Close-in Weapon Systems Market Size, Share & Industry Analysis, By System Type (Gun-Based, Missile-Based, Laser-Based, and Hybrid), By Platform (Land and Naval), By Range (Short Range (< 2 Km), Medium Range (2-9 Km), and Long Range (> 9 Km)), By Technology (Radar-Guided, EO/IR, Laser-Guided, Active & Passive Homing, and Hybrid), By Fit (OEM Fit and Retro-Fit), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

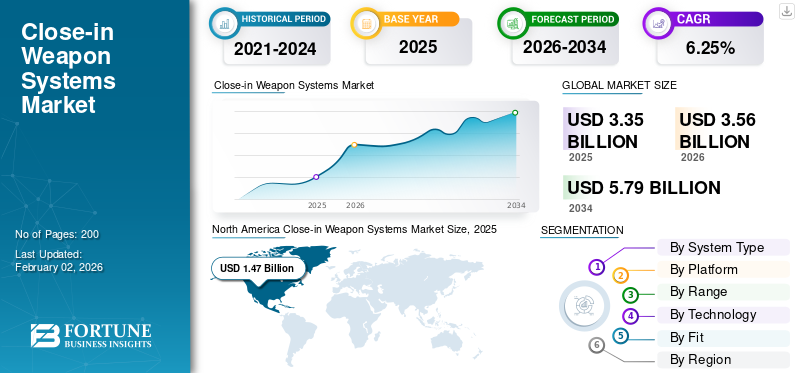

The global close-in weapon systems market size was valued at USD 3.35 billion in 2025 and is projected to grow from USD 3.56 billion in 2026 to USD 5.79 billion by 2034, exhibiting a CAGR of 6.25% during the forecast period.

Close-in Weapon Systems (CIWS) is a point defense weapon system designed to detect, track, and destroy incoming short-range threats, such as aircraft, missiles, and fast-attack craft, that have penetrated a warship's outer defense layers. These systems are either fully automated or semi-automated and use rapid-fire and missile-based weapon systems, integrating radar and electro-optical sensors for precise targeting.

Major players in the CIWS market include RTX Corp., Leonardo S.p.A., Thales Group, and Northrop Grumman, among others. These companies are driving the market growth by investing in next-generation CIWS systems with enhanced radar tracking, AI-assisted targeting, and missile integration capabilities. Rising defense spending, increasing naval modernization programs, and growing threats from drones and hypersonic weapons are encouraging these players to innovate and collaborate with military forces globally.

Download Free sample to learn more about this report.

Close-in Weapon Systems Market KEY TAKEAWAYS

- 2025 Market Size: USD 3.35 billion

- 2026 Market Size: USD 3.56 billion

- 2034 Forecast Market Size: USD 5.79 billion

- CAGR: 6.25% from 2026–2034

- North America dominated the market with a 41.16% share in 2025.

- Gun-based systems held a 45.45% share in 2026.

- Naval systems held a 68.30% share in 2026.

North America

North America held a 41.16% share, reaching USD 1.38 billion in 2025.

Europe

Europe accounted for 27.83% of the market, reaching USD 0.93 billion in 2025.

Asia Pacific

Asia Pacific held a 25.49% share, reaching USD 0.85 billion in 2025.

U.S.

The market is projected to reach USD 1.3 billion by 2026.

Japan

The market is projected to reach USD 0.13 billion by 2026.

Read More

Market Dynamics

Market Drivers

Rapid Modernization Rate of Naval Fleets and Increasing Geopolitical Tensions are Driving Market Growth

The CIWS market is primarily driven by the rapid modernization of naval fleets and the rising frequency of asymmetric and aerial threats. The U.S., China, India, and South Korea are expanding and upgrading their naval capabilities, leading to higher procurement of automated point defense systems. For instance, the U.S. DOD reported that the U.S. will be spending on naval systems is indeed projected to exceed USD 200 billion. This includes significant investments in shipbuilding, modernization, and new technologies such as CIWS and hypersonic missiles.

Increasing Need for Countering Evolving Threats is Further Boosting Market Growth

The CIWS market is witnessing significant development with the increasing threat of missile attacks, such as hypersonic missiles and rocket artillery. These weapons are lethal and can penetrate the defense layer in a minimum time, and with less effort. In such cases, CIWS plays a vital role in defending the vessels from such weapons. Moreover, increasing use of loitering munitions and saturation attacks from adversaries has necessitated advanced and reliable last-line defense systems.

