Cloud Sustainability Market Size, Share & Industry Analysis, By Solution (Carbon Footprint Management, Sustainable Cloud Optimization, and Green Cloud Infrastructure), By Deployment (Public Cloud, Private Cloud, and Hybrid Cloud), By Enterprise Type (Large Enterprises and Small & Medium Enterprises (SMEs)), By End-user (IT & Telecom, BFSI, Healthcare, Retail, Manufacturing, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

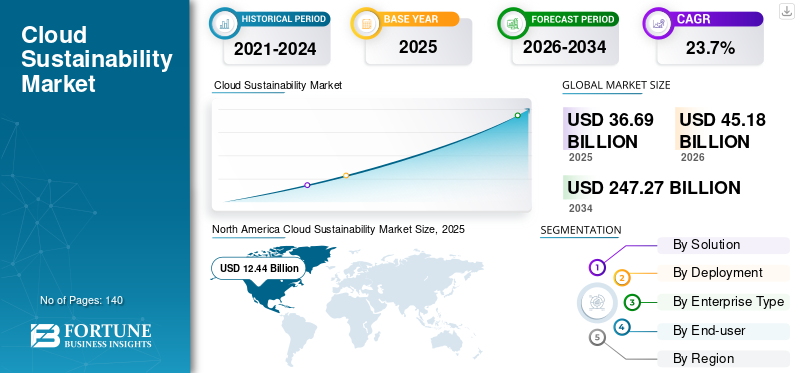

The global cloud sustainability market size was valued at USD 36.69 billion in 2025. The market is projected to grow from USD 45.18 billion in 2026 to USD 247.27 billion by 2034, exhibiting a CAGR of 23.7% during the forecast period. North America dominated the cloud sustainability market with a market share of 33.90% in 2025.

The global cloud sustainability market encompasses solutions and services, including carbon footprint management, sustainable cloud optimization, and green cloud infrastructure, delivered across public, private, and hybrid cloud environments to help enterprises mitigate the environmental impact of their cloud operations. It is used by large enterprises and small & medium enterprises (SMEs) across various sectors, including IT & telecom, BFSI, healthcare, retail, manufacturing, and government, to measure, manage, and minimize cloud-related energy use and emissions.

The market is driven by increasing climate reporting requirements, energy cost pressures, the growing use of AI and ML for environmental operations, and stronger enterprise demand for sustainable cloud infrastructure. Key companies operating in the market include Amazon Web Services, Inc., Microsoft Azure, Google LLC, IBM Corporation, Oracle Corporation, SAP SE, Salesforce, Inc., Dell Technologies Inc., Equinix, Inc., and Nutanix, Inc.

Download Free sample to learn more about this report.

Cloud Sustainability Market Key Takeaways

- 2025 Market Size: USD 36.69 billion

- 2026 Market Size: USD 45.18 billion

- 2034 Forecast Market Size: USD 247.27 billion

- CAGR: 23.7% from 2026–2034

- North America dominated the cloud sustainability market with a market share of 33.90% in 2025.

- Carbon Footprint Management is expected to grow at the maximum CAGR of 25.3%.

- The hybrid cloud is projected to grow at the highest CAGR of 25.2%.

North America

North America led the market with a value of USD 12.44 billion in 2025, supported by strong cloud adoption, advanced digital infrastructure, and growing net-zero commitments.

Europe

Europe accounted for the second-largest market share, driven by stringent environmental regulations and increasing investments in sustainable cloud operations.

Asia Pacific

Asia Pacific is anticipated to record the highest CAGR during the forecast period due to rapid digital transformation, expanding data center infrastructure, and rising sustainability initiatives.

U.S.

The country remains a major contributor to market growth, supported by hyperscale cloud investments, renewable energy adoption, and increasing focus on ESG compliance.

