Civil & Commercial Helicopter Market Size, Share, and Industry Analysis, By Number of Engines (Single Engine and Twin Engine), By Maximum Take-off Weight (MTOW) (Less than 3,000 Kg, 3,000 Kg to 9,000 Kg, and Greater than 9,000 Kg), By Application (Emergency Medical Service, Corporate Service, Search and Rescue Operation, Oil & Gas, and Others), By Point of Sale (New and Pre-Owned), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

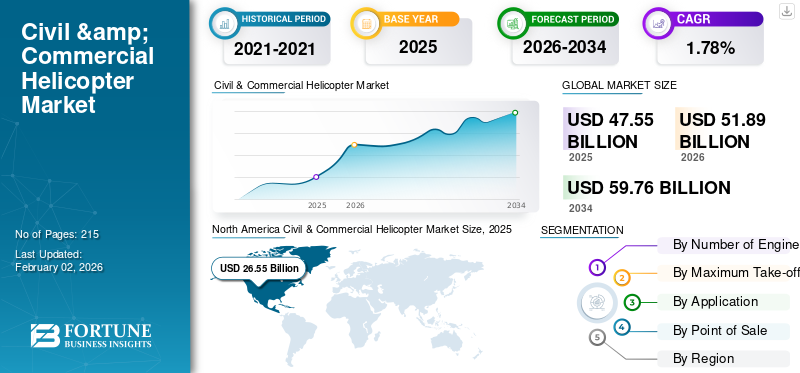

The global civil & commercial helicopters market size was valued at USD 47.55 billion in 2025. The market is projected to grow from USD 51.89 billion in 2026 to USD 59.76 billion by 2034, exhibiting a CAGR of 1.78% during the forecast period. North America dominated the civil & commercial helicopters market with a market share of 54.62% in 2025.

Helicopter is a type of rotary-wing aircraft that uses rotating blades to create lift and thrust. This design allows for vertical takeoff and landing, hovering, and flight in any direction capabilities. Helicopters are multipurpose for military, civil, commercial, and emergency operations. The civil and commercial helicopter market size is witnessing growth owing to the growing demand for emergency medical services (EMS), law enforcement, offshore oil and gas operations, corporate transport, and tourism. The rise of fuel efficiency and safer rotorcraft is also fueling the market size growth of civil and commercial helicopter. Additionally, ongoing infrastructure projects in emerging economies and the need to replace old fleets support further expansion.

Key players such as Airbus Helicopters, Leonardo S.p.A., Bell Textron Inc., Sikorsky (Lockheed Martin), and Russian Helicopters are fueling the market development. They are launching next-generation helicopters with enhanced safety features, hybrid-electric engines, and digital avionics, while expanding service networks to meet global commercial helicopter demand.

Download Free sample to learn more about this report.

Civil & Commercial Helicopter Market Key Takeaways

- 2025 Market Size: USD 47.55 billion

- 2026 Market Size: USD 51.89 billion

- 2034 Forecast Market Size: USD 59.76 billion

- CAGR: 1.78% from 2026–2034

- North America dominated the civil & commercial helicopters market with a 54.62% share in 2025.

- The twin-engine helicopter segment dominated the market in 2025.

- The less than 3,000 kg segment held the largest market share in 2025.

North America

North America generated USD 26.55 billion in revenue in 2025 and remained the leading regional market.

Europe

Europe accounted for 21.05% of the global market, reaching USD 9.84 billion in 2025.

Asia Pacific

Asia Pacific represented 15.46% of the global market with USD 6.21 billion in revenue in 2025.

U.S.

The country remains a key contributor to regional demand, supported by EMS, offshore transport, and corporate aviation activities.

Japan

The market is expected to witness steady growth driven by emergency services, tourism, and public safety operations.

Read More

CIVIL & COMMERCIAL HELICOPTER MARKET TRENDS

Amplified Demand from Developing Regions and Fleet Modernization is a Prominent Market Trend

The commercial and civil helicopter market in 2025 is recovering, stimulated by demand from emergency medical services, tourism, infrastructure, law enforcement, and energy markets, particularly in emerging markets and Asia-Pacific. Market growth is underpinned by fleet replacement requirements, new facility construction, and strategic OEM partnerships; the industry is subject to supply chain issues, but long-term prospects are positive.