For instance, Raytheon’s Phalanx systems are installed on over 450+ naval vessels and remain a top choice for over 25 navies globally. These systems can automatically search, detect, track, engage, and assess threats, making them a crucial last line of defense.

Market Restraints

High Development and Systems Integration Complexities Hinder Market Growth

Despite growing demand, the CIWS market faces restraints such as high acquisition and maintenance costs. For instance, a single unit of advanced CIWS such as Phalanx Block 1B can cost USD 10 to 15 million, excluding integration and maintenance. For smaller navies or developing nations, these costs pose a major barrier to widespread adoption. The challenge is compounded by the need for compatible shipboard integration, especially when modern systems must be retrofitted on older vessels.

Furthermore, maintaining CIWS systems requires skilled personnel and regular updates to software and sensors, which can burden logistics chains and budgets. Integrating with broader combat management systems is also complex, particularly for modular CIWS using both kinetic (guns) and missile interceptors. This technical barrier restricts deployment in some regions, especially where defense budgets are tightening.

Regulatory Framework and Export Controls Limit Market Expansion

Stringent regulations and export controls can limit the market by restricting the sale and transfer of these systems to certain countries, which affects companies operating in multiple regions or seeking to export their technology. Obtaining the necessary licenses and approvals for exporting CIWS can be time-consuming, leading to longer sales cycles and potentially delaying market expansion. Moreover, meeting the requirements of export control regulations adds complexity and cost to the sales process, potentially making it less attractive for some companies.

For instance, the U.S. has implemented export controls to restrict the transfer of certain advanced technologies, including those related to semiconductors and AI, to China, which can affect the CIWS market.

Market Opportunities

Demand from Emerging Economies for Modern CIWS Systems Provides Growth Opportunity

Significant opportunities lie in the increased defense spending by emerging economies such as India, Brazil, Indonesia, and Saudi Arabia, which are actively seeking to boost ship-based and land-based point defense systems. For instance, India’s naval budget rose by 15% in 2024, with a substantial portion allocated to the CIWS systems procurement and upgrades. Additionally, many of these nations are exploring indigenous development under offset and programs such as “Make-in-India”, which open partnership and co-development avenues for global CIWS manufacturers.

In November 2022, Larsen & Toubro (L&T) secured a weapon system contract to supply two units of a 40 mm naval gun system for the Indonesian Navy during the 2022 Indo Defense exhibition.

Nations are Focusing More on CIWS Technology with Counter-Drone Capabilities and are Adaptable to Asymmetric Warfare Tactics

Moreover, another opportunity lies in the counter-drone segment, where modern CIWS systems are being adapted to detect and destroy UAVs in swarms. CIWS, traditionally designed for anti-ship missile defense, are being integrated with counter-drone capabilities. This includes integrating radar, electronic warfare systems, and potentially laser or kinetic weapons to detect and neutralize threats from small unmanned aerial systems (sUAS).

In July 2024, Rheinmetall and Leonardo are developing advanced variants capable of engaging small, fast, low-flying threats using programmable airburst munitions and AI-enabled tracking, making CIWS a crucial asset not only for naval ships but also for land-based defense and critical infrastructure protection.

Close-in Weapon Systems Market Trends

Hybrid Gun and Missile Interceptors is a Major Trend in CIWS Market

The CIWS market is witnessing a trend toward hybrid systems combining gun and missile interceptors. For instance, RTX SeaRAM blends the radar and tracking system of the Phalanx with Rolling Airframe Missiles, offering layered close-in defense. This hybrid approach is becoming increasingly preferred for high-value assets and is influencing procurement decisions globally. Additionally, modularity and multi-role capabilities are emerging as key selling points in both land and maritime platforms.

In August 2024, the U.S. Department of Defense awarded an RTX contract worth USD 159.9 million to upgrade the U.S. Navy's MK 15 CIWS. Raytheon will supply MK 15 Mod 31 SeaRAM upgrade kits and associated hardware to the service branch over three years.

Integration of AI and ML to Increase Accuracy and Reduce Human Error

Another strong trend is the integration of AI and sensor fusion into CIWS platforms. Modern systems are using AI to reduce human reaction time, enhance threat prioritization, and improve hit probability even in cluttered environments. Firms such as Northrop Grumman and Thales, which allow autonomous threat engagement and improved situational awareness, are now developing AI-enhanced fire control systems. As a result, the market is expected to grow at a CAGR of 6.4% through 2032, with smart, AI-enabled systems leading the evolution.