Japan

Growing cloud migration initiatives, energy-efficiency programs, and corporate sustainability goals are accelerating demand for cloud sustainability solutions across the country.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growing Enterprise Focus on Net-Zero and ESG Targets Accelerates Adoption of Cloud Sustainability Practices

The surging enterprise commitment to net-zero and ESG goals is a key factor accelerating the adoption of cloud sustainability solutions. For instance,

- According to the NewClimate Institute’s Net Zero Stocktake 2025, 63% of publicly listed companies globally have set net-zero targets, representing approximately USD 36.6 trillion in annual revenue.

Organizations across sectors are increasingly prioritizing carbon neutrality and environmental accountability, prompting greater investments in tools that measure and optimize cloud-related emissions. This shift is further reinforced by internal sustainability mandates and stakeholder expectations, which require companies to demonstrate measurable progress toward climate targets. As a result, enterprises are leveraging cloud sustainability platforms to align their digital operations with long-term ESG strategies and regulatory compliance requirements.

MARKET RESTRAINTS

High Implementation Complexity and Limited Standardization Constrain Market Expansion

A key restraint in the cloud sustainability market is the high complexity involved in integrating carbon measurement and optimization tools across diverse cloud environments. Many organizations struggle with inconsistent data sources, fragmented systems, and differing methodologies for calculating cloud-related emissions. This challenge is further amplified by the lack of globally accepted standards for cloud carbon accounting, which creates uncertainty and slows adoption. As a result, enterprises delay or limit investments in cloud sustainability solutions due to perceived technical and operational burdens.

MARKET OPPORTUNITIES

Rising Demand for Sustainability-Focused Cloud Services Among SMEs Creates Market Opportunities

A significant opportunity in the cloud sustainability market lies in expanding tailored solutions for small and medium-sized enterprises (SMEs). While large enterprises have been early adopters of ESG-driven cloud initiatives, many SMEs are only beginning to formalize their sustainability strategies and lack in-house expertise or tools. For instance,

- According to The Institute of Chartered Accountants in England & Wales, only 8% of SMEs currently report on sustainability issues, indicating a large underserved market for tailored sustainability solutions.

Vendors can capitalize on this gap by offering simplified, cost-effective, and pre-configured cloud sustainability packages that bundle carbon tracking, optimization, and reporting capabilities. This segment represents a sizable untapped customer base, creating scope for scalable, subscription-based offerings that drive both market growth and broader adoption of sustainable cloud practices.

CLOUD SUSTAINABILITY MARKET TRENDS

Growing Adoption of Carbon-Aware Cloud Management and Real-Time Emissions Monitoring Fuels New Market Trends

The increasing integration of carbon-aware workload management and real-time emissions monitoring within cloud platforms drives the cloud sustainability market growth. For instance,

- According to industry experts, by 2026, 50% of organizations will adopt sustainability-enabled monitoring to reduce energy consumption and carbon footprint metrics for their hybrid cloud

Cloud providers and enterprises are embedding dashboards and analytics that quantify energy consumption and associated carbon output at the workload, application, and business-unit level. This capability enables IT teams to shift workloads across regions, time periods, or infrastructure types based on the relative carbon intensity of power sources, rather than solely on cost. As a result, organizations are moving from static sustainability reporting to continuous, data-driven optimization of their cloud environments.

Segmentation Analysis

By Solution

Green Cloud Infrastructure Dominates Owing to Growing Demand for Sustainable Data Centers

Based on the solution, the market is divided into carbon footprint management, sustainable cloud optimization, and green cloud infrastructure.

Green cloud infrastructure holds the largest share, as organizations prioritize green data centers, renewable-powered facilities, and optimized hardware as the foundational step to reducing the environmental impact of cloud operations. Moreover, major cloud providers have already made substantial capital expenditures (capex) investments in green infrastructure, resulting in large, recurring revenue streams from existing enterprise workloads.

