately USD 3.19 billion in 2026, equivalent to around 5.84% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 14.14 billion in 2026 and secure the position of the third-largest region in the market. The market is growing as the region is witnessing a rapidly aging population and a rising burden of non-communicable diseases and functional limitations associated with older age. These factors are expected to increase long-term demand for chronic pain treatment.

Japan Chronic Pain Drugs Market

The Japanese market in 2026 is estimated at around USD 3.20 billion, accounting for approximately 5.87% of the global market.

China Chronic Pain Drugs Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 4.18 billion, representing approximately 7.66% of global sales.

India Chronic Pain Drugs Market

The Indian market in 2026 is estimated at around USD 1.90 billion, accounting for roughly 3.47% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 4.53 billion in 2026. The market is growing in Latin America as population aging and the increasing burden of non-communicable diseases are causing more disability and long-term illness, including pain-linked conditions. Similarly, countries such as Brazil continue to strengthen cancer surveillance and access to specialist treatment. In the Middle East & Africa, the GCC is set to reach USD 1.08 billion in 2026.

South Africa Chronic Pain Drugs Market

The South African market is projected to reach approximately USD 0.43 billion by 2026, accounting for roughly 0.79% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Emphasis on Strategic Partnerships and New Product Launches by Key Players to Propel Market Expansion

The global market is fragmented, with companies such as Viatris Inc., Eli Lilly and Company, AbbVie Inc., Teva Pharmaceutical Industries Ltd, Amgen Inc., H. Lundbeck A/S, and Grünenthal GmbH holding significant global chronic pain drugs market share. Strategic partnerships, new product launches, pipeline development, and increased investments in the sector drive these companies' market share gains.

- For instance, in May 2025, Eli Lilly announced a definitive agreement to acquire Site One Therapeutics, a company developing small-molecule sodium channel inhibitors for pain and neuronal hyperexcitability disorders. Lilly stated the transaction would strengthen its non-opioid pain management pipeline, making it a major acquisition directly tied to the chronic pain therapeutics space.

Other notable players in the global market include Collegium Pharmaceutical, Inc., Haleon plc, and Kenvue Inc. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period.

LIST OF KEY CHRONIC PAIN DRUGS COMPANIES PROFILED

- Viatris Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- AbbVie Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Amgen Inc. (U.S.)

- Lundbeck A/S (Denmark)

- Grünenthal GmbH (Germany)

- Collegium Pharmaceutical, Inc. (U.S.)

- Haleon plc (U.K.)

- Kenvue Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Pacira BioSciences joined the PROBE Consortium, a public-private partnership aimed at improving osteoarthritis research, diagnosis, and treatment by leveraging data from more than 70 million individuals.

- August 2025: Teva received expanded indication from the U.S. FDA for AJOVY for the preventive treatment of episodic migraine in pediatric patients aged 6–17 years weighing at least 45 kg. The development broadens AJOVY’s addressable patient base and strengthens Teva’s position in the migraine-focused chronic pain segment.

- July 2025: Pacira BioSciences collaborated with Johnson & Johnson MedTech to expand ZILRETTA's market reach, an extended-release injectable for osteoarthritis knee pain. The collaboration aimed to co-promote the product through its early intervention sales force.

- May 2025: UPMC Enterprises, in collaboration with Redesign Health, launched Glimmer Health, a new company focused on supporting primary care physicians in delivering comprehensive chronic pain management. The development highlighted partnership-driven expansion of chronic pain care models.

- November 2024: Sangamo Therapeutics announced that the U.S. FDA cleared its IND application for ST-503 for idiopathic small fiber neuropathy, a type of chronic neuropathic pain. The development demonstrated that companies are continuing to invest in therapies for chronic pain conditions that are becoming more common and clinically important in aging populations.

REPORT COVERAGE

The global chronic pain drugs market report covers a detailed analysis of the industry across key drug classes, disease indications, age groups, product types, routes of administration, and distribution channels. It evaluates how the market is evolving due to the rising burden of long-term pain conditions such as musculoskeletal pain, neuropathic pain, cancer-related pain, and other persistent pain disorders that require ongoing treatment. The report also examines how demand is shifting with the growing preference for safer non-opioid therapies, the continued use of affordable generic medicines, and the development of targeted treatments for specific pain conditions. In addition, it provides insights into competitive developments, regulatory trends, pipeline activity, and regional growth patterns to present a complete view of the current and future market landscape. The study further highlights how rising adult patient populations, increasing long-term treatment needs, and continued innovation in pain management therapies are expected to support market expansion over the forecast period.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.01% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Disease Indication, Age Group, Type, Route of Administration, Distribution Channel, and Region |

| By Drug Class |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 52.50 billion in 2025 and is projected to reach USD 74.80 billion by 2034.

In 2025, the North America market value stood at USD 17.85 billion.

The market is expected to grow at a CAGR of 4.01% over the forecast period of 2026-2034.

The NSAIDs segment is expected to lead the market.

The growing aging population and higher pain burden are driving market growth.

Viatris Inc., Eli Lilly and Company, AbbVie Inc., Teva Pharmaceutical Industries Ltd, and Amgen Inc., are top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us