Download Free sample to learn more about this report.

Impact of Increasing Geopolitical Tensions, Ongoing, and Recent Conflicts in Europe, Middle East, and Asia Pacific

Rising Geopolitical Tensions and Regional Conflicts are Significantly Accelerating Demand for CIWS

CIWS, being critical for last-line defense, are becoming important assets on modern warships and high-value land-based assets. For instance, global military expenditure reached a record USD 2.4 trillion in 2024, with a substantial portion dedicated to air and missile defense. Moreover, rising tension amongst countries is rising demand for defense weapons thus will facilitate the close-in weapons system growth.

China's growing military presence and assertive actions in the South China Sea are prompting nations, including Japan, South Korea, and the Philippines, to invest in CIWS and other defense capabilities. Moreover, some nations in the region face some border tensions due to a complex mix of historical grievances, unresolved territorial disputes, competition for resources, and rising nationalism, which further fuels the demand for land-based CIWS.

In January 2025, Korea Bizwire news agency in South Korea reported that South Korea has begun developing a land-based adaptation of its Close-In Weapon System (CIWS-II) to address North Korean threats, including artillery, drones, ballistic missiles, and cruise missiles. The Defense Acquisition Program Administration (DAPA) is managing the project, building on the naval CIWS-II equipped with a 30mm GAU-8 Gatling gun and Active Electronically Scanned Array (AESA) radar.

The war in Ukraine has demonstrated the importance of CIWS in defending against missile and drone attacks, leading to increased procurement and development of these systems by both Ukraine and NATO members. For instance, United 24, a government organization in Ukraine, reported that since February 2024, the Russian army has launched more than 4,500 missiles at Ukraine, 20% of them coming from the sea. This implies the importance of CIWS in both the sea and on land to safeguard the nation's borders and strategic locations.

The ongoing conflict between Israel and Iran, as well as the conflict with Hamas, has highlighted the need for robust missile defense systems, including CIWS, to protect against missile and drone attacks. The conflict is also driving regional arms races. In January 2025, DCX Systems received an export order from Israel's Elta Systems Ltd. This contract involves the manufacture and supply of Close-In Weapon System (CIWS) module assemblies.

In conclusion, emerging conflicts and grey-zone warfare have prompted rapid procurement and upgrades of CIWS across both NATO and non-NATO countries. The Russia-Ukraine war has led eastern European nations to fast-track missile defense programs, while China’s increasing assertiveness in Indo-Pacific waters is prompting Japan, South Korea, and India to strengthen their naval CIWS capabilities.

SEGMENTATION ANALYSIS

By System Type

Gun-Based Systems Dominate with their Proven Reliability and Rapid Response Capabilities

The market is segmented by the system type into gun-based, missile-based, laser-based, and hybrid.

The gun-based systems segment is projected to dominate the market with a share of 45.45% in 2026, due to its proven reliability, rapid response capabilities, and relatively lower cost compared to missile-based systems. These systems, often featuring Gatling guns, are known for their high firing rate and effectiveness against various threats, including short-range missiles and aircraft. Moreover, gun-based CIWS can be adapted to various platforms and scenarios, including naval vessels, ground-based installations, and even some airborne applications.

For instance, in September 2022, Raytheon Missiles & Defense was awarded a USD 49.05 million firm-fixed-price contract for the procurement of four MK-15 CIWS (gun-based CIWS) Block 0 to Block 1B Baseline 2 Upgrade, Conversion, and related equipment for the Republic of Korea.

The hybrid segment is anticipated to show the fastest growth with the highest CAGR during the forecast period. Hybrid systems' ability to combine the capabilities of both gun-based and missile-based systems, offering an adaptable defense against a wider range of threats. Furthermore, the integration of CIWS with advanced defense technologies, including directed energy weapons and AI-driven targeting systems, is driving the adoption of hybrid systems. Moreover, this segment is also gaining traction as it addresses the limitations of relying solely on either guns or missiles for close-range defense.

By Platform

Increasing Deployments of CIWS on Naval Vessels to Enhance Defense Against Aerial Threats in Maritime Environments

Based on platform, the market is bifurcated into land and naval.