Carbon Footprint Management is expected to grow at the maximum CAGR of 25.3% as enterprises increasingly seek granular visibility into Scope 2 and cloud-related Scope 3 emissions to meet regulatory disclosure and ESG reporting requirements. The growing need for automated tracking, benchmarking, and audit-ready sustainability data is driving the accelerated adoption of advanced carbon accounting and analytics platforms.

By Deployment

Public Cloud Dominates the Market Growth Owing to Mature Energy-Efficient Infrastructure

Based on the deployment, the market is separated into public cloud, private cloud, and hybrid cloud.

Public cloud leads the market as hyperscale providers offer mature, globally distributed, and energy-optimized infrastructure that enables rapid, low-cost access to sustainable computing resources. Enterprises also perceive public cloud as an effective way to consolidate workloads from inefficient on-premise environments, thereby improving both cost and carbon performance.

The hybrid cloud is projected to grow at the highest CAGR of 25.2% as organizations adopt mixed environments to balance regulatory, data residency, and latency needs while still leveraging the capabilities of green public clouds. This model allows enterprises to progressively modernize legacy on-premise systems and integrate sustainability controls across both private and public environments, driving faster incremental adoption.

By Enterprise Type

Large Enterprises Dominate the Market Development Owing to Higher IT Spending and ESG Priorities

Based on the enterprise type, the market is divided into large enterprises and small & medium enterprises (SMEs).

Large enterprises hold the maximum share due to their higher IT spending capacity, complex global operations, and stronger pressure from regulators, investors, and customers to demonstrate ESG progress. These organizations are early adopters of sustainability-focused cloud transformation programs and typically engage in long-term, high-value contracts with cloud providers.

SMEs are expected to record the highest CAGR of 25.3% as cloud-native, subscription-based sustainability tools become more affordable and easier to deploy, eliminating the need for extensive in-house expertise. Growing awareness of regulatory expectations and supply-chain sustainability requirements is prompting SMEs to adopt lightweight solutions for emissions tracking and green cloud optimization.

By End-user

To know how our report can help streamline your business, Speak to Analyst

IT and Telecom Segment Dominates the Market Owing to High Cloud Usage and Early Sustainability Adoption

The end-user market is segmented into IT & telecom, BFSI, healthcare, retail, manufacturing, and other sectors.

IT & Telecom holds the highest share because this sector operates large-scale data centers and network infrastructure, making it both a major consumer of cloud resources and an early adopter of efficiency and decarbonization initiatives. Service providers are increasingly embedding sustainability as a differentiator in their cloud and connectivity offerings, further expanding demand within this segment.

Manufacturing is expected to post the highest CAGR of 27.2% as smart factories, IoT, and digital twin adoption increase reliance on energy-efficient cloud infrastructure. Rising pressure to decarbonize operations and supply chains further accelerates the adoption of sustainable cloud.

Cloud Sustainability Market Regional Outlook

By region, the market is categorized into North America, South America, Europe, Middle East & Africa, and Asia Pacific.

North America

North America Cloud Sustainability Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America dominates the cloud sustainability market owing to its high cloud adoption rate, presence of hyperscale data centers, and strong concentration of leading cloud providers and technology vendors. Enterprises in the region are early adopters of ESG frameworks and net-zero commitments, which drives substantial investment in green cloud infrastructure and carbon management tools. In addition, U.S. supportive regulatory discussions, access to renewable energy sources, and mature digital ecosystems further reinforce North America’s leading position in the market.

Download Free sample to learn more about this report.

Europe

Europe holds the second-largest cloud sustainability market share due to its stringent environmental regulations, including EU-wide climate targets and disclosure requirements that compel organizations to decarbonize their IT operations. Enterprises in key markets, including Germany, the U.K., and the Nordics, are proactively implementing sustainable cloud strategies to comply with regulatory, investor, and societal expectations. The region’s strong policy focus on energy efficiency and renewable integration supports steady demand for cloud sustainability solutions.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

The Asia Pacific region is expected to grow at the highest CAGR, driven by rapid cloud adoption, accelerating digital transformation, and large-scale data center expansion across countries such as China, India, Japan, and Southeast Asia. Governments and enterprises are increasingly prioritizing energy efficiency and emissions reduction as power demand from digital infrastructure continues to rise. As organizations in the region transition from traditional IT to cloud-first models, they are adopting sustainability-focused solutions to manage costs and comply with emerging environmental regulations.