-For Instance, in August 2025, Airbus partnered Mahindra Aerostructures to produce and assemble H125 helicopter fuselages in India, extending the "Make in India" alliance with deliveries from 2027 onwards.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Emergency Medical Services (EMS) and Public Safety Operations are Driving Market Growth

Helicopters play an important role in life-saving missions as they can take off and land vertically, hover in place, and reach crowded urban or remote rural areas where fixed-wing aircraft and ground ambulances struggle to reach. As road accidents, natural disasters, and medical emergencies rise, there is increasing dependence on air ambulance services for quicker patient transport and urgent medical care.

Moreover, helicopters are important for search and rescue (SAR), aerial firefighting, and law enforcement. Their ability to be deployed quickly and fly in the air recovers response time. Many governments and private companies are investing in modern helicopter fleets which have advanced avionics, night-vision systems, and medical gear to improve their emergency response capabilities. While other areas including offshore oil and gas operations, corporate transport, and tourism add to commercial helicopter market demand, the steady and growing need for emergency medical services (EMS) and safety-related missions is the important driver for civil and commercial helicopter market growth.

- For Instance, in December 2024, Airbus Helicopters reported that they have captured about 57% share of the civil and commercial market, which includes emergency services, and secured 450 net orders the highest since 2012 reflecting rising demand for rotorcraft deployed in public safety roles.

MARKET RESTRAINTS

High Operating and Maintenance Costs Associated with Helicopter Ownership and Operations Limit Market Expansion

Unlike fixed-wing aircraft, helicopters have complex rotor systems and engines that require frequent inspections, specialized parts, and highly trained technicians. Due to which it leads to high maintenance expenses. Additionally, fuel efficiency, pilot training, insurance premiums, and hangar or storage fees add to the financial burden for helicopter operators. Additionally, for many civil and commercial helicopter operators, especially in emerging economies, these costs make acquiring and using helicopters financially difficult. Resulting, when governments or private companies check the cost of helicopters for emergency medical services, offshore transport, or tourism, budget limits delay purchases or restrict fleet growth.

Furthermore, strict aviation safety and environmental regulations add extra costs since helicopter operators must meet emission standards, noise reduction rules, and safety upgrades. All these factors create barriers for smaller operators and slow down large-scale adoption, which limits overall commercial helicopter market growth despite growing demand.

- For Instance, The operation cost for a Robinson R22 Beta II light helicopter, including fuel, maintenance reserves, insurance, and other direct costs, is approximately USD 190 per hour based on 500 annual flight hours. For larger rotorcraft, hourly costs can range from USD 500 to USD 1,500 for light utility to midsize helicopters. Heavy-lift helicopters can cost up to USD 3,000 to USD 7,000 per hour.

MARKET OPPORTUNITIES

Technological Innovation and Expanding Applications Provide Strong Opportunities to Excel in Market

To excel in market major chance is integrating hybrid-electric and fully electric helicopters. These option have potential to lower operational costs, reduced emissions, and silent operations, which make them ideal choice for urban air mobility and environmentally friendly missions.

- For Instance, companies such as Airbus and Bell are already developing prototypes to take advantage of this shift.

Moreover, the growth of helicopter services in emerging markets such as Asia Pacific, Latin America, and Africa provide significant opportunity. Rising infrastructure development, offshore energy projects, and need for emergency medical service networks are rising demand in these areas. Tourism and aerial work, such as surveying, aerial firefighting, and agriculture, also present untapped market in these regions.

- For Instance, in June 2025, Joby Aviation took a significant step by delivering its first production eVTOL aircraft to Dubai, moving rapidly toward launching a commercial air taxi service in early 2026 under a six-year exclusive operating agreement with Dubai’s Road and Transport Authority.

Additionally, digitalization and predictive maintenance using AI and IoT are creating growth in service-related areas. Resulting boosting aftermarket revenue for original equipment manufacturers as well as makes helicopter operations more financially sustainable for smaller helicopter operators.

Download Free sample to learn more about this report.

Segmentation Analysis

By Number of Engines

Twin Engine Helicopters Dominated Market Owing to Application of this Helicopter in Various Sector

Based on number of engines, the Civil & Commercial Helicopter market segment is classified into single engine and twin engine.