The naval segment is projected to dominate the market with a share of 68.30 in 2026, the CIWS market and is anticipated to be the fastest-growing segment during the forecast period. The dominance of the segment is due to its increasing deployments of CIWS on naval vessels for enhanced defense against aerial threats in maritime environments and rising geopolitical tensions, and advancements in AI and improved targeting systems. Additionally, navies are actively replacing older, less capable CIWS with newer, more advanced systems, driving demand for modern, technologically superior solutions.

The land segment is expected to experience steady growth from 2025 to 2032. This is due to surging threats from UAVs, loitering munitions, and short-range missiles targeting military bases, critical infrastructure, and mobile ground units. As drone warfare and low-cost aerial attacks increase, militaries are deploying mobile and stationary CIWS units to protect airbases, forward operating bases, and radar stations. For instance, South Korea and the U.S. are investing heavily in land-based solutions, such as C-RAM systems.

In January 2025, South Korea’s development of a land-based Close-In Weapon System (CIWS-II) marked a significant step in enhancing its defense capabilities against North Korean threats. This new adaptation builds upon the existing naval CIWS-II, integrating a 30mm GAU-8 Gatling gun and AESA radar.

By Range

Increasing Demand for Modern Hybrid Systems that Combine Guns with Missiles or Advanced Interceptors Drives Mid-Range Segment

In terms of range, the market is divided into Short Range (< 2 Km), Medium Range (2-9 Km), and Long Range (> 9 Km).

The mid-range (2-9Km) CIWS is anticipated to be the fastest growing segment with the highest CAGR during the forecast period. The growth is driven by modern hybrid systems that combine guns with missiles or advanced interceptors. Systems including SeaRAM, C-Dome, and Pantsir-ME fall into this category, offering increased reaction time and the ability to neutralize threats such as anti-ship missiles, drones, and swarming attacks at a safer distance. Moreover, the demand is rising due to evolving threats that require interception before reaching the target.

The short range (>2km) segment is projected to dominate the market with a share of 44.08% in 2026. This includes traditional short-range gun-based CIWS such as the Phalanx, AK-630, and Type 730, which are highly reliable for last-layer defense. Due to their mature technology, proven combat effectiveness, and widespread deployment on naval platforms, this segment currently dominates the CIWS market, especially in retrofit programs.

For instance, in August 2023, Navantia officially announced its proposal to provide the Rheinmetall Oerlikon Millennium Gun 35mm Close-In Weapon System (CIWS) for the Philippine Navy’s upcoming CIWS requirement worth USD 91.55 million.

By Technology

Hybrid Guidance Systems are Anticipated to Drive Market Growth by Offering Guidance for Layered Detection and Neutralizing Threats

Based on technology, the market is sectioned into radar-guided, EO/IR, laser-guided, active & passive homing, and hybrid.

Hybrid guidance systems are projected to be the fastest-growing segment, with the highest CAGR, during the 2025-2032 period. The hybrid system combines radar, EO/IR, and missile guidance for layered detection and engagement. Hybrid systems are gaining traction as threats become faster, stealthier, and multi-vector. However, not yet dominant, this segment is evolving fast in advanced naval programs and may become a dominating segment by the forecast period.

For instance, AK630M and AK630 close-in weapon systems featuring the hybrid systems (Radar-Guided and Electro-Optical/Infrared (EO/IR)) have been installed on 500+ vessels globally.

Radar-Guided CWIS systems segment is projected to dominate the market with a share of 42% in 2026, with the most widely deployed and trusted systems globally, offering all-weather, high-speed tracking and engagement capabilities. Systems including Phalanx, Goalkeeper, and Kashtan rely heavily on the radar-based fire control, making this segment dominant due to its proven reliability, integration with combat management systems, and strong record of achievement in naval and ground defense forces.

Moreover, in February 2024, India’s local news agency reported that Gun & Shell Factory (GSF) Cossipore, a subsidiary of Advanced Weapons and Equipment India Limited (AWEIL) Kanpur, is going to build a dozen 30-mm AK-630M naval guns indigenously. The contract has been signed with Cochin Shipyard Limited for the indigenous production and supply of twelve 30-mm AK-630M naval guns, which will be installed in the Next Generation Missile Vessels (NGMV).

By Fit

Cost-Effectiveness and Ability to Improve Capabilities of Existing Naval Vessels Drive Demand for Retrofit Segment

By fit, the market is classified into OEM fit and retrofit.