Middle East & Africa, and South America

Middle East & Africa, and South America are expected to grow at a significant rate as cloud infrastructure investments accelerate and regional data centers increasingly integrate renewable energy and efficiency measures. Governments and large enterprises in these regions are beginning to adopt formal ESG agendas, which include decarbonizing their IT operations and enhancing transparency regarding emissions. Rising digitalization, coupled with greenfield cloud deployments that can be designed with sustainability principles from the outset, creates substantial headroom for future market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Launch New Products Using Technological Advancements to Strengthen Market Position

Players launch new products to enhance their market positioning by leveraging technological advancements, addressing diverse consumer needs, and staying ahead of competitors. They prioritize portfolio enhancement and strategic collaborations, as well as acquisitions and partnerships, to strengthen their offerings. Such strategic launches enable the technology companies to maintain and expand their market share in a rapidly evolving landscape.

LIST OF KEY CLOUD SUSTAINABILITY COMPANIES PROFILED

- Amazon Web Services, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Google LLC (U.S.)

- IBM Corporation (U.S.)

- Oracle Corporation (U.S.)

- SAP SE (Germany)

- Salesforce, Inc. (U.S.)

- Dell Technologies Inc. (U.S.)

- Equinix, Inc. (U.S.)

- Nutanix, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In November 2025, Tata Consultancy Services (TCS) launched Team SDG Universe, an interactive digital platform designed to educate children on the United Nations’ 17 Sustainable Development Goals (SDGs). This free, story-driven resource aims to help younger audiences understand, appreciate, and adopt sustainability-focused principles.

- In November 2025, Fujitsu, in collaboration with AWS Japan, established a business creation lab to advance joint innovation under their global strategic collaboration agreement. The lab combines Fujitsu’s industry expertise with AWS’s generative AI and cloud capabilities to help Japanese retail and service-sector customers modernize legacy systems and unlock new revenue opportunities.

- In June 2025, Salesforce launched Agentforce for Net Zero Cloud, a unified data-driven platform intended to support teams in meeting sustainability compliance requirements. The solution enables organizations to reduce their environmental impacts by providing integrated sustainability insights.

- In May 2025, Microsoft introduced a suite of new solutions and capabilities designed to help Azure users incorporate sustainability considerations into their cloud migration strategies. These enhancements also enable organizations to more effectively manage and reduce the carbon footprint associated with their cloud usage.

- In April 2025, Accenture expanded its strategic relationship with Google Cloud through the launch of new capabilities presented at Cloud Next ’25. These offerings aim to help organizations scale advanced cloud and AI technologies, thereby accelerating their digital transformation.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 23.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Solution, By Deployment, By Enterprise Type, By End-user, and By Region |

| By Solution |

|

| By Deployment |

|

| By Enterprise Type |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 36.69 billion in 2025 and is projected to reach USD 247.27 billion by 2034.

In 2025, the market value stood at USD 12.44 billion.

The market is expected to exhibit a CAGR of 23.7% during the forecast period of 2026-2034.

The green cloud infrastructure led the market in terms of solution.

The growing enterprise focus on net-zero and ESG targets accelerates the adoption of cloud sustainability solutions.

Amazon Web Services, Inc., Microsoft Corporation, and Google LLC are some of the prominent players in the market.

North America dominated the market in 2025.

Key factors include rising ESG commitments, stricter climate reporting standards, cost pressures from energy consumption, and the growing use of artificial intelligence and machine learning to automate carbon tracking and deliver more environmentally responsible cloud operations.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us