The twin engine helicopter segment dominated the market and is expected to be the fastest growing segment during the forecast period. Due to their higher safety, reliability, and performance benefits compared to single-engine models. With two engines, helicopters can keep flying safely if one engine fails. This feature makes them the preferred choice for offshore oil and gas transport, emergency medical services (EMS), search and rescue (SAR), and VIP or corporate travel where safety rules are stringent. Their ability to fly in tough weather, at night, and over water or mountains also increases their demand in various sector. Resulting, as global demand for important and high-performance operations keeps growing, the twin-engine segment is expected to grow the fastest during the forecast period.

- For Instance, in March 2025, at Verticon 2025, Metro Aviation signed a deal with Airbus for up to 36 H140 helicopters. This new light twin-engine model is designed for emergency medical services. The agreement includes 12 firm orders and 24 options.

By Maximum Take-off Weight

Helicopters with less than 3,000 kg MTOW Dominates Market Owing to their Multipurpose Uses and Affordability

Based on maximum take-off weight, the market is divided into less than 3,000 kg (Light helicopters), 3,000 kg to 9,000 kg (Medium helicopters), and greater than 9,000 kg (Heavy helicopters).

The less than 3,000 kg segment holds the largest civil & commercial helicopter market share and is anticipated to grow with highest CAGR during the commercial helicopter market forecast period. Light helicopters are preferred choice as they are multipurpose, affordable, and can be used for many ways. They are ideal for emergency medical services, tourism, pilot training, aerial surveys, agriculture, and law enforcement. These helicopters have lower operational costs and better maneuverability than heavier models. Additionally, their lower price makes them appealing in emerging markets in Asia Pacific and Latin America. Resulting, governments and private helicopter operators are increasing helicopter fleets with MTOW less than 3,000 kg for public services and commercial use, fueling the segment growth.

- For Instance, in February 2025, Airbus single-engine H125 having standard maximum takeoff weight (MTOW) is 2,370 kg, known as the AStar in the U.S., remains the Airbus best-selling rotorcraft, with more than 150 sold in 2024 alone.

By Application

Corporate Services Segment Dominates Due to Businesses and Wealthy Individuals Depending More on Helicopters for Executive Travel, VIP Transport, and Intercity Trips

The market further is divided by application into emergency medical services (ems), corporate services, search and rescue operation, oil and gas, and others.

The corporate services segment dominates the market as businesses and wealthy individuals depend more on helicopters for executive travel, VIP transport, and intercity trips. Helicopters offer unmatched speed, flexibility, and accessibility. They are mainly useful in crowded urban areas and regions with few airports. Corporate users search for the ability to land close to business centers, offshore locations, or private properties, which cuts travel time and boosts productivity. Moreover, market is also driven by increasing luxury tourism, charter services, and urban air mobility projects that expand premium helicopter services. Resulting, with increasing corporate spending on efficient transport options and the availability of modern, quieter, and more comfortable helicopters, the corporate services segment is anticipated to continue dominate position in the market.

- For Instance, in May 2023, Italian business aviation operator Air Corporate ordered 43 helicopters from Airbus on the last day of EBACE 2023. The order includes 40 single-engine helicopters (H125/H130) and three ACH160s from Airbus Corporate Helicopters in Line configuration with the Lounge package. This adds to two ACH160s that are already on order.

By Point-of-Sale

Owing to its Cost-Effectiveness and Flexibility, Pre-Owned Segment Dominated Market

Based on point-of-sale, the market is segmented into new and pre-owned.

The pre-owned helicopter segment dominates the civil and commercial helicopter market by point-of-sale. This is mainly due to cost benefits, faster availability, and flexibility for operators compared to buying new models. Many operators, especially those in emerging markets or smaller fleet owners in EMS, tourism, agriculture, and law enforcement, consider pre-owned helicopters. Due to these helicopters provide access to reliable aircraft at lower acquisition costs while still meeting mission needs. Moreover, the presence of OEM-backed refurbishment programs, leasing options, and digital marketplaces has increased the appeal of used helicopters.

- For Instance, in June 2023, Rotortrade, the global leader in helicopter distribution, announced the sale of its 100th pre-owned Leonardo helicopter. As the only international distributor of Leonardo pre-owned helicopters, Rotortrade has a long-term agreement with Leonardo that runs until 2026.

Additionally, with a large global fleet aging and many operators shifting to newer twin-engine or more advanced models, the secondary market is thriving. As a result, pre-owned helicopters continue to be the leading segment by point-of-sale.

Civil & Commercial Helicopter Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East.