The retrofit segment dominates and is anticipated to witness the fastest-growth during the forecast period. The cost-effectiveness and ability to improve the capabilities of existing naval vessels, resulting in the segment’s dominance. Retrofitting allows for the integration of advanced technology such as upgraded sensors, fire control systems, and faster-firing weapons on ships that are already in service, without the need to build entirely new platforms. This approach is particularly appealing to many countries, including NATO allies, as it allows them to address modern threats without the high cost and time associated with new construction. Moreover, an aged naval fleet requires the retrofit of advanced systems such as CWIS to tackle the modern threats.

OEM fit holds a significant share of the close-in weapon systems market. As militaries modernize their fleets of ships, aircraft, and ground vehicles, there is a strong demand for CIWS that are designed and integrated as part of the initial platform build. This allows for optimal performance, streamlined logistics, and a more cohesive defensive system.

Close-in Weapon Systems Market Regional Outlook

The CIWS market is studied across North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Close-in Weapon Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 1.38 billion in 2025, representing 41.16% of the global market landscape, and is expected to reach USD 1.47 billion in 2026. The rise in the adoption of next-generation CIWS and R&D on advanced tracking and guiding technology by key regional manufacturers is anticipated to fuel close-in weapon systems market growth in North America. The U.S. market is projected to reach USD 1.3 billion by 2026.

Moreover, the U.S. is increasing the federal budget for military procurement plans for all military platforms, such as air, sea, and land, which is leading to the market’s growth. Moreover, the region has a presence of key players such as RTX, Northrop Grumman, and Lockheed Martin.

For instance, in August 2023, the U.S. Department of Defense awarded Raytheon a USD 279.2 million contract to provide management support for the Army's Land-Based Phalanx Weapon System.

Europe

Europe is predicted to show significant growth during the forecast period and is also a hub for technological innovation in defense, with advancements in radar, sensor technologies, and weapon control systems contributing to the development of more efficient and capable CIWS. The increasing adoption of close-in weapons systems in the land-based segment for various threat protection applications across Germany, France, Ukraine, Russia, the Netherlands, and the U.K., is projected to support the market growth in Europe. The UK market is projected to reach USD 0.21 billion by 2026, and the Germany market is projected to reach USD 0.18 billion by 2026. Europe contributed 27.83% to the global market in 2025, with a valuation of USD 0.93 billion, and is projected to reach USD 0.99 billion in 2026.

In March 2024, it was announced that a contract worth USD 88.77 million had been signed between Aselsan and the Turkish Defense Industry Agency for the procurement of CIWS. Deliveries under the contract are scheduled to take place between 2024 and 2027.

Asia Pacific

Asia Pacific is expected to show the fastest growth with the highest CAGR during the forecast period. China, India, and Japan are actively investing heavily in retrofitting modern CIWS in their existing naval fleets, further contributing to the growth of the market. Moreover, some countries in the region are also focusing on developing and manufacturing their own close-in weapon systems, through various programs such as the “Make in India” program, reducing reliance on foreign suppliers and fostering technological independence. The Japan market is projected to reach USD 0.13 billion by 2026, the China market is projected to reach USD 0.3 billion by 2026, and the India market is projected to reach USD 0.21 billion by 2026. Asia Pacific accounted for USD 0.85 billion in 2025, representing 25.49% of the global market share, and is projected to reach USD 0.91 billion in 2026.

In March 2024, the Defense Ministry of India contracted L&T worth USD 925.0 million for the procurement of the Close-in Weapon System (CIWS). The CIWS is intended to offer terminal Air Defense to specific locations within the country.

In December 2020, the State Department approved a possible Foreign Military Sale to the Republic of Korea of two MK 15 MOD 25 Phalanx Close-In Weapons Systems (CIWS) Block 1B Baseline 2 systems and related equipment for an estimated cost of USD 39 million.

Rest of the World

The Middle East & Africa and Latin America further divide the rest of the world segment.

The Middle East & Africa region experiences frequent conflicts and tensions, necessitating robust defense systems to protect against missile attacks and other threats. Many countries, including Saudi Arabia, Israel, and others in the region, are investing in military modernization, including upgrading their naval capabilities with CIWS. In 2025, Middle East & Africa held 5.52% of the global market, reaching a valuation of USD 0.19 billion, and is projected to grow to USD 0.2 billion in 2026.

Latin America has long coastlines and exclusive economic zones that necessitate robust naval defenses, including CIWS, to protect maritime interests and enforce international norms. Several Latin American countries are modernizing their navies, including the acquisition and integration of CIWS.

Competitive Landscape

Key Industry Players

Top Companies Emphasize Technological Advancements and Strategic Partnerships to Maintain their Dominance

The close-in weapon systems market is characterized by a competitive landscape featuring key players such as RTX Corporation, Thales Naval, Rheinmetall, Norinco, and others. Key players focus on growing investment in research and development, a diversified product portfolio of CWIS systems, and strategic acquisitions. The key market players focus on long-term retrofitting and modernization contracts with multinational companies included in the market.

These companies are leveraging advanced technologies, including AI and autonomous integration, enhanced sensor technology, and improved munitions to enhance the effectiveness of their detection, tracking, and identification of objects or targets such as loitering munitions, drones, and hypersonic missiles. Overall, the focus on technological integration with AI, directed energy weapons, and advanced radar systems will drive significant growth in the close-in weapon systems market over the coming years.

LIST OF KEY CLOSE-IN WEAPON SYSTEM COMPANIES PROFILED:

- RTX Corporation (U.S.)

- Breda and Oto Melara (Italy)

- Thales Naval (Thales Group) (France)

- Tulamashzavod (Russia)

- Rheinmetall (Germany)

- General Dynamics Corporation (U.S.)

- Norinco (China)

- Aselsan (Turkey)

- Lockheed Martin (U.S.)

- FABA Sistemas (Poland)

- BAE Systems (U.K.)

- Leonardo S.p.A (Italy)

- L&T (India)

- Northrop Grumman (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In July 2025, South Korean firm LIG Nex1 launched a new facility worth USD 15.3 million to increase advanced Close-In Weapon System (CIWS-II) manufacturing in the provision of the country’s air defense competencies. The site, situated in the eastern Gyeongsangbuk-do area, is a proximity evaluation laboratory.

- In August 2023, the Taiwanese Navy installed the latest variant of Phalanx Close-In Weapon System (CIWS) into its main surface combatants to improve their ability to take out incoming threats. According to a local news agency, the Taiwanese Navy has spent approximately USD 313 million for the significant lethality upgrade.

- In March 2023, the U.S. DOD awarded Raytheon Missiles and Defense, a contract worth USD 113.63 firm-fixed-price modification for MK 15 close-in weapon system (CIWS) upgrades and conversions, system overhauls, and associated hardware.

- In October 2023, the U.K. defense agencies awarded Babcock International a three-year contract worth USD 18.91 million to continue providing critical support for the Royal Navy’s Phalanx Close-In Weapon Support System (CIWS).

- In February 2022, the U.S. Naval Surface Warfare Center Indian Head Division awarded Serco a contract worth USD 64 million, single-award, indefinite-delivery, indefinite-quantity (IDIQ). The contract has a five-year ordering period, where Serco will deploy, modernize, and modify the Close-In Weapon Systems (CIWS).

- In January 2022, the U.S. awarded Herndon a USD 64.41 million firm-fixed price, cost-plus-fixed-fee, indefinite-delivery/indefinite-quantity contract (N00174-22-D-0006) for the Close-In Weapons System (CIWS) Alteration Installation Team (AIT).

REPORT COVERAGE

The research report delivers a detailed analysis of the market and emphasizes key aspects such as key players, and offerings in close-in weapon systems. Moreover, the report deals with insights into market trends, competitive landscape, market competition, product pricing, regional analysis, market players, competition landscape, and the market status, and highlights key industry growth. In addition to the factors stated above, the report encompasses several direct and indirect influences that have subsidized the sizing of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.25% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By System Type

|

|

By Platform

|

|

|

By Range

|

|

|

By Technology

|

|

|

By Fit

|

|

|

By Region

|

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 3.56 billion in 2026 and is anticipated to be USD 5.79 billion by 2034.

The market will likely grow at a CAGR of 6.25% over the forecast period (2026-2034).

The top players in the industry are RTX Corporation, Breda and Oto Melara, Thales Naval, Tulamashzavod, Rheinmetall, General Dynamics Corporation, Norinco, Aselsan AS, Lockheed Martin, FABA Sistemas, BAE Systems, Leonardo S.p.A, L&T, and Northrop Grumman based on parameters such as services portfolio, regional presence, and industry experience.

North America dominated the global close-in weapon systems market in 2025, with USD 1.38 billion.

The rapid modernization rate of naval fleets and increasing geopolitical tensions are driving the market growth.

Manufacturing of hybrid weapon systems is the latest trend in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us