North America

North America Civil & Commercial Helicopter Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 26.55 billion in 2025, representing 54.62% of the global market landscape, and is expected to reach USD 28.71 billion in 2026. North America leads the market, with the U.S. having the largest fleet in the world. There is rising demand from EMS, law enforcement, corporate and VIP transport, and offshore oil and gas operations in the Gulf of Mexico. The U.S. also excels in adopting new technologies, including digital avionics and hybrid-electric helicopters. This growth is supported by a solid infrastructure and financing options.

- For Instance, in August 2024, The El Paso Fire Department signed a five-year contract with Air Methods to create Fire STAR (Shock and Trauma Air Rescue). This service will provide air medical transportation to improve the community's emergency medical response abilities.

Europe

Europe contributed 21.05% to the global market in 2025, with a valuation of USD 9.84 billion, and is projected to reach USD 10.84 billion in 2026. Europe is the second-largest market, driven by corporate services, EMS, and offshore energy activities in the North Sea. Major countries include France, Germany, the U.K., and Italy. The presence of key manufacturers including Airbus and Leonardo makes the region both a sourcing and purchasing center. There is a growing focus on green propulsion and quieter helicopters, which creates new opportunities.

- For Instance, in August 2024, ÖAMTC Air Rescue in Austria has received its 40th Airbus H135 helicopter. This addition strengthens its fleet for emergency medical services (EMS) and shows the continued need for helicopters in public safety.

Asia Pacific

Asia Pacific accounted for USD 6.21 billion in 2025, representing 15.46% of the global market share, and is projected to reach USD 6.92 billion in 2026. Asia Pacific is the fastest-growing region, spurred by improvements in infrastructure, tourism, offshore exploration, and EMS needs. China, India, Japan, and Australia are the main contributors. For instance, India is establishing its first private helicopter assembly line with Airbus-Tata to meet the increasing regional demand. Furthermore, fleet growth in China is speeding up due to urbanization and government investment in public services.

- For Instance, in May 2025, Airbus and Tata Advanced Systems (TASL) are starting India's first private helicopter assembly line in Karnataka in 2026. It will have an initial capacity of 10 helicopters each year. This facility, located in the Vemgal Industrial Area of Kolar, will make helicopters for India and neighboring countries. They plan to increase production to meet an expected regional demand of 500 light variants in the next twenty years.

Latin America

Latin America contributed approximately USD 3.4 billion to the global market in 2025, accounting for 3.24% share, and is expected to reach USD 3.77 billion in 2026. Latin America experiences steady growth, mainly driven by offshore oil and gas operations in Brazil, law enforcement in Mexico, and increasing tourism in Central and South America. Budget limitations lead operators to rely heavily on the used helicopter market, making affordable options a significant factor.

Middle East & Africa

In 2025, Middle East & Africa held 5.63% of the global market, reaching a valuation of USD 1.56 billion, and is projected to grow to USD 1.65 billion in 2026. The Middle East benefits from corporate and VIP demand, markets related to defense, and oil and gas operations, with the UAE and Saudi Arabia as key centers. Africa's growth is connected to resource exploration, EMS, and humanitarian efforts, though high costs and limited infrastructure continue to pose challenges.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Manufacturers are Directed Toward Technological Innovations and Fleet Modernization to Boost Market Growth

Airbus Helicopters is the leader, with a strong share in both light single-engine and twin-engine categories. Their top models, such as the H125, H135, and ACH160, are commonly used for EMS, tourism, and corporate services. Leonardo S.p.A. holds a strong position with its AW109, AW139, and AW169 platforms, especially in offshore transport and VIP/corporate services. Bell Textron is also a key competitor with its Bell 505, 407, and 429 models, which focus on versatility and cost-effectiveness. Sikorsky (Lockheed Martin) mainly focuses on defense but also provides platforms such as the S-76 and S-92 for offshore and corporate roles. Russian Helicopters, despite facing sanctions and geopolitical issues, still has a niche share in CIS and allied countries.

Technology innovation, fleet modernization, and pre-owned helicopter programs are reshaping the competitive landscape. Manufacturers are concentrating on eco-friendly propulsion, digital avionics, noise reduction, and predictive maintenance systems to set themselves apart. Meanwhile, the pre-owned helicopter market, led by companies such as Rotortrade in strategic partnerships with manufacturers such as Leonardo, has become an important growth area, especially in emerging regions where affordability matters.

LIST OF KEY CIVIL & COMMERCIAL HELICOPTERS COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Airbus Helicopters SAS (France)

- Leonardo Helicopters (Italy)

- Bell Helicopters (U.S.)

- Russian Helicopters (Rostec) (Russia)

- Hindustan Aeronautics Limited (HAL) (India)

- MD Helicopters (U.S.)

- Kawasaki Heavy Industries (Japan)

- Kaman Corporation (U.S.)

- The Robinson Helicopter Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In March 2025, Airbus Helicopters secured 118 commitments, including 63 firm orders, for its new H140 light twin helicopter at Verticon 2025, primarily from EMS operators such as Global Medical Response and ADAC Luftrettung.

- In August 2025, Airbus awarded Mahindra Aerostructures a contract to manufacture the main fuselage of the H125 at its Bengaluru plant, with the first delivery expected by 2027.

- In March 2024, The Helicopter Company (Saudi Arabia) signed agreements with Airbus and Leonardo for 38 firm orders and options for up to 210 helicopters. This includes H125s, H145s, AW139s, AW109s, AW169s, and AW189Ks.

- In March 2025, Leonardo received new orders for its AW169 platform. This includes three helicopters for offshore transport in China and three configured for EMS by Gama Aviation in the U.K.

- In January 2025, Sikorsky partnered with Blue Sky Network to equip S-70 Black Hawk helicopters with satellite-based communication and tracking systems for Search and Rescue (SAR) missions.

- In July 2024, NATO awarded Airbus, Leonardo, and Lockheed Martin contracts worth approx. USD 6.06 million each. These contracts are to conduct concept studies for the Next Generation Rotorcraft Capability (NGRC) program.

REPORT COVERAGE

The global helicopter market research report provides an in-depth technical analysis of the market, Civil & Commercial Helicopters market trends focusing on key aspects such as key players, market segments, and the impact of the Russia-Ukraine war, government bailout packages, and advancements in helicopter technologies. In addition, the report highlights aviation market trends, key industry developments, Civil & Commercial Helicopters market analysis and technological innovations driving demand. It also identifies factors contributing to commercial helicopter market growth during the helicopter market forecast period.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 1.78% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Number of Engines · Single Engine · Twin Engine |

|

By Maximum Take-off Weight (MTOW) · Less than 3,000 Kg · 3,000 Kg to 9,000 Kg · Greater than 9,000 Kg |

|

|

By Application · Emergency Medical Services (EMS) · Corporate Services · Search and Rescue Operation · Oil and Gas · Others |

|

|

By Point of Sale · New · Pre-Owned |

|

|

By Region · North America (By Number of Engines, Maximum Take-off Weight (MTOW), Application, Point of Sale, and Country) o U.S. (By Number of Engines) o Canada (By Number of Engines) · Europe (By Number of Engines, Maximum Take-off Weight (MTOW), Application, Point of Sale, and Country/Sub-region) o U.K. (By Number of Engines) o Germany (By Number of Engines) o France (By Number of Engines) o Italy (By Number of Engines) o Russia (By Number of Engines) o Rest of Europe (By Number of Engines) · Asia Pacific (By Number of Engines, Maximum Take-off Weight (MTOW), Application, Point of Sale, and Country/Sub-region) o China (By Number of Engines) o Japan (By Number of Engines) o India (By Number of Engines) o South Korea (By Number of Engines) o Australia (By Number of Engines) o Rest of Asia Pacific (By Number of Engines) · Latin America o Brazil (By Number of Engines) o Argentina (By Number of Engines) o Rest of Latin America (By Number of Engines) · Middle East & Africa o UAE (By Number of Engines) o Israel (By Number of Engines) o South Africa (By Number of Engines) · Rest of Middle East & Africa (By Number of Engines) |

Frequently Asked Questions

The global civil & commercial helicopters market size was valued at USD 47.55 billion in 2025. The market is projected to grow from USD 51.89 billion in 2026 to USD 59.76 billion by 2034, exhibiting a CAGR of 1.78% during the forecast period.

In 2025, the market value stood at USD 26.55 billion.

The market is expected to exhibit a CAGR of 1.78% during the forecast period of 2026-2034.

The Less than 3,000 Kg segment led the market by maximum take-off weight (MTOW).

Rising Demand for Emergency Medical Services (EMS) and Public Safety Operations are Driving the Market Growth

Lockheed Martin Corporation, Airbus Helicopters SAS, Leonardo Helicopters, Bell Helicopters, Russian Helicopters (Rostec) are the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 215

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us